|

市場調査レポート

商品コード

1687736

InGaAsカメラ- 市場シェア分析、産業動向・統計、成長予測(2025~2030年)InGaAs Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| InGaAsカメラ- 市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

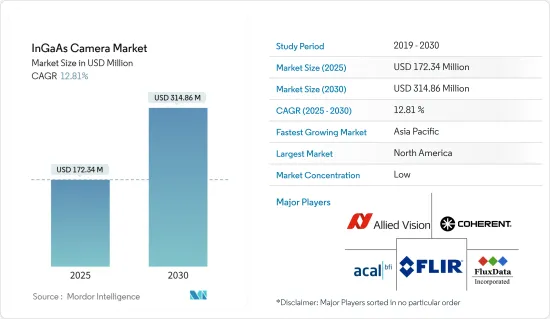

InGaAsカメラ市場規模は、2025年に1億7,234万米ドルと推定・予測され、予測期間(2025~2030年)のCAGRは12.81%で、2030年には3億1,486万米ドルに達すると予測されています。

ビジョンガイドロボットシステムなどの自動化ソリューションの採用が増加していること、汚染や欠陥検出のためにこれらのカメラの使用が増加していることが、調査した市場の成長を促進する重要な要因の1つです。

主要ハイライト

- InGaAsは、近赤外(NIR)と短波長赤外(SWIR)で高い光感度を持つIII-V族化合物半導体です。InGaAsカメラは、リアルタイムのインライン非破壊検査など、さまざまな用途でこの特長を利用しています。マシンビジョン向けのラインスキャンInGaAsカメラの需要の増加は、InGaAsカメラ市場の重要な促進要因です。

- InGaAsは、航空宇宙、軍事、通信、工業検査、分光などに使用される冷却ベースのカメラです。赤外線(IR)技術を持ち、夜間視認や大気中の霞を通した視認が可能で、主に軍や防衛軍で使用されています。小型、非冷却、軽量設計、高品質の暗視機能、付属の隠密アイセーフ・レーザー、対象認識、夜光に対する感度などの性能特性により、これらのカメラは防衛セグメントで多くの用途を見出しています。

- InGaAsカメラは、シリコン検出器がもはや機能しないNIR波長950~1,700nmと、シリコン検出器がもはや感度を持たない950~1,700nmの間のギャップを埋めています。バンドギャップが低いため、InGaAsはより包括的なNIR領域で感度を記載しています。Si-CCDと比較すると、バンドギャップが低いため、暗電流(熱によって発生する信号)も非常に高くなります。その結果、科学用InGaAs FPAカメラでは、不要なノイズ源を低減するために(-85℃まで)強力な冷却が必要となります。

- さらに、InGaAsは検出器材料として、湿度測定、表面膜分布、ポリマーと天然材料の分離などの選別作業といった近赤外(NIR)産業用途に手頃な代替手段を提供しました。その結果、工業生産とオートメーションにおける技術の利用が増加しています。

- インダストリー4.0は、ロボットなどの技術開発を加速させ、現在では産業オートメーションにおいて重要な役割を担っており、ロボットが産業における多くの中核業務を管理しています。InGaAsカメラの新しい用途には、ビジョン誘導ロボットなどがあります。これらのビジョンガイドロボットは、ビンからランダムな部品を見つけてピッキングするIRイメージャーと、各部品の向きを分析してベルトコンベアに載せるカメラで構成されています。

- さらに、マシンビジョンの使用は年々増加しています。一部の地域では、マシンビジョンの売上が過去最高を記録しています。Association for Advancing Automationによると、自動検査とガイダンス用のマシンビジョンは、2022年上半期も北米でプラス成長を続け、年間を通じて良好な市場成長が予測されています。このため、予測期間中、このような用途でInGaAsカメラの需要が高まることが予想されます。

- しかし、InGaAsカメラのコスト高が調査市場の成長を阻害する主要因の一つです。さらに、様々な国での厳しい輸出入規制の増加が、調査市場の開拓を抑制しています。

