|

市場調査レポート

商品コード

1237849

表面処理化学品市場- 成長、動向、および予測(2023年-2028年)Surface Treatment Chemicals Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 表面処理化学品市場- 成長、動向、および予測(2023年-2028年) |

|

出版日: 2023年03月03日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

表面処理化学品市場は、予測期間中に5%以上のCAGRで推移すると予想されています。

COVID-19の発生は、表面処理化学品の市場成長にプラスの影響を与えています。COVID-19のパンデミックの間、ウイルスに対抗するために新しい表面処理化学物質が開発されました。例えば、ALANOD GmbHのMIRO UV-C製品は、COVID-19ウイルスを効果的に破壊し、除菌装置の反射板の材料として利用されています。また、COVID-19ウイルス対策として、フェイスシールドを製造するための高性能で医療用グレードの透明フィルムが利用できるようになったことも大きな進展です。

主なハイライト

- 短期的には、消費者の需要と感染症の影響を軽減するための表面処理化学物質の使用による自動車産業の成長が、予測期間中の市場成長を後押ししています。

- しかし、化学的な表面処理の影響に関する懸念の高まりにより、業界に持ち込まれた規制を遵守するために、化学物質からバイオベース(グリーン)製品への移行が進んでいます。環境の持続可能性、エネルギー効率、複数のアプリケーション機能は、ニッチな製品開発でメーカーを抑制し、市場の成長をさらに妨げると考えられます。

- しかし、商業施設や住宅のインフラ建設における表面処理化学品の使用、バイオベースやクロムフリーの表面処理化学品への関心の高まりは、将来的に十分な成長機会をもたらすでしょう。予測期間中、市場には有利な機会が生まれると思われます。

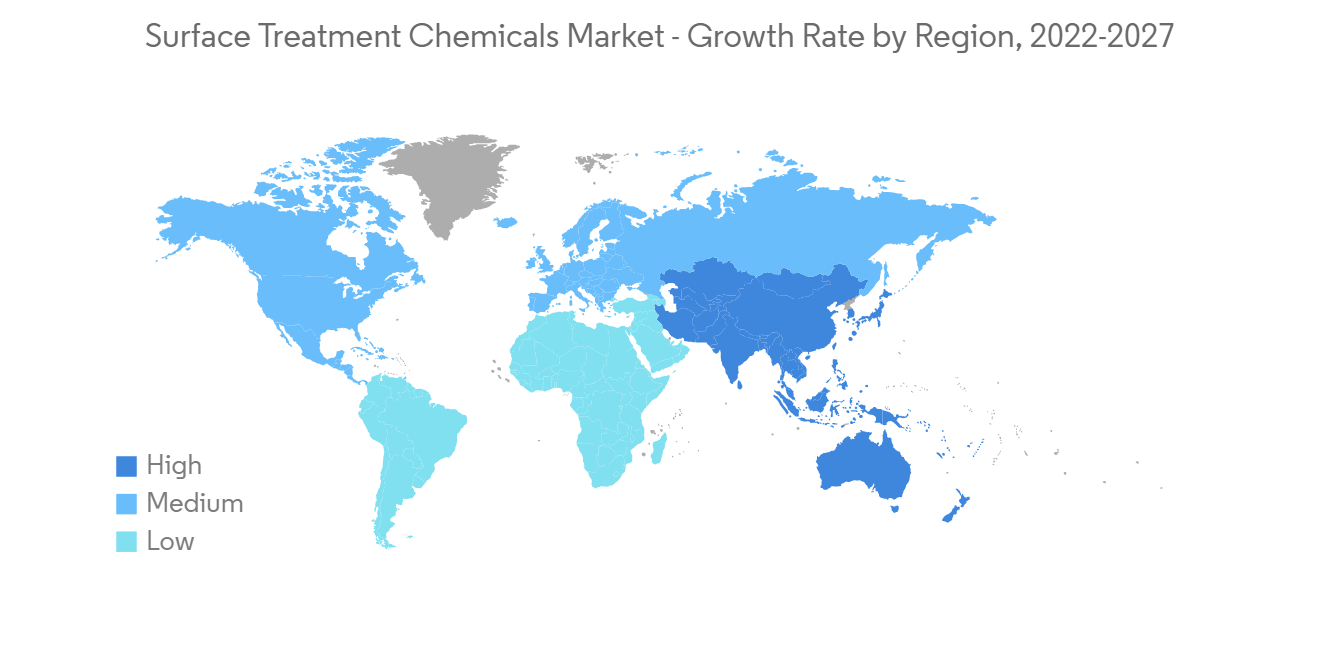

- 収益と予測では、アジア太平洋が予測期間中に世界市場を独占し、表面処理化学品の世界市場で最も高い市場シェアを占めると予想されます。

表面処理化学品市場の動向

自動車・輸送機器分野が大きなシェアを占めると予想される

- 電気自動車、軽量車、自律走行車、人工知能、コネクティビティなどの進歩により、自動車分野は最も破壊的な旅路を歩んでいます。自動車とその部品の製造に使用される材料は、自動車全体の性能を達成する上で重要であることが証明されました。

