|

市場調査レポート

商品コード

1910434

ガス検知器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Gas Detectors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ガス検知器:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年01月12日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

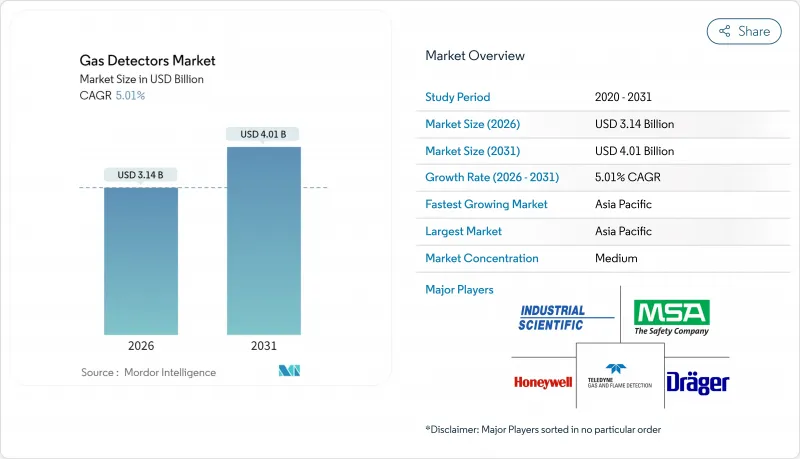

ガス検知器市場は2025年に29億9,000万米ドルと評価され、2026年の31億4,000万米ドルから2031年までに40億1,000万米ドルに達すると予測されています。

予測期間(2026-2031年)におけるCAGRは5.01%と見込まれます。

この成長軌跡は、リアルタイム労働者安全ソリューションへの資本投資増加、既存プラントにおける改修需要の拡大、予測分析エンジンに情報を提供する接続型検知プラットフォームの統合を反映しています。OSHA(米国労働安全衛生局)、NFPA 72(米国防火協会規格)、および地域鉱業規制の厳格な施行が設備更新サイクルを促進する一方、中流LNGハブ、水素生産資産、リチウムイオン電池ラインの持続的な拡張が、可燃性ガスおよび有毒ガス監視の基盤需要を高めています。安全システム向けのサイバーセキュリティ規制強化により、認証済みセンサーハードウェアとセキュアなIoTソフトウェアスタックを組み合わせられるベンダーへの調達が進んでいます。有線ネットワークが既存設備(ブラウンフィールド)設置では依然主流ですが、無線メッシュトポロジーと複数年対応バッテリーモジュールの進歩により、総設置コストが低下し、遠隔坑口や一時的なターンアラウンドゾーンなど未開拓のニッチ市場が開拓されつつあります。既存の世界のサプライヤーが、低ドリフト率、水素特異性、またはサブスクリプション型校正サービスを約束する専門分野の新規参入企業に対しシェア防衛を図る中、競合は激化しています。

世界のガス検知器市場の動向と洞察

危険産業における厳格な労働者安全規制

規制当局は定期的なスポットチェックではなく、リアルタイム環境テレメトリーを要求しており、鉱山、製油所、化学コンビナートに連続監視ネットワークの導入を促しています。OSHA(米国労働安全衛生局)の2025年データ駆動型検査プログラムは、オペレーターに従来の単一ガス検知器から、測定値を集中管理ダッシュボードへ送信するネットワーク化されたマルチガスアレイへの更新を促しています。オーストラリアの石炭関連法規では、坑内排水路(MDR)の認証が義務付けられており、防爆型固定ヘッドや地下メタンを3次元でマッピングするUAV搭載センサーの注文が急増しています。地方自治体の水道事業者は、硫化水素に関するNFPA 820の閾値に準拠する必要があり、湿式ポンプ室の換気設備に数千台規模の改修が行われています。主要ベンダーは、警報作動前に異常パターンを検知する予測分析ソフトウェアで対応し、インダストリアル・サイエンティフィック社の「2050年までに職場死亡事故を根絶する」といったゼロハーム指令に沿っています。単一製油所における年間コンプライアンス費用は10万米ドルを超えることもあり、これにより更新サイクルとサービス契約が固定化されます。

スマート接続型検知器の導入拡大

IoT接続により、ガス検知器市場は製品販売からデータサービスエコシステムへと転換しています。Blackline社のEXO 8は1回の充電で100日間クラウドへデータをストリーミングし、遠隔地の安全チームがリアルタイムで曝露動向を監視することを可能にします。Honeywell社のSensepoint XCLはBluetooth Low Energyでスマートフォンと連携し、技術者を段階的に導くとともに、校正期間を最大30%短縮します。予測ダッシュボードはセンサー交換を自動スケジュール化し、熟練労働者不足の緩和と予期せぬダウンタイムの削減を実現します。インダストリアル・サイエンティフィックのiNet Exchangeのようなサブスクリプション・バンドルは、ハードウェア、消耗品、分析機能を複数年契約にまとめ、調達を資本支出から運用支出へ移行させます。自動化されたコンプライアンス記録は監査準備を数週間から数時間に短縮し、異なる地域規制を扱う多国籍企業にとって魅力的な利点となります。

