|

市場調査レポート

商品コード

1687347

ウインドウフィルム:市場シェア分析、産業動向・統計、成長予測(2025~2030年)Window Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ウインドウフィルム:市場シェア分析、産業動向・統計、成長予測(2025~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

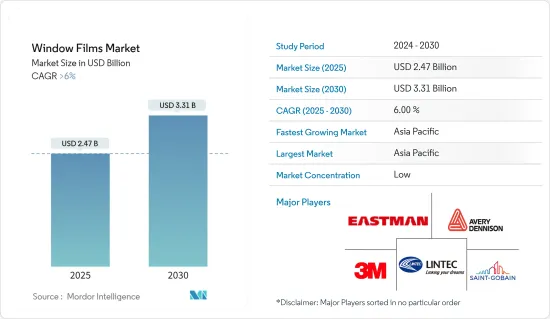

ウィンドウフィルムの市場規模は2025年に24億7,000万米ドルと予測され、予測期間中(2025~2030年)のCAGRは6%を超え、2030年には33億1,000万米ドルに達すると予測されています。

2020年のCOVID-19パンデミックは建設業界に悪影響を与えました。業界は物流や原材料の入手不能による課題に直面しました。これはウィンドウフィルム市場にも悪影響を与えました。しかし、パンデミック後の自動車産業の生産と販売の急増が市場の成長と回復を後押ししました。

主なハイライト

- 中期的には、カーボンフットプリントの削減が重視されるようになり、消費者の間で安全性とセキュリティに対する関心が高まっていることが、市場の成長を促す主な要因となっています。

- しかし、ウィンドウフィルムの施工にはある程度の技術的専門知識が必要であり、ウィンドウフィルム市場の成長を拡大するためには、技術的な問題や施工上の問題を改善する必要があります。また、スマートガラス市場の成長がウィンドウフィルム市場の妨げになる可能性もあります。

- また、紫外線(UV)保護に対する関心の高まりは、業界に新たな成長機会をもたらすと予測されています。

- アジア太平洋地域が市場を独占し、予測期間中に最も高い年間成長率を記録すると予想されます。

ウィンドウフィルム市場の動向

市場を独占する建築・建設セグメント

- ウィンドウフィルムは、日射調節のために建築業界で利用されています。日射熱を反射し、建物内の温度を快適に保つことができます。

- 建設分野では、装飾フィルム、紫外線(UV)カットフィルム、プライバシーフィルム、防眩フィルム、落書き防止フィルム、断熱フィルム、安全・防犯フィルムなどのウィンドウフィルムが使用されています。世界の建設産業は、主にインド、中国、米国などの国々によって牽引され、2030年までに8兆米ドルに達すると予想されています。

- 中国は建設ブームに沸いています。同国は世界最大の建設市場を持ち、世界の建設投資全体の20%を占めています。2030年までに13兆米ドル近くを建築に費やすと予想されています。

- 国家統計局(NBS)によると、中国では建設業界の事業活動指数(BASI)が2023年11月の55.9から12月時点で56.9に上昇しました。BASIスコアが50を上回ると業界の成長を示し、2023年10月のBASIスコアは53.5でした。

- インド産業・国内貿易振興省によると、2022年のインドの建設開発セクターへの外国直接投資(FDI)株式流入額は1億2,500万米ドル相当でした。米国の民間建設支出は2022年に増加し、公共部門の建設支出の約4倍となりました。米国は建設業界で大きなシェアを占めており、2022年には17億9,300万米ドルを超える年間支出を記録しました。

- 米国国勢調査局(USCB)によると、2023年12月の建設支出は季節調整済み年率で2兆960億米ドルと推計され、11月改定値の2兆783億米ドルを0.9%上回りました。また、2023年の建設額は1兆9,787億米ドルで、2022年の1兆8,487億米ドルを7.0%上回りました。

- したがって、前述の開発は、今後数年間、建設業界におけるウィンドウフィルムの需要を促進すると予想されます。

アジア太平洋地域が市場を独占

- アジア太平洋地域が市場を独占し、中国とインドが最大のシェアを占めると予想されます。中国は同地域で最大のGDPを誇ります。中国は最も急速に台頭している経済国のひとつであり、現在では世界最大の生産国のひとつとなっています。同国の製造業は、同国の経済に大きく貢献しています。中国はアジア太平洋の中でも建設業が盛んな国のひとつで、工業と建設業がGDPの約50%を占めています。

- 同国の人口動態は、今後も住宅建設の成長に拍車をかけると予想されます。世帯所得水準の上昇と農村部から都市部への人口移動が相まって、同国の住宅建設分野の需要を引き続き牽引すると予想されます。官民両部門による手ごろな価格の住宅への注目の高まりが、住宅建設分野の成長を促進すると予想されます。

