|

市場調査レポート

商品コード

1406052

骨内注入キット:市場シェア分析、産業動向と統計、2024年~2029年の成長予測Intraosseous Infusion Kits - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 骨内注入キット:市場シェア分析、産業動向と統計、2024年~2029年の成長予測 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

骨内注入キット市場は予測期間中に7.2%近いCAGRで推移すると予測されています。

主なハイライト

- COVID-19は、COVID-19以外の入院を伴う選択的手術のキャンセルにより市場成長に若干の影響を与えました。しかし、規制が解除されてからここ数年で市場成長は回復しました。COVID-19の新バリエーションは、現在のシナリオでは調査市場に大きな影響を与えないです。したがって、予測期間中、市場は安定した成長率を記録すると予想されます。

- 他の薬剤投与経路と比較して、骨内注入(IO)の利点は市場成長を促進すると予想されます。例えば、2021年2月にEuropean Journal of Trauma and Emergency Surgeryに掲載された調査論文には、1,218人の外傷患者と1,432件のデバイス挿入からなる9件の研究が含まれています。挿入成功率は95%で、合併症の発生率は0.9%でした。この論文では、骨内カテーテルは外傷患者において挿入成功率が高く、合併症の発生率が低いことが述べられています。

- さらに、米国国立生物工学情報センター(NCBI)が2022年2月に発表した論文では、骨内注入は効果的で安全な手技であり、患者の生存率を高めると述べられています。その結果、すべての看護専門家が、即時の末梢静脈アクセスが不可能な状況において、さまざまな腹腔内デバイスの使用方法を理解することは極めて重要です。IO注入に関する利点と意識の高まりは、予測期間中にIO注入キットの需要を促進すると予想されます。

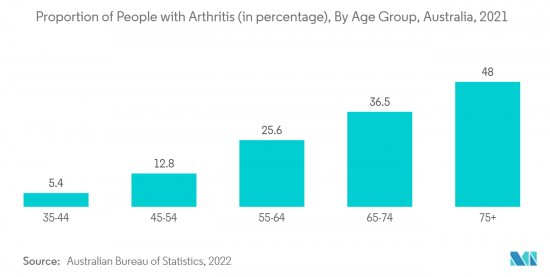

- さらに、関節炎や外傷の負担増は、これらの疾患が静脈アクセスの確立の難しさと関連しているため、IO注入の需要を促進すると予想されます。例えば、オーストラリア統計局2023年最新版によると、2021年のオーストラリアでは全年齢層の8人に1人(12.5%)が関節炎を患っていました。さらに、対関節炎2022年報告書によると、2021年に英国では2,030万人が関節炎や腰痛などの筋骨格系(MSK)疾患を患っていました。したがって、関節炎の世界の有病率の高さは、疾患の治療のための薬剤のより高い生物学的利用能のためのIO注入の需要を促進し、それによって市場の成長を増強すると予想されます。

- したがって、IO注入の利点や関節炎の世界の高負担などの前述の要因のために、調査市場は、分析期間にわたって成長を示すと予想されます。しかし、手続きや厳しい規制承認、製品リコールに関連する高コストは、市場の成長を抑制すると予想されます。

骨内注入キット市場の動向

予測期間中、病院セグメントが大きな市場シェアを占める見込み

- 病院は、関節炎、外傷、その他の骨疾患を含む病状を治療するための主要な治療環境です。病院セグメントは、即時救済のための治療の第一線としてIO注入キットを必要とする病院に入院する負傷患者や外傷患者の数が増加しているため、予測期間中に大きな成長率を示すことが期待されています。

- 外傷患者や火傷患者の入院件数が多いため、IO注入キットの需要が高まっています。こうした患者は静脈へのアクセスが悪く、救命のための輸液や薬剤を即座に投与する必要があるからです。例えば、サウジアラビア王国のKing Khalid Hospital Prince Sultan Center for Health ServicesとPrince Sattam Bin Abdulaziz University Hospitalで実施された2021年4月発行のSaudi Journal of Biological Science誌に掲載された調査では、熱傷患者を対象に調査が行われました。この調査によると、第1度熱傷の有病率は12.8%、第2度熱傷は71.1%、第3度熱傷は16.1%でした。したがって、世界的に火傷の発生件数が多いことから、入院需要が促進されることが予想され、他の投与経路では実現できない全身静脈系への点滴や薬剤の迅速な注入が可能になるため、市場成長をさらに押し上げることが期待されます。

