|

市場調査レポート

商品コード

1431744

航空インフラ:市場シェア分析、産業動向、成長予測(2024~2029年)Aviation Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| 航空インフラ:市場シェア分析、産業動向、成長予測(2024~2029年) |

|

出版日: 2024年02月15日

発行: Mordor Intelligence

ページ情報: 英文 110 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

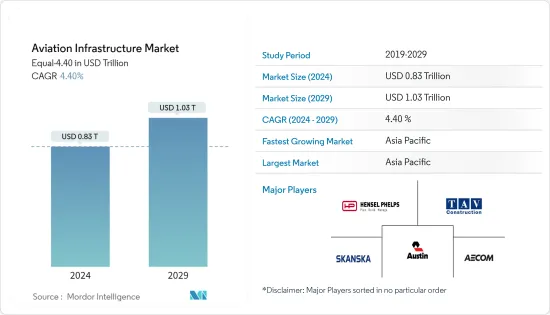

航空インフラ市場規模は2024年に8,300億米ドルと推定され、2029年には1兆300億米ドルに達し、予測期間中(2024-2029年)にCAGR 4.40%で成長すると予測されます。

民間航空機の運航、航空旅客数、将来の航空要件を満たすための航空インフラ・プロジェクトが世界的に大きく伸びていることが、今後数年間の調査対象市場の成長につながると予想されます。様々な航空当局が、商業運航の増加や空港のボトルネック問題の増加により、既存のインフラ企業と提携すると予想されています。これは、将来の航空需要に対応できる持続可能な空港インフラ・プロジェクトの開拓を確実にするためであり、それによって長期的に調査対象市場を牽引することになります。

その一方で、航空当局が課す厳しい規制などの要因が、調査対象市場の成長を妨げています。また、人工知能やブロックチェーン技術の利用が拡大することで、航空インフラ企業にとってのビジネスチャンスが拡大し、それによって市場が牽引されることが期待されています。

航空インフラ市場の動向

ターミナルセグメントは予測期間中に著しい成長を示す

航空インフラ市場において、ターミナルセグメントは著しい成長を示すと予測されます。世界の航空事業の増加に起因する空港ターミナル建設プロジェクトの大幅な増加や、空港のボトルネック問題を緩和する必要性が、今後数年間の市場の成長に弾みをつけると予想されます。

世界の航空産業は、航空交通旅客数の増加と相まって航空業務の増加により、近年著しい成長を遂げています。現在、さまざまな空港ターミナルが飽和レベルに達しようとしており、このような問題を緩和するために、いくつかの新しい空港ターミナル建設プロジェクトが増加しています。さらに、さまざまな空港インフラ企業も現在、将来の航空需要に対応できる新鋭空港ターミナルを建設するため、研究開発への投資拡大に取り組んでいます。

例えば、2023年11月、大手航空インフラ企業のヘンセル・フェルプス(Hensel Phelps)は、米国テキサス州に位置するサンアントニオ国際空港の新17ゲート・ターミナル建設で10億米ドル相当の契約を獲得したと発表しました。同社はまた、同ターミナルの継続的な計画と最終的な建設の監督も担当します。同様に2023年9月には、プネー国際空港の統合ターミナルビル(NITB)が2023年10月に運用を開始する予定でした。このプロジェクトには、インフラ整備の一環として、10のエアロブリッジと72のチェックインカウンターが含まれていました。新ターミナルビルの建設には、立体駐車場も含まれる予定だった。このように、飽和レベルに達する空港の数が世界的に増加していることに加え、将来の航空要件を満たすために空港ターミナルを近代化する必要性が高まっていることから、市場の見通しが明るいものとなり、予測期間中に世界的に新空港ターミナルの建設が拡大すると予想されます。

予測期間中、アジア太平洋地域が市場を独占

アジア太平洋地域は市場で最大のシェアを占めており、予測期間中もその支配が続くと予想されます。商業航空事業の増加や航空旅客輸送量の増加に起因する地域内の様々なインフラプロジェクトの成長などの様々な要因が、予測期間中に調査された市場の成長を促進すると予想されます。

