|

市場調査レポート

商品コード

1637848

マネージドインフラストラクチャサービス:市場シェア分析、産業動向、成長予測(2025年~2030年)Managed Infrastructure Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| マネージドインフラストラクチャサービス:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

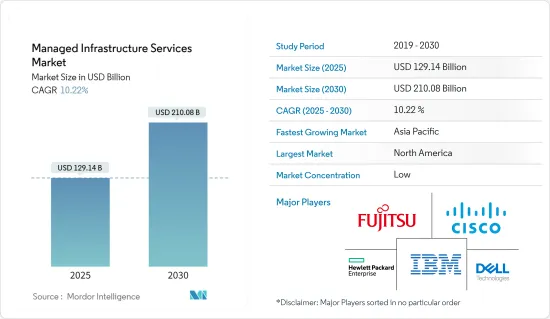

マネージドインフラストラクチャサービス市場規模は、2025年に1,291億4,000万米ドルと推定され、予測期間(2025~2030年)のCAGRは10.22%で、2030年には2,100億8,000万米ドルに達すると予測されます。

アナリティクス、クラウド、IoT、コグニティブ・コンピューティングなどの技術動向は、新たなビジネスの必要性を生み出しています。企業は、革新的なビジネスモデルの構築、ビジネスプロセスの最適化、従業員の能力向上、顧客体験のパーソナライズを目的として、これらのデジタル技術を採用しています。

主要ハイライト

- アプリケーションテスト、サービスカタログの作成、専門的なコンサルティングなど、専門的な付加価値サービスを提供するマネージドサービスにより、冗長なダウンタイムが削減されます。市場の開拓は、さまざまなモニタリングツールや、個によるチームが管理する多数のインフラ層によって支えられています。例えば、BMCの"BMC Helix ITSM "では、システムは集中化され、クラウドネイティブで、観測可能に接続され、AIOpsに最適化されています。このソリューションは、ITインフラ、アプリケーションパフォーマンス、ネットワークパフォーマンス、クラウドサービスのモニタリングツールからのデータを完全に公開します。さらに、チームと個人のダッシュボードは、各ユーザーのニーズに合わせてカスタマイズされます。

- クラウドベースの技術の普及と進歩が需要を押し上げ、市場を牽引しています。過去数年間、サーバーのブレークフィックスやトラブルシューティングなどの日常業務は、ITに対する注意を軽減するためにアウトソーシングされており、それによってITサービスベンダーの専門知識が活用されています。モビリティとクラウドによるデジタルトランスフォーメーションの導入が増加し、インフラの近代化が進んでいます。最新の技術強化に対応する必要性から、組織はインフラ管理サービスを選択するようになりました。

- コストと運用効率の改善、古くなったハードウェアの更新が市場を牽引しています。マネージドサービスにはいくつかの利点があり、中でも運用とビジネスプロセスの継続的改善への絶え間ない注力は最も重要なものです。Cisco Systems Inc.によると、マネージドサービスは社内の経常コストを30~40%削減し、効率を50~60%向上させています。さらに、インフラに新しく拡大された機器が導入されると、古いハードウェアが必ずしも互換性を持つとは限りません。データセンターの運用が増えるにつれ、ハードウェアは運用を強化する資産というよりも、むしろ運用を遅らせる負債になりかねないです。

- 利益率の低下、統合性や信頼性への懸念が、市場の成長を抑制しています。モビリティやクラウドコンピューティングといった新たな技術は、ビジネスの展望を急速に変えつつあります。企業は、顧客に望ましい利益を提供するために、これらの技術と同期する必要があります。また、重要なビジネスインフラのホスティングをによるパートナーに依頼する場合、信頼性に対する課題も市場の成長を妨げています。

- COVID-19の流行により、企業はリモートワークに大きな関心を寄せています。コロナウィルスの蔓延を食い止めるために各国政府が施した閉鎖措置の間、企業は業務の維持に気を配るようになり、クラウドサービスの利用は大きく伸びた。企業の間でクラウド移行がより広まり、場合によっては牽引役となることを見越して、ほとんどの企業はすでにマネージドクラウドサービスプロバイダーとの契約を更新しています。さらに、企業や組織は、デジタルトランスフォーメーションを推進するために、拡張現実や機械学習などの最先端技術を現在のITインフラに統合することを優先しました。

