|

市場調査レポート

商品コード

1237860

下大静脈フィルター市場- 成長、動向、予測(2023年-2028年)Inferior Vena Cava Filter Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 下大静脈フィルター市場- 成長、動向、予測(2023年-2028年) |

|

出版日: 2023年03月03日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

下大静脈フィルター市場は、予測期間中、約9.1%のCAGRで成長すると予測されています。

COVID-19は、患者の肺塞栓症の発症率を著しく高めたため、調査対象市場に大きな影響を与えました。下大静脈(IVC)フィルターは肺塞栓症の治療によく使用されるため、初期の流行期にこの病気の発生率が上昇したこともIVCフィルターの使用率を増加させました。例えば、2021年11月にBMC Respiratory Researchが発表した論文によると、フランスで行われた調査で、パンデミック初期に肺塞栓症で入院した患者さんの数が全体で約16%増加したことが明らかになりました。これらの増加は、ほとんどがCOVID-19波に起因するもので、COVID-19患者の肺塞栓症入院と関連していました。したがって、パンデミックは当初、市場に大きな影響を与えました。しかし、現在パンデミックは沈静化しており、肺塞栓症にかかるリスクも減少しているため、本調査の予測期間中は安定した成長が期待されます。

心臓疾患の有病率の上昇や低侵襲技術への需要の高まりなどの要因が、市場の成長を促す主な要因となっています。肺塞栓症(PE)と静脈血栓塞栓症(VTE)は、IVCフィルターが治療に使用される2つの疾患です。これらの疾患の有病率が世界的に高まっていることが、市場の成長を促す大きな要因となっています。例えば、2022年10月にJAMA Networkが発表した論文によると、肺塞栓症(PE)は、肺動脈の血流が閉塞することが多く、下肢の静脈から移動する血栓が原因で典型的に起こります。PEは、下肢の静脈から移動した血栓が原因で起こることが多く、その発生率は、世界全体で年間10万人あたり約60~120人と推定されています。

さらに、2022年3月にFrontiersが発表した論文によると、静脈血栓塞栓症(VTE)は、肺塞栓症(PE)と深部静脈血栓症(DVT)を併発することが多いとされています。米国では、これらの疾患に罹患している新規診断患者が年間375,000~425,000人いると推定されています。したがって、これらの疾患の有病率の上昇は、IVCフィルターの使用量を増加させると予想されます。

さらに、IVCフィルターによるVTE治療の利点も、市場の成長を後押ししています。例えば、2022年8月にNCBIが更新した記事によると、米国心臓協会(AHA)や米国胸部医師会(ACCP)といった世界中の様々な組織が、静脈血栓塞栓症(VTE)を発症し抗凝固薬の禁忌がある患者に対して下大静脈(IVC)フィルターの使用を推奨しています。

このように、肺塞栓症(PE)や静脈血栓塞栓症(VTE)の有病率の増加やIVCフィルターの利点など、上記の要因が市場の成長を後押しすると予想されます。しかし、デバイスの誤作動に伴うリスクや新興国市場における認知度の低さが、市場の成長を阻害すると予想されます。

主な市場動向

予測期間中、肺塞栓症の予防が大きなシェアを占めると予想される

肺塞栓症(PE)は、血栓が肺の動脈に詰まり、肺の一部への血流が遮断されることでしばしば発症する病気です。血栓は脚から発生し、心臓の右側を通って肺に至ることがほとんどです。肺塞栓症の治療には、下大静脈フィルター(IVC)がよく使われます。肺塞栓症の有病率の上昇、老年人口の増加、低侵襲技術への需要の高まりなどの要因が、この分野の成長を後押しすると予想されています。

肺塞栓症の有病率の増加は、IVCフィルターの使用量増加につながるため、セグメントの成長を促進する主要な要因となっています。例えば、2021年11月にLung Indiaが発表した記事によると、インドと韓国で研究が行われ、肺塞栓症の有病率はそれぞれ2%と5%であることが示されました。PEになる可能性は、頻脈、頻呼吸、呼吸性アルカローシスに陥っている患者さんで有意に高くなりました。

さらに、2021年6月にThe Department of Health and Aged Care of Australiaが発表したデータによると、毎年17,000人以上のオーストラリア人が肺塞栓症を発症すると推定されており、高齢化に伴い発症率は増加傾向にあります。塞栓症のリスクが高いグループは、高齢者、がんを患っている人、不動状態(例えば、入院)の人です。したがって、肺塞栓症が多いことから、IVCフィルターの使用量が増加し、セグメントの成長につながると予想されます。

