|

|

市場調査レポート

商品コード

1406191

ポリエチレンフラノエート(PEF):市場シェア分析、産業動向と統計、2024~2029年の成長予測Polyethylene Furanoate (PEF) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

|

|

|||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ポリエチレンフラノエート(PEF):市場シェア分析、産業動向と統計、2024~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

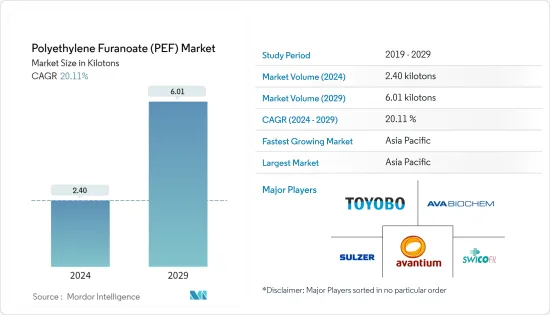

ポリエチレンフラノエート(PEF)市場規模は2024年に2.40キロトンと推定され、2029年には6.01キロトンに達し、予測期間(2024-2029年)のCAGRは20.11%で成長すると予測されます。

市場はCOVID-19によりマイナスの影響を受けました。COVID-19の大流行により、ウイルスの蔓延を抑えるために世界のいくつかの国が閉鎖状態に入りました。数多くの企業や工場が操業停止となったことで、世界の供給網が混乱し、世界の生産、納期、製品販売に打撃を与えました。現在、市場はCOVID-19の大流行から回復し、大幅に増加しています。

主なハイライト

- 市場を牽引している主な要因は、ボトル製造用ポリエチレンフラノエート需要の増加と繊維分野の需要増です。

- その反面、バイオPET、バイオPE、バイオPPなど他のバイオプラスチックの存在と原料の入手不可能性が市場成長の妨げになると予想される主な抑制要因です。

- 医療分野でのバイオベースポリマー需要の拡大は、市場成長にとって様々な有利な機会を提供すると予想されます。

- ポリエチレンフラノエートの世界市場はアジア太平洋地域が支配的で、中国やインドなどの国による消費が最も多いです。

ポリエチレンフラノエート(PEF)市場の動向

ボトルセグメントからの需要増加

- ポリエチレン・フラノエートは、その高い強度、穿刺強靭性、優れた耐熱性により、ボトルなどの用途での使用が増加しています。

- ポリエチレン・フラノエートはまた、酸素や二酸化炭素に対する耐性を高め、食品の酸化を防ぐ。ポリエチレン・フラノエートに対する飲食品産業での需要が増加し、結果として市場の成長を後押ししています。

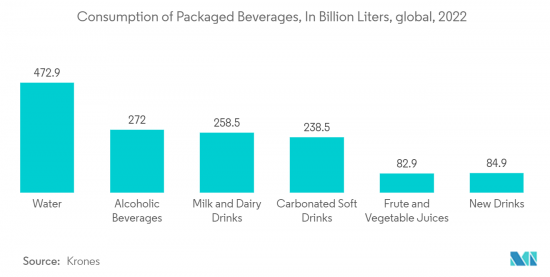

- 飲食品部門は欧州最大の製造業のひとつであり、製造されるボトルの主要な消費者でもあります。FoodDrinkEuropeによると、飲食品業界の売上高は2022年第4四半期に前期比2.3%増、2021年第4四半期比では前年同期比19.2%増となりました。

- さらに、EUの食品・飲料輸出額は2022年第4四半期に483億ユーロ(~509億米ドル)となり、2021年第4四半期と比較して17.5%の成長率を記録しました。この食品・飲料輸出の伸びは、業界のボトル需要に大きな影響を与えました。

- 環境・飲食品・農村地域省によると、英国の飲料製造中小企業数は1,610社で、30の大手飲料企業も含まれています。企業の成長に伴い、持続可能な素材で作られたボトルの需要も増加し、ポリエチレンフラノエート市場に影響を与えると思われます。

