デジタルツイン(DT):市場シェア分析、業界動向と統計、成長予測(2026年~2031年)

Digital Twin (DT) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)- 発行日

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日

- 商品コード

- 1939748

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 適宜更新あり 本レポートは最新情報反映のため適宜更新し、内容構成変更を行う場合があります。ご検討の際はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

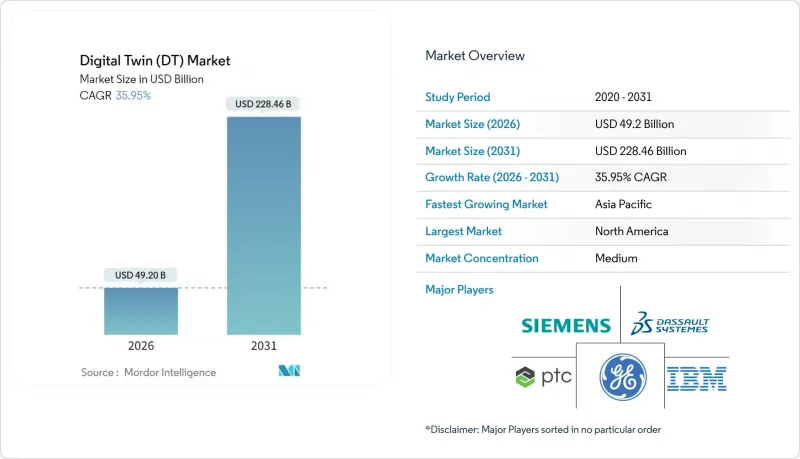

デジタルツイン市場は2025年に361億9,000万米ドルと評価され、2026年の492億米ドルから2031年までに2,284億6,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは35.95%と見込まれます。

追い風となる要因としては、産業用IoTプラットフォームの成熟化、エッジAIの広範な導入、安全上重要なインフラに対する規制要件が挙げられます。確立されたスマート工場投資により、製造業が最大の応用分野であり続けていますが、過酷な稼働環境下での資産健全性の向上を求める生産者の需要により、石油・ガス分野が最も強い成長を示しています。地域別では、北米が首位を維持していますが、中国、インド、日本における公共プログラムが大規模デジタル化へ資金を投入していることから、アジア太平洋地域が差を縮めつつあります。現在の支出の大半はソリューションが占めていますが、企業が統合ノウハウを求める中、サービス分野も急速に拡大しています。クラウド導入はオンプレミス型を上回る成長率を示しており、遠隔データ管理の安全対策やスケーラブルなアーキテクチャへの信頼が高まっていることを示しています。サイバーセキュリティの脆弱性や物理ベースモデリング人材の不足が成長見通しを抑制する要因となっていますが、導入の主要な方向性を変えるには至っていません。

世界のデジタルツイン(DT)市場の動向と洞察

産業用IoTプラットフォームの急速な成長

広範なIIoT導入によりリアルタイムデータが供給され、デジタルモデルと工場現場の同期が維持されています。シーメンスは2024年にXceleratorエコシステムの強みを背景に、デジタル事業収益が90億ユーロ(97億2,000万米ドル)と前年比22%増を記録しました。ハネウェルのForgeプラットフォームは1日30億以上のデータポイントを処理し、顧客工場における計画外ダウンタイムを35%削減しています。OPC UAやMQTTなどの標準化されたプロトコルは統合の摩擦を軽減し、工場が数か月ではなく数週間でデジタルツインを導入することを可能にします。その結果、着実なコスト削減、迅速な根本原因分析、より予測可能なキャパシティ計画が実現します。

デバイスレベルでのエッジ/AI推論の拡大

分析処理をクラウドからエッジへ移行することで、遅延を削減しデータ主権を維持します。マイクロソフトとシーメンスが共同開発した産業用基盤モデルは、資産レベルで推論を実行し、異常検知においてミリ秒単位の応答を可能にします。アウディでは現在、エッジに展開されたツインを通じて仮想PLCを運用し、実際の製造ラインにおけるサイクルタイムの最適化を実現しています。ローカルシミュレーションでは例外データのみが上流へ送信されるため、帯域幅の消費も抑制されます。専用チップとコンテナ化されたランタイムにより、二次サプライヤーの展開コストがさらに削減され、バリューチェーン全体でのAI対応ツインの普及が加速しています。