また、肺塞栓症は高齢になると発症することが多く、高齢者人口の増加が市場の成長を促進する大きな要因となっています。例えば、2022年8月にMDPIが発表した記事によると、肺塞栓症(PE)と深部静脈血栓症(DVT)は静脈血栓塞栓症(VTE)の2つの症状であり、これらの疾患は子供には珍しく、しばしば老齢疾患として考えられています。

したがって、肺塞栓症の有病率の上昇や老人人口の増加といった要因が、この分野の成長を後押しすると予想されます。

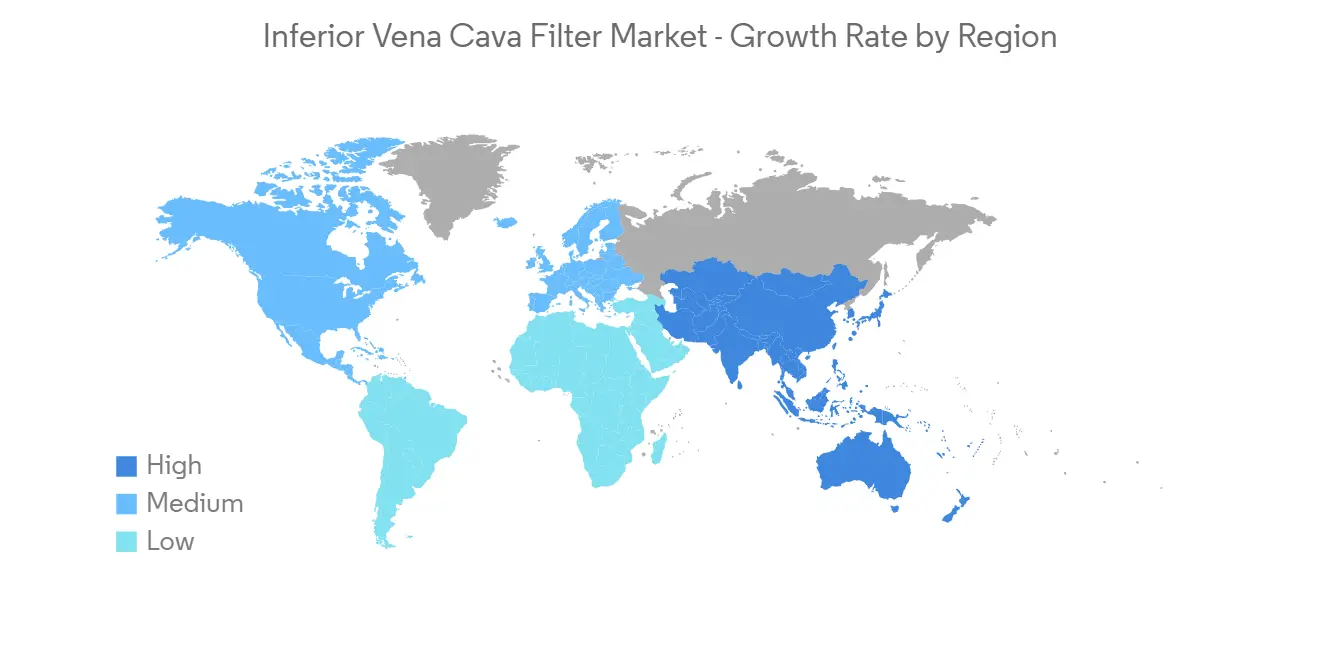

予測期間中、北米が市場において大きなシェアを占めると予想される

北米は、静脈血栓塞栓症(VTE)および肺塞栓症(PE)の治療におけるIVCフィルターの使用量の増加、VTEおよびPEの有病率の増加、高齢者人口の増加により、市場で大きなシェアを占めると予想されます。例えば、2022年6月にCDCが更新したデータによると、米国では毎年90万人もの人々が深部静脈血栓症(DVT)または肺塞栓症(PE)に罹患する可能性があると推定されています。したがって、この地域ではPEの有病率が高いことから、IVCフィルターの使用率が高まり、市場の成長につながると予想されます。

さらに、2022年8月にNCBIが更新した論文によると、米国では肺塞栓症(PE)の発生率は人口10万人あたり年間39~115人、DVTについては10万人あたり53~162人となっています。また、PEは女性よりも男性に多く発症することが指摘されています。このような疾病の発生率の増加は、同地域の市場成長を促進すると予想されます。

