|

市場調査レポート

商品コード

1637860

クラウド侵入防止ソフトウェア:市場シェア分析、産業動向と統計、成長予測(2025年~2030年)Cloud Intrusion Protection Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| クラウド侵入防止ソフトウェア:市場シェア分析、産業動向と統計、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

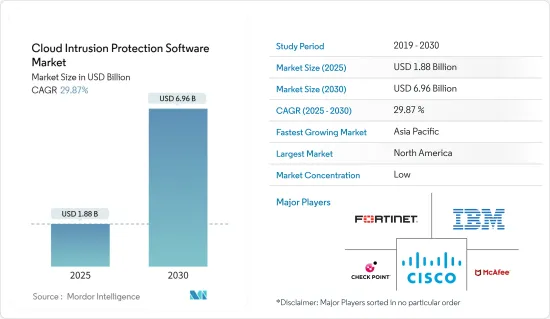

クラウド侵入防止ソフトウェア市場規模は2025年に18億8,000万米ドルと推定され、予測期間(2025-2030年)のCAGRは29.87%で、2030年には69億6,000万米ドルに達すると予測されます。

主なハイライト

- 多くの企業がクラウドサービスを導入し始めており、クラウドサービスの利用は幅広い分野で急速に拡大しています。ソフトウェアの脆弱性は深刻な問題になっており、新たな脅威をブロックするために新しいソフトウェア・アップデートがリリースされたときに、その環境にパッチを当てるのに苦労している組織もあります。

- クラウドIPSソリューションは、CVEデータベースに含まれる脆弱性を含む既知の脆弱性を悪用しようとするトラフィックをブロックすることで、クラウドベースおよびオンプレミスのアプリケーションを保護します。クラウドIPSは、セキュリティチームやITチームが手動で介入することなく新しい脆弱性から保護するため、企業のサーバー、ユーザーシステム、クラウドアプリケーションに手動でパッチを適用する負担が軽減されます。

- IC3によると、フィッシング攻撃は近年大幅に増加しています。2022年には、30万人以上がこのような攻撃の被害に遭っています。フィッシング攻撃には様々な形態があります。最も一般的なタイプは、バルクフィッシング、スミッシング、ビジネスメール詐欺(BEC)です。2022年には、調査対象となった世界企業の85%が大規模なフィッシング攻撃を経験したと回答し、ほぼ4社に3社がスミッシング詐欺の被害を受けたと回答しています。

- 増加するサイバー脅威とハッキングの試みが、企業や個人ユーザーをクラウド侵入防止ソフトウェアの利用に駆り立てています。また、ビジネス・ネットワークへの侵入インシデントの増加を考慮し、ネットワーク・セキュリティに対するIT支出も増加しています。侵入検知と侵入防止は、IT企業が標的型攻撃から身を守るために最も重要なハッキングとなっています。

- ハッカーから企業を守ることは、最近のIT企業にとって主要な取り組みとなっています。しかし、このソフトウェアによる複数のチェックや誤検知、誤検知によるネットワークパフォーマンスの低下は、市場の需要を失うことにつながります。

クラウド侵入防止ソフトウェア市場動向

電気通信と情報技術が飛躍的に成長する見込み

- クラウド侵入防止システムは、市場の他のあらゆる産業にサービスを提供する電気通信業界でますます採用されるようになっています。技術の進歩や最新の接続システムの採用が進むにつれて、自動車、小売、エネルギー・電力、政府サービス、ITセクター、その他技術を使用する産業などにおける通信サービスの需要は、過去10年間で漸増的な成長を遂げています。

- 通信産業は、あらゆる産業が支障なく操業するための重要なリンクです。クラウド・サービスの出現により、通信への依存度は高まっています。通信業界とIT業界は、より良いオペレーションを提供するために融合しました。現在、IT業界は大きな役割を果たしています。産業がクラウドと自動化に向かう中、業務をサポートするITシステムの導入が進み、通信業界はシステム全体の働きを円滑にするための接続と通信サービスを提供するようになっています。