同地域の民間航空事業は、近年著しい成長を遂げています。航空旅客数の増加により、同地域内の様々な航空会社は、新型で先進的な民間航空機の取得に向けて多額の投資を行っています。例えば、エア・インディアは2023年2月、国内線と国際線の両方で事業を拡大するため、250機のエアバス機を取得する計画を発表しました。一方、この地域では、近い将来の航空業界を支援することを目的とした様々な航空インフラ・プロジェクトも大幅に成長しています。

例えば、インドネシア政府は2023年11月、総工費2億6,300万米ドルの新空港建設を発表しました。別の例では、2023年6月、ベトナム空港公社がフーバイ国際空港の新ターミナル2の開業を発表しました。ターミナル2の建設は、9,600万米ドルの契約に基づいて2019年に開始されました。現在、同空港は毎年500万人の旅客に利用されると推定され、4つの旅客搭乗橋で結ばれています。このような発展は、この地域全体で調査された市場の成長を促進すると予想されます。

航空インフラ産業の概要

現在、空港インフラ関連企業は、タイムリーなインフラ・プロジェクト納入に取り組むとともに、新たな長期空港建設契約を獲得することで、市場シェアの拡大に取り組んでいます。同市場の主要企業はまた、空港当局とのパートナーシップを確立し、空港インフラ・プロジェクトの中で空港当局の要求を理解し、統合しようとしています。企業はまた、拡張現実や人工知能などの先進技術を統合して、航空業界のニーズにより良いサービスを提供することを期待しています。これは、予測期間中に調査された市場の成長を促進すると予想されます。

その他の特典

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件と市場定義

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場概要

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係の強さ

第5章 市場セグメンテーション

- 空港タイプ

- 商業空港

- 軍用空港

- 一般空港

- インフラタイプ

- ターミナル

- 管制塔

- 誘導路および滑走路

- エプロン

- 格納庫

- その他のインフラ

- 地域

- 北米

- 米国

- カナダ

- 欧州

- 英国

- ドイツ

- フランス

- その他欧州

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- ラテンアメリカ

- ブラジル

- その他ラテンアメリカ

- 中東・アフリカ

- アラブ首長国連邦

- サウジアラビア

- その他中東とアフリカ

- 北米

第6章 競合情勢

- ベンダー市場シェア

- 企業プロファイル

- Hensel Phelps

- Turner Construction Company

- Austin Industries

- AECOM

- The Walsh Group

- McCarthy Building Companies Inc.

- J.E. Dunn Construction Company

- PCL Constructors Inc.

- Skanska

- TAV Construction

- Royal BAM Group NV

- BIC Contracting LLC

- ALEC Engineering and Contracting

- Manhattan Construction Group Inc.

- Hill International Inc.

- The Sundt Companies Inc.

第7章 市場機会と今後の動向

The Aviation Infrastructure Market size is estimated at USD 0.83 trillion in 2024, and is expected to reach USD 1.03 trillion by 2029, growing at a CAGR of 4.40% during the forecast period (2024-2029).

A significant growth in terms of commercial aircraft operations, number of air traffic passengers, and aviation infrastructure projects worldwide for meeting future aviation requirements are expected to lead to the growth of the market studied in the coming years. Various aviation authorities are anticipated to partner with established infrastructure companies due to growing commercial operations and increasing airport bottleneck issues. This is to ensure the development of sustainable airport infrastructure projects capable of handling future aviation requirements, thereby driving the market studied in the long run.

On the other hand, factors such as stringent regulations imposed by aviation authorities hamper the growth of the market studied. The growing usage of artificial intelligence as well as blockchain technologies is also expected to lead to increasing business opportunities for aviation infrastructure companies, thereby driving the market studied.

Aviation Infrastructure Market Trends

Terminal Segment Will Showcase Remarkable Growth During the Forecast Period

The terminal segment is anticipated to show significant growth in the aviation infrastructure market. A substantial increase in airport terminal construction projects owing to the increasing global aviation operations, as well as the need to mitigate bottleneck issues at the airport is expected to provide a boost in the growth of the market studied in the coming years.

