|

市場調査レポート

商品コード

1641958

ソフトウェア定義ストレージ:市場シェア分析、産業動向、成長予測(2025年~2030年)Software-Defined Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| ソフトウェア定義ストレージ:市場シェア分析、産業動向、成長予測(2025年~2030年) |

|

出版日: 2025年01月05日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

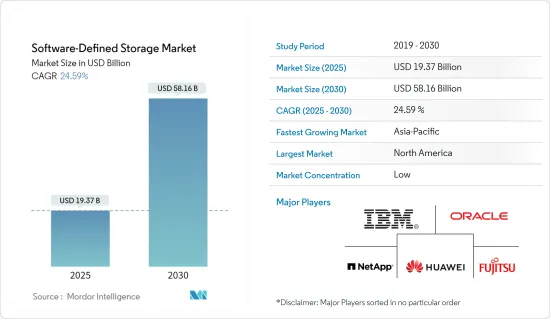

ソフトウェア定義ストレージの市場規模は、2025年に193億7,000万米ドルと推定され、予測期間中(2025~2030年)のCAGRは24.59%で、2030年には581億6,000万米ドルに達すると予測されています。

ソフトウェア定義ストレージ(SDS)により、企業はハードウェアプラットフォームからストレージリソースを抽象化でき、柔軟性、効率性、高速なスケーラビリティを実現できます。ソフトウェアで設計されたデータセンター(SDDC)アーキテクチャでは、リソースはサイロに置かれるのではなく、簡単に自動化、オーケストレーションできます。データによる効率とビジネス処理を改善する必要性が、中小企業におけるSDSソリューションの需要を後押ししています。

競合環境のため、企業は競争力を高めるために新しいテクノロジーに重点を移しています。SDSの利用は、プロセス制御を自動化し、従来のハードウェアをソフトウェアに置き換えることで、コストを最小限に抑えるのに役立ちます。

さまざまな企業で非構造化データが急増しているため、信頼性と安全性に優れたスケーラブルなストレージアーキテクチャに対する需要が高まっています。また、IoTの世界の普及に伴い、エッジで生成されるデータは急速に増加しています。SDSモデルは、導入の柔軟性を高め、単一のインターフェイスを通じてあらゆるストレージプラットフォームでソフトウェアを使用できるようにすることで、これらのニーズに対応します。

このテクノロジーは従来のストレージ方式よりも優れているため、デジタルトランスフォーメーションが進む企業やIT組織は、データストレージのニーズにSDSを採用する可能性が高いです。しかし、SDSへの移行を管理するための熟練したオペレータの必要性とセキュリティの懸念が、市場の成長を妨げると思われます。

市場の主要ベンダーは、データ保護と信頼性を強化したSDSソフトウェアソリューションを展開しています。

COVID-19の大流行により、民間および公共部門は従来のチャネルからデジタルチャネルに移行し、市民、企業、公共部門のスタッフが遠隔地から公共サービスにアクセスし、データを安全に共有できるようになった。ソフトウェア定義ストレージは、パンデミック時に企業にとって重要であることを証明し、パンデミック後もデータストレージの継続的な成長が見込まれています。

ソフトウェア定義ストレージ市場動向

BFSIセグメントは大幅な成長が見込まれる

- 銀行は、急激なデータ増加を伴う高度に規制された業務環境であり、各拠点間で連携するアプライアンスとの統合、スケールアップ、アウトを行うために、安全性と可用性の高いストレージ機能が必要です。ソフトウェア定義ストレージ・ソリューションは、膨大なデータセットの処理、暗号化によるファイルへのアクセス制限、さらにはデータのバックアップとリカバリなど、BFSI業務の改善に役立ちます。

- BFSIセグメントは競争が激しく、ITインフラが市場のダイナミックな需要に柔軟に対応できるよう、テクノロジーを活用しています。Software-Definedデータセンターは、銀行がアグリゲーターアプリを立ち上げることを可能にし、小売顧客が頻繁に使用するアプリを統合します。食品、旅行、eコマースなど、さまざまな使用事例を1つのアプリで簡単に操作できたり、決済オプションを統合できたりといった利点が、顧客の日常的な銀行業務に役立っています。

- BFSIの膨大なデータをより良く管理するニーズの高まりは、ソフトウェア定義ストレージ市場で大きなシェアを占めています。BFSIセグメントは、予測期間中に最も速い成長を記録すると予測されています。これは、競争上の優位性を獲得し、同セグメントで進行中のデジタル変革を後押しするために、顧客データ分析の需要が増加していることに起因しています。

- デジタル経済の拡大に伴い、データは銀行業界にとって不可欠な要素となっています。Software-Definedインフラストラクチャーとストレージ・ソリューションにより、世界の銀行は、オンプレミスのデータに迅速にアクセスし、分析し、クラウド上で共有することが可能になり、フロントオフィスからバックオフィス業務まで対応できるようになった。

アジア太平洋地域が最速の成長を遂げる見込み

- アジア太平洋地域では、さまざまな企業で非構造化データの量が急増しており、オンプレミス・デバイスやクラウド環境に保存されています。また、この地域全体でモノのインターネット(IoT)が普及し、エッジで生成されるデータが急激に増加しています。

