骨内注入デバイス市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Intraosseous Infusion Devices Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日

- 商品コード

- 1773417

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

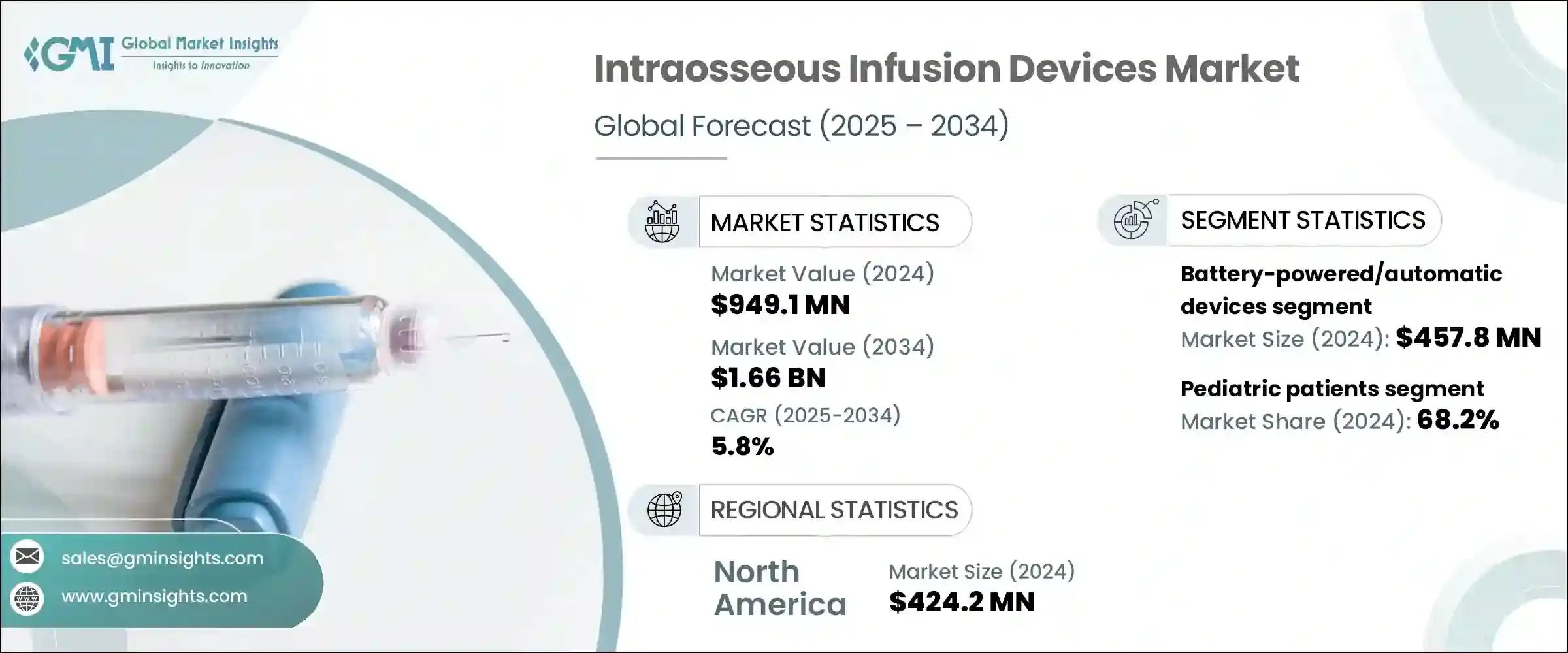

骨内注入デバイスの世界市場は、2024年には9億4,910万米ドルと評価され、CAGR 5.8%で成長し、2034年には16億6,000万米ドルに達すると予測されています。

骨内注入デバイスは、特に従来の静脈アクセスが遅れたり、効果がないことが判明した場合に、骨髄に直接輸液、投薬、血液製剤を迅速に投与するために設計されています。これらのデバイスは、時間が限られていたり、生理学的制約や患者の状態により末梢静脈にアクセスできない場合に、信頼できる血管アクセスを提供し、重要な医療緊急時に不可欠です。

