|

市場調査レポート

商品コード

1237832

電気自動車用モーターマイクロコントローラー市場- 成長、動向、および予測(2023年-2028年)Electric Vehicle Motor Micro Controller Market - Growth, Trends, And Forecasts (2023 - 2028) |

||||||

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。

| 電気自動車用モーターマイクロコントローラー市場- 成長、動向、および予測(2023年-2028年) |

|

出版日: 2023年03月03日

発行: Mordor Intelligence

ページ情報: 英文 100 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

現在、電気自動車用モーターマイクロコントローラー市場の規模は33億6,000万米ドルで、今後5年間で69億3,000万米ドルに達すると予想され、CAGRは15.58%に達するとされています。

コロナウイルスの世界の大流行により、電気自動車用モーターマイクロコントローラーの市場は、深刻な操業停止、販売減少、自動車生産停止などの悪影響を受けています。ロックダウンの実施やコロナウイルスの世界の急速な拡大により、EVM(Electric Vehicle Motor)コントローラの市場は苦境に立たされています。自動車産業のメーカーは、エコシステムの混乱や電気自動車の販売減少による損失を補填しています。

一方、世界の自動車産業は、COVID-19の販売減少から回復しつつある一方で、別の危機がその復活を阻んでいます。世界の半導体の不足により、世界中の自動車の生産が混乱し、新車の販売が遅れる可能性があります。現代のインフォテインメントシステム、ADAS(先進運転支援システム)、ABS(アンチロック・ブレーキ・システム)などの電子安定化システムに活用される電子制御ユニットの必須部品であるマイクロコントローラーの不足は、自動車メーカーに減産を強いています。その結果、自動車メーカーは不足が改善するまで特定の場所での生産を停止しています。一方、市場は近い将来、急速に動き出すと予想されています。

自動車のタスクの自動化を担当するマイクロコントローラーは、自動化の進展に伴い需要が高まっています。MCUは、自動車のさまざまな部品に電気を分配したり、排気システムをきれいに保ったり、燃料使用量を減らしたりといった自動タスクを実行するために自動車に採用されています。軽量、高性能、低燃費のため、電気自動車は発展途上国でますます人気が高まっています。バッテリー駆動の電気自動車は、低排出ガスであることから、消費者の間で人気が高まっています。電気自動車に最先端の部品を使用するため、大手自動車メーカーは投資と生産能力の拡大を進めています。

さらに、自動車の電動化に伴い、電気自動車(EV)の要件に合わせた新鮮で特殊なMCUの需要が高まっています。業界各社は、EVの需要の急増に対応するため、最先端の商品を開発し、多大な研究開発費を投入しています。

