|

市場調査レポート

商品コード

1666678

閉鎖型遷移スイッチ市場の機会、成長促進要因、産業動向分析、2025~2034年の予測Closed Transition Transfer Switch Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 閉鎖型遷移スイッチ市場の機会、成長促進要因、産業動向分析、2025~2034年の予測 |

|

出版日: 2024年12月26日

発行: Global Market Insights Inc.

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

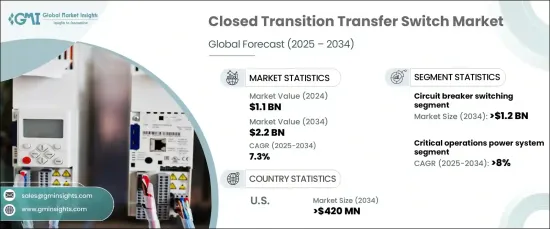

閉域遷移型トランスファースイッチの世界市場規模は2024年に11億米ドルとなり、2025年から2034年にかけてCAGR 7.3%で拡大すると予測されています。

同市場は、ミッションクリティカルな環境における信頼性の高い電力転送ソリューションに対する需要の高まりにより、着実な成長を遂げています。ヘルスケア、データセンター、製造業など、事業運営に継続的な無停電電源が必要なセクターでは、機器の故障を防ぎ、事業効率を維持するために、こうしたスイッチの採用が増加しています。

電力網の近代化に重点を置く政府の取り組みが、市場の拡大に寄与しています。特に、再生可能エネルギー、ハイブリッド・システム、マイクログリッドの統合が進んでいることが後押ししています。これらの技術が普及するにつれ、安定した電力供給を維持するためには、信頼性の高い電力移行システムが不可欠となります。さらに、エネルギー効率基準の厳格化と自動化技術の利用の増加が、市場成長の推進に重要な役割を果たしています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 11億米ドル |

| 予測金額 | 22億米ドル |

| CAGR | 7.3% |

サーキットブレーカー機構を使用する市場セグメントは、2034年までに12億米ドルを超えると予想されます。この成長は、信頼性が重要な要素である産業において、無停電電源に対する差し迫ったニーズが原動力となっています。サーキットブレーカを使用したトランスファースイッチは、このようなシナリオに理想的で、ダウンタイムを最小限に抑え、繊細な機器を保護するシームレスな電力移行を提供します。この需要は、再生可能エネルギー源の拡大やスマートグリッド技術の進歩によってさらに促進されており、これらの技術には、強化された故障保護と安定した電力フローが必要です。

クリティカルなオペレーションにおける閉域遷移型トランスファースイッチの市場は急速に成長し、2034年までのCAGRは8%を超えると予測されています。この需要の急増は、継続的な電力供給に大きく依存している産業と関連しており、わずかな中断でも重大な結果をもたらす可能性があります。その結果、企業は停電から業務を守るため、無停電電源装置(UPS)やバックアップ発電機などのバックアップ電源ソリューションへの投資を増やしています。自動化、スマートグリッド、再生可能エネルギーの利用が増え、エネルギー効率基準を満たすことに重点が置かれていることも、この成長をさらに後押ししています。

米国では、閉域遷移型トランスファースイッチ市場は、2034年までに4億2,000万米ドルを超えると予想されています。この成長促進要因は、ヘルスケア、製造、データ管理などの分野で信頼性の高い電力転送システムへの需要が高まっていることです。再生可能エネルギーやスマートグリッド技術の採用が、こうしたシステムの必要性を加速させています。停電や機器保護への懸念が高まる中、閉域遷移型トランスファースイッチの市場は成長を続けており、シームレスな電力移行を実現する信頼性の高いソリューションを業界に提供しています。