その迅速な動作と信頼性により、さまざまなヘルスケア環境における救急医療プロトコルの要となっています。迅速な介入が患者の転帰に大きな影響を与える外傷、ショック管理、脱水症などの緊急時に広く使用されています。救急部、救急車サービス、現場医療部隊のヘルスケア専門家は、特に一刻を争うシナリオにおいて、効率的な蘇生とドラッグデリバリーのためにこれらのデバイスに依存しています。骨内アクセスの使用拡大も、民間および軍の医療サービス全体にわたって、訓練プログラムやプロトコルの統合がますます重視されるようになっていることに支えられています。そのコンパクトな構造、携帯性、使いやすさは、従来の病院環境以外での採用をさらに推進し、遠隔地や病院前のケアでの幅広い展開を可能にしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 9億4,910万米ドル |

| 予測金額 | 16億6,000万米ドル |

| CAGR | 5.8% |

市場は製品タイプ別に、電池式、手動式IO針、自動装置、衝撃駆動システムに区分されます。2024年には、電池式/自動装置セグメントが最大の収益シェアを獲得し、4億5,780万米ドルに達しました。これらのデバイスは、そのスピードと配備の容易さにより、救急医療において頼りになるソリューションとなっており、しばしば手動の同等品よりも効率的であることが証明されています。自動静脈内システムは、特に高圧の状況下で、従来の静脈内ルートが選択できない場合に信頼できる代替手段を提供します。その設計は、最小限の訓練で済む一方で、高い初回成功率を実現するため、緊急車両、航空救急車、軍事作戦で好まれるツールとなっています。その過酷な状況下での性能は、世界中のヘルスケア・システムでの採用を後押ししており、緊急時の即応態勢や戦闘ケア・システムを強化するための政府からの投資によって、さらに強化されています。

年齢層別では、市場は成人患者と小児患者に分類されます。2024年には、小児患者が市場全体の68.2%を占め、大半のシェアを占めています。幼少の患者、特に乳幼児や新生児にバスキュラーアクセスを確立するには、静脈が小さく脆弱であるため、しばしば特有の課題が生じる。腹腔内注入は効果的な代替手段を提供し、医療従事者は救命治療を迅速かつ確実に行うことができます。その結果、集中治療室、外来サービス、救急部などにおいて、小児専用の腹腔内デバイスに対する需要が高まっています。小児救急対応に関する世界の基準では、最前線での介入方法として腹腔内アクセスを取り入れる傾向が強まっており、このためヘルスケア施設では、小児ケアに重点を置いた互換性のある機器や包括的なトレーニングプログラムに投資するようになっています。

最終用途の観点から、市場は病院・診療所、外来手術センター、その他の環境に区分されます。病院・診療所セグメントは2024年に主導的地位を占めており、今後数年間も力強い成長を維持すると予想されます。外傷、心停止、敗血症や血液量減少性ショックなどの重篤な病態の増加により、入院患者や救急患者の環境では迅速で信頼性の高いバスキュラーアクセスソリューションの必要性が高まっています。静脈内注入は、特に重症患者や静脈の位置がわかりにくい患者など、静脈へのアクセスが遅れたりできなかったりする場面で重要な選択肢となっています。主要ヘルスケア機関は、緊急治療プロトコールに骨髄内デバイスを組み込んでおり、世界中の病院や外傷センターでその存在感をさらに高めています。

2024年の世界市場は北米がリードし、総評価額は4億2,420万米ドルでした。このリーダーシップは、高度なヘルスケア・インフラと、同地域全体での救急処置の多さに支えられています。米国では、市場は2023年の3億6,550万米ドルから2024年には3億8,290万米ドルに成長しました。需要の高さは、特に静脈内投与が不可能な患者において、即座に血管アクセスを必要とする幅広い緊急症例に対応する必要性から生じています。これらのデバイスは救急医療プロトコルの重要な構成要素となっており、さまざまな臨床使用事例において信頼できる代替手段を提供しています。