電気自動車用モーターマイクロコントローラーの市場動向

世界の電気自動車普及の高まり

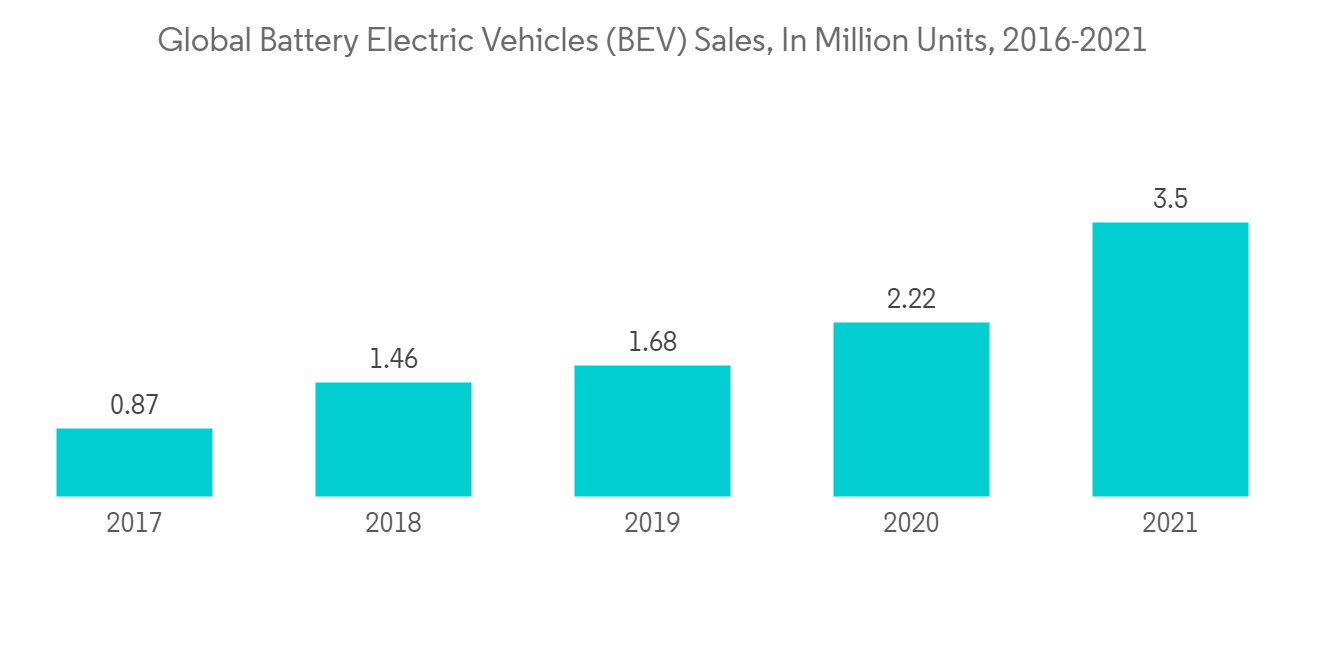

BEVやPHEVの販売台数の増加、材料の進歩やパッケージングの改善によるパワートレイン部品のコストダウンが市場を牽引しています。また、電池の高コスト化により、車両性能やパワーエレクトロニクスの強化が必要となっています。

さらに、消費者が従来の自動車よりも電気自動車を選択することを奨励するために、世界各国の政府によってさまざまなプログラムや政策が実施されています。2025年までに150万台の電気自動車の普及を目指すカリフォルニア州のZEVプログラムは、電気自動車の購入を奨励するそのような取り組みの一つです。このほか、インド、中国、英国、韓国、フランス、ドイツ、ノルウェー、オランダなどでも、さまざまな優遇措置がとられています。

COVID-19の普及後、電気自動車の販売台数は大きく伸びた。世界各国の政府によるロックダウンは、経済を減速させ、電気自動車や充電インフラシステムの販売に打撃を与えました。インバーターやリチウムイオン電池パックなどの追加部品の入手に影響が出ました。電気自動車に不可欠なコンポーネントがパワーインバーターです。電気自動車に不可欠な部品がパワーインバーターで、バッテリーからのエネルギーを変換することでトラクションモーターを使い、自動車を推進させます。

電気自動車のメーカーは、消費者に受け入れられるかどうかという大きな課題に直面しています。充電インフラの不足、EVの高コスト(EVのコストはエントリーレベルの高級車とほぼ同じ)などの要因から、電気自動車がもたらすメリットにもかかわらず、消費者は購入に消極的です。COVID-19の影響で、インドを含むいくつかの国は、5万基以上の充電ステーションを建設し、充電インフラを改善する計画を保留せざるを得ませんでした。

重要なのは、いくつかのOEMが電気自動車を生産するためだけに製品ラインを再編するつもりであることです。例えば、ゼネラルモーターズは2021年に、2025年までに電気自動車と自律走行車に200億米ドルを費やすと発表しました。2023年までに、20の新しい電気自動車モデルを導入し、中国と米国で年間100万台以上の電気自動車を販売する意向です。

