|

市場調査レポート

商品コード

1940611

PD-1およびPD-L1阻害剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)PD-1 And PD-L1 Inhibitors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| PD-1およびPD-L1阻害剤:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 160 Pages

納期: 2~3営業日

|

概要

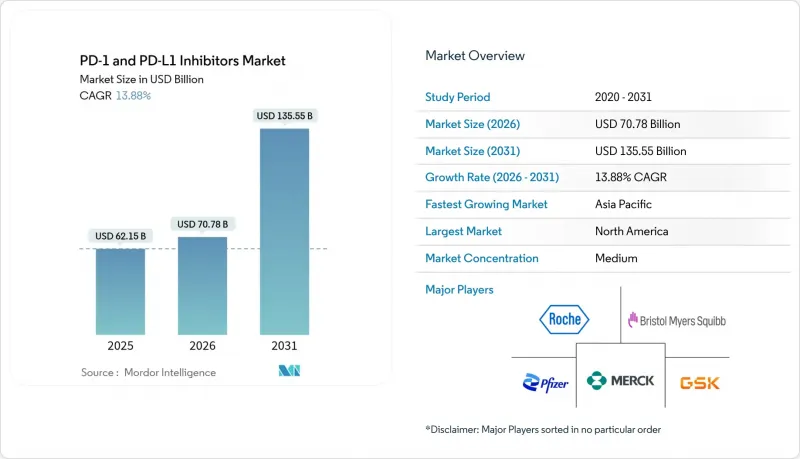

PD-1およびPD-L1阻害剤市場の規模は、2026年には707億8,000万米ドルと推定されております。

これは2025年の621億5,000万米ドルから成長した数値であり、2031年には1,355億5,000万米ドルに達すると予測されております。2026年から2031年にかけての年間平均成長率(CAGR)は13.88%で推移する見込みです。

成長は、迅速な規制当局の承認、絶え間ない適応拡大への投資、そして腫瘍タイプを横断して免疫チェックポイントの有用性を拡大する二重特異性構造体の登場に支えられています。2024年12月にFDAが皮下投与型ニボルマブを承認したことで、特許満了後も収益源を保護できる新たな投与形態が実証されました。特にPD-1/VEGFやPD-1/CTLA-4の併用療法は、無増悪生存期間の有意な延長効果を継続的に示しており、処方医の信頼を強化するとともに高価格設定の基盤を支えています。米国および欧州の大規模な支払者システムは依然として高額な取得コストを吸収していますが、中国における数量ベースの調達モデルは価格低下圧力を生み出し、多国籍企業に新興経済圏における発売戦略の再検討を迫っています。デジタル薬局、遠隔腫瘍学チャネル、および新規参入した低分子経口剤は患者のアクセスを拡大し、従来の点滴センター経済を再構築することで、PD-1およびPD-L1阻害剤市場にさらなる成長のベクトルを生み出しています。

世界のPD-1およびPD-L1阻害剤市場の動向と洞察

ブロックバスター製品の適応拡大に向けた爆発的な研究開発費

製薬企業は、承認済みPD-1/PD-L1薬剤の新たな適応症開拓を目的とした市販後調査に過去最高の資金を投入しています。メルク社単独でもペムブロリズマブを用いた1,600件以上の臨床試験を進行中であり、これにより同分子は有利な償還ステータスを維持しつつ、追加の患者コホートを確保しています。2024年6月にFDAが原発性進行子宮内膜がんの一次治療として承認したことで、無増悪生存期間中央値が6.5ヶ月から11.1ヶ月に延長され、臨床的価値が強化されるとともに製品ライフサイクルが延伸されました。欧州当局もこの勢いに呼応し、2024年11月に悪性胸膜中皮腫に対する肯定的見解を示しました。これは、世界各国の規制当局が既存の安全性データを活用して審査期間を短縮する傾向にあることを示しています。適応症の継続的な拡大はバイオシミラーへの切り替えを遅らせ、プレミアム価格を維持し、PD-1/PD-L1阻害剤市場の成長軌道をさらに加速させます。

米国FDAおよび中国NMPAによる迅速なリアルタイム腫瘍学審査

規制当局は現在、開発期間を短縮する段階的申請、代替エンドポイントの承認、リアルタイム諮問会議を認めています。2024年12月のFDAによる皮下投与ニボルマブ承認は、申請から承認まで10ヶ月以内で実現し、当局の機敏性向上を浮き彫りにしました。中国NMPAも同等のスピードで2024年に48のファースト・イン・クラスのがん治療薬を承認し、チェックポイント阻害剤が最大の単一治療カテゴリーを占めました。非小細胞肺がんにおける第3相試験で優れたデータを示したイボネシマブへの条件付き承認は、優先審査インセンティブが競争のタイムラインを再設定する実態を浮き彫りにしています。加速化されたサイクルは投資回収期間を短縮し、リスク調整後正味現在価値を向上させ、PD-1およびPD-L1阻害剤市場への資本流入を強化しています。