InGaAsカメラ市場動向

産業オートメーションが最大市場シェアを占める見込み

- 市場成長を促進する主要因の1つは、様々な用途におけるInGaAsカメラ需要の増加です。また、産業オートメーションセグメントでInGaAsカメラの使用が増加していることも市場成長を促進する要因の一つです。InGaAsカメラは、他のタイプのカメラよりも性能が高いため、サーマルイメージング、マシンビジョン、品質管理などの産業オートメーション用途で使用されています。

- マシンビジョンシステムの採用が増加していることから、産業オートメーションセグメントでのInGaAsカメラの需要が見込まれています。マシンビジョン環境では、カメラシステムは生産ラインで製品をスキャンするために使用されます。カメラは画像をキャプチャし、事前に定義された基準と比較します。

- さらに、マシンビジョンは、ロボットの有効性とビジネスにおける全体的な価値を向上させるために、ロボットと組み合わせて使用されることが多くなっています。このようなロボットには、手元のタスクをガイドするカメラがハンドポジションに取り付けられています。例えば、IFRの2023年版レポートによると、業務用ロボットの世界在庫は2022年に約350万台と過去最高を更新する予定です。一方、導入額は推定157億米ドルに達します。

- さらに、予測期間中に産業用ロボットの導入が増加すると予想されることから、調査対象市場では産業用セグメントからの需要がプラスに転じると見込まれます。IFRによると、産業用ロボットの年間導入台数は2024年までに51万8,000台に達する見込みです。

- さまざまな産業がこの技術を利用して生産を自動化し、製品の品質と速度を向上させています。様々な産業で高品質検査と自動化のニーズが高まっていることがマシンビジョン需要を牽引し、最終的にInGaAsカメラ市場を押し上げます。さらに、InGaAsカメラ市場の参入企業による研究開発の増加と新製品の発売が、InGaAsカメラ市場を大きく後押ししています。

- 例えば、2023年1月、Lucid Vision Labsは1.3MPと0.3MPの新製品Triton SWIR IP67規格産業用ビジョンカメラを発表しました。Triton SWIRはGigE PoEカメラで、広帯域・高感度のSony SenSWIR 1.3MP IMX990と0.3MP IMX991 InGaAsセンサを搭載しており、可視光と不可視光のスペクトルで画像をキャプチャでき、ピクセルサイズは5mです。

北米が最大の市場シェアを占める見込み

- 軍事・防衛用途でUAVやUGVのようなロボットの使用が増加していることから、北米ではInGaAsカメラの需要が増加すると予想されます。さらに、産業セグメントでのオートメーションや先端技術の普及が進んでいることも、同地域の研究市場の成長を後押ししています。

- 企業、学術機関、連邦政府に最先端のオートメーション技術への投資を奨励することを目的とした先進製造パートナーシップのような政府プログラムの結果、マシンビジョンシステムの生産は増加します。これにより、市場の成長に明るい展望が生まれると考えられます。

- InGaAsカメラは、煙、霧、霞、水蒸気などの悪条件を見通すために軍事・防衛セグメントで広く使用されているため、米国のような国々は防衛予算と先端機器への支出を増やしています。例えば、米国では2023会計年度に8,133億米ドルの国防予算を要求しています。このような国防支出は、市場の需要を促進すると予想されます。

- さらに、シリコンウエハーのパターン検査などの用途でInGaAsカメラの需要が増加している半導体産業は、米国を中心とした北米地域で牽引力を増しています。米国CHIPS法などの好意的な政府投資やベンダーによるチップ産業への投資が、予測期間中のInGaAsカメラ需要を促進すると予想されます。

- InGaAsカメラは、光干渉断層計(OCT)や分光法などの医療画像用途において、高感度・低ノイズを実現します。米国、カナダなどの国々は、医療産業の発展に絶えず投資しており、医療画像用途におけるInGaAsカメラの使用増加の成長機会を促進すると期待されています。