- さらに、5G、AI、IoTなどの技術の急速な成長に伴い、データ漏洩を防止し、ネットワーク全体のデータを保護する必要があります。さらに、パートナーシップや製品イノベーションといった市場プレイヤーの戦略や開拓が、予測期間中のセグメント成長を促進すると予想されます。

- 例えば、2022年9月、VMwareはMWC Las Vegasで、RAN、5Gコア、エッジの展開、ライフサイクル管理を早めることを目的とした様々な斬新な製品とパートナーシップを発表しました。これには、VMwareのTelco Cloud Platform Ecosystemの拡張形態が含まれ、レギュレータプレーンとワーカーノードプールを個別にアップグレードし、東西ネットワークトラフィックのIDPSで5Gネットワークを保護することができます。VMwareはまた、MavenirのJoined Packet Coreを含む275以上のクラウドおよび仮想ネットワーク機能からなるパートナーエコシステムが拡大しているため、ネットワークサービスの利用を高速化できると述べています。

- サイバー攻撃の増加により、企業はデータ漏洩やデータ盗難を防ぐためにITインフラへの支出を増やしています。ITと電気通信はサイバーコネクティビティに重要な役割を担っているため、ITと電気通信業界のサイバーセキュリティ支出は他の業界よりも高くなると予想されています。Hiscox Cyber Readiness Report 2022によると、ドイツにおける企業のサイバーセキュリティに対するIT支出の割合は、2021年の21%から2022年には24%に増加しました。サイバー攻撃による企業のリスクは大幅に拡大しており、そのため予防への投資が拡大しています。

北米が市場成長に大きく貢献

- 北米市場は、クラウドIPSソフトウェア企業が注力している市場です。北米市場はクラウドIPSソフトウェアへの貢献度が最も高いです。大企業の存在、サイバー攻撃の頻度の増加、ホスティングサーバーの増加といった要因がこの地域の市場を牽引しています。

- さらに、米国では近年、組織や個人が直面するサイバー脅威や攻撃の総数が急増しているため、サイバーセキュリティはますます重要な分野となっています。Identity Theft Resource Centerによると、2022年に米国で発生したデータ漏洩の総数は約1802件に上った。一方、2022年には4億2,200万人以上の個人が、漏洩、データ侵害、暴露を含むデータ侵害によって大きな影響を受けました。

- また、同国では2021年までに、手作業が少なく自動化が進んでいる組織を標的にしたフィッシングやランサムウェア攻撃が増加します。2023年1月に発表されたEmsisoftの年末レポートによると、米国政府が脅威を封じ込めようと努力しているにもかかわらず、2022年の学校へのサイバー攻撃の件数は2021年とほぼ同じです。サイバー脅威とハッキングの取り組みは、北米のクラウド侵入者保護ソフトウェア市場を牽引すると予想されます。

- 2023年2月、ウインドストリーム・エンタープライズは、北米初の完全管理型セキュリティ・サービス・エッジ(SSE)ソリューションを発表しました。Cato Networksが提供するWindstream Enterprise SSEは、ネットワーク・トラフィックを監視し、悪意のあるコンテンツをブロックする侵入防止システム(IPS)を含む、内蔵セキュリティ機能の完全なコレクションを提供し、エクスプロイト、マイグレーション、ランサムウェア、その他のネットワークベースの攻撃など、さまざまなサイバー脅威から保護します。

- 2023年6月、AT&T CybersecurityとVertek Corporationは、中規模および大規模企業向けに統合セキュリティ管理(USM)を提供するために提携しました。Vertekの最先端のセキュリティ・オペレーション・センター(SOC)は、脅威からビジネスを保護しようとする企業顧客に、予測的かつプロアクティブな緩和と脅威検出のサービスを提供します。Vertekは、包括的な多層サイバーセキュリティ・プラットフォームであるVertekの24/7/365 SOCの一部として、AT&T CybersecurityのUSM Anywhereソリューションを使用しています。これは、リアルタイムの侵入検知と応答監視、行動監視、詳細な脆弱性スキャン、SIEM、ログ管理から構成され、刻々と変化し進化する環境である脅威に対して、顧客に比類のない保護を提供します。

