|

市場調査レポート

商品コード

1641990

ボールバルブ:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Ball Valve - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ボールバルブ:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

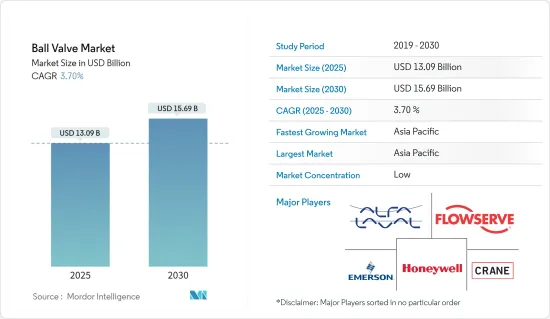

ボールバルブ市場規模は2025年に130億9,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは3.7%で、2030年には156億9,000万米ドルに達すると予測されています。

石油・ガス需要の大幅な増加は、ボールバルブ市場の成長に寄与する重要な要因の1つであると予想されます。さらに、急速な工業化と都市化も新興国市場の開拓を支える重要な要因です。

主要ハイライト

- ボールバルブは基本的に1/4回転で作動するバルブであり、確実なシャットオフを提供する能力により、産業用途のクリーンなガス、圧縮空気、液体サービスに適しています。しかし、スラリーサービスに使用する場合は、破片の蓄積を防ぐ対策を講じる必要があります。さらに、これらのバルブは非常に頑丈で、単純なオン/オフ動作を必要とする用途に非常に適しています。また、耐久性が高く、何度使用しても安定した性能を維持します。

- ボールバルブは石油・ガス生産設備で最も広く採用されている流体遮断弁です。これらのバルブは、炉に供給する燃料ガスシステムにも使用されています。このような用途から、産油地域や巨大な石油精製能力を持つ地域は、製品ベンダーにとって魅力的な対象となっています。さらに、このようなプラントは入札浮動で開発されるため、このようなソリューション・プロバイダーと提携・協力関係にある市場ベンダーは競争上有利になると予想されます。

- あらゆる種類の材料の中で、ステンレスは耐腐食性が高いため、重要性を増しており、今後もその重要性が確認されると予想されます。バルブは頻繁に開閉するため、腐食は重大な問題を引き起こす可能性があります。これらのバルブは、食品加工工場に利益をもたらすことができる過酷な水タイプにはるかに良い持ちこたえます。ステンレスバルブは、真鍮などの他の材料よりも高い定格圧力を持っているという事実は、さらにその採用を推進しています。

- さらに、バルブのポートや弁座の数によって、一方向、双方向、多方向など、さまざまなタイプのボールバルブが利用できることも、工業的な採用を補完しています。これらのバルブは、高圧パイプライン用、低圧パイプライン用の分類に基づいて製造され、使用事例をさらに広げています。複数のベンダーが常に革新的な新製品に投資しており、これが市場を牽引する大きな要因の一つとなっています。

- スマートバルブの出現や自動化・制御システムの組み込みを含むバルブ技術の進歩は、市場に新たな展望をもたらしています。環境問題への関心の高まりや規制の義務化は、環境に優しくエネルギー効率の高いバルブの必要性に拍車をかけています。排出を最小限に抑え、低リーク率でエネルギー効率を高めたボールバルブを提供するメーカーは、サステイナブルソリューションに対する需要の拡大を捉えることができます。

- バタフライバルブのような代替バルブタイプはステムが小さく弱い傾向にあるため、ボールバルブは一般的に大きな口径で採用されています。洋上掘削プラットフォームや浮体式生産貯蔵積出設備(FPSO)のような、スペースの制約や構造的負荷が最も重要な状況では、ユーザーはボールバルブに代わるものを選びます。さらに、流量制御の精度が限られていることが、調査された市場の成長に対する課題となっています。

ボールバルブ市場の動向

食品加工産業が重要な用途を持つ見込み

- 食品加工産業は、ボールバルブが重要な用途を見つける注目すべきセクターです。製品の充填プロセスでは、調整された流れを維持する必要があり、ボールバルブが不可欠なコンポーネントとなっています。この産業で使用されるバルブには、材料に直接接触するもでは、水や蒸気などの公益事業サービスで使用されるもの2種類があります。どちらの場合も、バルブはいくつかの産業規制、特に食品材料に接触するものに準拠しなければなりません。このことは、メーカーにとって規制認可を得るための大きな課題であり、厳しい産業基準を満たすバルブを設計する必要があります。