- 北米のInGaAsカメラ市場は、この地域で活動する様々なエンドユーザーからの高度で効果的なイメージングシステムに対する需要が着実に増加しているため、予測される期間中に良好な成長率を経験すると予測されています。さらに、ロボットの普及に伴う産業オートメーションの進歩や、防衛・軍事産業における政府支出は、今後数年間市場を牽引すると予想されます。

InGaAsカメラ産業概要

InGaAsカメラ市場は、多くの大手企業や新規参入企業によって構成されているため、競争が激しいです。各社は消費者需要の増加に対応するため、既存製品の革新に努めており、市場競争を激化させています。さらに、需要の高まりが新たな参入企業を引き付け、市場をセグメント化しています。主要参入企業としては、Allied Vision Technologies GmbH、Acal BFI Limited Company、Coherent Inc.、Flir Systems Inc.などが挙げられます。

2022年12月、JAIは、複数のCMOSセンサと短波長赤外(SWIR)スペクトルから画像データを収集するためのインジウムガリウムヒ素(InGaAs)技術によるセンサで構成される4センサラインスキャン技術を特徴とする新しい産業用プリズムベースラインスキャンカメラ、SW-4010Q-MCLの発売を発表しました。

2022年11月、Allied Visionは、1.9μmまたは2.2μmまでの波長を高い量子効率で検出できるInGaAsセンサを拡大搭載したGoldeye SWIRカメラ4機種の発売を発表しました。統合されたデュアルステージセンサ冷却といくつかのオンボード画像補正機能は、卓越した画質で特定のスペクトル特徴を可視化するための重要な要因の一つです。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- 技術スナップショット

- 非冷却

- 冷却

- 市場促進要因

- マシンビジョン用途の採用増加

- 軍事・防衛活動における需要の高まり

- 市場課題

- InGaASカメラの高い調達コスト

- 輸出入に関する厳しい規制

- COVID-19の産業への影響評価

第5章 市場セグメンテーション

- 用途別

- 軍事・防衛

- 産業オートメーション

- モニタリングとセキュリティ

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- アジア

- 中国

- インド

- 日本

- オーストラリア・ニュージーランド

- 東南アジア

- ラテンアメリカ

- 中東・アフリカ

- 北米

第6章 競合情勢

- 企業プロファイル

- Allied Vision Technologies GmbH(TKH group)

- Acal BFI Limited Company(Discoverie Group PLC)

- Coherent Inc.

- Flir Systems Inc.

- FluxData Inc.

- Hamamatsu Photonics KK

- Lambda Photometrics Ltd.

- New Imaging Technologies

- Specim Spectral Imaging Ltd.

- Raptor Photonics Ltd.

- Sensors Unlimited(Collins Aerospace Company)

- Teledyne Dalsa Inc.(Teledyne Technologies Incorporated)

- Xenics Inc.

第7章 投資分析

第8章 市場機会と今後の動向

The InGaAs Camera Market size is estimated at USD 172.34 million in 2025, and is expected to reach USD 314.86 million by 2030, at a CAGR of 12.81% during the forecast period (2025-2030).

The increasing adoption of automation solutions, such as vision-guided robotic systems, and the increasing use of these cameras for contamination and defect detection are among the significant factors driving the growth of the studied market.

Key Highlights

- InGaAs is an III-V compound semiconductor with high photosensitivity in the near-infrared (NIR) and short-wave infrared (SWIR). The InGaAs camera uses this feature in various applications, including real-time in-line non-destructive inspection. The rise in demand for line scan InGaAs cameras for machine vision applications is a crucial driver of the InGaAs camera market.

- InGaAs are cooling-based cameras used in aerospace, military, telecommunications, industrial inspection, and spectroscopy. It has infrared (IR) technology, which allows for night vision or visibility through atmospheric haze and is primarily used by military and defense forces. Because of their performance characteristics, such as small, uncooled, lightweight design, high-quality night vision, attached covert eye-safe lasers, target recognition, and sensitivity to nightglows, these cameras find many applications in defense.