The global aviation industry has witnessed significant growth in recent years due to increasing aviation operations coupled with growing air traffic passenger numbers. Currently, various airport terminals are on the verge of reaching saturation levels, and this has led to an increase in several new airport terminal construction projects to mitigate such issues. Moreover, various airport infrastructure companies are also now engaged in increasing their investments in research and development to construct new and advanced airport terminals that will be capable of handling future aviation requirements.

For instance, in November 2023, Hensel Phelps, a leading aviation infrastructure company, announced that it was awarded a contract worth USD 1 billion to construct the new 17-gate terminal of the San Antonio International Airport located in Texas, United States. The company will also be responsible for overseeing the continued planning and eventual construction of the terminal. Similarly, in September 2023, the Integrated Terminal Building (NITB) at Pune International Airport was expected to start operations in October 2023. The project included 10 aerobridges and 72 check-in counters as a part of its infrastructure development. The construction of the new terminal building was to include a multilevel car parking area. Thus, a growing number of airports worldwide reaching saturation levels, as well as the increasing need to modernize airport terminals to meet future aviation requirements, is expected to generate a positive market outlook, leading to growth in the construction of new airport terminals globally during the forecast period.

Asia-Pacific Dominates the Market During the Forecast Period

Asia-Pacific held the largest shares in the market and is expected to continue its domination during the forecast period. Various factors, such as growth in various infrastructure projects within the region owing to an increase in commercial aviation operations and growing air passenger traffic, are expected to propel the growth of the market studied during the forecast period.

Commercial airline operations within the region have witnessed significant growth in recent years. Increasing air passenger numbers have led various air carriers within the region to invest significantly toward acquiring new and advanced commercial aircraft. For instance, in February 2023, Air India announced that it plans to acquire 250 Airbus aircraft in order to increase its operations in both domestic and international sectors. On the other hand, the region also witnessed substantial growth in various aviation infrastructure projects intended to support the aviation industry in the near future.

For instance, in November 2023, the Indonesian government announced the construction of a new airport that is expected to be fully operational by 2024, with a total construction cost of USD 263 million. In another instance, in June 2023, the Airport Corporation of Vietnam announced the inauguration of the new terminal 2 of the Phu Bai International Airport. The construction of Terminal 2 was flagged off in 2019 under a contract valued at USD 96 million. Currently, the airport is estimated to serve 5 million passengers each year and is connected by four passenger boarding bridges. Such developments are anticipated to drive the growth of the market studied across the region.

Aviation Infrastructure Industry Overview

The aviation infrastructure market is fragmented, with various players holding significant shares. Some of the major players in the aviation infrastructure market are Hensel Phelps, Skanska, TAV Construction, AECOM, and Austin Industries.

Currently, airport infrastructure companies are engaged in increasing their market share by engaging in timely infrastructure project deliveries as well as obtaining new long-term airport construction contracts. Key players in the market are also establishing partnerships with airport authorities to understand and integrate their requirements within airport infrastructure projects. Companies are also looking forward to integrating advanced technologies such as augmented reality and artificial intelligence to better service the needs of the aviation industry. This is expected to drive the growth of the market studied during the forecast period.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.3 Market Restraints

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Airport Type

- 5.1.1 Commercial Airport

- 5.1.2 Military Airport

- 5.1.3 General Aviation Airport

- 5.2 Infrastructure Type

- 5.2.1 Terminal

- 5.2.2 Control Tower

- 5.2.3 Taxiway and Runway

- 5.2.4 Apron

- 5.2.5 Hangar

- 5.2.6 Other Infrastructure Types

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canda

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Hensel Phelps

- 6.2.2 Turner Construction Company

- 6.2.3 Austin Industries

- 6.2.4 AECOM

- 6.2.5 The Walsh Group

- 6.2.6 McCarthy Building Companies Inc.

- 6.2.7 J.E. Dunn Construction Company

- 6.2.8 PCL Constructors Inc.

- 6.2.9 Skanska

- 6.2.10 TAV Construction

- 6.2.11 Royal BAM Group NV

- 6.2.12 BIC Contracting LLC

- 6.2.13 ALEC Engineering and Contracting

- 6.2.14 Manhattan Construction Group Inc.

- 6.2.15 Hill International Inc.

- 6.2.16 The Sundt Companies Inc.