IT/OTスタック全体におけるサイバーフィジカルセキュリティの脆弱性

スペイン国立サイバーセキュリティ研究所は、ITとOTを橋渡しするツインが攻撃対象領域を拡大し、プロセスコントローラーをデータ完全性脅威に晒すと指摘しています。最近のランサムウェア被害では、メーカーがツインデータレイクの浄化作業のため数日間の生産停止を余儀なくされました。ゼロトラストアーキテクチャの統合やスタッフ研修により、平均18ヶ月の導入遅延が発生しています。マルチテナントツインは、協業速度を低下させずにパートナーアクセスをセグメント化する必要があるため、複雑性を増しています。

セグメント分析

2025年、製造業はデジタルツイン市場の35.10%を占めました。これは組み込み型IIoTセンサー、予知保全プログラム、継続的改善文化によるものです。自動車・電子機器工場ではラインレベルのデジタルツインを導入し、タクトタイムの変動や品質・歩留まりのパターンを分析することで、廃棄率を二桁単位で削減しています。特に資源集約型の冶金・セメント事業では、エネルギー効率の向上がさらなる投資回収効果をもたらします。このセグメントは着実に拡大し、他業種が追いつく中でも数量面での優位性を維持すると予測されます。

石油・ガス分野は現在規模が小さいもの、海洋事業者による遠隔点検・故障隔離機能の需要から、2031年までにCAGR28.1%で拡大すると予測されます。上流部門では地震データと生産記録を統合した貯留層ツインを導入し、エンジニアが掘削装置を動員する前に坑井改修シナリオをシミュレーション可能にしています。中流企業ではパイプライン・ツインを漏洩検知に活用し、下流の精製所(例:シェル)ではDNV基準で検証されたツイン技術により計画外ダウンタイムを20%削減した実績があります。政府の脱炭素化目標も導入を促進しており、ツイン技術はフレア最小化や熱統合戦略の最適化に貢献します。両セグメントにおいて、AI支援シナリオテストによりツインは監視から意思決定支援システムへと進化し、導入全体のシェアを拡大しています。

ソリューションカテゴリー(ソフトウェアプラットフォーム、物理エンジン、接続ハードウェア)は、企業が中核機能を獲得した2025年に支出の62.85%を占めました。ベンダーはモデリングライブラリを可視化エンジンとバンドルし、プロセスエンジニアがゼロからコーディングせずにレプリカを構築できるようにしています。ライセンシングモデルは使用量ベースの階層へ移行し、ティア2サプライヤー間のアクセスを拡大しています。

一方、サービス分野はCAGR30%で急速に拡大しております。導入コンサルティングではデータパイプラインの調整、意味論的モデルの構築、シミュレーション精度の検証を実施。マネージドサービス契約ではツインの健全性指標監視、パッチ適用、ドリフト対策アルゴリズム調整を行い、資産所有者にとって予測可能な運用コストを実現します。成果ベースの契約が普及する中(ロールスロイス社のTotalCareはツイン分析を基盤としたエンジン稼働率を保証)、サービスパートナーはより多くのリスクを引き受け、請求時間を基準とするのではなく効率向上に連動した料金体系を採用しています。このモデルは顧客ロイヤルティを強化し、プラットフォームの継続的改善を促進します。

デジタルツイン市場レポートは、アプリケーション(製造業、エネルギー・電力、航空宇宙・防衛、石油・ガス、自動車、その他)、コンポーネント(ソリューション/プラットフォーム、サービス)、導入形態(オンプレミス、クラウド)、企業規模(大企業、中小企業(SME))、地域別に分類されています。

地域別分析

北米は、インダストリー4.0の早期導入、大規模な航空宇宙プログラム、産業用SaaSへの堅調なベンチャー資金調達を背景に、2025年のデジタルツイン市場収益の37.95%を占めました。米国航空規制当局によるシミュレーションベース認証の承認は、航空機OEMおよびティア1サプライヤーにおけるツイン投資の広範な促進につながっています。カナダおよび米国のエネルギー大手は、厳格化する環境政策に沿い、メタン漏洩率削減のためパイプラインおよびLNGターミナルのツインを導入しています。サイバー保険の成熟した枠組みと標準化されたデータ保護義務により、クラウド導入が特に進んでいます。