- 表面処理化学品は、自動車部品の全体的な性能に大きな影響を与えると考えられています。

- 数ある産業の中でも、自動車産業は長い間、表面処理化学品の最も大きな需要を生み出してきました。主要な企業はすべて、自動車部門に表面処理化学品を供給しています。

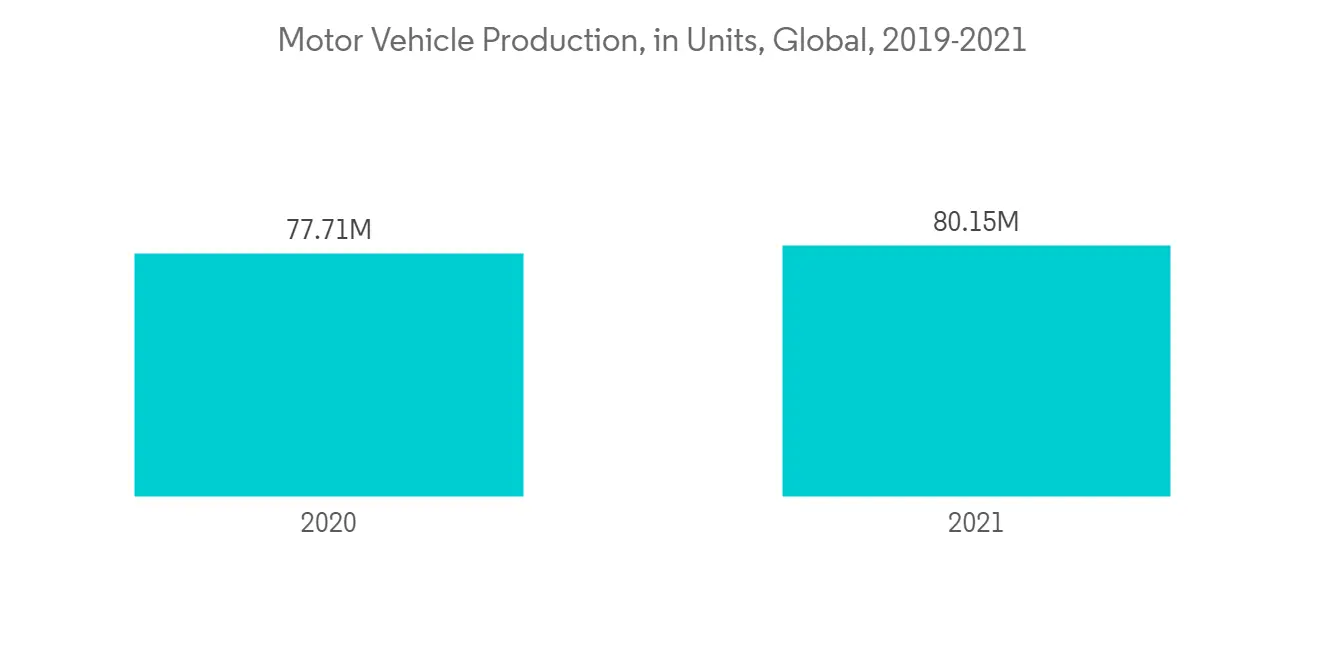

- 国際自動車製造者機構(OICA)によると、2021年の世界の自動車生産台数は約8015万台であり、2020年の7771万台と比較しています。

- 世界貿易機関(WTO)によると、2021年の自動車製品の輸入額は約2860億米ドルで、米国は第2位の輸入国でした。同時に、同国は約1,260億米ドル相当の自動車製品を輸出しています。

- 上記のすべての要因が自動車・輸送分野を牽引し、予測期間中に表面処理化学品の需要を高めると予想されます。

アジア太平洋地域が市場を独占する

- アジア太平洋は、市場シェアと市場収益の面で表面処理化学品市場を独占しています。同地域は、予測期間中、その優位性を維持し続けるものと思われます。

- 同地域、特に中国において、住宅だけでなく商業施設の建設にも表面処理化学品が採用されつつあることが、同地域の市場を押し上げると予想されます。

- 長寿命で耐摩耗性の高い製品に対する需要の高まりは、木材、ガラス、宝飾品、医療など、さまざまな産業で採用されています。建設業の評価では、製品の需要が高いです。表面処理化学品は、自動車セクターの拡大に伴い、より大きな拡大を経験しています。