- したがって、水、ソフトドリンク、フルーツジュース、アルコール飲料などの飲料の包装におけるボトル需要の増加は、予測期間中にポリエチレンフラノエート市場を推進すると思われます。

市場を独占するアジア太平洋地域

- 予測期間中、アジア太平洋地域がポリエチレンフラノエート市場を独占すると予想されます。中国、インド、日本などの国々では、飲食品、包装、繊維、自動車など様々なエンドユーザー産業からの需要が増加しているため、ポリエチレンフラノエートの需要が増加しています。

- 環境問題への関心の高まりから、バイオベースのボトル、フィルム、繊維に対する傾向と意識の高まりが、植物から抽出された100%バイオベースのリサイクル可能なポリマーであるポリエチレンフラノエート市場を同地域で促進すると予想されます。

- 中国国家統計局によると、中国では2023年1~4月に5,912万トンのノンアルコール飲料が生産されました。4月のノンアルコール飲料の生産量は1,455万トンで、前年同期の生産量を約3%上回りました。予測期間中、PEF製ボトルの需要は最終的に高まると思われます。

- さらに、日本のアサヒグループホールディングスによると、2022年中、清涼飲料の市場シェアの大半は、レディ・トゥ・ドリンクのお茶(30%)が獲得し、レディ・トゥ・ドリンクのコーヒー(18%)、炭酸飲料(15%)、ミネラルウォーター(14%)が続きました。残りのシェアは果汁飲料、乳性飲料、その他に分散しています。

- ポリエチレンフラノエート繊維は、ポリエチレンフラノースをベースにしたボトルからリサイクルされ、100%バイオベースのTシャツの加工に使用されます。これらの繊維は、肥料や農薬などの工業製品の包装に使用されています。また、カーペット、衣類、スポーツウェアにも使用されています。

- 中国国家統計局の月報によると、2023年4月の中国の衣料用繊維生産量は約27億5,000万(m)でした。報告書によると、1月から4月までの中国全体の繊維生産量は108億(m)強でした。

- このように、上記の要因は政府の支援と相まって、予測期間中のポリエチレンフラノエート需要の増加に寄与しています。

ポリエチレンフラノエート(PEF)産業概要

ポリエチレンフラノエート市場は高度に統合されており、主要企業が大きな市場シェアを占めています。市場の主要企業には、Avantium、東洋紡、Sulzer Ltd.、AVA Biochem AG、Swicofil AGなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- ボトル製造におけるポリエチレンフラノエート需要の増加

- 繊維セグメントからの需要増加

- その他の促進要因

- 抑制要因

- 代替品の存在

- 限られた原料の入手可能性

- バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション(市場規模)

- 用途

- ボトル

- フィルム

- 繊維

- 地域

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他のアジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他の欧州

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他の中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- AVA Biochem AG

- Avantium

- Sulzer Ltd

- Swicofil AG

- Toyobo Co., Ltd.

第7章 市場機会と今後の動向

- 医療分野におけるバイオベースポリマーの需要拡大

- その他の機会

The Polyethylene Furanoate Market size is estimated at 2.40 kilotons in 2024, and is expected to reach 6.01 kilotons by 2029, growing at a CAGR of 20.11% during the forecast period (2024-2029).

The market was negatively impacted due to COVID-19. Owing to the pandemic, several countries worldwide went into lockdown to curb the spread of the virus. The shutdown of numerous companies and factories disrupted worldwide supply networks and harmed global production, delivery schedules, and product sales. Currently, the market recovered from the COVID-19 pandemic and is increasing significantly.

Key Highlights

- Major factors driving the market studied are the increasing demand for polyethylene furanoate for bottle manufacturing and the rising demand from the fibers segment.

- On the flip side, the presence of other bioplastics such as bio-PET, bio-PE, bio-PP, etc., and the unavailability of raw materials are the major restraints expected to hinder the market's growth.

- Growing demand for bio-based polymers in the medical sector is expected to offer various lucrative opportunities for market growth.

- The Asia-Pacific region dominated the global polyethylene furanoate market, with the largest consumption from countries such as China and India.