- InGaAs cameras bridge the gap between NIR wavelengths 950-1700 nm, where silicon detectors no longer work, and 950 - 1700 nm, where silicon detectors are no longer sensitive. Because of its lower bandgap, InGaAs provide sensitivity over a more comprehensive NIR range. When compared to Si-CCDs, the lower bandgap is also responsible for a much higher dark current (thermally generated signal). As a result, scientific InGaAs FPA cameras require intense cooling (down to -85°C) to reduce some unwanted noise sources.

- Moreover, as a detector material, InGaAs provided an affordable alternative for near-infrared (NIR) industrial applications such as humidity measurement, surface film distributions, and sorting tasks such as separating polymers from natural materials. As a result, the use of technology in industrial manufacturing and automation is increasing.

- Industry 4.0 accelerated the development of technologies such as robots, which now play a critical role in industrial automation, with robots managing many core operations in industries. New applications for InGaAs cameras include vision-guided robotics and automated butchering. These vision-guided robots are made up of IR imagers that find and pick random parts from a bin, followed by a camera that analyzes the orientation of each part and places it on a conveyor belt.

- Furthermore, the use of machine vision is increasing year after year. Machine vision sales are at an all-time high in some regions. According to the Association for Advancing Automation, machine vision for automated inspection and guidance continued its positive growth trajectory in North America in the first half of 2022, with favorable market growth predicted throughout the year. This is expected to drive demand for InGaAs cameras in such applications during the forecast period.

- However, the higher cost of InGaAs cameras is one of the major factors impeding the growth of the studied market. Furthermore, a rise in stringent import and export regulations across various countries restrains the development of the studied market.

InGaAs Camera Market Trends

Industrial Automation Expected to Occupy the Largest Market Share

- One of the key factors driving market growth is the increasing demand for InGaAs cameras in various applications. Another factor driving market growth is the increasing use of InGaAs cameras in the industrial automation sector. InGaAs cameras are used in industrial automation applications like thermal imaging, machine vision, and quality control because they outperform other types of cameras.

- The increasing adoption of machine vision systems is expected to drive demand for InGaAs cameras in the industrial automation segment. In a machine vision environment, a camera system is used to scan products on a production line. The camera captures the image and compares it to pre-defined criteria.

- Moreover, machine vision is increasingly being used in conjunction with robots to improve their effectiveness and overall value to the business. These robots have a camera mounted at the hand position that guides them through the task at hand. For example, according to IFR's 2023 report, the global stock of operational robots was to reach a new high of approximately 3.5 million units in 2022. In the meantime, the value of installations reached an estimated USD 15.7 billion.

- Furthermore, with the adoption of industrial robots expected to increase over the forecast period, the studied market is expected to see a positive increase in demand from the industrial segment. The annual installation of industrial robots is expected to reach 518 thousand units by 2024, according to IFR.

- Different industries use this technology to automate production and improve product quality and speed. The growing need for high-quality inspection and automation in various industries drives the demand for machine vision, eventually boosting the InGaAs camera market. Furthermore, increased R&D and the launch of new products by InGaAs camera market players are propelling the InGaAs camera market significantly.

- For instance, in January 2023, Lucid Vision Labs unveiled its brand-new 1.3MP and 0.3MP Triton SWIR IP67-rated industrial vision cameras. The Triton SWIR is a GigE PoE camera with wide-band and high-sensitivity Sony SenSWIR 1.3MP IMX990 and 0.3MP IMX991 InGaAs sensors capable of capturing images in visible and invisible light spectrums and a pixel size of 5m.

North America is Expected to Account for the Largest Market Share

- The rising use of robotics like UAVs and UGVs in military and defense applications is expected to increase demand for InGaAs cameras in North America. Moreover, higher penetration of automation and advanced technologies in the industrial domain favors the growth of the studied market in the region.

- The production of machine vision systems will be increased as a result of government programs like the Advanced Manufacturing Partnership, which aims to encourage businesses, academic institutions, and the federal government to invest in cutting-edge automation technologies. This will create a positive outlook for the market's growth.