- 中国国家統計局によると、中国の建設産業は継続的に拡大しており、2021年の総生産額はおよそ25兆9,000億人民元(3兆8,200億米ドル)に達するとされています。都市化の進展に乗じて、中国の建設業は同年に29兆人民元(4兆2,800億米ドル)以上の生産額を生み出しています。

- 国際自動車建設機構(OICA)によると、中国の自動車生産台数は2020年の2522万台に対し、2021年には2608万台となっています。

- 工業化は市場の需要にも影響を及ぼしています。重機は定期的な保護が必要なため、生産者は錆などを防ぐために表面処理剤でコーティングしています。

- さらに、インドや日本などの国も、調査された市場の成長に貢献しています。このため、予測期間中、表面処理化学品市場の需要はさらに高まると予想されます。

表面処理化学品市場の競合分析

表面処理化学品市場は、その性質上、断片的なものです。市場の主要メーカーには、PPG Industries Inc.、Atotech Deutschland GmbH、Henkel AG &、DOW、Chemetall Inc.、その他(順不同)があります。

その他の特典です。

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 促進要因

- 自動車産業の成長

- 感染症の影響を軽減するための表面処理化学品の使用について

- 抑制要因

- 化学製品からバイオベース(グリーン)製品へのシフト

- 有害クロム成分の排出に関する厳しい環境規制について

- 産業バリューチェーン分析

- ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品・サービスの脅威

- 競合の度合い

第5章 市場セグメンテーション(金額ベース市場規模)

- 化学品タイプ

- メッキ用化学品

- クリーナー

- コンバージョンコーティング

- その他(冷却水、塗料用剥離剤など)

- ベース素材

- メタル

- プラスチック

- その他の基材(ガラス、合金、木材)

- エンドユーザー産業

- 自動車・輸送機器

- 建設

- エレクトロニクス

- 産業機械

- その他(石油・ガスパイプライン、電力、軍需、パッケージなど)

- 地域

- アジア太平洋地域

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米地域

- 中東・アフリカ地域

- 南アフリカ

- サウジアラビア

- その他中東・アフリカ地域

- アジア太平洋地域

第6章 競合情勢

- M&A、ジョイントベンチャー、コラボレーション、契約など

- 市場シェア(%)**/ランキング分析

- 主要なプレーヤーが採用した戦略

- 企業プロファイル

- Aalberts Surface Technologies

- ALANOD GmbH & Co. KG

- Atotech

- Atotech Deutschland GmbH

- Bulk Chemicals Inc.

- Chemetall Inc.

- ChemTech Surface Finishing Pvt. Ltd.

- DOW

- Henkel AG & Co. Ltd.

- IONICS

- Nippon Paint Holdings Co., Ltd.

- OC Oerlikon Management AG

- PPG Industries Inc.

- Quaker Chemical Corporation

- The Sherwin-Williams Company

- YUKEN Surface Technology, S.A. de C.V.

第7章 市場機会と今後の動向

- 建設業における表面処理剤の使用について

- バイオベースやクロムフリーの表面処理化学品への関心の高まり

- プリント配線板における表面処理化学品の消費拡大

The Surface Treatment Chemicals market is expected to register a CAGR of over 5% during the forecast period.

The outbreak of COVID-19 has positively impacted the market growth for surface treatment chemicals. During the COVID-19 pandemic, new surface treatment chemicals were developed to counteract the virus. For example, ALANOD GmbH's MIRO UV-C product effectively destroyed the COVID-19 virus and is utilized as a material for reflectors in sanitizing equipment. Another significant development in the fight against the COVID-19 virus has been the availability of high-performance and medical-grade transparent film to produce face shields.

Key Highlights

- Over the short term, the growth in the automotive industry due to the demand for consumers and the use of surface treatment chemicals to reduce the impact of infections is propelling the market growth during the forecast period.

- However, the growth in concerns regarding the effects of chemical surface treatment has led to the shift from chemicals to bio-based (green) products to abide by the regulations brought into the industry. Environmental sustainability, energy efficiency, and multiple application capabilities restrain manufacturers in niche product development and will further hamper market growth.

- Nevertheless, using surface-treating chemicals in construction for commercial and residential infrastructure and growing interest in bio-based and chromium-free surface-treatment chemicals will provide ample growth opportunities in the future. They will likely create lucrative opportunities for the market over the forecast period.

- In terms of revenue, Asia-Pacific is expected to dominate the global market during the forecast period and dominate the highest market share in the global surface treatment chemicals market.