- さらに、2022年7月にISTATが発表したプレスリリースによると、パンデミック(世界的大流行)の状況とそれを食い止めるための対策が、2021年の交通事故と移動の動向に引き続き影響を与えたといいます。前年と比べ、2021年3月から6月にかけてイタリアでは事故と負傷が大幅に増加し、下半期にはパンデミック流行前の水準に非常に近いところまで戻った。同資料によると、2021年の負傷者数は約20万4,700人(28.6%増)、交通事故件数は15万1,900件(28.4%増)。すべての数値が前年に比べて増加しています。このように、交通事故件数の増加により外傷や入院の件数が増加していることから、薬剤を迅速に投与できるIO注入キットの利用が増加し、市場拡大に寄与することが期待されます。

- さらに、2022年2月に発表された交通安全観測所のデータによると、2022年1月にはフランス本土の道路で約260件の死亡事故が発生しています。警察が記録した2022年1月の負傷事故件数は3,728件で、3,508件だった2021年を上回った。交通事故の多くは重傷であり、早急な栄養補給や投薬が必要であるため、このようなケースを治療するための病院における骨内注入キットの需要を押し上げています。

- したがって、前述の要因により、このセグメントは予測期間中に大きな成長率を記録すると予想されます。

予測期間中、北米が骨内注入キット市場を独占する見込み

- 北米は、関節炎や火傷などの外傷の負担が大きいこと、研究開発(R&D)支出の増加、IO注入治療に対する認知度の上昇、同地域に市場企業が集中していることなどの要因から、市場を独占すると予測されています。

- カナダ統計局の2022年8月の更新によると、2021年には35歳から49歳の65万7,900人、50歳から64歳の200万人、65歳以上の310万人が関節炎を患っています。また、関節炎財団の2022年の報告によると、米国では30万人近くの子供が若年性関節炎を患っていました。調査された子供の36%は、重度の不快感を報告し、日常活動を著しく制限しました。これらの統計は、他の投与経路が有効でないこのような疾患において、大腿骨遠位部または脛骨遠位部および近位部に薬剤を投与するためのIO注入キットの需要が高いことを示しています。このような要因が、予測期間中の同地域の市場成長を押し上げると予想されます。

- さらに、National Institute of Health, Estimates of Funding for Various Research, Condition, and Disease Categories(RCDC), May 2022 updateによると、米国における関節炎の研究開発費は2021年に3億1,200万米ドル、2022年に3億2,400万米ドルでした。関節炎の研究のために政府から提供される助成金は、市場企業が効果的な骨内投与経路を持つ革新的なデバイスを開発する機会を創出することが期待され、これが今後数年間の市場成長を促進することがさらに期待されます。

- したがって、関節炎の高い負担、研究開発費の増加、市場企業の高い集中などの上記の要因のおかげで、調査市場の成長は北米地域で予想されます。

骨内注入キット産業概要

骨内注入キット市場は、世界的および地域的に事業を展開する企業が数社存在するため、その性質上競合が激しいです。競合情勢には、主要または重要な市場シェアを保有する数社の国際企業および地元企業の分析が含まれます。市場参入企業には、エアロヘルスケア、BD(ベクトン・ディッキンソン・アンド・カンパニー)、BPBメディカ-バイオプシーベル、クックメディカル、PAVmed Inc.、パフォーマンスシステムズ(パーシスメディカル)、テレフレックス(ピングメディカル)、イステムメディカルなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 外傷と関節炎の症例増加

- 他の薬物投与経路に対する優位性

- 市場抑制要因

- 処置に伴う高コスト

- 厳しい規制当局の承認と製品回収

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(市場規模)

- デバイス技術別

- バッテリー駆動

- 手動式

- 衝撃駆動

- 投与経路別

- 大腿骨遠位部

- 胸骨

- 脛骨遠位および近位

- その他の投与経路

- エンドユーザー別

- 病院

- 外来手術センター

- その他のエンドユーザー

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- GCC

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- その他の南米

- 北米

第6章 競合情勢

- 企業プロファイル

- Aero Healthcare

- BD(Becton, Dickinson and Company)

- BPB Medica-Biopsybell

- Cook Medical

- PAVmed Inc.

