|

市場調査レポート

商品コード

1406025

軍事用センサー:市場シェア分析、産業動向・統計、成長予測、2024年~2029年Military Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts 2024 - 2029 |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 軍事用センサー:市場シェア分析、産業動向・統計、成長予測、2024年~2029年 |

|

出版日: 2024年01月04日

発行: Mordor Intelligence

ページ情報: 英文 95 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

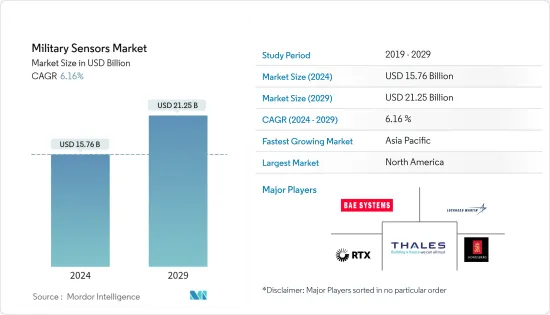

軍事用センサー市場規模は2024年に157億6,000万米ドルと推定され、2029年には212億5,000万米ドルに達し、予測期間(2024-2029年)のCAGRで6.16%の成長が予測されます。

微小電気機械システム(MEMS)ベースのデバイスの進化と急速な採用により、ナビゲーションと位置決め用の高度なマイクロジャイロ、赤外線イメージング用のマイクロボロメーター、レーザービームのステアリング用のマイクロミラーなどが開発されています。RF MEMSとナノテクノロジーは、100GHzを超える速度での衛星通信や、真の時間遅延を実現する電子的にステア可能なRF位相シフターなど、航空宇宙・防衛アプリケーションにおける画期的な進歩をもたらす可能性があります。

現代の軍事システムは、その任務を遂行するために複雑なソフトウェアと相互接続性に大きく依存しています。サイバー対応軍用システムの電子攻撃、センサーフュージョン、通信などの高度な機能は、敵対勢力に対する、あるいは敵対環境での重要な作戦中に、装備された軍隊に戦術的な優位性を提供します。防衛軍における戦域認識に対する需要の高まり、MEMS技術の進歩、ナビゲーションシステムとのアンチジャミング機能の統合といった要因が、市場の成長を後押ししています。しかし、サイバーセキュリティのリスク、軍事用センサーの設計の複雑さ、精度の低さが市場の成長を抑制しています。

軍事用センサー市場の動向

予測期間中、空挺セグメントが最も高いCAGRで成長する見込み

現代の軍用機は、さまざまな任務に対応できるように作られています。世界の航空機の増加により、空挺セグメントにおける軍事用センサーの需要が増加しています。米国、インド、中国、イラン、イスラエル、ロシアなどの国々は、既存の航空隊の近代化とアップグレードに投資しています。中国は無人プラットフォームにステルス技術を使用し、さらに多くのUAVのバリエーションを発表しています。さらに、世界の支出増と防衛力強化のための支出増が市場成長の原動力となっています。

さらに、有人プラットフォームに比べて無人プラットフォームの費用対効果と運用の容易さが、防衛用途(監視と攻撃作戦の両方)におけるUAVの急速な普及を後押ししています。軍事組織もまた、世界中の紛争地域に無人プラットフォームを大々的に配備しています。

予測期間中、アジア太平洋地域が最も高い需要を生み出す見込み

アジア太平洋地域は、予測期間中、地域の防衛力の近代化を促進するいくつかの進行中のプログラムを理由に、軍事用センサーの最も高い需要を生成すると予想されます。例えば、インドネシア国防省はトルコと3億米ドル相当の最新鋭無人機12機を購入する契約を締結し、老朽化した軍備の近代化に向けた同国の継続的な取り組みの新たな一歩を踏み出しました。運用機数では、この地域は航空機と回転翼航空機の保有機数が最も多く、14,529機です。このうち戦闘機は約4,998機で、520機の特殊目的機、46機のタンカー、1,008機の輸送機、3,079機の訓練用ヘリコプターがあります。近隣諸国間の地政学的緊張の高まりと、高度な脅威検知システムに対する需要の高まりが、この地域の市場成長を後押しすると予想されます。

軍事用センサー産業の概要

軍事用センサー市場は半統合化されており、多くの著名なプレーヤーがより大きな市場シェアを争っていることが特徴です。軍事用センサー市場の著名なプレーヤーは、RTX Corporation、Lockheed Martin Corporation、Kongsberg Gruppen ASA、BAE Systems plc、THALESです。ベンダーは、エンドユーザーに付加価値の高いセンサーソリューションを提供する手段として、現在の機能を強化し、画期的な機能を導入するために提供する製品を変更しています。これは、差別化の低い製品を競争力のある価格で導入するのに役立ちます。さらに、エンドユーザーである防衛軍の設計・性能仕様に適合した高度なセンサーを開発するために、メーカー間の戦略的コラボレーションが増加しています。これは予測期間中、業界の利害関係者に利益をもたらすと予想されます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手・消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- アプリケーション

- 情報・監視・偵察(ISR)

- 通信・ナビゲーション

- ターゲット認識

- 電子戦

- 指揮統制

- プラットフォーム

- 空挺

- 陸上

- 海上

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- イタリア

- ロシア

- ドイツ

- その他欧州

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- メキシコ

- その他ラテンアメリカ

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他中東・アフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Honeywell International Inc.