初期費用の高さと製品差別化の限界

産業用マルチガス携帯型検知器の単価は500~1,500米ドルですが、設置機器・試運転・ユーザートレーニングを含めると倍増します。AimSafety PM400は558.57米ドル、Gas Clipのメンテナンスフリー型MGC Simpleは697.07米ドルと、校正不要を謳う製品ほど価格プレミアムが顕著です。低コストのアジア製クローン製品は、確立されたブランドを最大50%も下回る価格で販売されており、予算制約のあるプラントでは利益率を圧迫し、更新計画を遅延させています。固定システムの設置費用は、認定配管、制御盤、機能試験を含めると、中規模製油所セクションで100万米ドルを超えることがよくあります。規制の執行が依然として一貫していない地域では価格感応度が高まり、一部の事業者がアップグレードを先送りできる状況が生じています。

セグメント分析

有線セグメントは2025年の収益の50.35%を占めました。既存の製油所、LNGプラント、化学工業団地では、危険区域基準を満たす実績ある有線ループが採用されているためです。こうしたレガシー環境では、防爆型接続ボックスや電磁干渉に耐える装甲ケーブル配線が、ガス検知器市場において引き続き好まれています。しかしながら、無線ソリューションは2031年までCAGR7.05%で拡大が見込まれております。これは、掘削コストや一時的な操業停止スケジュールが迅速な導入を必要とするプロジェクトに支えられております。初期世代の無線システムはバッテリー寿命の制限に悩まされておりましたが、第二世代のメッシュ設計では単一充電で最大100日間の稼働を実現し、複数のゲートウェイを経由してデータを中継することでプラントの監視制御ネットワークに到達することが可能となっております。新規建設の水素ハブやバッテリープラントでは、無線ノードが有線接続の安全区域ゲートウェイにデータを供給するハイブリッドアーキテクチャの予算配分が増加しており、柔軟性と確定的な稼働時間を両立させています。規制当局は適切な冗長性を備えた無線生命安全ループの認可を開始しており、この政策の進化により、欧州連合や米国の一部地域などにおける従来の導入障壁が取り除かれつつあります。これを受け、機器メーカーは研究開発をファームウェアベースのサイバーセキュリティ、OTネットワークのセグメンテーション、米国国立標準技術研究所(NIST)ガイドラインに準拠した無線センサー校正ルーチンに注力しています。この移行によりソリューション全体の平均販売価格(ASP)が上昇し、ベンダーがネットワーク状態を遠隔監視するサブスクリプション収益が導入されます。これにより、今後5年間は有線ノードの絶対的なセンサー数が優勢であるにもかかわらず、ガス検知器市場の価値プールが拡大します。

無線技術の普及は、分散した現場機器を共通の資産パフォーマンスダッシュボードで統合しようとするデジタルトランスフォーメーション予算からも恩恵を受けています。調達チームが総所有コストを算定する際、導管・ケーブルトレイ・火気作業許可証の不要化が、無線分析装置のプレミアムな定価を相殺することが多いのです。可動性の向上は、ターンアラウンド作業中に安全カバー範囲を拡大します。この期間には仮設配管の変更により毎日新たな漏洩経路が生じるためです。2024年のターンアラウンドシーズンに無線パックを試験導入した下流石油化学企業からは、閉所作業違反が15%減少、メンテナンス期間が8%短縮されたとの報告が寄せられています。こうした運用上の成果は投資回収モデルを強化し、経営陣の支持を確固たるものとし、ガス検知器市場全体における無線技術のシェア拡大をさらに加速させています。

地域別分析

アジア太平洋地域は2025年に世界収益の48.60%を占め、中国の石炭化学複合施設急増、インドの新規製油所建設、東南アジアの電池サプライチェーン投資拡大を背景に、6.92%という最速のCAGRを維持すると予測されます。中国国家緊急管理部の頻繁な安全監査により、施設運営者は未認証の低コスト輸入品からATEXおよびIECEx準拠機器への切り替えを迫られています。韓国と日本は水素充填ネットワークを加速させており、消防法規で義務付けられた二重冗長水素センサーを各ポンプに組み込んでいます。インドの「Jal Jeevan Mission」は数千の水処理施設における塩素・オゾン監視システムの更新を促し、需要をさらに拡大させています。国内の電子機器メーカーは窒化ガリウムパワースイッチの製造を拡大しており、特殊なアンモニアおよび塩化水素検知装置に新たな機会が生まれています。