マネージドインフラストラクチャサービス市場の動向

クラウドセグメントが最も高い成長を示す見込み

- クラウド導入の登場は、マネージドインフラストラクチャサービスプロバイダー(MISP)の領域に変化をもたらし、パブリッククラウドまたはプライベートクラウド上で技術サービスを提供するデリバリーモデルを採用させました。クラウドが提供する利点を考慮し、企業は適切なクラウドプロバイダーの選択、クラウドへの移行、移行後のクラウドサービスの管理を行うため、クラウドプロバイダー(Google、AWS、Microsoftなど)と提携しているMISPを求めています。

- 企業の需要が高まる中、様々な企業が既存のマネージドクラウドインフラストラクチャサービスを進化させています。例えば、2022年12月、スイスの金融会社Klarpay AGは、クラウドベースのインフラを構築するためにAmazon Web Servicesの利用を決定しました。同社は、データセンターの運用にリソースを費やす代わりに、スケーラブルでAPI対応のトランザクション機能などの新機能を開発することでバンキング商品を強化するなど、価値の高い業務に集中しました。

- デジタルプラットフォームを利用する消費者はますます増えており、大容量のデータを保存するために、広いネットワークをカバーする高速データ転送のための継続的なデジタル化の進歩に対する需要が高まっています。ITビジネスにおける消費者ベースの成長を加速させた技術の例としては、遠隔学習、マルチ参入企業ゲーム、ビデオ会議、ライブストリーミングなどがあります。IT組織が大量のデータを保存し、より良いサービスを提供するためには、巨大なサーバーとデータストレージ・ユニットが必要です。

- 強化されたクラウドインフラ、IoT対応エコシステムなどの最近の技術動向は、米国のIT部門全体に新たなビジネスの必要性を生み出す機会を提供しており、米国におけるパブリッククラウドの普及率は、パンデミック時に高くなると予測されています。さらに、FujitsuはAmazon Web Services(AWS)からAWSの公式マネージドインフラプロバイダー・パートナーに認定され、クラウドトランスフォーメーションを加速し、デジタルトランスフォーメーションの迅速な推進を支援し、企業や政府のイノベーションを加速する同社の能力が認められました。このような事例は、予測期間中、米国全体の市場の需要を促進すると予想されます。

アジア太平洋が大幅な市場成長を占める

- アジア太平洋は、中国やインドなど様々な国々におけるITとIT対応サービスの主要な供給源であるため、市場の大幅な成長を占めています。例えば、ITとBPM部門はインドで最も重要な経済生成源の1つとなっており、GDPと福祉に大きな影響を与えています。IT部門は、22年度にはインドのGDPの7.4%を生み出したが、2025年までにはGDPの10%を占めるようになると予想されています。全米ソフトウェアサービス企業協会(Nasscom)によると、インドのIT産業の収益は22年度に2,270億米ドルに達し、前年比15.5%増となりました。インドのIT投資額は、2021年の818億9,000万米ドルから、2023年には1,103億米ドルに増加すると予測されています。

- アジア太平洋におけるマネージドインフラストラクチャサービスの成長に寄与している主要要因の1つは、さまざまなセグメントにおける急速なデジタル化と技術の進歩です。企業は、業務効率、俊敏性、競合を強化するために、先進的ITインフラへの依存度を高めています。その結果、こうした複雑なIT環境の最適なパフォーマンスとセキュリティを確保できる専門的なマネージドサービスの必要性が極めて重要になっています。

- アジア太平洋におけるクラウド技術の採用も、アジア太平洋のマネージドインフラストラクチャサービス市場に影響を与えています。企業が柔軟性と拡大性を高めるためにクラウドに移行するのに伴い、マネージドインフラストラクチャサービスはクラウドベースのインフラ管理にまで拡大し、オンプレミス環境とクラウド環境のシームレスな統合を実現しています。このハイブリッド・マルチクラウドアプローチにより、企業は変化するワークロードや需要に適応しながら、ITリソースを最適化することができます。