- ボールバルブは、大容量、温度、圧力の制御と維持において非常に効率的です。飲食品セグメントでは、サニタリーボールバルブは搬送パイプの接続と調整に使用され、ステンレス製であるため、搬送中の流体の純度、安定性、品質を保証します。また、サニタリーバルブは消毒や洗浄が容易で、衛生を促進します。様々なベンダーが継続的に製品を発表しているため、市場の成長が見込まれています。

- 例えば、2022年11月、作動バルブと機器制御のメーカーであるValworxは、最近、飲食品製造セグメントでの展開に適した衛生的なボールバルブの新シリーズを発表しました。これらのボールバルブは、目立つ位置インジケーターを装備し、NamurとISOマウントに対応しています。バルブは2方弁と3方弁があり、0.5インチから4インチまで様々なサイズがあります。バルブの新しい製品ラインは、FDA、USDA、3-A規格に適合しています。

- ステンレスは、食品加工セグメントでは重要な懸念事項である腐食に対して幅広い耐性を持つため、ますます重要な材料として認識されるようになっています。これらのバルブはまた、より攻撃的な水の組成にさらされたときに優れた耐久性を実証し、食品加工工場に顕著な利点を提供しています。さらに、ステンレスバルブは、真鍮のような代替材料と比較して、より高い定格圧力を有しています。例えば、典型的な1インチの真鍮製ボールバルブの定格圧力は600 PSIですが、同じサイズの標準的なステンレス製ボールバルブの定格圧力は1,000 PSIです。この特性は、食品加工産業の高圧用途に特に適しています。

- 世界の様々な地域で都市化率が高まっており、包装食品の需要が大幅に高まっています。また、特に都市部におけるライフスタイルの変化も、包装・加工食品に対する需要が増え続ける一因となっています。食料安全保障を確保し、自給自足の目標を達成するため、各国は食品加工産業を発展させるための規制改正や経済特区の開発などの努力を行っています。

- 人口問題ラボによると、2023年時点で世界の都市化率は57%に達しています。北米、ラテンアメリカ、カリブ海諸国は、80%を超える都市人口を誇り、その先頭を走っています。

- 調査対象市場の成長にとって有利なシナリオは、他の国々でも観察されています。インド産業・国内貿易振興省は、2022年のインドにおける食品加工部門への投資予定額は1,203億7,000万インドルピー(14億7,000万米ドル)と報告しました。インド食品加工産業省は、PLIスキームの実施を含め、バリューチェーン全体にわたる投資を奨励する取り組みを行っており、2026-27年までに食品加工能力を3,000億インドルピー(36億米ドル)近く拡大し、直接的・間接的な追加雇用を創出することが期待されています。このようなイニシアチブはボールバルブに大きな機会を提供すると予想されます。

北米が大きな市場シェアを占めると予想される

- 北米は、石油・ガス、電力、食品包装、化学など多様な産業で大きな需要を誇るボールバルブの有力市場です。米国とカナダは莫大な需要を示しており、産業オートメーションの迅速な統合がさらに拍車をかけています。この動向は、同地域におけるボールバルブ市場の需要を刺激すると予想されます。

- 北米地域では、インテリジェントボールバルブへの要求が高まっています。この地域の主要産業は、中央制御ステーションを通じて調整される先進的モニタリング技術を補完するために、プロセッサとネットワーク機能を組み込んだボールバルブに移行しています。プロセス産業における自動化の採用の増加は、この需要動向をさらに強化します。

- 米国は、カナダとは対照的に、地域の需要を拡大する上で極めて重要な役割を担っています。米国では、石油・ガス、精製、発電を中心に、ほぼすべてのエンドユーザー部門で需要が伸びています。エネルギー消費量の増加が、これらのセクターにおける需要増加の主要要因です。例えば、EIAによると、2022年の米国の即時エネルギー消費総量は約102.92クアドリリオンBtuで、そのうち石油消費量は約31%でした。

- さらに、石油・ガスやその他の石油製品に対する需要の高まりも、石油生産者の増産や新たな採油地の開拓を後押ししており、調査対象市場のさらなる成長が期待されています。例えば、2022年11月、カナダエネルギー請負業者協会(CAOEC)は、2023年にはカナダで約6,409の坑井が掘削される見込みであり、2022年から約15%増加すると発表しました。

