|

市場調査レポート

商品コード

1237841

非航空分野市場- 成長、動向、および予測(2023年-2028年)Non-Aeronautical Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 非航空分野市場- 成長、動向、および予測(2023年-2028年) |

|

出版日: 2023年03月03日

発行: Mordor Intelligence

ページ情報: 英文 105 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

非航空分野の市場は、予測期間中にCAGR7%以上の成長が見込まれています。

世界の航空セクターは、COVID-19のパンデミックにより、未曾有の困難に直面しました。パンデミックは航空部門に大きな影響を与え、旅客輸送量の大幅な減少を招き、空港運営の需要に悪影響を及ぼしました。国際航空運送協会(IATA)のレポート2020によると、世界の航空貨物需要は2020年に大幅な減少を示しました。アジア太平洋地域の航空会社は、2020年2月の貨物需要が2020年1月と比較して15.5%減少したことを示しました。航空セクターは、規制の緩和と航空交通量の増加により、COVID-19後に大幅な回復を見せ、その結果、非航空分野サービスに対する需要が増加しました。

航空セクターの急速な拡大と、旅客の快適性を高めるための空港での非航空サービスへの投資の増加が、市場の成長を後押ししています。空港数の増加により、食事サービス、レンタカーサービス、貨物処理システムなどの非航空系サービスの需要が高まり、市場成長を後押ししています。非航空分野サービスの収益は、旅客にさまざまなサービスを提供するコンセッショナリーに課される賃料によって生み出されます。これらのサービスには、空港の駐車場、銀行、広告、小売、空港敷地内のレンタカー施設などが含まれます。

欧州連合(EU)の運輸保安庁(TSA)やその他の規制機関による航空貨物のスクリーニングに関する厳しい規制により、いくつかの空港は既存の貨物スクリーニングシステムの強化を余儀なくされています。このように、空港における非航空分野サービスに対する需要の高まりが、市場成長の原動力となっています。

非航空分野の市場動向

グランドハンドリングシステムは、予測期間中に大きな成長を遂げるでしょう。

グランドハンドリングシステム分野は、予測期間中に著しい成長を示すと推定されます。航空機のグランドハンドリングシステムは、航空機が地上にいる間やターミナルゲートに駐機している間に、航空機にサービスを提供するために使用される機器から構成されています。地上支援機器には、電源システム、バゲージハンドリングシステム、セキュリティシステム、ウォーターサービス車などが含まれます。

航空旅行者の増加や航空分野への支出の増加は、グランドハンドリングシステムに対する需要の高まりにつながります。国際航空運送協会の報告書によると、航空部門はパンデミック後に力強い回復を示しました。航空旅客の全体数は、2024年までに40億人に達するでしょう。同レポートによると、2021年には2019年の47%の水準になるとのことです。航空旅客数は、2022年に83%、2023年に94%、2024年に103%、2025年に111%に改善すると予想されています。これは、空港の成長につながり、グランドハンドリングシステムの需要を生み出します。2022年5月、人工知能企業のG3 Global Bhdは、マレーシア空港ホールディングスBhd(MAHB)から、KL国際空港(KLIA)とKLIA2の空港統合セキュリティ・安全システム(AIS3)を設計・開発する1億1838万RMの契約を締結しました。このように、グランドハンドリングシステムの調達契約が増加していることが、市場の成長を促進しています。