- さらに、MIT技術が発表した「クラウドエコシステムインデックス2022」によると、シンガポールは8.48点を獲得し、世界のクラウドコンピューティングインフラの中で最高位となりました。韓国、日本、オーストラリア、ニュージーランドは、2022年にクラウドサービスにとって有利なエコシステムを持つアジア太平洋諸国のトップスコアでした。この評価は、アジア太平洋がデジタルインフラの推進に取り組んでいることを強調するものであり、クラウドサービス、ひいてはマネージドインフラストラクチャサービスにとって魅力的な拠点となっています。

マネージドインフラストラクチャサービス産業概要

マネージドインフラストラクチャサービス市場は、技術的に確立された多くの大手企業が参入しているため、非常に細分化されており、競争は激化することが予想されます。また、市場を維持し顧客を維持するために、各社は強力な競争戦略を採用しており、競争企業間の敵対関係が激化しています。主要参入企業は、Fujitsu、Cisco Systems Inc.、Dell Technologies Inc.などがあります。

2023年9月、世界的に著名なITインフラストラクチャサービスプロバイダーであるKyndrylとフルスタッククラウドサービスプロバイダーのExpedientが提携を発表しました。この提携により、キンドリルはエクスペディエントの信頼性の高いクラウドインフラとデータセンターのコロケーションを活用することで、産業をリードするサイバー耐障害能力を顧客に向上させています。エクスペディエントの高度に相互接続されたデータセンターの全国ネットワークは、クラウドディファレンスのマルチクラウドサービスの主要コンポーネントである受賞歴のあるインフラに特化しています。インフラは、VMwareベースのExpedient Enterprise Cloud、プライベートクラウド、さまざまな地域やセグメントの顧客や見込み客の需要に合わせたカスタマイズ構成で提供されます。

2023年8月、世界のB2Bサブスクリプション・コマースプラットフォームのAppDirectは、ADCom Solutionsのネットワーク・オペレーションセンター(NOC)とVEEUEプラットフォームを買収したと発表しました。ADCom Solutionsは、複雑なITインフラの設計、導入、包括的な管理を専門とするマネージドサービスの世界のプロバイダーです。AppDirectは、今回の買収により、技術アドバイザーの広範なネットワークへのアクセスをVEEUEに提供できるようになり、AppDirectは1万人のアドバイザーチャネルを通じて、マネージドネットワークとインフラストラクチャサービス一式を導入できるようになります。

2022年11月、デジタルトランスフォーメーション、ハイパフォーマンス・コンピューティング、情報技術インフラの世界リーダーであるアトスと、Amazon.com, Inc.の子会社であるAmazon Web Services(AWS)は、本日、世界戦略的トランスフォーメーション契約を発表しました。この契約により、大規模なインフラアウトソーシング契約を締結しているアトスの顧客は、クラウドへのワークロード移行を加速し、デジタルトランスフォーメーションを完了することができます。複数年にわたる産業初の契約により、AtosとAWSは戦略的パートナーシップをさらに強化することができます。AtosはAWSを優先的なエンタープライズクラウドプロバイダーとして選択し、AWSはアトスをITアウトソーシングとデータセンター変革の戦略的パートナーとして認定しました。この提携により、Atosの顧客は、Atosからビジネスと技術アドバイザリー、デジタルエンジニアリング、マネージドサービスを受けることで、クラウドへの移行を早めることができます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 市場の定義と範囲

- 調査の前提

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 産業の利害関係者分析

- 産業の魅力-ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場力学

- 市場促進要因

- クラウドマネージドインフラストラクチャサービスの利用の増加

- クラウドベースの技術の普及と進歩が需要を押し上げる

- コストと運用効率の改善、老朽化したハードウェアの更新

- 市場抑制要因

- 利益率の低下、統合と信頼性への懸念

- COVID-19がマネージドインフラストラクチャサービス市場に与える影響

第6章 市場セグメンテーション

- 導入タイプ別

- オンプレミス

- クラウド

- サービスタイプ別

- デスクトッププリントサービス

- サーバー

- インベントリー

- その他

- エンドユーザー別

- BFSI

- ITとテレコム

- 医療

- 製造業

- 小売

- その他

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- その他のラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他の中東・アフリカ

- 北米

第7章 競合情勢

- 企業プロファイル

- Fujitsu Ltd

- Cisco Systems Inc.