2024年までに、フォルクスワーゲンは大衆向けブランド全体で電気自動車に360億米ドルを投資する意向です。フォルクスワーゲンは、2025年までに電気自動車が世界販売台数の25%以上を占めるようになると主張しています。

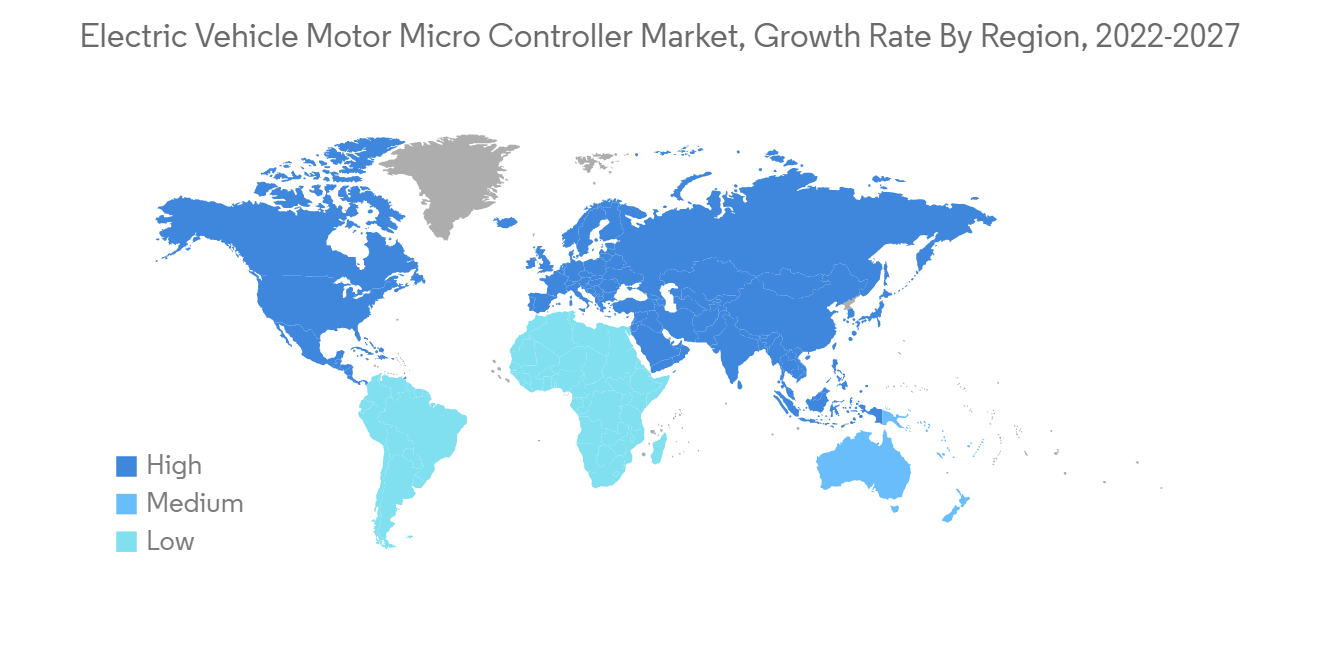

アジア太平洋地域が市場をリードする

電気自動車の世界市場は、アジア太平洋地域が大半を占めています。予測期間中、市場は大きく成長すると予想され、中国が電気自動車の販売をリードしています。

中国と日本は、最先端の電気自動車の開発と技術的進歩を支援しています。また、インドネシアのような国でも、重要な電気モビリティプロジェクトが実施されています。

中国は、世界の電気自動車産業における主要なプレーヤーです。さらに、中国政府は人々に電気自動車を導入するよう奨励しています。同国は、2040年までに電気モビリティに完全に切り替えることを計画しています。中国の電気乗用車市場も世界最大級の規模であり、ここ数年増加傾向にあります。予測期間中もより高い成長が見込まれており、電気自動車用コネクタの需要にも好影響を与えると思われます。