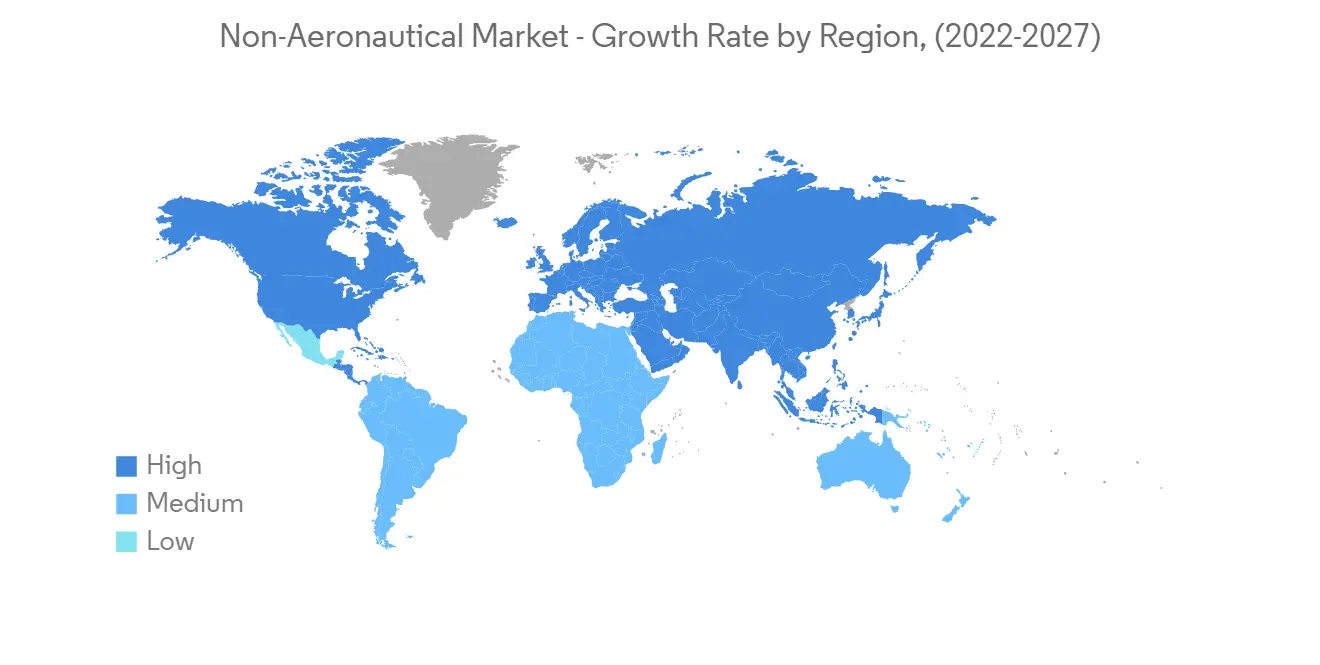

アジア太平洋地域が予測期間中に最も高い成長率を示すと予測される

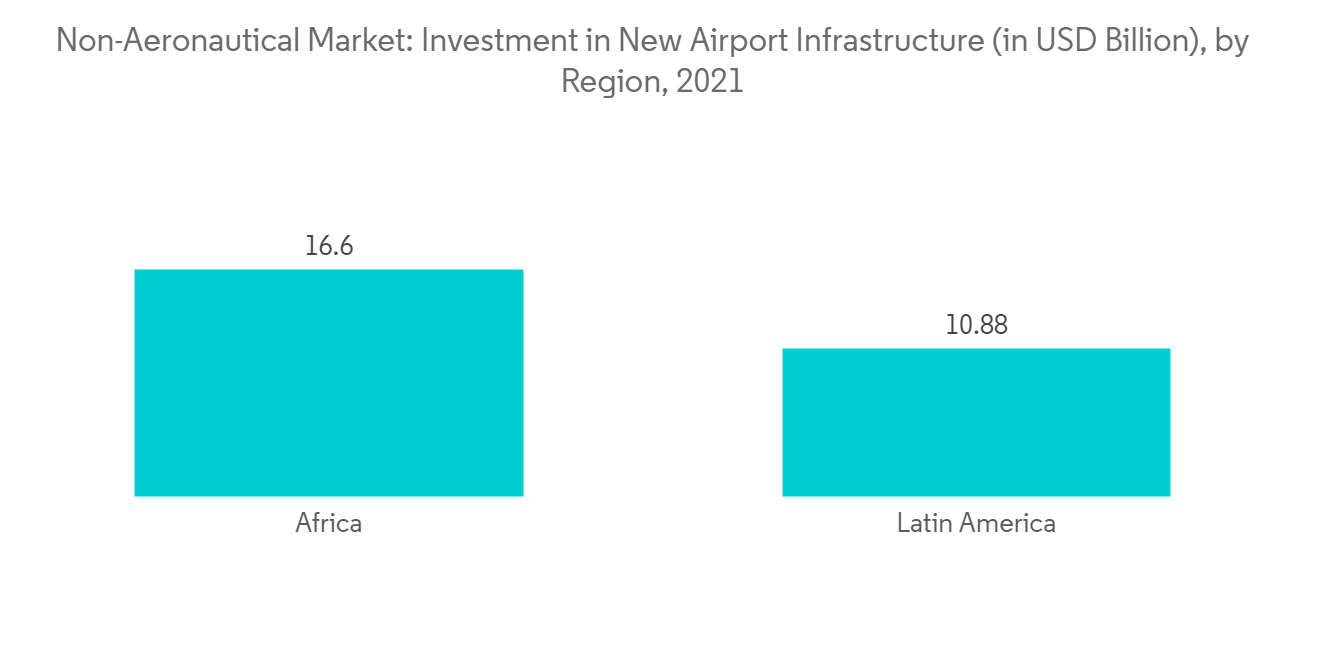

アジア太平洋地域は、予測期間中に著しい成長を見せると予測されています。この成長は、貨物輸送量の増加、空港数の増加、中国やインドなどの新興国による航空分野への支出増加によるものです。アジア太平洋地域では、中国、インド、日本、シンガポールなどの主要国が、新しい空港の建設や既存の空港の拡張を計画しています。空港の増加は、非航空分野サービスに対する需要の高まりにつながり、市場の成長を促進します。

2020年2月、インド政府は2024年までに100の新空港を建設すると発表しました。これにより、飲食品サービス、レンタカーサービス、手荷物取扱設備などの需要が生まれます。さらに、2022年6月には、インドの連邦民間航空大臣が、2024年から2025年までに33の貨物ターミナルを追加すると発表しました。

例えば、2022年11月、タタ・スターバックスは、ネットワークを拡大するため、国内の6都市に8つの空港店舗を開設する予定であると発表しました。その都市とは、ブバネスワル、ベンガルール、ゴア、ジャイプール・グワハティ、ラクナウです。さらに、2022年10月には、高級チョコレートブランドのスモアが、バンガロール国際空港(BAIL)に新しいカフェをオープンしました。このように、空港での乗客の快適性を向上させるための非航空サービスへの投資の高まりが、アジア太平洋地域の市場成長を牽引しています。

非航空分野市場の競合他社分析

非航空系サービスの市場は、空港で様々なサービスを提供する複数のサプライヤーによって細分化されているのが特徴です。しかし、非航空系市場の著名なプレーヤーとしては、Aena SME SA、GROUPE ADP、香港空港公社、Airports of Thailand Plc、Fraport Group、Heathrow(SP)Ltd.などが挙げられます。業界内の競争が激化する中、サービスプロバイダーは空港での旅客体験を高めることに高い関心を寄せています。2022年8月、空港サービス事業者Aenaの子会社であるAena Desarrollo Internacionalが、ブラジル国内の11空港の30年間のコンセッション契約を獲得し、さらに5年間の延長の可能性もあります。契約は2023年2月に締結される予定です。契約金額は4億7,300万米ドルです。

その他の特典です。

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件条件

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- 産業の魅力/ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- サービス別

- フードサービス

- レンタカー

- バゲッジハンドリングシステム

- その他サービス

- 地域別

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- ロシア

- その他欧州

- アジア太平洋地域

- インド

- 中国

- 日本

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ地域

- 中東・アフリカ地域

- アラブ首長国連邦

- サウジアラビア

- 南アフリカ

- その他中東・アフリカ地域

- 北米

第6章 競合情勢について

- ベンダーのマーケットシェア

- 企業プロファイル

- AENA SME SA

- GROUPE ADP

- Airport Authority Hong Kong

- Airports of Thailand Plc

- Fraport Group

- London Heathrow Airports Limited

- Japan Airport Terminal Co. Ltd

- Vinci SA