- Dell Technologies Inc.

- IBM Corporation

- Hewlett Packard Enterprise

- Microsoft Corporation

- TCS Limited

- Canon Inc.

- Alcatel-Lucent SA(Nokia Corporation)

- Toshiba Corporation

- Verizon Communications Inc.

- Citrix Systems Inc.

- Deutsche Telekom AG

- Xerox Corporation

- Ricoh Company Ltd

- Lexmark International Inc.

- Konica Minolta Inc.

第8章 投資分析

第9章 市場機会と今後の動向

The Managed Infrastructure Services Market size is estimated at USD 129.14 billion in 2025, and is expected to reach USD 210.08 billion by 2030, at a CAGR of 10.22% during the forecast period (2025-2030).

Technology trends such as analytics, Cloud, IoT, and Cognitive Computing are creating new business imperatives. Companies are adopting these digital technologies to build innovative business models, optimize business processes, empower their workforce, and personalize the customer experience.

Key Highlights

- Redundant downtime is reduced through managed services, which offer specialized value-added services like application testing, service catalog creation, and professional consulting. The market's development is aided by various monitoring tools and numerous layers of infrastructure controlled by separate teams. For instance, in BMC's "BMC Helix ITSM" the system is centralized, cloud-native, connected with observability, and optimized for AIOps. This solution fully exposes data from monitoring tools for IT infrastructure, application performance, network performance, and cloud services. Additionally, team and individual dashboards are customized to each user's needs.

- Technological proliferation and advancement of cloud-based technology boosting the demand is driving the market. Over the past few years, daily operations of break-fix and troubleshooting of servers have been outsourced to reduce their attention over IT, thereby allowing the expertise of IT service vendors. An increase in the adoption of digital transformation with mobility and cloud has led to infrastructure modernization. The need to keep up with the latest technological enhancements has led organizations to opt for infrastructure-managed services.

- Improved cost and operational efficiency and updates of outdated hardware are driving the market. Managed services offer several benefits, relentless focus on continuous improvement of operational and business processes being the most significant one. According to Cisco Systems, managed services reduce recurring in-house costs by 30-40% and increase efficiency by 50-60%. Moreover, as new and enhanced equipment is introduced to the infrastructure, the old hardware might not always be compatible. As data center operations increase, the hardware could become more of a liability which slows down operations, than an asset that enhances them.

- Declining profit margins and integration and reliability concerns are restraining the market to grow. Emerging technologies, such as mobility and cloud computing, are rapidly changing the business landscape. Companies have to be in sync with these technologies to deliver desired benefits to the customers. Reliability concerns are also challenging the market to grow when hiring another partner to host critical business infrastructure.

- Businesses are putting a lot of attention on remote working due to the COVID-19 pandemic. The use of cloud services grew significantly as companies became more concerned with maintaining operations during lockdowns imposed by various governments to stop the spread of the coronavirus. In anticipation of cloud migration becoming more widespread among corporations and, in some cases, even gaining traction, most businesses have already renewed their contracts with managed cloud service providers. Additionally, businesses and organizations prioritized integrating cutting-edge technologies like augmented reality and machine learning into their current IT infrastructure to promote digital transformation.

Managed Infrastructure Services Market Trends

The Cloud Segment is Expected to Exhibit the Highest Growth

- The advent of cloud deployment has brought changes in the managed infrastructure services providers (MISP) space and made them embrace a delivery model for delivering technology services over a public or private cloud. Considering the advantages the cloud offers, businesses are seeking MISPs that have partnerships with cloud providers (such as Google, AWS, Microsoft, etc.) to choose the right cloud providers, migrate to the cloud, and manage cloud services after the transition.