北米は収益シェアで第2位を占めており、OSHA(米国労働安全衛生局)の規制強化、シェールガス処理、メキシコ湾岸の液化天然ガス輸出ターミナルが牽引しています。ニューヨーク市の地方法157号により、2025年5月までに住宅用天然ガス検知器の設置が義務付けられ、ガス検知器市場の住宅・小規模商業分野に数百万台規模の需要が創出されます。米国ではインフラ投資雇用法に基づく水素ハブ事業において、暗号化無線バックボーンを備えたマルチガス固定ネットワークが規定され、水素専用センサーの受注を促進しています。カナダのオイルサンド事業では、-40℃でも精度を維持するヒーターや分析装置が指定され、極寒対応機器ラインを有するベンダーが優位です。メキシコのモンテレイ及びバヒオ周辺産業回廊では、自動車塗装工場にVOC検知器を統合し、OEMの持続可能性監査に対応しています。

欧州では、ATEX(防爆指令)の厳格な順守、EPBD(エネルギー性能指令)に基づく室内空気質規制、脱炭素化目標が相まって、継続的な機器更新が維持されています。ドイツのライン川沿いの大規模化学工業地帯では、ベンゼンやブタジエンのモニタリングに投資し、漏洩排出量の削減を図っています。一方、英国では商業オフィスにおけるCO2モニタリングを義務化し、利用者の健康増進を推進しています。北海沖合プラットフォームでは、100ppmを超える硫化水素濃度に対応する認証済み検知ヘッドが求められており、プラットフォーム上部構造を200メートルにわたってカバーする開放型赤外線ユニットも併せて導入されています。東欧加盟国ではEU結束基金を活用し、地域暖房プラントの近代化を進めており、熱電併給モジュールに一酸化炭素およびメタンセンサーを統合しています。地中海地域のLNG輸入ターミナルでは、運用を中断せずに既存桟橋を改修するため、無線式炎検知・ガス検知パッケージを採用しています。

中東・アフリカ地域は収益シェアこそ小さいもの、グリーン水素パイロットプラント、液化プラント、鉱業拡張回廊において堅調な導入が進んでいます。GCC地域の精製所はユーロVI硫黄規制に対応するため水素化分解装置を改修し、その過程で触媒ビーズ式LEL検知ヘッドをアップグレードしています。南アフリカの金鉱山では、鉱物資源省による監督強化により、深部坑道での連続固定監視が義務付けられています。ラテンアメリカでは、ブラジルのプレソルト沖合油田が高濃度の硫化水素に対応した高仕様検知器を必要とする一方、チリのリチウム塩水処理施設では環境法令順守のため塩化水素分析装置を導入しています。こうした地域的な動向が相まって、予測期間を通じてガス検知器市場は多層的な均衡成長を維持する見込みです。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3か月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 危険産業における厳格な労働者安全規制

- スマートで接続された検知器の設置増加

- リアルタイム多ガス監視に対する需要の増加

- 中流LNGおよび水素インフラの拡張

- スマートビルにおける室内空気質規制への対応

- リチウムイオン電池工場におけるガス漏洩監視

- 市場抑制要因

- 初期費用の高さと製品差別化の限界

- 保守・校正の負担

- IIoT対応検知器におけるサイバーセキュリティ上の懸念

- 半導体センサーの供給不足が定期的に発生すること

- サプライチェーン分析

- 規制情勢

- テクノロジーの展望

- マクロ経済的要因が市場に与える影響

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測

- 通信タイプ別

- 有線

- ワイヤレス

- エンドユーザー業界別

- 石油・ガス

- 化学品および石油化学製品

- 上水道および下水道

- 金属・鉱業

- ユーティリティ

- その他のエンドユーザー産業

- 検出器タイプ別

- 固定

- 電気化学

- 半導体

- 光イオン化

- 触媒

- 赤外線

- MEMS

- ポータブルおよび可搬型

- マルチガス

- 単一ガス

- 固定

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- ロシア

- その他欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- 東南アジア

- その他アジア太平洋地域

- 中東・アフリカ

- 中東

- サウジアラビア

- アラブ首長国連邦

- その他中東

- アフリカ

- 南アフリカ

- エジプト

- その他アフリカ

- 中東

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場シェア分析

- 企業プロファイル

- Honeywell International Inc.

- Dragerwerk AG & Co. KGaA

- MSA Safety Incorporated

- Emerson Electric Co.

- Industrial Scientific Corporation

- Teledyne Gas & Flame Detection(Teledyne Technologies Inc.)

- Riken Keiki Co., Ltd.

- Crowcon Detection Instruments Ltd.

- Hanwei Electronics Group Corp.

- Trolex Ltd.

- Sensidyne LP

- New Cosmos Electric Co., Ltd.

- SENSIT Technologies LLC

- International Gas Detectors Ltd.

- GfG Gesellschaft fur Geratebau mbH

- GASTEC Corporation

- Yokogawa Electric Corp.

- Siemens AG-Process Safety Division

- Pem-Tech Inc.

- RKI Instruments Inc.

- WatchGas B.V.

- Ion Science Ltd.

- Ametek-Sensor Electronics