- Airports de Paris SA

- Korea Airports Corp

第7章 市場機会と今後の動向

The non-aeronautical market is expected to grow a CAGR of more than 7% during the forecast period.

The global aviation sector faced unprecedented challenges due to the COVID-19 pandemic. The pandemic significantly affected the aviation sector, which resulted in a drastic reduction in passenger traffic, which has negatively affected demand for airport operations. According to the International Air Transport Association (IATA) report 2020, the global demand for air cargo witnessed a significant decline in 2020. Asia-Pacific airlines witnessed cargo demand fall by 15.5% in February 2020 compared to January 2020. The aviation sector saw significant recovery post-COVID-19 due to reduced restrictions and increased air traffic, which resulted in the growing demand for non-aeronautical services.

The rapid expansion of the aviation sector and increasing investments in non-aeronautical services at airports for enhancing passenger comfort drive the market's growth. An increasing number of airports leads to the growing demand for food services, car rental services, cargo handling systems, and other non-aeronautical services boosting the market growth. The revenue for non-aeronautical services is generated through rents charged to concessionaires that offer a wide range of services to passengers. These services include car parking at the airports, banking, advertising, retail, and car rental facilities on the airport site.

Stringent regulations related to air cargo screening by the Transportation Security Agency (TSA) and other regulatory bodies in the European Union (EU) have forced several airports to enhance their existing cargo screening systems. Thus, the growing demand for non-aeronautical services at airports drives market growth.