- 地域の人口増加や様々なセグメントでの水消費量の増加が予想されるため、ボールバルブの需要を賄うために新たな水処理施設が地域に設置される可能性が高いと予想されています。注目すべき例としては、2022年9月にニューヨーク州当局が発表した、7つの自治体の上下水道インフラプロジェクトに2億3,200万米ドル以上を割り当てたことが挙げられます。ニューヨーク州環境施設公社は、累積支出が7億6,300万米ドルを超える水インフラ構想を促進するため、資金を供与し、低コストの融資包装を提供しました。処理場設立のためのこれらの投資は、必然的にボールバルブの必要性を増大させています。

- ボールバルブは圧力と流量を調整するために利用されます。その漏れにくい性質は、特に液体を扱う化学産業で非常に有利に働く特筆すべき特性です。2022年7月、BASFはルイジアナ州アセンションパリッシュにある化学製造コンプレックスの生産能力を倍増させることを目的とした7億8,000万米ドル相当のプロジェクトへの最終投資決定を宣言しました。この拡大プロジェクトは7年以上にわたるもので、合わせて10億米ドル以上の資本投資となり、同社は北米全域の建設、民生用電子機器、道路運送、自動車など様々なセグメントでの製品需要の増加に対応できるようになります。

ボールバルブ産業概要

ボールバルブ市場は細分化されており、複数の参入企業で構成されているが、現在大きなシェアを占めているグループはないです。各社は製品の専門性を高めるため、合併や買収を行っています。同市場は消費者層が広いため、有利な投資機会と見られています。主要市場参入企業には、Flowserve Corporation、Alfa Laval、Crane Co.、Honeywell International Inc.などがあります。

- 2023年11月-Alfa Lavalは、新たに2つのバルブを追加し、バルブポートフォリオを拡大。新しいバルブ、Unique Mixproof ProcessとUnique Mixproof CIPは、媒体を常に分離することで製品の安全性を高めます。また、完全バランス設計により、高圧でのリスクフリーな取り扱いが可能になります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- COVID-19の市場への影響

第5章 市場力学

- 市場促進要因

- 各国における工業化の進展

- プロセス安全性に対する需要の高まり

- 市場課題

- バルブの修理によるダウンタイム

第6章 市場セグメンテーション

- 材料別(定性分析)

- 鋳鉄

- 鋼鉄

- 合金ベース

- その他

- エンドユーザー産業別

- 石油・ガス

- 化学

- 水・廃水

- 電力

- 飲食品

- 製薬

- その他

- 地域別

- 北米

- 欧州

- アジア

- オーストラリア・ニュージーランド

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- ALFA LAVAL

- CIRCOR International Inc.

- Crane Co.

- Castel SRL

- Sanhua USA

- Curtiss-Wright Corporation

- Danfoss A/S

- Emerson Electric Co

- Georg Fischer Ltd

- Flowserve Corporation

- Hitachi Ltd

- Honeywell International Inc.

- KITZ Corporation

- Mueller Water Products Inc

第8章 投資分析

第9章 市場の将来展望

The Ball Valve Market size is estimated at USD 13.09 billion in 2025, and is expected to reach USD 15.69 billion by 2030, at a CAGR of 3.7% during the forecast period (2025-2030).

A significant rise in the demand for oil and gas is expected to be one of the significant factors contributing to the ball valve market growth. Additionally, rapid industrialization and urbanization are other essential factors supporting the development of the studied market.

Key Highlights

- The ball valve is essentially a valve that requires a quarter-turn to operate and is well-suited for clean gas-compressed air and liquid service in industrial applications, owing to its ability to provide a secure shutoff. However, when used for slurry service, measures must be taken to prevent the accumulation of debris. Furthermore, these valves are incredibly robust and highly suitable for applications requiring a simple on/off action. They're also highly durable and maintain consistent performance even after many use cycles.

- Ball valves are the most widely adopted fluid shutoff valves among oil and gas production facilities. These valves are also used in fuel gas systems feeding furnaces. Such applications make the oil-producing regions and regions with huge oil refining capacities attractive targets for the product vendors. Furthermore, as such plants are developed on tender floatation, the market vendors with partnerships and collaborations with such solution providers are expected to have a competitive advantage.

