|

市場調査レポート

商品コード

1910653

成形繊維包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Molded Fiber Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 成形繊維包装:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

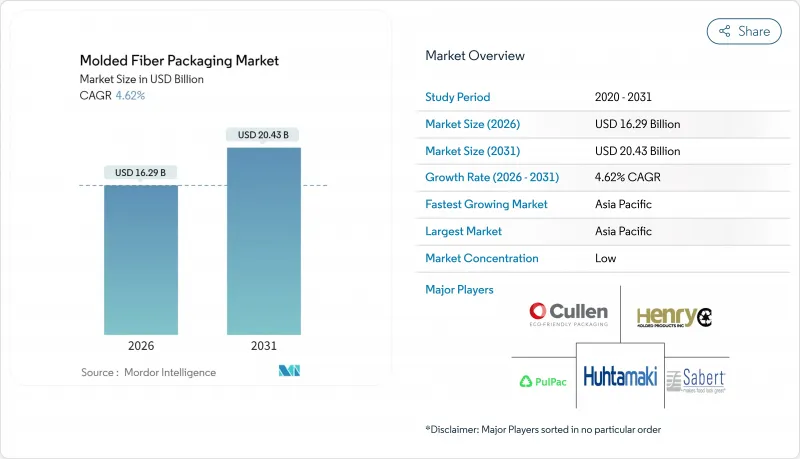

成形繊維包装市場の規模は、2026年には162億9,000万米ドルと推定されており、2025年の155億7,000万米ドルから成長を続けています。

2031年までの予測では204億3,000万米ドルに達し、2026年から2031年にかけてCAGR4.62%で拡大が見込まれます。

使い捨てプラスチックの禁止拡大、CO2排出量を80%削減し生産量を10倍に高める乾式成形繊維技術の急速な普及、そして電子商取引量の増加が相まって需要を支えています。生産者は、コスト、機械的強度、持続可能性のバランスを取るため、ハイブリッド繊維の研究開発を加速しています。一方、クイックサービスレストラン(QSR)が堆肥化可能な包装形式への取り組みを拡大していることで、大量消費のエンドマーケットが拡大しています。合併の激化により買い手と売り手の力学は変化していますが、欧州のパルプ価格が2024年4月に1トン当たり1,380ユーロ(1,496米ドル)でピークに達したため、利益率への圧力は依然として続いています。

世界の成形繊維包装市場の動向と洞察

使い捨てプラスチックに対する規制禁止

急速に進む法規制により、コンプライアンスリスクが成形繊維製品の即時発注へと転換しています。バージニア州では大規模食品ベンダー向け発泡スチロール禁止が2025年7月に施行され、オレゴン州では2025年1月に同様の規則が導入されました。また欧州連合規則2025/40では、2040年までにプラスチック包装の65%を再生材とすることを義務付けています。オーストラリアの2024年包装改革では、廃棄コストを内部化する拡大生産者責任が組み込まれています。こうした整合性のある規制により代替が加速し、成形繊維包装市場は小売業者や食品ブランドにとってデフォルトの選択肢となっています。

電子商取引と食品配送チャネルの成長

消費者向けミールキットや食料品配送サービスでは、断熱性と衝撃保護が求められますが、軽量プラスチックでは持続可能な形でこれを実現することが困難です。テンパーパック社の繊維ベースライナーは、出荷量を削減し、単一クライアントで年間400台のトラックを削減できるため、材料価格のプレミアムを相殺する輸送コスト削減効果を示しています。顧客のバックログが繰り返されることで明らかになった未充足需要は、成形繊維包装市場に生産能力拡大のインセンティブをもたらしています。

高級再生繊維の価格変動

欧州パルプのスポット価格は2024年4月に1トン当たり1,380ユーロ(1,496米ドル)に達し、前年比14%の上昇となりました。ヘッジ対策が取れなかった加工業者には厳しい状況です。北欧の供給混乱と森林伐採規制の強化が製紙工場の閉鎖を促し、コスト変動を拡大させています。成形繊維包装業界の中堅・中小企業は運転資金の逼迫に直面し、提携または撤退を迫られています。

セグメント分析

トランスファー成形繊維は2025年に49.62%という圧倒的なシェアを獲得し、設置ベースと汎用性により成形繊維包装市場を支えました。熱成形品は規模こそ小さいもの、バリアコーティングと美観の向上により高級ブランドを惹きつけ、6.45%のCAGRで成長が見込まれます。厚肉成形は工業用緩衝材として依然重要であり、加工グレードは装飾仕上げに対応します。軽度の脱リグニン処理により引張強度が22%向上し、電子機器包装への適用可能性が高まっています。熱成形品向け成形繊維包装市場規模は、3Dドライ成形によるサイクルタイム短縮と金型コスト削減により、着実な拡大が見込まれます。