クラウド侵入防止ソフトウェア業界概要

クラウド侵入防止ソフトウェアの市場は、サイバー攻撃の増加により非常に細分化されています。市場シェアを維持するため、多くの企業が既存の製品ポートフォリオをアップグレードする一方、新規参入企業も市場を開拓し、ニーズに合わせた製品を発売し続けています。このダイナミックな市場の主要企業には、Cisco Systems Inc.、IBM Corporation、Fortinet Inc.、Check Point Software Technologies Ltd.、Symantec Corporationなどがあります。

2023年6月、3D LiDARソリューションの主要企業であるQuanergy Solutions, Inc.は、著名なサービスベースのシステムインテグレーション企業であるConvergintと戦略的パートナーシップを結びました。この提携は、ユーティリティ分野に高度な境界侵入検知機能を提供することを目的としています。

2022年10月、Moxaは、MXsecurityが開発したセキュリティ管理ソフトウェアとともに、EDR-G9010シリーズ保護ルータにIDS/IPS機能を導入しました。この製品ポートフォリオへの追加は、NAT、ファイアウォール、スイッチ、およびVPN機能を備えたセキュアルータを提供し、目的に応じた管理およびサイバーセキュリティソリューションを強化します。IDS/IPSの搭載により、EDR-G9010シリーズは次世代産業用ファイアウォールに変身し、脅威の防止と検出機能が強化され、サイバーセキュリティの脅威から重要なインフラをさらに保護します。

2022年12月、コアライトは、強化された侵入検知ソフトウェア(IDS)サブスクリプションのソフトウェアの大幅な機能強化を発表しました。これらの機能強化により、セキュリティチームはセキュリティツールをシームレスに統合し、その効果を高めることができます。これは、トリアージ、検証、修復作業を促進するために必要な証拠と組み合わせたアラートを生成することによって達成されます。さらに、これらの改善により、顧客は従来のIDSソリューションをCorelightのより高度な製品に置き換えることができます。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の成果

- 調査の前提

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

- 技術スナップショット

第5章 市場力学

- 市場促進要因

- サイバー脅威とハッキングの試み

- ネットワークセキュリティに対するIT支出の増加

- 市場抑制要因

- 偽陽性と偽陰性の検出

- 多重チェックによるネットワークパフォーマンスの低下

第6章 市場セグメンテーション

- サービス別

- コンサルティング

- マネージドサービス

- 設計と統合

- トレーニングと教育

- 業界別

- 通信・情報技術

- 銀行・金融サービス

- 石油・ガス

- 製造業

- ヘルスケア

- 政府機関

- 旅行・運輸

- 小売業

- エンターテイメントとメディア

- その他業界別

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- Cisco Systems Inc.

- IBM Corporation

- Fortinet Inc.

- Check Point Software Technologies Ltd

- HP Inc.

- McAfee Inc.(Intel Corporation)

- Dell Inc.

- Trustwave Corporation

- AlienVault Inc.(AT&T Cybersecurity)

- Broadcom Inc.(Symantec Corporation)

第8章 投資分析

第9章 市場機会と今後の動向

The Cloud Intrusion Protection Software Market size is estimated at USD 1.88 billion in 2025, and is expected to reach USD 6.96 billion by 2030, at a CAGR of 29.87% during the forecast period (2025-2030).

Key Highlights

- The use of cloud services is growing rapidly in a broad range of areas as more companies are beginning to implement cloud services. Software vulnerabilities have become a serious problem, and several organizations struggle to patch their environments when new software updates are released to block emerging threats.

- Cloud IPS solutions protect cloud-based and on-premises applications by blocking traffic that attempts to exploit known vulnerabilities, including those contained in the CVE database. This reduces the burden of manually patching enterprise servers, user systems, or cloud applications, as Cloud IPS protects against new vulnerabilities without requiring manual intervention by security or IT teams.