世界の競合情勢は、老舗企業と新興企業が混在しています。Pyng Medical社、Teleflex社、Dickinson and Company社、PerSys Medical社、Becton社、Cardinal Health社などの主要企業は、2024年の世界収益の約70%を占めています。これらの企業は市場シェア強化のため、買収、製品革新、戦略的提携を通じて積極的に事業拡大を図っています。同時に、いくつかの地域メーカーや地元メーカーが、費用対効果の高い代替製品を提供することで市場に浸透しつつあります。顧客基盤の拡大と製品入手のしやすさの向上を目的とした合併、新製品展開、地域拡大イニシアティブの急増により、競合のダイナミクスはさらに激化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- サプライヤーの情勢

- バリューチェーンに影響を与える要因

- 業界への影響要因

- 促進要因

- 緊急事態と外傷の発生率の増加

- 軍隊や救急医療サービス(EMS)による採用の増加

- デバイス設計における技術的進歩

- ヘルスケア従事者の意識向上と研修

- 業界の潜在的リスク&課題

- 高度な骨内注入デバイスの高コスト

- 不適切な配置による合併症のリスク

- 市場機会

- 新興市場における外傷治療への投資増加

- 病院前および救急車ケアプロトコルへの統合の強化

- 促進要因

- 成長可能性分析

- 規制情勢

- 北米

- 欧州

- アジア太平洋地域

- ラテンアメリカ

- 中東・アフリカ

- テクノロジーとイノベーションの情勢

- 現在の技術動向

- 新興技術

- 将来の市場動向

- 特許分析

- 価格分析

- 製品タイプ別

- 地域別

- ギャップ分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品タイプ別、2021年~2034年

- 主要動向

- 手動IO針

- 電池式/自動デバイス

- 衝撃駆動型デバイス

第6章 市場推計・予測:年齢別、2021年~2034年

- 主要動向

- 小児患者

- 成人患者

第7章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院と診療所

- 外来手術センター

- その他の用途

第8章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Aero Healthcare

- Becton, Dickinson and Company

- Biopsybell

- Bound Tree Medical

- Cardinal Health

- Cook Medical

- Henry Schein

- Implox

- PAVmed

- PerSys Medical

- Pyng Medical

- SAM Medical

- Sarnova

- Teleflex

- Vidacare

目次

The Global Intraosseous Infusion Devices Market was valued at USD 949.1 million in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 1.66 billion by 2034.Intraosseous infusion devices are designed for rapid administration of fluids, medications, and blood products directly into the bone marrow, particularly when conventional intravenous access proves to be delayed or ineffective. These devices are essential in critical medical emergencies, offering dependable vascular access when time is limited or peripheral veins are inaccessible due to physiological constraints or patient conditions.

Their rapid action and reliability make them a cornerstone in emergency medical protocols across various healthcare environments. They are widely used in trauma cases, shock management, and dehydration emergencies where quick intervention can significantly impact patient outcomes. Healthcare professionals in emergency departments, ambulance services, and field medical units rely on these devices for efficient resuscitation and drug delivery, especially in time-sensitive scenarios. The expanding use of intraosseous access has also been supported by increasing emphasis on training programs and protocol integration across both civilian and military medical services. Their compact build, portability, and ease of use have further propelled adoption beyond traditional hospital settings, enabling wider deployment in remote and pre-hospital care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $949.1 Million |

| Forecast Value | $1.66 Billion |

| CAGR | 5.8% |

The market is segmented by product type into battery-powered, manual IO needles, or automatic devices, and impact-driven systems. In 2024, the battery-powered/automatic devices segment captured the largest revenue share, reaching USD 457.8 million. These devices have become the go-to solution in emergency care due to their speed and ease of deployment, often proving more efficient than their manual counterparts. Automatic intraosseous systems offer a reliable alternative when conventional intravenous routes are not an option, especially under high-pressure circumstances. Their design requires minimal training while still delivering high first-attempt success rates, making them a preferred tool in emergency vehicles, air ambulances, and military operations. Their performance in extreme conditions has boosted adoption across healthcare systems worldwide, further reinforced by investments from governments to enhance emergency readiness and combat care systems.