状況が正常化するにつれ、日本における電気自動車の需要も増加の兆しを見せています。需要の増加に対応するため、パートナーシップ、ベンチャー、合併などが、日本における電気自動車用部品の販売を後押しすると予想されます。

- 2022年4月:ホンダがゼネラルモーターズと提携し、手頃な価格の電気自動車を開発。自動車メーカーは、主に小型クロスオーバーSUV向けに、GMのUltium EVバッテリーをベースとした新しいアーキテクチャを構築する予定です。

インドの電気自動車市場は成長段階にあります。TATA、Mahindra、MGなど、インドの自動車メーカーは、手頃な価格の電気自動車を提供するための取り組みを行っています。さらに、政府も国内の温室効果ガスの排出を減らすために電気モビリティを支援しています。

韓国政府は、今後10年間の電気自動車産業について高い目標を掲げています。同国は、車両とそれを支えるインフラに多額の投資を行っています。例えば、韓国政府は電気自動車の購入を補助金で支援することも行っています。ソウル政府は、電気自動車1台につき約7,500米ドルの補助金を支給しています。

自動車メーカーも、増大する電気自動車の需要を拡大するために投資を行っています。例えば、以下のようなものです。

- 現代自動車は、2023年までに世界でのシェアを拡大するために160億米ドルを投資する計画です。新製品の製造・発売の増加に伴い、マイクロコントローラーの需要は今後数年間で拡大することが予想されます。

電気自動車用モーターマイクロコントローラー市場の競合他社分析

電気自動車用モーターマイクロコントローラー市場には、Continental AG、Infineon Technologies AG、Toyota Industries Corporation、Robert Bosch GmbH、BorgWarner Incなどの著名企業が存在しています。競合、消費者の好みの頻繁な変化、急速な技術進歩は、予測期間中の市場の成長に脅威となると予想されます。

電気自動車用モーターマイクロコントローラーの世界市場における主要企業は、M&Aや新施設の建設を通じて、その存在感を高めています。例えば、以下のようなものです。

- 2022年10月:長城汽車の発表によると、江蘇省無錫市にJianjun WEI会長とWensheng Technology(Tianjin)(Wensheng Technology)を中心に、Xindong Semiconductor Technologyが設立される予定です。登録資本金は5,000万人民元(約420万米ドル)で、この合弁会社は主に集積回路設計とマイクロコントローラーの生産に注力する予定です。

その他の特典。

- エクセル形式の市場予測(ME)シート

- 3ヶ月のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件条件

- 調査対象範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターズ5フォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- タイプ別

- AC永久磁石同期モータコントローラ

- AC非同期モーターコントローラ

- DCモーターコントローラ

- パワー出力

- 1~20KW

- 21~40KW

- 41~80KW

- 80KW以上

- 推進タイプ別

- プラグインハイブリッド車

- バッテリー電気自動車

- 燃料電池電気自動車

- 地域別に見る

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- ロシア

- その他欧州

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- その他アジア太平洋地域

- 世界のその他の地域

- 南米

- 中東・アフリカ地域

- 北米

第6章 競合情勢について

- ベンダーのマーケットシェア

- 企業プロファイル

- BorgWarner Inc.

- Continental AG

- Delphi Technologies PLC.

- Denso Corporation

- FUJITSU

- Hitachi Automotive Systems

- Mitsubishi Electric

- Robert Bosch GmbH

- Siemens AG

- Texas Instruments

- Toyota Industries Corporation

- Infineon Technology AG

- Delta Electronics

- Renesas Electronics Corporation

第7章 市場機会と今後の動向

Currently, the Electric Vehicle Motor Micro Controller Market is valued at USD 3.36 Billion and is expected to reach USD 6.93 Billion over the next five years at a CAGR of 15.58%.