- With the increasing demand from enterprises, various companies have made advancements in their existing managed cloud infrastructure service. For instance, in December 2022, the Swiss finance company Klarpay AG decided to use Amazon Web Services to create its cloud-based infrastructure. Instead of spending its resources to operate a data center, the company concentrated on high-value tasks, such as enhancing its banking product by creating new features like scalable and API-enabled transactional capabilities.

- Increasingly more consumers are using digital platforms, which has increased the demand for ongoing digitalization advancements for high-speed data transport with wide network coverage for large amounts of data storage. Examples of technologies that have accelerated the growth of the consumer base in the IT business include distance learning, multiplayer gaming, videoconferencing, and live streaming. Enormous servers and data storage units are necessary for IT organizations to store large amounts of data and offer improved services.

- Recent technology trends, such as enhanced cloud infrastructure, IoT enabled ecosystems, have provided opportunities in creating new business imperatives across the US IT sector, and the penetration of public cloud in the United States is predicted to be higher during a pandemic. Additionally, Fujitsu has been recognized by Amazon Web Services (AWS) as an official AWS-managed infrastructure provider partner, thereby validating the company's capabilities in accelerating cloud transformation and helping fast-track digital transformation, and accelerating innovation for enterprises and government. Such instances are expected to fuel the demand of the market across the United States during the forecast period.

Asia-Pacific Account for a Significant Market Growth

- Asia-Pacific region accounts for the significant market growth due to dominating sources of IT and IT-enabled services in various countries such as China and India. For instance, the IT & BPM sector has become one of India's most significant economic generators, substantially impacting its GDP and welfare. The IT sector generated 7.4% of India's GDP in FY22; by 2025, it is expected to account for 10% of its GDP. The Indian IT industry's revenue reached USD 227 billion in FY22, a 15.5% YoY growth, according to the National Association of Software and Service Companies (Nasscom). India was predicted to spend USD 110.3 billion on IT in 2023, up from an estimated USD 81.89 billion in 2021.

- One of the key factors contributing to the growth of managed infrastructure services in the Asia-Pacific region is the rapid digitization and technological advancements across various sectors. Enterprises are increasingly relying on advanced IT infrastructure to enhance operational efficiency, agility, and competitiveness. As a result, the need for specialized managed services that can ensure the optimal performance and security of these complex IT environments has become crucial.

- The region's adoption of cloud technologies also influences the Asia-Pacific managed infrastructure services market. As organizations migrate to the cloud for enhanced flexibility and scalability, managed infrastructure services extend to cloud-based infrastructure management, ensuring seamless integration between on-premises and cloud environments. This hybrid and multi-cloud approach allows businesses to optimize their IT resources while adapting to changing workloads and demands.

- Further, according to an MIT Technology publication, Singapore ranked highest on the Cloud Ecosystem Index 2022, with a score of 8.48, for cloud computing infrastructure worldwide. South Korea, Japan, Australia, and New Zealand were top-scoring Asia-Pacific nations with favorable ecosystems for cloud services in 2022. This recognition emphasizes the region's commitment to advancing its digital infrastructure, making it an attractive hub for cloud services and, by extension, managed infrastructure services.

Managed Infrastructure Services Industry Overview

The managed infrastructure services market is highly fragmented as many large, technologically established players are present in the industry, and the rivalry is expected to be on the higher side. Additionally, in order to sustain in the market and retain their clients, companies are employing powerful competitive strategies, thereby intensifying competitive rivalry in the market. Key players are Fujitsu Ltd, Cisco Systems Inc., Dell Technologies Inc., etc.

In September 2023, Kyndryl, a prominent provider of IT infrastructure services globally, and Expedient, a Full-Stack Cloud service provider, announced a partnership. This partnership will improve Kyndryl's industry-leading cyber resilience capabilities to customers by utilizing Expedient's reliable cloud infrastructure and data center colocation. Expedient's highly interconnected nationwide network of data centers is dedicated to its award-winning infrastructure, a key component of its Cloud Different multi-cloud services. Infrastructure is offered in VMware-based Expedient Enterprise Cloud, private cloud, and customized configurations to suit the demands of clients and prospects in various geographies and sectors.