- オンライン決済の導入は急激に増加しており、企業が処理する必要のある膨大な量のデータが毎日生成されるため、ソフトウェア定義ストレージ・ソリューションの需要が高まっています。

- さらに、Huaweiを通じて中国でSDSを提供しているFalconStorなどの主要ベンダーは、中国を含むアジア太平洋地域の顧客/企業はITサービスにとって最大の潜在市場の1つであり、最新のストレージソリューションへの移行に前向きであると指摘しています。移行傾向は主に、データセキュリティ、リカバリ、仮想リソースと非仮想リソースの統合といった課題を克服するためです。

- クラウドストレージの利用は、国内のインターネットユーザー数の増加に牽引され、積極的に増加する見通しです。

- 中国やインドのような新興国は、依然としてストレージを従来のハードウェアに依存しており、技術の進歩に対応するためにデジタルトランスフォーメーションの必要性が高まっています。これらの国は、予測期間中、ソフトウェア定義ストレージ(SDS)サプライヤーに潜在的な商機を提供すると予想されます。

ソフトウェア定義ストレージ業界の概要

ソフトウェア定義ストレージ市場は細分化されており、IBM Corporation、Oracle Corporation、NetApp Inc.などの大手企業が参入しています。市場の主要企業は継続的に新製品を革新し、M&Aや生産能力拡大などの活動を活発化させ、競争をさらに激化させています。

2023年11月マルチクラウドデータ管理ソリューションのプロバイダーであるDDNは、次世代ソフトウェア定義ストレージプラットフォームであるDDN Infiniaを発表しました。このプラットフォームは、データオーケストレーションとAIベースの最適化を活用し、コンピューティングとジェネレーティブAIを加速します。DDN Infiniaは、マルチテナント、コンテナ化、最高レベルのスピードと効率性を、管理の容易さと強力なセキュリティ属性と組み合わせています。このソリューションは、データ管理に求められるワークフローを簡素化します。

2023年9月カナダの投資銀行であるTD証券は、為替変換や大口取引などのホールセール・バンキングに重点を置いているが、TD証券のブロック・ストレージは複数のストレージ・ポケットから構成されており、メンテナンスが困難でした。TD証券では、一般的なインフラ・スペシャリストがストレージを管理していました。そこでTD証券は、ソフトウェア定義ストレージシステムであるDell PowerMaxの導入を決定しました。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場概要

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- 産業バリューチェーン分析

- マクロ経済が市場に与える影響の評価

第5章 市場力学

- 市場促進要因

- 企業全体のデータ量の急増

- プロセス産業を遠隔管理するための産業モビリティに対する需要の増加

- 市場の課題

- 高コストと設置の煩雑さ

第6章 市場セグメンテーション

- タイプ別

- ブロック

- ファイル

- オブジェクト

- ハイパーコンバージドインフラ

- 企業規模別

- 中小企業

- 大企業

- エンドユーザー業界別

- BFSI

- 通信・IT

- 政府機関

- その他エンドユーザー

- 地域別

- 北米

- 欧州

- アジア

- ラテンアメリカ

- 中東・アフリカ

第7章 競合情勢

- 企業プロファイル

- IBM Corporation

- Oracle Corporation

- Netapp Inc.

- Huawei Technologies Co. Ltd

- Fujitsu Limited

- Genetec Inc.

- VMWare Inc.(Dell Inc.)

- Hitachi Vantara Corp.

- Pure Storage Inc.

- Promise Technology Inc.

- FalconStor Software Inc.

- StarWind Software Inc.

第8章 投資分析

第9章 市場の将来

The Software-Defined Storage Market size is estimated at USD 19.37 billion in 2025, and is expected to reach USD 58.16 billion by 2030, at a CAGR of 24.59% during the forecast period (2025-2030).

The software-defined storage (SDS) enables organizations to abstract storage resources from the hardware platform, offering flexibility, efficiency, and faster scalability. In the software-designed data center (SDDC) architecture, resources can be easily automated and orchestrated rather than residing in siloes. The need to improve efficiency and business processing with data drives the demand for SDS solutions in small and medium-sized enterprises.

Due to the competitive environment, companies have shifted their focus toward new technology to have a competitive edge. SDS usage helps minimize the cost by automating process controls and replacing traditional hardware with software.

The booming volume of unstructured data across various enterprises augments the demand for a scalable storage architecture that is reliable and secure. In addition, with the proliferation of IoT globally, the data generated at the edge is rapidly increasing. The SDS model addresses these needs by increasing deployment flexibility and enabling organizations to use the software with any storage platform through a single interface.

Due to this technology's advantages over traditional storage methods, enterprises or IT organizations undergoing digital transformation will likely adopt SDS for their data storage needs. However, the need for more skilled operators to manage the transition toward SDS and security concerns will hinder the market's growth.

The key vendors in the market have been rolling out SDS software solutions with enhanced data protection and reliability, owing to the growing requirements of large companies in the banking and telecom sectors.

