|

市場調査レポート

商品コード

1939088

キサンタンガム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年)Xanthan Gum - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| キサンタンガム:市場シェア分析、業界動向と統計、成長予測(2026年~2031年) |

|

出版日: 2026年02月09日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

概要

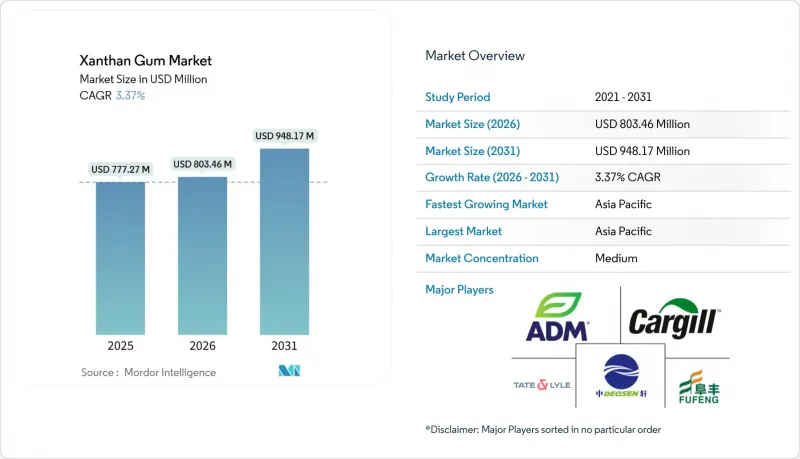

キサンタンガム市場は、2025年の7億7,727万米ドルから2026年には8億346万米ドルへ成長し、2026年から2031年にかけてCAGR3.37%で推移し、2031年までに9億4,817万米ドルに達すると予測されております。

この成長は、様々な産業分野において費用対効果の高い粘度調整剤としてキサンタンガムが広く使用されていることに起因しております。食品産業では配合に広く活用される一方、特殊掘削流体メーカーはその性能特性を活用しております。さらに、パーソナルケアおよび製薬産業では製品開発にその特性を活用しております。キサンタンガムの擬塑性挙動と幅広いpHレベルでの安定性は、温度変化、機械的ストレス、イオン相互作用といった厳しい条件下でも一貫した性能を保証します。さらに、グルテンフリーのベーカリー製品、植物由来の乳製品代替品、クリーンラベルの調味料に対する消費者需要の高まりが市場を支えています。石油・ガス産業では、キサンタンガムの耐塩性が高塩分掘削環境における貯留層の完全性を向上させます。業界関係者は戦略的投資を通じて市場ニーズに対応しており、北米企業は生産能力の拡大を進め、アジア太平洋地域のメーカーは地域的な供給安定性と製造効率の向上に向け、操業の最適化に注力しています。

世界のキサンタンガム市場の動向と洞察

飲食品業界における増粘剤・安定剤としての利用拡大

食品メーカーは、キサンタンガムの擬塑性特性が製品配合にもたらす大きな利点を認識しています。この汎用性の高い原料を配合することで、メーカーは製品の均一性を効果的に維持しつつ、原材料数を抑えたクリーンラベル製品に対する消費者の高まる需要に対応しています。このバイオポリマーは、わずか0.05%という低濃度で安定した乳化液を形成する優れた効率性を示し、乳製品、焼き菓子、飲料など幅広い分野における食感改良のコスト効率に優れた解決策となっています。急成長中の植物性ミルク代替品市場では、メーカーがキサンタンガムを活用し、従来の乳製品に匹敵する滑らかでクリーミーな口当たりを再現。消費者の期待に応える粘度特性を実現しています。FDAによる数量制限のない継続的な承認は業界の信頼を強化し、メーカーによる新たな用途の開拓を促進しています。この市場促進要因は特に乾燥キサンタンガム分野の成長を後押ししており、製品の優れた保存安定性と精密な投与を可能にする特性が、大規模食品加工工程の要件に完全に合致しています。

乳化特性によるパーソナルケア・化粧品分野での採用拡大

キサンタンガムの皮膜形成特性により、化粧品開発者は製品のテクスチャーを向上させると同時に、パーソナルケア製品における天然成分への消費者需要の高まりに対応できます。調査によれば、キサンタンガムの濃度変化が化粧品皮膜表面の特性に影響を与え、メーカーは製品のテクスチャーや塗布特性を精密に制御することが可能です。本原料は他の天然ガムとの優れた相溶性を示し、界面活性剤を含まない処方で合成乳化剤への依存度を低減するのに役立ちます。この移行は、規制枠組みが合成代替品よりも天然由来成分をますます優先する欧州および北米市場で特に顕著です。液体キサンタンガム処方を好むパーソナルケア業界の傾向は、天然ソリューションへの広範な市場動向を反映し、この製品カテゴリーの大幅な成長を継続的に牽引しています。

敏感な方における潜在的なアレルギー反応

キサンタンガムは広範な臨床研究を通じて一貫して高い安全性を示していますが、孤立したアレルギー反応事例の出現により、特に敏感な用途において規制当局の監視強化と消費者意識の高まりが生じています。欧州食品安全機関(EFSA)による包括的な再評価では、生後12週以上の乳児を含む一般人口に対するキサンタンガムの安全性が再確認されました。しかしながら、同機関は市販製品中の有害元素に対する監視プロトコルの強化を推奨するなど、追加的な安全対策を講じています。こうした動向を受け、製造業者は特に医薬品や乳幼児食品用途において、製品の包括的な純度を証明し明確なトレーサビリティ経路を確立するため、より厳格な文書化要件に直面しています。欧州連合が中国からの非適合キサンタンガム輸入品を対象とした通報制度を導入したことは、市場アクセスを維持するために厳格な品質管理基準を維持することの根本的な重要性を強調しています。こうした進化する規制上の考慮事項は、市場での成功のために厳格な安全基準の遵守が依然として最優先事項であるプレミアム用途に主に影響を及ぼしています。