さらに、VTEやPEは老齢と関連するため、同地域の老人人口の増加も市場の成長を促進する主要な要因となっています。例えば、カナダ統計局が2022年7月に発表したデータによると、カナダでは約733万605人が65歳以上の高齢者であり、これは総人口の18.8%を占めると推定されています。

このように、VTEやPEの有病率の上昇、老年人口の増加など、上記のような要因から、同地域では市場の成長が期待されています。

その他の特典です。

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場の定義

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 心疾患の有病率の上昇

- 低侵襲技術の需要の高まり

- 市場抑制要因

- デバイスの誤動作に伴うリスク

- 新興国における認識の甘さ

- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション(金額別市場規模-USD million)

- アプリケーション別

- 静脈血栓塞栓症治療

- 肺塞栓症予防

- 製品タイプ別

- 回収可能

- 常設

- エンドユーザー別

- 病院

- 外来手術センター

- その他

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- アジア太平洋地域

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他アジア太平洋地域

- 中東・アフリカ地域

- GCC

- 南アフリカ

- その他中東・アフリカ地域

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 北米

第6章 競合情勢について

- 企業プロファイル

- Adient Medical Inc.

- ALN

- Argon Medical

- B. Braun Melsungen AG

- Becton, Dickinson and Company

- Boston Scientific Corporation

- Braile Biomedica

- Cardinal Health

- Cook Medical

- Cordis

- Volcano Corporation

第7章 市場機会と今後の動向

The inferior vena cava filter market is anticipated to grow with a CAGR of nearly 9.1%, during the forecast period.

COVID-19 had a significant impact on the studied market as it significantly increased the incidence of pulmonary embolism among patients. Inferior vena cava (IVC) filters are often used for treating pulmonary embolism, so the rising incidence of the disease during the early pandemic also increased the usage of IVC filters. For instance, according to an article published by BMC Respiratory Research in November 2021, a study was conducted in France which showed that the overall number of patients hospitalized with pulmonary embolism increased by approximately 16% during the early pandemic. These increases were mostly attributed to COVID-19 waves, which were associated with pulmonary embolism hospitalization in COVID-19 patients. Hence, the pandemic had a significant impact on the market initially. However, as the pandemic has currently subsided, the risk of getting a pulmonary embolism has also decreased, thus the studied market is expected to have stable growth during the forecast period of the study.

Factors such as the rising prevalence of cardiac ailments and the growing demand for minimally invasive techniques are the major factors driving the market growth. Pulmonary embolism (PE) and venous thromboembolism (VTE) are the two diseases where IVC filters are used for treatment. The rising prevalence of these diseases around the world is a major factor driving the growth of the market. For instance, according to an article published by the JAMA Network in October 2022, pulmonary embolism (PE) is often characterized by occlusion of blood flow in a pulmonary artery, which happens typically due to a thrombus that travels from a vein in a lower limb. The incidence of PE is estimated to be approximately 60 to 120 per 100,000 people per year globally.

Furthermore, according to an article published by Frontiers in March 2022, Venous thromboembolism (VTE) is often associated with pulmonary embolism (PE) and deep venous thrombosis (DVT). It is estimated that there are 375,000 - 425,000 newly diagnosed patients per year in the United States that are suffering from these diseases. Hence, the rising prevalence of such diseases is expected to increase the usage of IVC filters.

Additionally, the advantages of the treatment of VTE using IVC filters are also enhancing the market growth. For instance, according to an article updated by NCBI in August 2022, various organizations around the world such as the American Heart Association (AHA) and American College of Chest Physicians (ACCP) recommend the use of inferior vena cava (IVC) filters in patients that have the venous thromboembolic disease (VTE) and having a contraindication to anticoagulant medications.

Thus, the above-mentioned factors such as the increasing prevalence of pulmonary embolism (PE) and venous thromboembolism (VTE), and the advantages of IVC filters, are expected to boost the growth of the market. However, the risks associated with device malfunction and the lack of awareness in developing countries are expected to impede market growth.