技術革新の潮流は、転写部品の耐油性・耐湿性を高めるハイブリッド積層技術へと移行しています。メーカー各社はCFD(計算流体力学)を活用し真空サイクルを最適化、繊維使用量を最大12%削減しています。競合優位性は、独自開発の成形スクリーンと水回収システムによる運用コスト低減に依存する状況です。

トレイは2025年売上高の34.07%を占め基幹製品であり続けましたが、クイックサービスレストランチェーンがヒンジ強度と積載効率を要求するため、クラムシェル容器とコンテナはCAGR5.17%が見込まれます。手軽なスナックや食事宅配サービスの成長が需要をさらに加速させています。エンドキャップとインサートは電子機器や家電製品の衝撃吸収ニーズを満たし、ポリエチレンフリーバリア材の登場によりカップの需要も拡大しています。

炭酸カルシウムやカオリンなどの鉱物系充填剤は剛性と白色度を向上させ、生産ラインの速度を大幅なコスト増なしに高めます。ただし、鉱物の過剰添加は耐衝撃性を低下させるため、配合設計者は充填剤比率を慎重に調整します。現在の採用曲線が持続すれば、クラムシェルに起因する成形繊維包装市場の規模は、10年後に10億米ドル台半ばに達する可能性があります。

地域別分析

アジア太平洋地域は2025年に成形繊維包装市場で38.45%のシェアを占め、中国とインドがリサイクル困難なプラスチックの禁止措置を緩和する中、2031年まで年平均6.65%の成長率で拡大すると予測されます。持続可能な素材に対する政府補助金が国内機械購入を促進し、人件費の優位性が投資回収期間を短縮しています。堅調な中産階級の消費により、コンビニエンスフード、電子機器、医薬品の需要量が増加しています。

北米では、2032年までにプラスチック使用量を25%削減することを義務付けるカリフォルニア州法案SB 54などの規制が推進力となっています。ブランドの公約が繊維製クラムシェルの早期採用を促進する一方、国内パルプ資源が原料価格の変動を緩和しています。しかしながら、労働市場の逼迫と高エネルギーコストにより、大規模コンバーターに有利な自動化への投資が迫られています。

欧州では循環型経済が重視され、規制2025/40により再生材含有率の基準が強化されます。オーストリアとフィンランドのメーカーは先進的な繊維成形ラインを活用し、EU全域の需要に対応します。日本では2025年6月施行の改正ポジティブリスト制度により、厳格な移行試験が義務付けられ、規律あるサプライヤーが活用できる参入障壁が生じています。南米、中東・アフリカでは、都市化と廃棄物インフラの整備が進み、一人当たりプラスチック使用量が低いという未開拓の成長領域が存在し、成形繊維の採用に向けた道筋が整っています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 消費者の嗜好がリサイクル可能で環境に優しい包装材へ移行

- 使い捨てプラスチックに対する規制上の禁止措置

- 電子商取引および食品配達チャネルの成長

- 生分解性クラムシェル容器のQSR(クイックサービスレストラン)導入状況

- 3Dドライ成形繊維技術の商業化

- ブランドレベルでのカーボンニュートラル宣言

- 市場抑制要因

- 高品質再生繊維の価格変動性

- バイオプラスチックおよびコート紙板代替品

- 湿潤食品に対するバリア特性の制約

- 資本集約的なカスタム金型要件

- 業界バリューチェーン分析

- 規制情勢

- テクノロジーの展望

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争の激しさ

- マクロ経済要因が市場に与える影響

第5章 市場規模と成長予測

- 成形繊維タイプ別

- 厚肉

- トランスファー成形

- 熱成形

- 処理済み

- 製品タイプ別

- トレイ

- クラムシェル容器およびコンテナ

- カップおよびカップホルダー

- お皿とお椀

- その他の製品タイプ

- 原材料の調達先別

- 再生紙

- バージンパルプ

- ハイブリッドファイバーブレンド

- エンドユーザー業界別

- 食品・飲料

- 電子機器および家電製品

- 医療・医療機器

- 産業

- その他のエンドユーザー産業

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリアおよびニュージーランド

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- アラブ首長国連邦

- サウジアラビア

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- ケニア

- ナイジェリア

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Huhtamaki Oyj

- Brodrene Hartmann A/S

- Sonoco Products Company

- UFP Technologies Inc.

- Omni-PAC Group UK

- Henry Molded Products Inc.

- Pactiv Evergreen Inc.

- Cullen Packaging Ltd.

- Genpak LLC

- Sabert Corporation

- International Paper Co.

- Enviropak Corporation

- Keiding Inc.

- PulPac AB

- Stora Enso Oyj

- Heracles Packaging SA

- Earthpac(US)

- Fiber Mold A/S

- Fabri-Kal Corporation

- TMP Technologies