Non-Aeronautical Market Trends

Ground Handling Systems Will Showcase Significant Growth During the Forecast Period

The ground handling systems segment is estimated to show remarkable growth during the forecast period. The aircraft ground handling systems consists of equipment used to offer services to an aircraft while it is on the ground and parked at a terminal gate. The ground support equipment includes power systems, baggage handling systems, security systems, water service vehicles, and others.

An increasing number of air travelers and growing spending on the aviation sector leads to rising demand for ground handling systems. According to the International Air Transport Association report, the aviation sector witnessed a strong recovery after the pandemic. The overall number of air passengers will reach 4 billion by 2024. The report stated that in 2021, the numbers were 47% of 2019 levels. The number of air travelers is expected to improve to 83% in 2022, 94% in 2023, 103% in 2024, and 111% in 2025. This leads to growing airports, creating demand for ground handling systems. In May 2022, G3 Global Bhd, an artificial intelligence company, signed a contract worth RM118.38 million from Malaysia Airports Holdings Bhd (MAHB) to design and develop an airport-integrated security and safety system (AIS3) for the KL International Airport (KLIA) and KLIA2. Thus, the rising procurement contract of ground handling systems propels market growth.

Asia Pacific is Estimated to Show Highest Growth During the Forecast Period

Asia-Pacific is projected to show remarkable growth during the forecast period. The growth is due to rising cargo traffic, a growing number of airports, and increasing expenditure on the aviation sector from emerging economies such as China and India. In Asia-Pacific, major countries like China, India, Japan, and Singapore are planning to construct new airports and expand the existing airports. An increasing number of airports leads to rising demand for non-aeronautical services, thus driving the growth of the market.

In February 2020, the Indian government announced that 100 new airports would be built by 2024. This will create demand for food and beverage services, car rental services, baggage handling equipment, and other services. Furthermore, in June 2022, the Union Civil Aviation Minister of India announced that the country will have 33 additional cargo terminals by 2024-2025.

For instance, in November 2022, Tata Starbucks announced that it is planning to open eight airport stores across six cities in the country to expand its network. The cities are Bhubaneswar, Bengaluru, Goa, Jaipur Guwahati, and Lucknow. Furthermore, in October 2022, Smoor, the luxury chocolate brand opened a new cafe at the Bangalore International Airport (BAIL). Thus, rising investment in non-aeronautical services for improving passenger comfort at the airport drives market growth across the Asia Pacific.

Non-Aeronautical Market Competitor Analysis

The market for non-aeronautical services is fragmented in nature and is characterized by several suppliers who provide various services at airports. However, some of the prominent players in the non-aeronautical market are Aena SME SA, GROUPE ADP, Airport Authority Hong Kong, Airports of Thailand Plc, Fraport Group, and Heathrow (SP) Ltd. With the growing competition in the industry, the service providers are highly focused on enhancing passenger experience at airports. In August 2022, Aena Desarrollo Internacional, a subsidiary of airport services operator Aena, won a concession contract for 11 airports in Brazil for 30 years, with the possibility of an additional five years. The contract is scheduled to be signed in February 2023. The value of the contract was USD 473 million.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Industry Attractiveness / Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Services

- 5.1.1 Food Services

- 5.1.2 Car Rentals

- 5.1.3 Baggage Handling Systems

- 5.1.4 Other Services

- 5.2 By Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Russia

- 5.2.2.5 Rest of Europe

- 5.2.3 Asia Pacific

- 5.2.3.1 India

- 5.2.3.2 China

- 5.2.3.3 Japan

- 5.2.3.4 Rest of Asia Pacific

- 5.2.4 Latin America

- 5.2.4.1 Brazil

- 5.2.4.2 Rest of Latin America

- 5.2.5 Middle East and Africa

- 5.2.5.1 United Arab Emirates

- 5.2.5.2 Saudi Arabia

- 5.2.5.3 South Africa

- 5.2.5.4 Rest of Middle East and Africa

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 AENA SME SA

- 6.2.2 GROUPE ADP

- 6.2.3 Airport Authority Hong Kong

- 6.2.4 Airports of Thailand Plc

- 6.2.5 Fraport Group

- 6.2.6 London Heathrow Airports Limited

- 6.2.7 Japan Airport Terminal Co. Ltd

- 6.2.8 Vinci SA

- 6.2.9 Airports de Paris SA

- 6.2.10 Korea Airports Corp