- As InGaAs cameras are widely used in the military and defense sector to see through unfavorable conditions such as smoke, fog, haze, and water vapor, countries like the United States have increased their defense budgets and expenditure on advanced equipment. For example, a budget request for national defense of USD 813.3 billion in the United States has been made for the fiscal year 2023. Such defense spending is expected to drive market demand.

- Furthermore, the semiconductor industry, where demand for InGaAs cameras in applications such as silicon wafer pattern inspection is increasing, is gaining traction in the North American region, particularly in the United States. Favorable government investments, such as the US CHIPS Act, and vendor investments in the chip industry are thus expected to drive demand for InGaAs cameras during the forecast period.

- InGaAs cameras provide high sensitivity and low noise in medical imaging applications such as optical coherence tomography (OCT) and spectroscopy. Countries such as the United States, Canada, and others are constantly investing in advancing their medical industries, which is expected to drive growth opportunities in the increasing use of InGaAs cameras in medical imaging applications.

- The InGaAs camera market in North America is anticipated to experience favorable growth rates during the anticipated period due to the steadily increasing demand for advanced and effective imaging systems from various end-users operating in the area. Furthermore, advancements in industrial automation with the widespread adoption of robots and government spending in the defense and military industries are expected to drive the market in the coming years.

InGaAs Camera Industry Overview

The InGaAs camera market is competitive due to the market consisting of many large players as well as new players. Companies are trying to innovate their existing products to cater to increasing consumer demand, making the market competitive. Furthermore, the growing demand attracts new players, making the market fragmented. Some of the major players are Allied Vision Technologies GmbH, Acal BFI Limited Company, Coherent Inc., and Flir Systems Inc., among others.

In December 2022, JAI announced the launch of SW-4010Q-MCL, a new industrial prism-based line scan camera featuring 4-sensor line scan technology consisting of multiple CMOS sensors and a sensor based on indium gallium arsenide (InGaAs) technology to collect image data from the short wave infrared (SWIR) spectrum.

In November 2022, Allied Vision announced the launch of four new Goldeye SWIR camera models equipped with an extended range of InGaAs sensors, capable of detecting wavelengths up to 1.9 μm or 2.2 μm at high quantum efficiencies. The integrated dual-stage sensor cooling and several onboard image correction features are among the key factors to make specific spectral features visible with outstanding image quality.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview?

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Technology Snapshot

- 4.4.1 Uncooled

- 4.4.2 Cooled

- 4.5 Market Drivers

- 4.5.1 Increasing Adoption in Machine Vision Applications

- 4.5.2 Rising Demand in Military and Defense Operations

- 4.6 Market Challenges

- 4.6.1 High Procurement Cost of InGaAS Cameras

- 4.6.2 Stringent Regulation on Export and Import

- 4.7 Assessment of Impact of COVID-19 on the Industry

5 MARKET SEGMENTATION

- 5.1 By Application

- 5.1.1 Military and Defense

- 5.1.2 Industrial Automation

- 5.1.3 Surveillance and Security

- 5.1.4 Other Applications

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 United Kingdom

- 5.2.2.2 Germany

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.3 Asia

- 5.2.3.1 China

- 5.2.3.2 India

- 5.2.3.3 Japan

- 5.2.3.4 Australia and New Zealand

- 5.2.3.5 South East Asia

- 5.2.4 Latin America

- 5.2.5 Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Allied Vision Technologies GmbH (TKH group)

- 6.1.2 Acal BFI Limited Company (Discoverie Group PLC)

- 6.1.3 Coherent Inc.

- 6.1.4 Flir Systems Inc.

- 6.1.5 FluxData Inc.

- 6.1.6 Hamamatsu Photonics KK

- 6.1.7 Lambda Photometrics Ltd.

- 6.1.8 New Imaging Technologies

- 6.1.9 Specim Spectral Imaging Ltd.

- 6.1.10 Raptor Photonics Ltd.

- 6.1.11 Sensors Unlimited (Collins Aerospace Company)

- 6.1.12 Teledyne Dalsa Inc. (Teledyne Technologies Incorporated)

- 6.1.13 Xenics Inc.