- インドは建設業界にとって最大の市場であり、不動産と都市開発部門が増加しています。インドブランドエクイティ財団(IBEF)によると、インドの不動産産業は2030年までに1兆米ドルに達し、2025年までに国内総生産(GDP)に約13%寄与すると見られています。これにより、ウィンドウフィルム市場の需要が増加し、同地域の市場が活性化すると思われます。

- 建築需要は好調ですが、インドでは自動車産業も増加しています。例えば、インド自動車工業会(SIAM)によると、乗用車生産台数は2023年に458万台に達し、2022年の365万台から25.5%の伸びを記録しました。さらに、2023年には国内で1,586万台以上の二輪車が販売されました。

- また、OICAによると、中国の自動車生産台数は2023年に3,016万台に達し、年間10.6%の伸びを示しました。

- また、Oxford Economicsは、2037年までに中国、米国、インドが全世界の建設工事の51%を占めると予測しています。これは、アジア太平洋の2カ国で世界的に膨大な建設量が発生することを意味し、予測期間中にウィンドウフィルムの需要を大きく伸ばす可能性があります。

- このような要因から、同地域のウィンドウフィルム市場は予測期間中に安定した成長が見込まれます。

ウィンドウフィルム産業の概要

世界のウィンドウフィルム市場は断片化されており、上位2社が世界市場で大きなシェアを占めています。同市場の主要企業(順不同)には、Eastman Chemical Company、3M、Avery Dennison Corporation、Saint-Gobain、Lintec Corporationなどがあります。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 安全・防犯ウィンドウフィルムに対する需要の増加

- カーボンフットプリントの削減への関心の高まり

- 抑制要因

- 技術、保証、施工の問題

- スマートガラス市場の成長

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競合の程度

第5章 市場セグメンテーション

- タイプ別

- 日射調整・UVカットフィルム

- 装飾用フィルム

- 安全・セキュリティフィルム

- プライバシーフィルム

- 断熱フィルム

- その他

- エンドユーザー産業別

- 自動車

- 建築・建設

- 住宅用

- 商用

- インフラ・施設

- 海洋

- その他

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- ベトナム

- マレーシア

- インドネシア

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- ロシア

- トルコ

- ノルディック

- スペイン

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- コロンビア

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- カタール

- ナイジェリア

- アラブ首長国連邦

- エジプト

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場シェア(%)**/ランキング分析

- 主要企業の戦略

- 企業プロファイル

- 3M

- Armolan Greece

- Avery Dennison Corporation

- Eastman Chemical Company

- HYOSUNG CHEMICAL

- Johnson Window Films Inc.

- LINTEC Corporation

- NEXFIL

- Rayno Window Film

- Saint-Gobain

- TORAY INDUSTRIES INC.

第7章 市場機会と今後の動向

- 紫外線防止に対する関心の高まり

The Window Films Market size is estimated at USD 2.47 billion in 2025, and is expected to reach USD 3.31 billion by 2030, at a CAGR of greater than 6% during the forecast period (2025-2030).

The COVID-19 pandemic in 2020 adversely affected the construction industry. The industry faced challenges due to logistics and raw materials' unavailability. This also negatively impacted the window films market. However, the automotive industry's upsurge in production and sales post-pandemic propelled the market's growth and recovery.

Key Highlights

- Over the medium term, the major factors driving the market's growth are increasing emphasis on reducing carbon footprint and increasing safety and security concerns among consumers.

- However, some technical expertise is required to install window films, and the technicality and installation issues need to be improved to increase the growth of the window film market. Also, the growth in the smart glass market may cause hindrances to the window film market.

- Also, the growing concern for ultraviolet (UV) protection is projected to create new growth opportunities for the industry.

- Asia-Pacific is expected to dominate the market and will likely witness the highest annual growth rate during the forecast period.

Window Films Market Trends

The Building and Construction Segment to Dominate the Market

- Window films are utilized in the construction industry for solar control. They can reflect solar radiation heat and maintain a comfortable temperature inside buildings. Window films are used in the construction sector for solar control due to their ability to reflect the heat from solar radiation and maintain a comfortable ambiance in terms of the temperature inside the structure or building.

- In the construction segment, window films, such as decorative, ultraviolet (UV) block, privacy, anti-glare, anti-graffiti, insulating films, and safety and security films, are used. The global construction industry is expected to reach USD 8 trillion by 2030, primarily driven by countries like India, China, and the United States.

- China is amid a construction mega-boom. The country has the largest building construction market in the world, making up 20% of all construction investment globally. The country is expected to spend nearly USD 13 trillion on buildings by 2030.