- According to IC3, Phishing attacks have significantly increased in recent years. In 2022, more than 300,000 people fell victim to such attacks. Phishing attacks come in many forms. The most common types are bulk phishing, smishing, and business email compromise (BEC). In 2022, 85% of global organizations surveyed stated that they had experienced a major phishing attack, and almost three in four said they were affected by a smishing scam.

- The increasing number of cyber threats and hacking attempts drive companies and individual users to use cloud intrusion protection software. In addition, considering the increasing number of intrusion incidents in business networks, there has been increased IT spending on network security. Intrusion detection and prevention have been the most important hacks for IT companies to protect themselves from targeted attacks.

- Saving a company from hackers has become a major effort by IT companies these days. However, network performance loss owing to several checks and false positives and false negative detections by this software can lead to a loss of market demand.

Cloud Intrusion Protection Software Market Trends

Telecom and Information Technology Expected to Grow Exponentially

- Cloud intrusion protection systems are being increasingly adopted in the telecom industry, which serves every other industry in the market. With technological advancements and the increasing adoption of modern connectivity systems, the demand for communication services in industries such as automotive, retail, energy and power, government services, the IT sector, and other industries employing technology has seen incremental growth over the past decade.

- The telecom industry is a critical link for every industry to operate without interruptions. With the advent of cloud services, the dependence on communication is growing. The telecom and IT industries have merged to provide better operations. The IT industry nowadays plays a major role. With industries moving toward cloud and automation, they are increasingly deploying IT systems to support operations and telecom industries to provide connectivity and communication services to facilitate the working of the whole system.

- Moreover, with the prompt growth in technology such as 5G, AI, and IoT, it is necessary to prevent data breaches and protect the data across the network. Moreover, strategies and development by market players, such as partnerships and product innovations, are expected to drive segment growth during the forecast period.

- For instance, in September 2022, VMware launched various novel products and partnerships at MWC Las Vegas, intended to hasten RAN, 5G core, edge deployments, and lifecycle managing. This includes VMware, an extended form of its Telco Cloud Platform Ecosystem so workers can upgrade the regulator plane and worker node pools distinctly and protect their 5G networks with IDPS for east-west network traffic. VMware also stated that it can speed up the utilization of network services owing to the growing partner ecosystem of over 275 cloud- and virtual-network functions, including Mavenir's Joined Packet Core.

- The increasing number of cyberattacks has boosted businesses to increase their IT infrastructure spending to prevent data breaches and data theft. As IT and telecom hold a significant stake in cyber connectivity, the IT and telecom industry's cybersecurity spending is expected to be higher than the other industries. As per Hiscox Cyber Readiness Report 2022, the share of companies' IT spending on cyber security in Germany increased from 21% in 2021 to 24% in 2022. The risk to companies of cyber-attacks is expanding significantly, hence the expanded investment in prevention.

North America is the Major Contributor to the Market Growth

- The North American market has been the focus of cloud IPS software companies. The North American market is the highest contributor to cloud IPS software. Factors such as the presence of large enterprises, the growing frequency of cyber-attacks, and the increasing number of hosted servers are driving the market in the region.

- Moreover, cybersecurity has become an increasingly important area of focus in the United States in recent years due to the surge in the total count of cyber threats and attacks that organizations and individuals face. As per the Identity Theft Resource Center, in 2022, the total number of data compromises in the United States stood at around 1802 cases. Meanwhile, over 422 million individuals were greatly affected in 2022 by data compromises, including leakage, data breaches, and exposure.

- The country also marks an increase in phishing and ransomware attacks targeting organizations with less manual effort and high automation by 2021. According to Emsisoft's year-end report published in January 2023, the number of cyberattacks on schools in 2022 is almost the same as in 2021, despite the US government's efforts to contain the threat. Cyber threats and hacking efforts are expected to drive North America's cloud intruder protection software market.