In August 2023, AppDirect, a global B2B subscription commerce platform, announced that it had acquired the Network Operations Center (NOC) and VEEUE platform of ADCom Solutions. ADCom Solutions has been a global provider of managed services, specializing in designing, implementing, and comprehensively administrating complex IT infrastructures. AppDirect will be able to offer VEEUE access to the extensive network of technology advisers through this acquisition, allowing AppDirect to introduce a suite of managed network and infrastructure services through its channel of 10,000 advisors.

In November 2022, Atos, a global leader in digital transformation, high-performance computing, and information technology infrastructure, and Amazon Web Services, Inc. (AWS), a subsidiary of Amazon.com, Inc., today announced a global Strategic Transformation Agreement. This agreement enables Atos customers with large-scale infrastructure outsourcing contracts to accelerate workload migrations to the cloud and complete digital transformation. With the multiyear, first-in-the-industry deal, Atos and AWS can further their strategic partnership. Atos has chosen AWS as its preferred enterprise cloud provider, and AWS has identified Atos as a strategic partner for IT outsourcing and data center transformation. With the help of this arrangement, Atos' clients may hasten their transitions to the cloud by receiving business and technology advisory, digital engineering, and managed services from Atos.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Market Definition and Scope

- 1.2 Study Assumptions

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Stakeholder Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Consumers

- 4.3.3 Threat of New Entrants

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing use of Cloud Managed Infrastructure Services

- 5.1.2 Technological Proliferation and Advancement of Cloud Based Technology Boosting the Demand

- 5.1.3 Improved cost and Operational Efficiency and Update of Outdated Hardware

- 5.2 Market Restraints

- 5.2.1 Declining Profit Margins and Integration and Reliability Concerns

- 5.3 Impact of COVID-19 on Managed Infrastructure Services Market

6 MARKET SEGMENTATION

- 6.1 By Deployment Type

- 6.1.1 On-premise

- 6.1.2 Cloud

- 6.2 By Services Type

- 6.2.1 Desktop and Print Services

- 6.2.2 Servers

- 6.2.3 Inventory

- 6.2.4 Other Types

- 6.3 By End User

- 6.3.1 BFSI

- 6.3.2 IT and Telecom

- 6.3.3 Healthcare

- 6.3.4 Manufacturing

- 6.3.5 Retail

- 6.3.6 Other End Users

- 6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 Germany

- 6.4.2.2 UK

- 6.4.2.3 France

- 6.4.2.4 Spain

- 6.4.2.5 Rest of Europe

- 6.4.3 Asia-Pacific

- 6.4.3.1 China

- 6.4.3.2 Japan

- 6.4.3.3 India

- 6.4.3.4 Australia

- 6.4.3.5 Rest of Asia-Pacific

- 6.4.4 Latin America

- 6.4.4.1 Brazil

- 6.4.4.2 Mexico

- 6.4.4.3 Argentina

- 6.4.4.4 Rest of Latin America

- 6.4.5 Middle East and Africa

- 6.4.5.1 UAE

- 6.4.5.2 Saudi Arabia

- 6.4.5.3 South Africa

- 6.4.5.4 Rest of Middle East and Africa

- 6.4.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 Fujitsu Ltd

- 7.1.2 Cisco Systems Inc.

- 7.1.3 Dell Technologies Inc.

- 7.1.4 IBM Corporation

- 7.1.5 Hewlett Packard Enterprise

- 7.1.6 Microsoft Corporation

- 7.1.7 TCS Limited

- 7.1.8 Canon Inc.

- 7.1.9 Alcatel-Lucent SA (Nokia Corporation)

- 7.1.10 Toshiba Corporation

- 7.1.11 Verizon Communications Inc.

- 7.1.12 Citrix Systems Inc.

- 7.1.13 Deutsche Telekom AG

- 7.1.14 Xerox Corporation

- 7.1.15 Ricoh Company Ltd

- 7.1.16 Lexmark International Inc.

- 7.1.17 Konica Minolta Inc.