アジア太平洋地域は政府主導のメガプロジェクトに支えられ、26.0%という最高CAGRを記録しています。中国の「デジタル中国建設計画」では新規インフラに都市デジタルツインの構築を義務付け、国内外ベンダー向けの大型調達案件を生み出しています。インドの「サンガム・デジタルツイン計画」は、6G対応に向けた全国的な通信網アップグレードにネットワークツイン機能を統合しています。日本のNTTデジタルツインコンピューティングイニシアチブは、交通・災害対応アルゴリズムに情報を提供する都市規模の複製を支援します。韓国とシンガポールはスマート工場・スマート港湾のパイロット事業を推進し、リアルタイムのカーボンフットプリント追跡を重視しています。同地域のサプライチェーンにおける中心性により、ここで得られた知見は世界のOEMメーカーへ迅速に普及します。

欧州では規制要件が中心課題となり着実に進展しています。デジタル製品パスポートは製造業者に対し製品ライフサイクル全体のトレーサビリティ組み込みを義務付け、事実上大量生産品への軽量ツイン導入を必須としています。ドイツの「インダストリー4.0プラットフォーム」は標準化された管理シェルガイドラインを提供し、中小企業の統合負担を軽減しています。フランスは海軍建造における競争優位性維持のため仮想造船所ツインに投資し、北欧諸国は建築ツインを活用してネットゼロ基準を達成しています。中東・アフリカ地域は未成熟ながら有望です:UAEとサウジアラビアは油田ツインや巨大プロジェクト都市ツインのパイロット事業を実施し、大規模拡張前に効率性と持続可能性のメリットを追求しています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 産業用IoTプラットフォームの急速な成長

- デバイスレベルにおけるエッジ/AI推論の拡大

- 資産集約型産業における安全上重要なインフラのデジタル化に向けた規制推進

- 既存設備プロジェクトにおける設備投資(CAPEX)削減のための仮想試運転需要

- リアルタイム資産レプリカデータを必要とする成果ベースのサービス契約の台頭

- EUおよび米国におけるデジタル製品パスポートの普及

- 市場抑制要因

- IT/OTスタック全体におけるサイバーフィジカルセキュリティの脆弱性

- 特定分野における物理ベースモデリングの専門知識不足

- フェデレーテッドツインで生成されるデータの不透明な知的財産権の帰属

- 相互運用性を制限するシミュレーション標準の断片化

- 重要規制枠組みの評価

- バリューチェーン分析

- テクノロジーの展望

- ポーターのファイブフォース

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 主要利害関係者への影響評価

- 主要使用事例と事例研究

- 市場のマクロ経済的要因への影響

- 投資分析

第5章 市場セグメンテーション

- 用途別

- 製造業

- エネルギー・電力

- 航空宇宙・防衛

- 石油・ガス

- 自動車

- その他

- コンポーネント別

- ソリューション/プラットフォーム

- サービス

- 展開モード別

- オンプレミス

- クラウド

- 企業規模別

- 大企業

- 中小企業(SMEs)

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- 北欧諸国

- その他欧州地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- トルコ

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- ナイジェリア

- その他アフリカ

- 中東

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- ASEAN

- オーストラリア

- ニュージーランド

- その他アジア太平洋地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- ANSYS, Inc.

- AVEVA Group plc

- Bentley Systems, Incorporated

- Cal-Tek S.R.L.

- Cityzenith, Inc.

- Dassault Systemes SE

- General Electric Company

- Hexagon AB

- International Business Machines Corporation

- Lanner Group Limited(Royal HaskoningDHV)

- Mevea Ltd.

- Microsoft Corporation

- Oracle Corporation

- PTC Inc.

- Rescale, Inc.

- Robert Bosch GmbH(Bosch.IO)

- SAP SE

- Schneider Electric SE

- Siemens AG

- Amazon Web Services, Inc.

第7章 市場機会と将来の展望

- 発行日

- 発行

- Mordor Intelligence

- ページ情報

- 英文 135 Pages

- 納期

- 2~3営業日