セグメント分析

乾燥キサンタンガムは2025年においても85.76%という大きな市場シェアを維持しており、食品製造業界における確固たる地位を示しています。食品メーカーは、保存安定性と既存の粉末処理システムとのシームレスな統合性を理由に、一貫して乾燥キサンタンガムを選択しています。このセグメントの市場リーダーシップは、信頼性の高い貯蔵特性と精密な投与能力の提供能力に基づいて構築されています。これらは、製品の均一性と運用コスト管理が主要な関心事である大規模な操業を管理する食品生産者にとって、基本的な要件です。

一方、液体キサンタンガムは市場シェアは小さいもの、2031年までCAGR5.30%とより堅調な成長可能性を示しています。この成長軌道は主に、即時溶解性と混合効率の向上が重要な運用要件となる特定の産業用途によって牽引されています。液体形態の性能特性は、原料の迅速な混入と均一な分散が求められる製造工程において特に価値を発揮します。

地域別分析

アジア太平洋地域は、コスト効率の高い製造と堅牢な発酵インフラを背景に、2025年には35.22%のシェアでキサンタンガム市場を牽引する見込みです。中国は生産能力を活かし、国内需要と世界の輸出の両方に応える中心的な役割を担っています。代替基質やプロセス最適化による製造コスト削減を目指すイノベーションに支えられ、同地域は2031年までCAGR4.58%で成長すると予測されています。さらに、進化する規制枠組みにより品質管理基準が強化され、国際的な輸出要件を満たし、これまで市場アクセスに影響を与えてきたコンプライアンス上の課題に対処しています。

北米では、クリーンラベルの動向と産業用途の拡大を背景に、安定した需要成長が見込まれます。同地域は強力な規制枠組みの恩恵を受け、高品質製品に対するプレミアム価格設定が可能となっています。重要な進展として、カナダにおけるJungbunzlauer社の2億米ドル規模の施設が挙げられ、地域の生産能力を拡大し輸入依存度を低減します。さらに、特に非在来型掘削における石油・ガス用途が、キサンタンガムの熱安定性と環境面での利点から需要を牽引しています。成熟した食品加工産業と医薬品用途における確立された規制経路が、同地域の成長可能性をさらに強化しています。欧州は厳格な品質要件と持続可能性への注力に支えられ、プレミアム用途において強い存在感を維持しています。欧州食品安全機関(EFSA)の安全性評価は規制面での確実性を提供しますが、有害元素に対する監視強化がコンプライアンスコストを増加させています。一方、南米、中東・アフリカでは、食品加工産業の成長とキサンタンガムの利点に対する認識の高まりに伴い、新たな機会が生まれています。ただし、技術的専門知識の不足や従来品と比較したコストの高さが、これらの地域での普及における課題となっています。

その他の特典:

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

よくあるご質問

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場情勢

- 市場概要

- 市場促進要因

- 飲食品業界における増粘剤・安定剤としての利用拡大

- 乳化特性によるパーソナルケア・化粧品分野での採用拡大

- クリーンラベル・天然原料への需要増加

- グルテンフリーおよびビーガン製品への需要増加

- 低脂肪・低カロリー食品製品の人気が高まっています

- 石油・ガス産業における掘削流体および増進採油技術への応用拡大

- 市場抑制要因

- 敏感な方におけるアレルギー反応の可能性

- 厳格な食品安全・品質基準

- 代替製品の入手可能性

- 途上地域における認知度の低さ

- サプライチェーン分析

- 規制の見通し

- ポーターのファイブフォース

- 新規参入業者の脅威

- 買い手・消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場規模と成長予測(金額および数量)

- 形態別

- 液体

- ドライ

- 用途別

- 飲食品

- ベーカリー製品

- 菓子類

- 食肉製品

- 冷凍食品

- 乳製品

- 飲料

- その他

- 医薬品

- パーソナルケアおよび化粧品

- 石油精製所

- その他の用途

- 飲食品

- 地域別

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- スペイン

- オランダ

- ポーランド

- その他欧州地域

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- その他アジア太平洋地域

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- その他中東・アフリカ地域

- 北米

第6章 競合情勢

- 市場集中度

- 戦略的動向

- 市場ランキング分析

- 企業プロファイル

- Tate & Lyle PLC

- Fufeng Group

- Deosen Biochemical Ltd.

- Cargill, Incorporated

- Archer Daniels Midland

- Ingredion Incorporated

- Solvay S.A.

- Jungbunzlauer Suisse AG

- Shandong Unionchem Co., Ltd.

- Hebei Xinhe Biochemical Co., Ltd.

- Foodchem International Corp.

- Meihua Holdings Group Co., Ltd.

- Qingdao BZ Oligo Biotech Co., Ltd.

- Ceamsa

- Seawin Biotech Group

- Mitsubishi Corporation

- International Flavors & Fragrances Inc.

- C.E. Roeper GmbH

- Kerry Group plc

- CP Kelco