第III相主要併用試験における資本支出の増加

適応型多群試験では、対象集団の拡大、追跡期間の延長、複雑なバイオマーカーパネルが要求され、患者1人あたりの支出は最大6万1,907米ドルに達します。100件以上のペムブロリズマブ併用試験を並行して実施するスポンサー企業は、優良企業のキャッシュフローさえも脅かす累積予算に直面しています。中小バイオテック企業は資金調達難に直面し、パイプラインの多様化が鈍化しています。こうした経済的要因により予測CAGRは1.4ポイント低下するもの、市場全体の成長勢いは逆転しません。

セグメント分析

PD-1阻害剤は2025年の収益の80.92%を占め、PD-1およびPD-L1阻害剤市場規模は502億9,000万米ドルに相当します。その優位性は、黒色腫、肺がん、膀胱がん、頭頸部がんにおける堅調な生存データに起因します。包括的な安全性データ、ガイドラインへの定着、臨床医の習熟度が、腫瘍学センター全体での処方慣性を強化しています。大規模な臨床試験投資により、第一選択治療としての地位が確保され、新たな腫瘍タイプへの展開を通じて二桁成長が持続しています。

開発企業が経口剤、ヘテロ二量体、ポリマー模倣体などの技術革新を推進する中、成長の勢いはPD-L1分子へと移行しています。in vitro研究では、iBodiesがPD-L1遮断効果を維持しつつ熱安定性を向上させることが示されており、コールドチェーンコストの低減が期待されます。ABSK043および後続経口剤は、診療時間を短縮し、患者の利便性を高め、小売薬局やオンライン薬局を通じた流通を可能にする可能性があります。これらの利点が、PD-L1阻害剤の予測CAGR19.85%を支え、PD-1&PD-L1阻害剤市場におけるPD-1優位性を徐々に縮小させつつも覆すことはありません。

地域別分析

北米は、革新技術の迅速な導入、広範な民間保険適用範囲、およびFDAの世界のベンチマークとしての役割を背景に、2025年の世界収益の46.90%を占めました。ペトセムタマブとペンブロリズマブなどの新規併用療法に対する画期的治療薬指定は、臨床導入までの時間を短縮し、治療基準の向上を促進します。2026年開始のインフレ抑制法価格交渉を含む法規制の変化は、将来の利益率に不確実性をもたらしますが、アンメットニーズが高いことから、短期的な導入を阻害する可能性は低いと考えられます。

欧州市場は成熟しつつも価格感応度の高い特性を持っています。2025年施行の欧州医薬品庁(EMA)共同臨床評価規則により証拠基準が統一され、国境を越えた迅速な導入が期待されますが、医療技術評価機関(HTA)による費用対効果の精査は継続されます。補助療法用ペムブロリズマブに関する商業的アクセス契約は、NICEの閾値を満たすためメーカーが割引スキームを適応させる実例を示しています。中国発のトリーパリマブおよびティスレリズマブがEMAで承認されたことで競合が激化し、地域におけるチェックポイント阻害剤の多様化が進む姿勢が示されました。

アジア太平洋地域は15.83%のCAGRで最も急速に成長する市場です。中国はNMPA改革により2024年に228の新薬を承認(多くがPD-1/PD-L1経路関連)し、販売数量を牽引。国内大手企業は価格譲歩を活用して大規模入札を固め、ASEAN市場への進出基盤を築いています。日本では高齢化に伴うがん発生率の上昇により安定した成長が持続し、オーストラリアでは国民健康保険による早期導入が推進されています。この地域全体として、販売量の拡大と革新的なパイプラインの貢献の両面を実現し、PD-1およびPD-L1阻害剤市場の世界の勢いを強化しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- ブロックバスター資産の新効能拡大に向けた爆発的な研究開発費支出

- 米国FDA及び中国NMPAによるがん治療薬の迅速なリアルタイム審査

- 中国における数量ベースの調達制度が国内PD-(L)1メーカーを優遇

- 二特異性/三特異性抗体の台頭/後期臨床試験段階へ

- AIを活用したバイオマーカー発見が奏効率を向上

- ポイント・オブ・ケア診断の進歩が臨床試験の脱落率を低下

- 市場抑制要因

- 第III相主要併用試験における設備投資の増加

- キートルーダ及びオプジーボの2028年米国特許満了問題

- 世界の償還制度の不均一性;費用対効果に関するHTAの反発

- 新興低分子PD-(L)1経口剤の参入が抗体医薬のシェアを侵食

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 阻害剤タイプ別

- PD-1阻害剤

- PD-L1阻害剤

- 用途別

- 非小細胞肺がん

- メラノーマ

- 腎臓がん

- ホジキンリンパ腫

- その他のがん

- 流通チャネル別

- 病院薬局

- 小売薬局

- オンライン薬局

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 中東・アフリカ

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 北米

第6章 競合情勢

- 市場集中度

- 市場シェア分析

- 企業プロファイル

- Merck & Co.

- Bristol-Myers Squibb

- F. Hoffmann-La Roche AG

- AstraZeneca PLC

- Sanofi SA

- Pfizer Inc.

- Regeneron Pharma Inc.

- GSK plc

- Amgen Inc.

- Eli Lilly and Co.

- Novartis AG

- BeiGene Ltd.

- Innovent Biologics

- Hengrui Medicine

- Akeso Inc.

- Henlius Biotech

- Seagen Inc.

- Shanghai Junshi Biosciences

- Arcus Biosciences

- Leap Therapeutics