Key Market Trends

Prevention of Pulmonary Embolism is Expected to Hold a Significant Share Over the Forecast Period

Pulmonary embolism (PE) is a disease that often occurs when a blood clot gets stuck in an artery in the lung, blocking blood flow to part of the lung. Blood clots most often start in the legs and travel up through the right side of the heart and into the lungs. Inferior vena cava (IVC) filters are often used for the treatment of pulmonary embolism. Factors such as the rising prevalence of pulmonary embolism, rising geriatric populations, and the increasing demand for minimally invasive techniques are expected to boost segment growth.

The increasing prevalence of pulmonary embolism is a major factor driving the segment growth, as it leads to more usage of IVC filters. For instance, according to an article published by Lung India in November 2021, a study was conducted in India and South Korea which showed the prevalence of pulmonary embolism to be 2% and 5%, respectively. The likelihood of getting PE was significantly higher in patients who were suffering from tachycardia, tachypnea, and respiratory alkalosis.

Furthermore, according to the data published by The Department of Health and Aged Care of Australia in June 2021, it is estimated that more than 17,000 Australians every year will have a pulmonary embolism, and the incidence is increasing as the population ages. Groups at higher risk of embolism are older people, people who have cancer, and people who are immobilized (for example, hospitalized). Hence, the high prevalence of pulmonary embolism is expected to increase the usage of IVC filters, thus leading to segment growth.

Moreover, old age is often associated with pulmonary embolism cases, and the rising geriatric population thus becomes a major factor driving the growth of the market. For instance, according to an article published by MDPI in August 2022, Pulmonary embolism (PE) and deep-vein thrombosis (DVT) are the two manifestations of Venous thromboembolism (VTE), and these diseases are uncommon in children and are often considered as an old age disease.

Hence, the factors such as the rising prevalence of pulmonary embolism and the rising geriatric population are expected to boost segment growth.

North America is Expected to Hold a Significant Share in the Market Over the Forecast Period

North America is expected to hold a significant share of the market due to the increasing usage of IVC filters for the treatment of venous thromboembolism (VTE) and pulmonary embolism (PE), the increasing prevalence of VTE and PE, and the rising geriatric population. For instance, according to the data updated by CDC in June 2022, it is estimated that as many as 900,000 people could be affected with deep vein thrombosis (DVT) or pulmonary embolism (PE) each year in the United States. Hence, the high prevalence of PE in the region is expected to boost the usage of IVC filters, leading to market growth.

Furthermore, according to an article updated by NCBI in August 2022, the incidence of pulmonary embolism (PE) ranges from 39 to 115 per 100,000 population annually, and for DVT, the incidence ranges from 53 to 162 per 100,000 people in the United States. The incidence of PE is noted to be more in males as compared to that females. Thus, the increasing incidence of such diseases is expected to boost market growth in the region.

Moreover, as VTE and PE are associated with old age, the rising geriatric population in the region is also a major factor driving the growth of the market. For instance, according to the data published by Statistics Canada in July 2022, it is estimated that around 7,330,605 people are aged 65 years or older in Canada, and this accounts for 18.8% of the total population.

Thus, due to the above mentioned factors such as the rising prevalence of VTE and PE, and the rising geriatric population, the market is expected to experience growth in the region.

Competitive Landscape

The inferior vena cava filter market is fragmented in nature and consists of a few major players. The companies have been following various strategies such as acquisitions, partnerships, investments in research activities, and new product launches to sustain themselves among the competitors in the global market. Companies like ALN, Argon Medical, B. Braun Melsungen AG, Becton, Dickinson and Company, Boston Scientific Corporation, Braile Biomedica, Cardinal Health, Cook Medical, and Volcano Corporation, among others, hold a substantial share in the market.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Cardiac Ailments

- 4.2.2 Growing Demand of Minimally Invasive Techniques

- 4.3 Market Restraints

- 4.3.1 Risks associated with the Device Malfunction

- 4.3.2 Lack of Awareness in Developing Countries

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 By Application

- 5.1.1 Treatment of Venous Thromboembolism

- 5.1.2 Prevention of Pulmonary Embolism

- 5.2 By Product Type

- 5.2.1 Retrievable

- 5.2.2 Permanent

- 5.3 By End-User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Others

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Adient Medical Inc.

- 6.1.2 ALN

- 6.1.3 Argon Medical

- 6.1.4 B. Braun Melsungen AG

- 6.1.5 Becton, Dickinson and Company

- 6.1.6 Boston Scientific Corporation

- 6.1.7 Braile Biomedica

- 6.1.8 Cardinal Health

- 6.1.9 Cook Medical

- 6.1.10 Cordis

- 6.1.11 Volcano Corporation