The global coronavirus pandemic has had a negative impact on the market for Electric Vehicle Motor (EVM) controllers due to severe lockdowns, decreased sales, and a halt in automobile production. The market for Electric Vehicle Motor (EVM) controllers has suffered due to the widespread implementation of lockdowns and the rapid global spread of the coronavirus. Manufacturers in the automotive industry are making up for losses caused by the disruption of the ecosystem and the decline in sales of electric vehicles.

On the other hand, while the global automotive industry is recovering from the COVID-19 sales drop, another crisis is preventing its revival. Production of automobiles around the world is disrupted by a worldwide shortage of semiconductors, which may delay the sales of new vehicles. The scarcity of microcontrollers, which are an essential component of the electronic control units that are utilized in contemporary infotainment systems, Advanced Driver Assist Systems (ADAS), Anti-lock Braking Systems (ABS), and other electronic stability systems, has forced automobile manufacturers to reduce production. As a result, automakers halt production at specific locations until the shortage improves. On the other hand, the market is anticipated to move quickly in the near future.

Microcontrollers that are in charge of automating vehicle tasks are in high demand due to the development of automation. MCUs are employed in automobiles to carry out automatic tasks like distributing electricity to various vehicle components, keeping the exhaust system clean, and lowering fuel usage. Due to their low weight, high performance, and low fuel consumption, electric cars are becoming increasingly popular in developing nations. Battery-powered electric vehicles are becoming increasingly popular with consumers due to their low emissions. To use cutting-edge components for electric vehicles, major automakers are investing and expanding their production capacity.

Additionally, as vehicles become electrified, there is a growing demand for fresh, specialized MCUs that are tailored to meet the requirements of Electric Vehicles (EVs). Companies in the industry are developing cutting-edge goods and funding great R&D efforts to meet the spike in demand for EVs.

Electric Vehicle Motor Micro Controller Market Trends

Increased Electric Vehicle Adoption Globally

The market is being driven by increased sales of BEVs and PHEVs, as well as lower costs for powertrain components due to material advancements and improved packaging arrangement. In addition, the high cost of batteries has necessitated enhancements to vehicle performance as well as power electronics.

In addition, various programs and policies have been implemented by governments worldwide to encourage consumers to choose electric vehicles over conventional ones. The California ZEV program, which aims to have 1.5 million electric vehicles on the road by 2025, is one such initiative that encourages the purchase of electric vehicles. India, China, the United Kingdom, South Korea, France, Germany, Norway, and the Netherlands are additional nations that provide various incentives.

After COVID-19 spread, sales of electric vehicles increased significantly. Lockdowns imposed by governments worldwide have slowed the economy and hurt sales of electric vehicles and charging infrastructure systems. The availability of additional components, such as inverters and lithium-ion battery packs, was affected. An integral component of electric vehicles is a power inverter. It uses a traction motor to propel the vehicle by converting energy from the batteries.

Manufacturers of electric vehicles have faced a significant challenge in gaining consumer acceptance. Due to factors such as a lack of charging infrastructure and the high cost of EVs (EV costs are almost the same as those of entry-level luxury cars), consumers have been reluctant to purchase electric vehicles despite the benefits they provide. Due to COVID-19, several nations, including India, had to put their plans to construct over 50,000 charging stations and improve the charging infrastructure on hold.

Significantly, several OEMs intend to restructure their product lines solely to produce electric automobiles. For instance, General Motors announced in 2021 that by 2025, it would spend USD 20 billion on electric and autonomous vehicles. By 2023, the company intends to introduce 20 new electric models and sell more than 1 million electric cars annually in China and the United States.

By 2024, Volkswagen intends to invest USD 36 billion in electric vehicles across its mass-market brands. The business claims that by 2025, electric vehicles will account for at least 25% of its global sales.

Asia-Pacific is Leading the Market

Asia-Pacific accounts for the majority of the global market for electric vehicles. Over the forecast period, the market is expected to grow significantly, with China leading the sales of electric vehicles.

China and Japan support cutting-edge electric vehicle development and technological advancement. Significant electric mobility projects are also being implemented in nations like Indonesia.