- Persys Medical

- Istem Medikal

- Teleflex Inc(Pyng Medical)

第7章 市場機会と今後の動向

The intraosseous infusion kits market is anticipated to register a CAGR of nearly 7.2% during the forecast period.

Key Highlights

- COVID-19 impacted market growth slightly due to the cancellations of elective procedures involving hospitalization other than COVID-19. However, the market growth recovered in the last few years since the restrictions were lifted. The new variants of COVID-19 have no significant impact on the studied market in the current scenario. Hence, the market is expected to register a stable growth rate during the forecast period.

- The advantages of intraosseous infusion (IO) over other routes of administration of drugs are expected to propel market growth. For instance, a research article published in the European Journal of Trauma and Emergency Surgery in February 2021 included nine studies comprising 1,218 trauma patients and 1,432 device insertions. The insertion success rate was 95%, and the incidence of complications was 0.9%. The article stated that intraosseous catheters have high insertion success rates and a low incidence of complications in trauma patients.

- Additionally, an article published in February 2022 by the National Center for Biotechnology Information (NCBI) stated that intraosseous infusion is an effective and safe technique, that increases patient survival. As a result, it is critical that all nursing professionals understand how to use the various intraosseous devices in situations where immediate peripheral venous access is not possible. The advantages and rising awareness about IO infusion are expected to propel the demand for IO infusion kits during the forecast period.

- Furthermore, the rising burden of arthritis and trauma is expected to propel the demand for IO infusion as these diseases are associated with difficulty in establishing venous access, which is made possible by the use of intraosseous needles. For instance, as per the Australian Bureau of Statistics 2023 update, one in eight (12.5%) people of all ages had arthritis in Australia in 2021. Additionally, as per versus arthritis 2022 report, 20.3 million people had a musculoskeletal (MSK) condition such as arthritis or back pain in the United Kingdom in 2021. Therefore, the high prevalence of arthritis worldwide is expected to propel the demand for IO infusion for the greater bioavailability of drugs for the treatment of diseases, thereby augmenting market growth.

- Therefore, owing to the aforementioned factors, such as the advantages of IO infusion and the high burden of arthritis worldwide, the studied market is anticipated to witness growth over the analysis period. However, the high cost associated with Procedures and stringent regulatory approvals and product recalls is expected to restrain the market growth.

Intraosseous Infusion Kits Market Trends

Hospital Segment is Expected to Hold a Significant Market Share Over The Forecast Period

- Hospitals are the primary care settings for treating medical conditions, including arthritis, trauma, and other bone disorders. The hospital segment is expected to witness a significant growth rate during the forecast period owing to the rising number of injured and traumatic patients admitted to hospitals that require IO infusion kits as a first line of treatment for immediate relief.

- The high number of hospitalizations for trauma and burn patients boosts the demand for IO infusion kits as such people have compromised intravenous access and need immediate delivery of life-saving fluids and medications. For instance, research published in April 2021 in the Saudi Journal of Biological Science conducted at the King Khalid Hospital Prince Sultan Center for Health Services and Prince Sattam Bin Abdulaziz University Hospital in the Kingdom of Saudi Arabia surveyed patients with burns. The study stated that the prevalence of first-degree burns was 12.8%, second-degree burns were 71.1%, and third-degree burns were 16.1%. Therefore, the high number of burns worldwide is expected to propel the demand for hospitalization, which is further expected to boost market growth as it enables the quick infusion of intravenous fluids and drugs into the systemic venous system, which cannot be achieved via another route of administration.