Surface Treatment Chemicals Market Trends

The Automotive and Transport Segment is Anticipated to Hold a Significant Share

- The automotive sector is through the most disruptive journey, with advances in electric vehicles, lightweight vehicles, autonomous vehicles, artificial intelligence, and connectivity. The materials used to manufacture automobiles and their components proved critical in achieving overall vehicle performance.

- Surface treatment chemicals are thought to have a significant impact on the overall performance of automobile parts.

- Among numerous industries, the automotive industry has long been the most significant demand generator for surface treatment chemicals. All the major firms supply surface treatment chemicals to the car sector.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), world motor vehicle production in 2021 was about 80.15 million, compared to 77.71 million units in 2020.

- According to the World Trade Organization (WTO), with a value of about USD 286 billion in 2021, the United States was the second largest importer of automotive products. Simultaneously, the country exported automotive products worth around USD 126 billion.

- All the factors above are expected to drive the automotive and transport segment, enhancing the demand for surface treatment chemicals during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific dominates the surface treatment chemicals market in terms of market share and market revenue. The region is set to continue to flourish in its dominance over the forecast period.

- The growing adoption of surface treatment chemicals in construction for commercial as well as residential infrastructure in the region, especially in China, is expected to boost the market in the region.

- Rising demand for long-lasting and wear-resistant products is employed in a variety of industries, including wood, glass, jewelry, medicine, and others. In construction ratings, the product is in high demand. Surface treatment chemicals are experiencing greater expansion as the automobile sector expands.

- According to the National Bureau of Statistics of China, China's construction industry has been continuously expanding, with a total production value of roughly CNY 25.9 trillion (USD 3.82 trillion) in 2021. Taking advantage of growing urbanization, China's construction sector generated more than CNY 29 trillion (USD 4.28 trillion) in production that year.

- According to the Organisation Internationale des Constructeurs d'Automobiles (OICA), motor vehicle production in China was 26.08 million units in 2021, compared to 25.22 million units in 2020.

- The industrialization has also had an impact on market demand. Heavy machinery requires regular protection, so producers coat it with surface treatment chemicals to prevent rust and other problems.

- Furthermore, countries like India and Japan have also been contributing to the growth of the market studied. This is expected to further drive the demand for the surface treatment chemicals market over the forecast period.

Surface Treatment Chemicals Market Competitor Analysis

The Surface Treatment Chemicals market is fragmented in nature. Some major manufacturers in the market include PPG Industries Inc., Atotech Deutschland GmbH, Henkel AG & Co. Ltd., DOW, Chemetall Inc., and others (in no particular order).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growth in the Automotive Industry

- 4.1.2 The Use of Surface Treatment Chemicals to Reduce the Impact of Infections

- 4.2 Restraints

- 4.2.1 Shift from Chemicals to Bio-based (Green) Products

- 4.2.2 Strict Environmental Regulations for the Emission of Hazardous Chromium Components

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Value)

- 5.1 Chemicals Type

- 5.1.1 Plating Chemicals

- 5.1.2 Cleaners

- 5.1.3 Conversion Coatings

- 5.1.4 Other Chemical Types (Coolants, Paint Strippers)

- 5.2 Base Material

- 5.2.1 Metals

- 5.2.2 Plastics

- 5.2.3 Other Base Materials (Glass, Alloys, Wood)

- 5.3 End-User Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Construction

- 5.3.3 Electronics

- 5.3.4 Industrial Machinery

- 5.3.5 Others (Oil and Gas Pipeline, Power, Military, Packaging, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) **/ Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aalberts Surface Technologies

- 6.4.2 ALANOD GmbH & Co. KG

- 6.4.3 Atotech

- 6.4.4 Atotech Deutschland GmbH

- 6.4.5 Bulk Chemicals Inc.

- 6.4.6 Chemetall Inc.

- 6.4.7 ChemTech Surface Finishing Pvt. Ltd.

- 6.4.8 DOW

- 6.4.9 Henkel AG & Co. Ltd.

- 6.4.10 IONICS

- 6.4.11 Nippon Paint Holdings Co., Ltd.

- 6.4.12 OC Oerlikon Management AG

- 6.4.13 PPG Industries Inc.

- 6.4.14 Quaker Chemical Corporation

- 6.4.15 The Sherwin-Williams Company

- 6.4.16 YUKEN Surface Technology, S.A. de C.V.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Use of Surface-treating Chemicals in Construction

- 7.2 Growing Interest in Bio-Based and Chromium-Free Surface Treatment Chemicals

- 7.3 Increasing Surface Treatment Chemical Consumption in Printed Circuit Boards