- Among all the types of materials, stainless steel is gaining and is expected to witness importance since they are more corrosion-resistant. Because valves open and close frequently, corrosion can cause significant issues. These valves hold up much better to harsher water types, which can benefit food processing plants. The fact that stainless steel valves also have a higher pressure rating than other materials, such as brass, further drives their adoption.

- Furthermore, the availability of ball valves in different variants, such as unidirectional, bidirectional, or multi-directional, depending on valve ports and the valve seat number, also complements their industrial adoption. These valves are also manufactured based on the classification for high-pressure or low-pressure pipelines, further expanding their use cases. Several vendors are constantly investing in innovative new products, which is acting as one of the major factors driving the market.

- The advancements in valve technology, including the emergence of smart valves and the incorporation of automation and control systems, present fresh prospects in the market. The rising environmental concerns and regulatory mandates fuel the need for eco-friendly and energy-efficient valves. Manufacturers who provide ball valves with minimized emissions, low leakage rates, and enhanced energy efficiency can seize the expanding demand for sustainable solutions.

- Ball valves are commonly employed in larger bore sizes, as alternative valve types like butterfly valves tend to have smaller and weaker stems. In situations where space constraints and structural load are paramount, such as offshore drilling platforms and floating production storage and offloading (FPSOs), users opt for alternatives to ball valves. Furthermore, the limited precision in flow rate control poses a challenge to the growth of the examined market.

Ball Valve Market Trends

Food Processing Industry Expected to Have Significant Applications

- The food processing industry is a notable sector where ball valves find significant application. The process of product fillings necessitates the maintenance of a regulated flow, making ball valves an essential component. The valves employed in the industry are of two types: those that come in direct contact with the material and those used in utility services such as water and steam. In both cases, the valves must comply with several industry regulations, particularly those that come in contact with food material. This presents a considerable challenge for manufacturers to obtain regulatory approvals, requiring them to design valves that meet stringent industry standards.

- Ball valves are highly efficient in controlling and maintaining high volume, temperature, and pressure. In the food and beverage sector, sanitary ball valves are utilized to connect and regulate conveyance pipes, ensuring the purity, stability, and quality of fluids during transport due to their stainless steel construction. Sanitary valves are also easy to disinfect and clean, promoting hygiene. The market is expected to grow due to continuous product launches by various vendors.

- For instance, in November 2022, Valworx, a producer of actuated valves and equipment controls, recently introduced a novel range of hygienic ball valves suitable for deployment in the food and beverage manufacturing sector. These ball valves are equipped with a conspicuous position indicator and are compatible with Namur and ISO mountings. The valves are obtainable in two- and three-way configurations and available in various sizes ranging from 0.5 to 4 inches. The new line of valves conforms to the FDA, USDA, and 3-A standards.

- Stainless steel is increasingly recognized as a crucial material due to its extensive resistance to corrosion, a significant concern in the food processing sector. These valves have also demonstrated exceptional durability when exposed to more aggressive water compositions, offering notable advantages to food processing plants. Moreover, stainless steel valves possess a higher pressure rating compared to alternative materials like brass. For instance, a typical 1-inch brass ball valve may have a pressure rating of 600 PSI, whereas a standard stainless steel ball valve of the same size would likely have a pressure rating of 1000 PSI. This characteristic renders them particularly suitable for high-pressure applications within the food processing industry.

- The growing urbanization rate across various parts of the world significantly enhances the demand for packaged food. Changing lifestyles, especially in urban areas, also contribute to the ever-increasing demand for packaged and processed foods. To ensure food security and achieve self-sufficiency goals, various countries are making efforts such as making regulatory changes and developing special economic zones to develop food processing industries.

- According to Population Reference Bureau, as of 2023, global urbanization stood at 57 percent. North America, Latin America, and the Caribbean led the pack, boasting urban populations exceeding 80 percent.

- A favorable scenario for the growth of the studied market has also been observed in other countries. The Department for Promotion of Industry and Internal Trade reported that the proposed investment in the food processing sector in India was valued at INR 120.37 billion (USD 1.47 billion) in 2022. Efforts are being taken to encourage investments across the entire value chain by the Indian Ministry of Food Processing Industries, including the implementation of the PLI scheme, which is expected to expand food processing capacity by nearly INR 30,000 crore (USD 3.6 billion) and create additional direct and indirect employment by the year 2026-27. Such initiatives are expected to offer significant opportunities for the ball valves.