- Furthermore, in July 2022, a press release by ISTAT stated that the pandemic situation and the measures for containing it continued to influence the trend of road accidents and mobility in 2021. Compared to the previous year, accidents and injuries increased substantially in Italy in March-June 2021, returning to levels very close to those of the pre-pandemic period in the second half of the year. As per the same source, in the year 2021, around 204.7 thousand were injured (+28.6%), and 151.9 thousand is the number of road accidents number (+28.4%). All values increased in comparison to the previous year. Thus, the increasing number of road accidents is increasing the number of trauma and hospitalizations, which is expected to increase the utilization of IO infusion kits for the rapid delivery of medications and contribute to market growth.

- Additionally, data from the Road Safety Observatory published in February 2022 stated that in January 2022, around 260 fatalities occurred on the roads of mainland France. The number of injury accidents recorded by police forces was 3,728 in January 2022, which was higher than that of 2021, which accounted for 3,508 accidents. A large number of road accidents are associated with severe injury, which requires immediate nutrients and medications, thereby boosting the demand for intraosseous infusion kits in hospitals for treating such cases.

- Therefore, owing to the aforementioned factors, the segment is expected to register a significant growth rate during the forecast period.

North America is Expected to Dominate the Intraosseous Infusion Kits Market Over the Forecast Period

- North America is expected to dominate the market owing to factors such as the high burden of arthritis and trauma cases such as burns, increased research and development (R&D) spending, rising awareness about the IO infusion treatment, and the high concentration of market players in the region.

- According to Statistics Canada's August 2022 update, 657.9 thousand people aged 35 to 49 years, 2 million aged 50 to 64, and 3.1 million people aged 65 and above had arthritis in 2021. Also, as per the Arthritis Foundation 2022 report, nearly 300 thousand children in the United States had juvenile arthritis. 36% of the surveyed children reported severe discomfort, significantly limiting their daily activities. These statistics indicate the high demand for IO infusion kits for the administration of medications in the distal femur or distal and proximal tibia in such diseases where another route of administration is not effective. Such factors are expected to boost market growth in the region during the forecast period.

- Furthermore, according to the National Institute of Health, Estimates of Funding for Various Research, Condition, and Disease Categories (RCDC), May 2022 update, the spending on R&D in the United States for arthritis was USD 312 million in 2021 and USD 324 million in 2022. The grant provided by the government for the research of arthritis is expected to create opportunities for market players to develop innovative devices with effective intraosseous routes of administration, which is further expected to propel market growth in the upcoming years.

- Therefore, owing to the above-mentioned factors, such as the high burden of arthritis, rising R&D spending, and high concentration of market players, the growth of the studied market is anticipated in the North American region.

Intraosseous Infusion Kits Industry Overview

The intraosseous infusion kits market is competitive in nature due to the presence of a few companies operating globally as well as regionally. The competitive landscape includes an analysis of a few international as well as local companies that hold major or significant market shares. Some market players are Aero Healthcare, BD (Becton, Dickinson and Company), BPB Medica - Biopsybell, Cook Medical, PAVmed Inc., Performance Systems, Inc. (Persys Medical), Teleflex (Pyng Medical), and Istem Medikal.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Cases of Trauma and Arthritis

- 4.2.2 Advantages over Other Route of Drug Administrations

- 4.3 Market Restraints

- 4.3.1 High Cost associated with Procedure

- 4.3.2 Stringent Regulatory Approvals and Product Recalls

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD)

- 5.1 By Device Technology

- 5.1.1 Battery Powered

- 5.1.2 Manual

- 5.1.3 Impact Driven

- 5.2 By Route of Administration

- 5.2.1 Distal Femur

- 5.2.2 Sternum

- 5.2.3 Distal and Proximal Tibia

- 5.2.4 Other Routes of Administration

- 5.3 By End-Users

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Other End-Users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aero Healthcare

- 6.1.2 BD (Becton, Dickinson and Company)

- 6.1.3 BPB Medica - Biopsybell

- 6.1.4 Cook Medical

- 6.1.5 PAVmed Inc.

- 6.1.6 Persys Medical

- 6.1.7 Istem Medikal

- 6.1.8 Teleflex Inc (Pyng Medical)