- In February 2023, Windstream Enterprise announced the first fully managed Security Service Edge (SSE) solution in North America, powered by Cato Networks. Windstream Enterprise SSE, powered by Cato Networks, offers a complete collection of built-in security features, including an Intrusion Prevention System (IPS) to monitor network traffic and block malicious content, protect against a variety of cyber threats such as exploits, migrations, ransomware, and other network-based attacks.

- In June 2023, AT&T Cybersecurity and Vertek Corporation partnered to deliver Unified Security Management (USM) to mid-sized and large businesses. Vertek's cutting-edge Security Operations Center (SOC) provides predictive and proactive mitigation and threat detection services to enterprise customers looking to protect their businesses against threats. Vertek uses AT&T Cybersecurity's USM Anywhere solution as part of Vertek's 24/7/365 SOC, a comprehensive multi-layered cybersecurity platform. It comprises real-time intrusion detection and response monitoring, behavioral monitoring, in-depth vulnerability scanning, SIEM, and log management to offer customers unparalleled protection against the threat, which is an ever-changing and evolving environment.

Cloud Intrusion Protection Software Industry Overview

The market for cloud intrusion protection software has become highly fragmented due to the increasing number of cyber attacks. To retain their market share, many companies are upgrading their existing product portfolios while new players continue to explore the market and launch products tailored to their needs. Some of the key players in this dynamic market include Cisco Systems Inc., IBM Corporation, Fortinet Inc., Check Point Software Technologies Ltd, and Symantec Corporation.

In June 2023, Quanergy Solutions, Inc., a leading provider of 3D LiDAR solutions, formed a strategic partnership with Convergint, a prominent service-based systems integration company. This collaboration aims to deliver advanced perimeter intrusion detection capabilities for the utility sector.

In October 2022, Moxa introduced IDS/IPS functionality to its EDR-G9010 Series protected routers, along with the MXsecurity-developed security management software. This addition to their product portfolio enhances the purpose-built management and cybersecurity solutions, offering a secure router equipped with NAT, firewall, switch, and VPN functionality. The inclusion of IDS/IPS transforms the EDR-G9010 Series into a next-generation industrial firewall, bolstered with threat prevention and detection capabilities, providing added protection to critical infrastructure against cybersecurity threats.

In December 2022, Corelight unveiled significant software enhancements for its enhanced intrusion detection software (IDS) subscription. These enhancements allow security teams to seamlessly integrate security tools and increase their effectiveness. This is achieved by generating alerts combined with the necessary evidence to facilitate triage, validation, and remediation efforts. Furthermore, these improvements empower customers to replace legacy IDS solutions with Corelight's more advanced offerings.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

- 4.4 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Cyber Threats and Hacking Attempts

- 5.1.2 Increased IT Spending on Network Security

- 5.2 Market Restraints

- 5.2.1 Detection of False Positives and False Negatives

- 5.2.2 Loss of Network Performance Due to Multiple Checks

6 MARKET SEGMENTATION

- 6.1 By Service

- 6.1.1 Consulting

- 6.1.2 Managed Service

- 6.1.3 Design and Integration

- 6.1.4 Training and Education

- 6.2 By Industry Vertical

- 6.2.1 Telecom and Information Technology

- 6.2.2 Banking and Financial Service

- 6.2.3 Oil and Gas

- 6.2.4 Manufacturing

- 6.2.5 Healthcare

- 6.2.6 Government

- 6.2.7 Travel and Transport

- 6.2.8 Retail

- 6.2.9 Entertainment and Media

- 6.2.10 Other Industry Verticals

- 6.3 Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Latin America

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Cisco Systems Inc.

- 7.1.2 IBM Corporation

- 7.1.3 Fortinet Inc.

- 7.1.4 Check Point Software Technologies Ltd

- 7.1.5 HP Inc.

- 7.1.6 McAfee Inc. (Intel Corporation)

- 7.1.7 Dell Inc.

- 7.1.8 Trustwave Corporation

- 7.1.9 AlienVault Inc. (AT&T Cybersecurity)

- 7.1.10 Broadcom Inc. (Symantec Corporation)