Polyethylene Furanoate (PEF) Market Trends

Increasing Demand from Bottles Segment

- Polyethylene furanoate is increasingly used in applications such as bottles due to its high strength, puncture toughness, and good heat resistance.

- Polyethylene furanoate also increases oxygen and carbon dioxide resistance, preventing food products from oxidizing. It is increasing the demand for polyethylene furanoate in the food & beverage industry and consequently boosting its market growth.

- The food and beverage sector is one of the largest manufacturing industries in Europe and the major consumer of bottles manufactured. According to FoodDrinkEurope, the food and beverage industry turnover increased by 2.3% in Q4 2022, compared to the previous quarter, and increased by 19.2% Y-o-Y compared to Q4 2021.

- Furthermore, European Union exports of food and drinks were valued at EUR 48.3 billion (~USD 50.9 billion) in Q4 2022, registering a growth rate of 17.5% compared to Q4 2021. This growth in food and drink exports greatly impacted the industry's bottle demand.

- According to the Department for Environment, Food, and Rural Affairs, the number of beverage-manufacturing SMEs in the United Kingdom accounted for 1.61 thousand, along with 30 large beverage businesses. With the growing companies, the demand for bottles made from sustainable material would also increase, thereby affecting the polyethylene furanoate market.

- Therefore, growing demand for bottles in the packaging of beverages such as water, soft drinks, fruit juices, and alcoholic beverages is likely to propel the polyethylene furanoate market during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific region is expected to dominate the market for polyethylene furanoate during the forecast period. In countries like China, India, and Japan, owing to the rising demand from various end-user industries, including food and beverage, packaging, textile, and automotive, the demand for polyethylene furanoate is increasing in the region.

- Due to rising environmental concerns, the growing trend and awareness of bio-based bottles, films, and fibers are anticipated to propel the polyethylene furanoate market in the region as it is a 100% bio-based recyclable polymer extracted from plants.

- According to the National Bureau of Statistics of China, 59.12 million metric tons of non-alcoholic beverages were produced in China during the first four months of 2023. The production of non-alcoholic beverages in April amounted to 14.55 million metric tons, approximately 3% more than the previous year's production for the same period. It would eventually enhance the demand for bottles made from PEF during the forecast period.

- Moreover, according to the Asahi Group Holdings in Japan, during 2022, the majority of the market share of soft drinks was acquired by ready-to-drink tea (30%), followed by ready-to-drink coffee (18%), carbonated drinks (15%) and mineral water (14%). The rest of the share was distributed among fruit juice, lactic drinks, and others.

- Polyethylene furanoate fibers are recycled from polyethylene furanose-based bottles and are used in processing 100% biobased t-shirts. These fibers are used in packaging industrial products like fertilizers and pesticides. They are also used in carpets, clothing, and sports apparel.

- According to the National Bureau of Statistics of China's monthly report, the country produced around 2.75 billion m of clothing fabric in April 2023. The overall textile production in the nation from January to April was little more than 10.8 billion, as stated in the report.

- Thus, the factors above, coupled with government support, are contributing to the increasing demand for polyethylene furanoate during the forecast period.

Polyethylene Furanoate (PEF) Industry Overview

The polyethylene furanoate market is highly consolidated, with top players accounting for a major market share. Some of the key companies in the market include Avantium, Toyobo Co., Ltd., Sulzer Ltd., AVA Biochem AG, and Swicofil AG.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand of Polyethylene Furanoate for Bottles Manufacturing

- 4.1.2 Rising Demand from Fibers Segment

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Presence of Substitutes

- 4.2.2 Limited Raw Material Availability

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Application

- 5.1.1 Bottles

- 5.1.2 Films

- 5.1.3 Fibers

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle-East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle-East and Africa

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 AVA Biochem AG

- 6.4.2 Avantium

- 6.4.3 Sulzer Ltd

- 6.4.4 Swicofil AG

- 6.4.5 Toyobo Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing demand for Bio-based Polymers in Medical Sector

- 7.2 Other Opportunities