目次

第1章 調査手法と調査範囲

- 市場の定義

- 基本推定と計算

- 予測計算

- データソース

- 1次データ

- 2次データ

- 有償

- 公的

第2章 エグゼクティブサマリー

第3章 業界洞察

- エコシステム分析

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長可能性分析

- ポーターの分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- PESTEL分析

第4章 競合情勢

- 戦略ダッシュボード

- イノベーションと持続可能性の展望

第5章 市場規模・予測:事業別、2021年~2034年

- 主要動向

- 手動

- 非自動

- 自動

- バイパス分離

第6章 市場規模・予測:スイッチング機構別、2021年~2034年

- 主要動向

- コンタクター

- サーキットブレーカー

第7章 市場規模・予測:定格電流別、2021年~2034年

- 主要動向

- 400アンペア以下

- 401アンペア~1600アンペア

- 1600アンペア以上

第8章 市場規模・予測:設置場所別、2021年~2034年

- 主要動向

- 緊急システム

- 法定システム

- 重要業務用電源システム

- オプション待機システム

第9章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- フランス

- ロシア

- 英国

- イタリア

- スペイン

- アジア太平洋

- 中国

- 日本

- 韓国

- インド

- オーストラリア

- 中東・アフリカ

- UAE

- サウジアラビア

- 南アフリカ

- ラテンアメリカ

- ブラジル

- アルゼンチン

第10章 企業プロファイル

- AEG Power Solutions

- ABB

- Briggs &Stratton

- Caterpillar

- Cummins

- Eaton

- General Electric

- Generac Power Systems

- Kohler

- Midwest Electric Products

- One Two Three Electric

- Schneider Electric

- Siemens

- Vertiv Group

- Victron Energy

The Global Closed Transition Transfer Switch Market was valued at USD 1.1 billion in 2024 and is projected to expand at a CAGR of 7.3% from 2025 to 2034. The market is seeing steady growth due to the rising demand for reliable power transfer solutions in mission-critical environments. Sectors that require continuous, uninterrupted power for their operations, such as healthcare, data centers, and manufacturing, are increasingly adopting these switches to prevent equipment failures and maintain operational efficiency.

Government initiatives focused on modernizing power grids are contributing to market expansion. A notable boost comes from the growing integration of renewable energy, hybrid systems, and microgrids. As these technologies become more widespread, the need for reliable power transition systems becomes essential to maintaining consistent power flow. Additionally, stricter energy efficiency standards and the increasing use of automation technologies are playing a key role in driving market growth.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.1 Billion |

| Forecast Value | $2.2 Billion |

| CAGR | 7.3% |

The market segment using circuit breaker mechanisms is expected to exceed USD 1.2 billion by 2034. This growth is driven by the pressing need for uninterrupted power in industries where reliability is a critical factor. Circuit breaker-based transfer switches are ideal in these scenarios, offering seamless power transitions that minimize downtime and protect sensitive equipment. This demand is further fueled by the expansion of renewable energy sources and advancements in smart grid technologies, which require enhanced fault protection and stable power flow.

The market for closed transition transfer switches in critical operations is set to grow rapidly, with a projected CAGR exceeding 8% through 2034. This surge in demand is linked to industries that rely heavily on a continuous power supply, where even minor interruptions can have significant consequences. Consequently, businesses are investing more in backup power solutions, such as uninterruptible power supplies (UPS) and backup generators, to safeguard their operations against power outages. The increased use of automation, smart grids, and renewable energy, along with a focus on meeting energy efficiency standards, further drives this growth.

In the U.S., the market for closed transition transfer switches is expected to surpass USD 420 million by 2034. This growth is driven by the increasing demand for reliable power transfer systems in sectors like healthcare, manufacturing, and data management. The adoption of renewable energy and smart grid technologies is accelerating the need for these systems. As power outages and equipment protection concerns rise, the market for closed transition transfer switches continues to thrive, providing industries with a dependable solution for seamless power transitions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Strategic dashboard

- 4.2 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Operations, 2021 – 2034 (‘000 Units, USD Million)

- 5.1 Key trends

- 5.2 Manual

- 5.3 Non-automatic

- 5.4 Automatic

- 5.5 By-pass isolation

Chapter 6 Market Size and Forecast, By Switching Mechanism, 2021 – 2034 (‘000 Units, USD Million)

- 6.1 Key trends

- 6.2 Contactor

- 6.3 Circuit breaker

Chapter 7 Market Size and Forecast, By Ampere Rating, 2021 – 2034 (‘000 Units, USD Million)

- 7.1 Key trends

- 7.2 ≤ 400 Amp

- 7.3 401 Amp to 1600 Amp

- 7.4 > 1600 Amp

Chapter 8 Market Size and Forecast, By Installation, 2021 – 2034 (‘000 Units, USD Million)

- 8.1 Key trends

- 8.2 Emergency systems

- 8.3 Legally required systems

- 8.4 Critical operations power systems

- 8.5 Optional standby systems

Chapter 9 Market Size and Forecast, By Region, 2021 – 2034 (‘000 Units, USD Million)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.2.3 Mexico

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 Russia

- 9.3.4 UK

- 9.3.5 Italy

- 9.3.6 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 South Korea

- 9.4.4 India

- 9.4.5 Australia

- 9.5 Middle East & Africa

- 9.5.1 UAE

- 9.5.2 Saudi Arabia

- 9.5.3 South Africa

- 9.6 Latin America

- 9.6.1 Brazil

- 9.6.2 Argentina

Chapter 10 Company Profiles

- 10.1 AEG Power Solutions

- 10.2 ABB

- 10.3 Briggs & Stratton

- 10.4 Caterpillar

- 10.5 Cummins

- 10.6 Eaton

- 10.7 General Electric

- 10.8 Generac Power Systems

- 10.9 Kohler

- 10.10 Midwest Electric Products

- 10.11 One Two Three Electric

- 10.12 Schneider Electric

- 10.13 Siemens

- 10.14 Vertiv Group

- 10.15 Victron Energy