The COVID-19 pandemic resulted in private and public sectors shifting from traditional channels to digital channels to enable citizens, businesses, and public sector staff to access public services and securely share data from remote locations. Software-defined storage has proven its importance for businesses during the pandemic and is anticipated to see continued growth in data storage post-pandemic.

Software-Defined Storage Market Trends

The BFSI Segment is Expected to Witness Significant Growth

- The banks are a highly regulated operational environment with exponential data growth and require highly secure and highly available storage capabilities to integrate, scale up, and out with appliances that link together across sites. The software-defined storage solutions help improve BFSI operations, including handling massive data sets, limited access to files with encryption, and even data backup and recovery.

- The BFSI segment is highly competitive, leveraging technology to ensure its IT infrastructure is highly flexible to meet dynamic market demands. Software-defined data centers enable banks to launch an aggregator app, consolidating the frequently used apps by retail customers. Benefits such as ease of operation from a single app for different use cases like food, travel, and e-commerce and integration of payment options are helping customers in everyday banking activities.

- The rising need for better managing vast data from BFSI contributes a substantial share of the software-defined storage market. The BFSI segment is anticipated to record the fastest growth during the forecast period, attributed to the increasing demand for customer data analysis to achieve a competitive advantage and boost the ongoing digital transformation in the segment.

- With the increase in the digital economy, data is an essential part of the banking industry. Software-defined infrastructure and storage solutions enable global banks to rapidly access, analyze, and share on-premises data in the cloud from front-to-back office operations.

Asia-Pacific is Expected to Witness Fastest Growth

- Asia-Pacific is experiencing rapid growth in the volume of unstructured data across various enterprises, which is being stored in on-premises devices and cloud environments. Also, with the proliferation of the internet of things (IoT) across the region, the data generated at the edge is drastically increasing.

- The adoption of online payments is rising exponentially, generating a huge amount of data daily, which the companies need to process, propelling the demand for software-defined storage solutions.

- Moreover, the key vendors, such as FalconStor, which provides SDS in China through Huawei, indicated that customers/enterprises in Asia-Pacific, including China, are one of the greatest potential markets for IT services and are positive about switching to modern storage solutions. The propensity to shift is mainly to overcome challenges such as data security, recovery, and the integration of virtual and non-virtualized resources.

- The use of cloud storage is poised to increase aggressively, driven by the country's rising number of internet users.

- Emerging economies like China and India are still dependent on traditional hardware for storage and the need for digital transformation to stay up with technological advancements; these countries are expected to provide a potential commercial opportunity for software-defined storage (SDS) suppliers during the forecast period.

Software-Defined Storage Industry Overview

The software-defined storage market is fragmented, with major players like IBM Corporation, Oracle Corporation, and NetApp Inc. The key players in the market are continuously innovating new products and rising activities such as mergers and acquisitions and capacity expansion, further increasing the competition.

November 2023: DDN, a provider of multi-cloud data management solutions, has announced DDN Infinia, a next-generation software-defined storage platform. This platform leverages data orchestration and AI-based optimization to accelerate computing and generative AI. DDN Infinia combines multi-tenancy, containerization, and the highest levels of speed and efficiency with ease of management and powerful security attributes. The solution simplifies workflows for the data management demands.

September 2023: TD Securities, a Canadian investment bank that focuses on wholesale banking such as currency conversion and large trades, introduced its TD Securities' block storage setup made up of several storage pockets, making it hard to maintain. General infrastructure specialists managed storage at TD Securities. TD Securities has thus selected to move forward with a software-defined storage system, Dell PowerMax.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porters Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Assessment of Impact of Macroeconomic on the Market

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Rapidly Growing Volume of Data Across Enterprises

- 5.1.2 Increased Demand for Industrial Mobility for Remotely Managing the Process Industry

- 5.2 Market Challenges

- 5.2.1 High Cost and Compliacted in Installation

6 MARKET SEGMENTATION

- 6.1 By Type

- 6.1.1 Block

- 6.1.2 File

- 6.1.3 Object

- 6.1.4 Hyper-converged Infrastructure

- 6.2 By Size of Enterprise

- 6.2.1 Small and Medium Enterprise

- 6.2.2 Large Enterprise

- 6.3 By End-user Industries

- 6.3.1 BFSI

- 6.3.2 Telecom and IT

- 6.3.3 Government

- 6.3.4 Other End-user Industries

- 6.4 By Geography

- 6.4.1 North America

- 6.4.2 Europe

- 6.4.3 Asia

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Oracle Corporation

- 7.1.3 Netapp Inc.

- 7.1.4 Huawei Technologies Co. Ltd

- 7.1.5 Fujitsu Limited

- 7.1.6 Genetec Inc.

- 7.1.7 VMWare Inc. (Dell Inc.)

- 7.1.8 Hitachi Vantara Corp.

- 7.1.9 Pure Storage Inc.

- 7.1.10 Promise Technology Inc.

- 7.1.11 FalconStor Software Inc.

- 7.1.12 StarWind Software Inc.