China is a key player in the global electric vehicle industry. Moreover, the government of China is encouraging people to adopt electric vehicles. The country is planning to switch to electric mobility by 2040 completely. The Chinese electric passenger car market is also one of the largest worldwide and has been increasing over the last few years. It is expected to grow higher in the forecast period, which will also positively impact the demand for electric vehicle connectors.

As the situation is normalizing, the demand for electric vehicles in Japan shows signs of growth. To cater to the rising demand, partnerships, ventures, and mergers are expected to boost the sales of electric cars components in Japan; for instance,

- April 2022: Honda partnered with General Motors to develop affordable electric vehicles. Automakers plan to create a new architecture based on GM's Ultium EV battery, primarily for small crossover SUVs.

The Indian electric vehicle market is in its growing stage. Automobile manufacturers in India, such as TATA, Mahindra, MG, etc., are taking initiatives to provide affordable electric driving options. Moreover, the government is also supporting electric mobility to reduce the exhaust emissions of greenhouse gases in the country.

The South Korean government has set high goals for its electric vehicle industry over the next ten years. The country is making heavy investments in vehicles and infrastructure to support them. For instance, the government of South Korea is also supporting the purchase of electric cars with a subsidy. The Seoul government is providing a subsidy of approximately USD 7,500 for each electric passenger car.

Car manufacturers are also investing to scale up the growing demand for electric vehicles. For instance,

- Hyundai Motors plans to invest USD 16 billion to increase its market share in the world by 2023. With the increase in the manufacturing and launching of new products, the demand for microcontrollers is bound to grow in the upcoming years.

Electric Vehicle Motor Micro Controller Market Competitor Analysis

The Electric Vehicle Motor Micro Controller Market has a presence of prominent players like Continental AG, Infineon Technologies AG, Toyota Industries Corporation, Robert Bosch GmbH, BorgWarner Inc., etc. The competition, frequent changes in consumer preferences, and rapid technological advancements are expected to pose a threat to the market's growth during the forecast period.

Major players in the global market for Electric Vehicle Motor (EVM) controllers are expanding their presence through mergers and acquisitions or the construction of new facilities. For instance,

- October 2022: Xindong Semiconductor Technology Co., Ltd. will be established in Wuxi, Jiangsu, with Jianjun WEI, its chairman, and Wensheng Technology (Tianjin) Co., Ltd. (Wensheng Technology), according to Great Wall Motor's announcement. With a registered capital of CNY 50 million (around USD 4.20 million), the joint venture will primarily focus on integrated circuit design and the production of microcontrollers.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Porters 5 Force Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 AC Permanent Magnet Synchronous Motor Controller

- 5.1.2 AC Asynchronous Motor Controller

- 5.1.3 DC Motor Controller

- 5.2 Power Output

- 5.2.1 1 to 20 KW

- 5.2.2 21 to 40 KW

- 5.2.3 41 to 80 KW

- 5.2.4 Above 80 KW

- 5.3 By Propulsion Type

- 5.3.1 Plug-in Hybrid Vehicle

- 5.3.2 Battery Electric Vehicle

- 5.3.3 Fuel Cell Electric Vehicle

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Russia

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Rest of the World

- 5.4.4.1 South America

- 5.4.4.2 Middle-East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles*

- 6.2.1 BorgWarner Inc.

- 6.2.2 Continental AG

- 6.2.3 Delphi Technologies PLC.

- 6.2.4 Denso Corporation

- 6.2.5 FUJITSU

- 6.2.6 Hitachi Automotive Systems

- 6.2.7 Mitsubishi Electric

- 6.2.8 Robert Bosch GmbH

- 6.2.9 Siemens AG

- 6.2.10 Texas Instruments

- 6.2.11 Toyota Industries Corporation

- 6.2.12 Infineon Technology AG

- 6.2.13 Delta Electronics

- 6.2.14 Renesas Electronics Corporation