North America is Expected to hold a Significant Market Share

- North America stands as a prominent market for ball valves, boasting substantial demand across diverse industries such as oil and gas, electricity, food and packaging, and chemicals. Both the United States and Canada exhibit immense demand, further fueled by the swift integration of industrial automation. The projected trend is expected to stimulate the market demand for ball valves in the region.

- North American area is witnessing a growing requirement for intelligent ball valves. Prominent regional industries are transitioning towards ball valves that incorporate processors and networking capabilities to complement advanced monitoring technology, which is coordinated through a central control station. The increased adoption of automation in process industries further reinforces this demand trend.

- The United States assumes a pivotal role in augmenting regional demand in contrast to Canada. The nation experiences a growing demand across nearly all end-user sectors, particularly in oil and gas, refining, and power generation. Higher energy consumption is the primary factor behind the higher demand across these sectors. For instance, according to EIA, total immediate energy consumption in the United States in 2022 was about 102.92 quadrillions Btu, of which petroleum consumption was about 31 percent.

- Furthermore, higher demand for oil & gas and other petroleum products also drives oil producers to increase their production and explore new oil extraction sites, which are expected to help the studied market grow further. For instance, in November 2022, the Canadian Association of Energy Contractors (CAOEC) announced that in 2023, it expects about 6,409 wells to be drilled in Canada, an approximately 15 percent increase from 2022.

- It is expected that new water treatment facilities will likely be set up in the region to feed the demand for ball valves as a result of an anticipated increase in regional population and increased water consumption across different sectors. A notable example is the recent announcement by New York State officials in September 2022, wherein they allocated over USD 232 million for water and sewer infrastructure projects in seven municipalities. The New York State Environmental Facilities Corporation granted funds and offered low-cost financing packages to facilitate water infrastructure initiatives with a cumulative expenditure exceeding USD 763 million. These investments in establishing treatment plants will inevitably augment the need for ball valves.

- Ball valves are utilized to regulate pressure and flow. Their leak-proof nature is a notable attribute that renders them highly advantageous, particularly in the chemical industry involving liquids. In July of 2022, BASF declared its final investment decision on a project worth USD 780 million, aimed at doubling the production capacity of its chemical manufacturing complex in Ascension Parish, Louisiana. The expansion project, which spans over seven years and represents a combined capital investment of over USD 1 billion, will enable the company In order to meet the growing demand for its products in a variety of sectors, such as construction, appliances, road haulage, and automobiles throughout North America.

Ball Valve Industry Overview

The ball valve market is fragmented and consists of several players, with no group currently holding a major share in the market. The companies are engaging in mergers and acquisitions to increase their expertise in the product. The market is viewed as a lucrative investment opportunity due to its wide consumer base. Some key market players include Flowserve Corporation, Alfa Laval, Crane Co., Honeywell International Inc., etc.

- November 2023 - Alfa Laval expands its valve portfolio with two new additions. The new valves, Unique Mixproof Process, and Unique Mixproof CIP enhance product safety by ensuring media is always separated. Their fully balanced design also enables risk-free handling at high pressures.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Growing Industrialization in Various Countries

- 5.1.2 Growing Demand for ProcessSafety

- 5.2 Market Challenges

- 5.2.1 Downtime Due to Repairing of Valves

6 MARKET SEGMENTATION

- 6.1 By Material (Qualitative Analysis)

- 6.1.1 Cast Iron

- 6.1.2 Steel

- 6.1.3 Alloy Based

- 6.1.4 Other Materials

- 6.2 By End-User Industry

- 6.2.1 Oil and Gas

- 6.2.2 Chemicals

- 6.2.3 Water and Waste Water

- 6.2.4 Power

- 6.2.5 Food and Beverage

- 6.2.6 Pharmaceutical

- 6.2.7 Other End-User Industries

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 ALFA LAVAL

- 7.1.2 CIRCOR International Inc.

- 7.1.3 Crane Co.

- 7.1.4 Castel SRL

- 7.1.5 Sanhua USA

- 7.1.6 Curtiss-Wright Corporation

- 7.1.7 Danfoss A/S

- 7.1.8 Emerson Electric Co

- 7.1.9 Georg Fischer Ltd

- 7.1.10 Flowserve Corporation

- 7.1.11 Hitachi Ltd

- 7.1.12 Honeywell International Inc.

- 7.1.13 KITZ Corporation

- 7.1.14 Mueller Water Products Inc