- TE Connectivity Ltd.

- RTX Corporation

- Lockheed Martin Corporation

- THALES

- Kongsberg Gruppen ASA

- Ultra

- Aerosonic LLC(Transdigm Group)

- General Electric Company

- BAE Systems plc

- Vectornav Technologies LLC

- Viooa Imaging Technology Inc.

- Imperx Inc.

第7章 市場機会と今後の動向

The Military Sensors Market size is estimated at USD 15.76 billion in 2024, and is expected to reach USD 21.25 billion by 2029, growing at a CAGR of 6.16% during the forecast period (2024-2029).

The evolution and rapid adoption of microelectromechanical systems (MEMS)-based devices have led to the development of sophisticated micro gyros for navigation and positioning, microbolometers for infrared imaging, and micromirrors for steering laser beams. RF MEMS and nanotechnology could lead to breakthroughs in aerospace and defense applications, such as satellite communications at speeds in excess of 100 GHz and electronically steerable RF phase shifters for true-time delay.

Modern military systems are heavily reliant on complex software and interconnectivity to perform their missions. Advanced features, such as an electronic attack, sensor fusion, and communications, of the cyber-enabled military systems provide a tactical edge to the equipped armed forces against an adversary force or during critical operations in a hostile environment. Factors such as increasing demand for battlespace awareness amongst defense forces, ongoing advancements in MEMS technology, and integration of anti-jamming capabilities with navigation systems will be driving the growth of the market. However, cybersecurity risks, complexity in the designs of military sensors, and lack of accuracy would be constraining the growth of the market.

Military Sensors Market Trends

Airborne Segment Expected to Register the Highest CAGR During the Forecast Period

Modern military planes are made to do different kinds of missions. An increase in the global aerial fleet has led to a rise in the demand for military sensors in airborne segments. Countries like the United States, India, China, Iran, Israel, and Russia, among others, have invested in modernizing and upgrading their existing air fleets. China is using stealth technology in unmanned platforms and is unveiling more UAV variants. Furthermore, rising global expenditure and rising spending on enhancing defense capabilities drive market growth.

Moreover, the cost-effectiveness and ease of operations of unmanned platforms, compared to manned platforms, aided the rapid adoption of UAVs in defense applications (for both surveillance and attack operations). Military organizations are also largely deploying unmanned platforms in conflict regions across the world. Also instances such as in September 2022, the US Army awarded phase two contracts to defense firms Raytheon and L3Harris for the development of prototype sensors that were to support the service's next-gen airborne intelligence, surveillance, and reconnaissance program dubbed HADES. These factors render a positive outlook for the airborne military sensors segment of the market during the forecast period.

Asia-Pacific is Expected to Generate the Highest Demand During the Forecast Period

The Asia-Pacific region is expected to generate the highest demand for military sensors on account of the several ongoing programs fostering the modernization of the regional defense forces during the forecast period. In the Asia-Pacific, several modernization programs are underway to enhance the current capabilities of the commercial and military end-users in the region. For instance, Indonesia's Defence Ministry sealed a deal with Turkey to acquire 12 cutting-edge drones valued at USD 300 million, marking yet another step in the country's ongoing efforts to modernize its aging military equipment. In terms of operational fleet, the region has the largest fleet of aircraft and rotorcraft, with 14,529 aircraft. Out of these, combat aircraft constitute about 4,998, along with 520 special purpose aircraft, 46 tankers, 1,008 transport, and 3,079 training and helicopters. The increasing geopolitical tensions between neighboring nations and the rising demand for advanced threat detection systems are expected to aid the growth of the market in this region.

Military Sensors Industry Overview

The military sensors market is semi-consolidated and marked by the presence of many prominent players competing for a larger market share. The prominent players in the military sensors market are RTX Corporation, Lockheed Martin Corporation, Kongsberg Gruppen ASA, BAE Systems plc, and THALES. Vendors are modifying their offerings to enhance current capabilities and introduce revolutionary features as a means to deliver value-added sensor solutions to end users. This helps introduce low-differentiated products at competitive pricing. Furthermore, strategic collaboration between manufacturers is on the rise to develop sophisticated sensors that conform with the design and performance specifications of the end-user defense forces. This is expected to benefit industry stakeholders during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application

- 5.1.1 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.1.2 Communication and Navigation

- 5.1.3 Target Recognition

- 5.1.4 Electronic Warfare

- 5.1.5 Command and Control

- 5.2 Platform

- 5.2.1 Airborne

- 5.2.2 Terrestrial

- 5.2.3 Naval

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 France

- 5.3.2.3 Italy

- 5.3.2.4 Russia

- 5.3.2.5 Germany

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Mexico

- 5.3.4.3 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Honeywell International Inc.

- 6.2.2 TE Connectivity Ltd.

- 6.2.3 RTX Corporation

- 6.2.4 Lockheed Martin Corporation

- 6.2.5 THALES

- 6.2.6 Kongsberg Gruppen ASA

- 6.2.7 Ultra

- 6.2.8 Aerosonic LLC (Transdigm Group)

- 6.2.9 General Electric Company

- 6.2.10 BAE Systems plc

- 6.2.11 Vectornav Technologies LLC

- 6.2.12 Viooa Imaging Technology Inc.

- 6.2.13 Imperx Inc.