By age group, the market is categorized into adult and pediatric patients. In 2024, pediatric patients accounted for the majority share, commanding 68.2% of the total market. Establishing vascular access in young patients, especially infants and neonates, often presents unique challenges due to small and fragile veins. Intraosseous infusion offers an effective alternative, allowing medical professionals to administer life-saving treatments quickly and reliably. As a result, the demand for pediatric-specific intraosseous devices has grown across intensive care units, ambulatory services, and emergency departments. Global standards for pediatric emergency response increasingly incorporate intraosseous access as a frontline intervention, which has encouraged healthcare facilities to invest in compatible equipment and comprehensive training programs focused on pediatric care.

In terms of end use, the market is segmented into hospitals and clinics, ambulatory surgical centers, and other settings. The hospitals and clinics segment held the leading position in 2024 and is expected to maintain strong growth over the coming years. Rising cases of trauma, cardiac arrest, and critical conditions such as sepsis and hypovolemic shock have intensified the need for swift and reliable vascular access solutions in inpatient and emergency environments. Intraosseous infusion has become a critical option in scenarios where intravenous access is either delayed or unachievable, especially in patients who are critically ill or whose veins are hard to locate. Major healthcare organizations have integrated intraosseous devices into their emergency care protocols, further accelerating their presence across hospitals and trauma centers globally.

North America led the global market in 2024, with a total valuation of USD 424.2 million. This leadership is supported by advanced healthcare infrastructure and a high volume of emergency procedures across the region. In the United States, the market grew from USD 365.5 million in 2023 to USD 382.9 million in 2024. High demand stems from the need to handle a wide range of emergency cases that require immediate vascular access, especially in patients for whom intravenous methods are not viable. These devices have become a vital component of emergency medical protocols, offering a dependable alternative across a spectrum of clinical use cases.

The global competitive landscape features a mix of well-established players and emerging companies. Key participants such as Pyng Medical, Teleflex, Dickinson and Company, PerSys Medical, Becton, and Cardinal Health collectively accounted for around 70% of global revenue in 2024. These companies are actively expanding through acquisitions, product innovations, and strategic partnerships to reinforce their market share. At the same time, several regional and local manufacturers are penetrating the market by offering cost-effective alternatives. Competitive dynamics are further intensified by a surge in mergers, new product rollouts, and regional expansion initiatives aimed at broadening customer bases and enhancing product accessibility.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product type

- 2.2.3 Age group

- 2.2.4 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Factor affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising incidence of emergency conditions and trauma cases

- 3.2.1.2 Increased adoption by military and emergency medical services (EMS)

- 3.2.1.3 Technological advancements in device design

- 3.2.1.4 Growing awareness and training among healthcare professionals

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced intraosseous infusion devices

- 3.2.2.2 Risk related to complications due to improper placements

- 3.2.3 Market opportunities

- 3.2.3.1 Growing investments in trauma care across emerging markets

- 3.2.3.2 Increased integration into pre-hospital and ambulance care protocols

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Future market trends

- 3.7 Patent analysis

- 3.8 Pricing analysis

- 3.8.1 By product type

- 3.8.2 By region

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTLE analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Manual IO needles

- 5.3 Battery-powered/automatic devices

- 5.4 Impact-driven devices

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pediatric patients

- 6.3 Adult patients

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profile

- 9.1 Aero Healthcare

- 9.2 Becton, Dickinson and Company

- 9.3 Biopsybell

- 9.4 Bound Tree Medical

- 9.5 Cardinal Health

- 9.6 Cook Medical

- 9.7 Henry Schein

- 9.8 Implox

- 9.9 PAVmed

- 9.10 PerSys Medical

- 9.11 Pyng Medical

- 9.12 SAM Medical

- 9.13 Sarnova

- 9.14 Teleflex

- 9.15 Vidacare

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 130 Pages

- 納期

- 2~3営業日