- According to the National Bureau of Statistics (NBS), in China, the construction industry's business activity index (BASI) rose to 56.9 as of December 2023 from 55.9 in November 2023. The BASI score above 50 indicates growth in the industry, and the October 2023 BASI score was 53.5.

- According to the Department for Promotion of Industry and Internal Trade of India, the foreign direct investment (FDI) equity inflow for the construction development sector in India was worth USD 125 million in 2022. The United States' spending on private construction grew in 2022 and was nearly four times larger than construction spending in the public sector. The United States holds a significant share of the construction industry, which recorded an annual expenditure of over USD 1,793 million in 2022.

- According to the US Census Bureau (USCB), construction spending in December 2023 was estimated at a seasonally adjusted annual rate of USD 2,096.0 billion, 0.9% above the revised November estimate of USD 2,078.3 billion. Moreover, the construction value was USD 1,978.7 billion in 2023, 7.0%higher than the USD 1,848.7 billion spent in 2022.

- Therefore, the aforementioned developments are expected to drive the demand for window films in the construction industry through the years to come.

Asia-Pacific to Dominate the Market

- Asia-Pacific is expected to dominate the market, with China and India accounting for the largest share. China has the largest GDP in the region. China is one of the fastest emerging economies, and it has become one of the biggest production houses in the world today. The country's manufacturing sector is one of the major contributors to the country's economy. China is one of the major countries in Asia-Pacific with ample construction activities, with the industrial and construction industries accounting for approximately 50% of the GDP.

- Demographics in the country are expected to continue to spur growth in residential construction. Rising household income levels combined with the population migrating from rural to urban areas are expected to continue to drive demand for the residential construction segment in the country. Increased focus on affordable housing by both the public and private sectors will drive growth in the residential construction segment.

- India is the largest market for the construction industry, with an increase in the real estate and urban development segment. According to the Indian Brand Equity Foundation (IBEF), the Indian real estate industry will likely reach USD 1 trillion by 2030 and contribute approximately 13% to the country's GDP by 2025. This will increase the demand for the window film market and propel its market in the region.

- Although the demand for construction is good, the automotive industry in India is also increasing. For instance, according to the Society of Indian Automobile Manufacturers (SIAM) India, the passenger vehicle production volume reached 4.58 million in 2023, registering a 25.5% growth over 3.65 million in 2022. Moreover, in 2023, over 15.86 million units of two-wheelers were sold domestically across the country.

- Also, according to OICA, automotive production in China reached 30.16 million in 2023, an annual increase of 10.6%.

- Also, Oxford Economics estimates that China, the United States, and India will account for 51% of all construction work done worldwide by 2037. This means a huge global construction volume will occur in the two Asia-Pacific countries and can significantly grow the demand for window films during the forecast period.

- Due to all such factors, the market for window films in the region is expected to grow steadily during the forecast period.

Window Films Industry Overview

The global window films market is fragmented, with the top two companies holding significant shares in the global market. Some of the major players in the market (not in any particular order) include Eastman Chemical Company, 3M, Avery Dennison Corporation, Saint-Gobain, and Lintec Corporation.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Demand for Safety and Security Window Films

- 4.1.2 Increasing Emphasis on Reducing Carbon Footprint

- 4.2 Restraints

- 4.2.1 Technical, Warranty, and Installation Issues

- 4.2.2 Growing Smart Glass Market

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Type

- 5.1.1 Solar Control and UV Blocking Films

- 5.1.2 Decorative Films

- 5.1.3 Safety and Security Films

- 5.1.4 Privacy Films

- 5.1.5 Insulating Films

- 5.1.6 Other Types

- 5.2 End-user Industry

- 5.2.1 Automotive

- 5.2.2 Building and Construction

- 5.2.2.1 Residential

- 5.2.2.2 Commercial

- 5.2.2.3 Infrastructural and Institutional

- 5.2.3 Marine

- 5.2.4 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Vietnam

- 5.3.1.7 Malaysia

- 5.3.1.8 Indonesia

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Russia

- 5.3.3.6 Turkey

- 5.3.3.7 NORDIC

- 5.3.3.8 Spain

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Qatar

- 5.3.5.4 Nigeria

- 5.3.5.5 United Arab Emirates

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Armolan Greece

- 6.4.3 Avery Dennison Corporation

- 6.4.4 Eastman Chemical Company

- 6.4.5 HYOSUNG CHEMICAL

- 6.4.6 Johnson Window Films Inc.

- 6.4.7 LINTEC Corporation

- 6.4.8 NEXFIL

- 6.4.9 Rayno Window Film

- 6.4.10 Saint-Gobain

- 6.4.11 TORAY INDUSTRIES INC.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Concerns Regarding UV Protection