|

|

市場調査レポート

商品コード

1196965

オフィススペースの世界市場- 成長、動向、予測(2023年~2028年)Global Office Space Market - Growth, Trends, and Forecasts (2023 - 2028) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| オフィススペースの世界市場- 成長、動向、予測(2023年~2028年) |

|

出版日: 2023年01月23日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

世界のオフィススペース市場は、予測期間中に12%のCAGRで推移すると予想されます。

多くのオフィスが無事に職場復帰を果たし、リーシングの勢いが戻ってきました。都心部を中心に引き合いが増えており、リーシング活動も活発化しています。オフィススペース市場では、純吸収量がパンデミック発生後初めてプラスに転じた。ITおよびITeSセクターは、上位都市の賃貸活動全体の主要な促進要因の一つであり、これらの企業による大量採用は、大規模な質の高いオフィススペースへの需要に影響を与えます。

COVID-19は、いくつかの世界なオフィススペース利用者の中期的な不動産戦略に影響を及ぼすと予想されます。第3四半期は、デルタの蔓延に起因するCOVID規制の再燃により、世界の一部地域で景気回復が妨げられましたが、ほとんどの国で景気は回復を続けています。不確実性は依然として継続的なテーマですが、オフィススペースは現在、需要回復の兆しを見せています。

2020年4月以降、リーシングは減少していますが、オフィススペースではいくつかの興味深い傾向が現れています。例えば、オキュピアは、パンデミックが始まった2020年4月以降、オフィススペースの更新をますます進めています。入居者は、健康やウェルネスを重視したモダンな設備を備えた新世代のオフィスを求めています。柔軟性がより重視され、分散した労働力のためのコワーキングスペースの探求に熱心なオキュッパーも出てくるでしょう。

入居者は、現在の良好な市場力学を利用して、更新の交渉を行っています。また、リースの柔軟性を高めることも検討しています。入居者の意思決定は昨年よりも早く、新世代のオフィスに注目が集まっています。各国で従業員の再入社が始まっており、多くの企業が2022年1月以降に従業員の再入社を予定しています。これにより、入居者のリーシングの意思決定はより迅速に行われるようになります。企業は、既存のオフィススペースを設計・変更し、新しい健康プロトコルに従い、なおかつ社会的な交流やコラボレーションを促進しながら、企業の確立した文化をサポートするという課題に直面することになるでしょう。

オフィススペース市場の動向

オフィススペース空室率の上昇

世界中のオフィス市場の全体的なセンチメントとアクティビティは、速度は異なるもの、改善されています。2021年第3四半期、世界のリース量は前年同期を上回りました。しかし、2019年第3四半期と比較すると25%低い水準にとどまっており、回復は進んでいるもの、まだ終わっていないことを示しています。全地域で2019年第3四半期の出来高を下回っています。2021年第3四半期、世界の純吸収量はパンデミック発生後初めてプラスに転じました。

2021年第3四半期の空室率は上昇基調を維持し、前期比30bps増の14.6%となりました。これは、パンデミック発生以来、最も遅い上昇率です。プロジェクト完了の遅れを受け、2022年は開発サイクルのピークになると予想されます。地域別には、大きく変動しています。米国では、開発完了は今年がピークで来年は大幅に減速すると予想されますが、欧州とアジア太平洋では、2022年に向けてパイプラインがそれぞれ24%、13%増加し続けると予想されます。このため、今後数カ月は空室率に上昇圧力がかかると思われます。

オフィススペース賃料の上昇

オフィスの再入居率はまだ国によって大きく異なりますが、現在世界的に上昇し始めています。これは重要なことで、新たなスペース需要が確定する前に、企業はハイブリッドオフィスやリモートワークが需要プロファイルにどのような影響を与えるかについて、より多くの証拠を必要としているのです。ほとんどの市場でテナントが入りやすい状況が続いており、家主はテナントを誘致しようと躍起になっています。しかし、一部の市場では、入居者の品質に対する要求が高まっているため、プレミアムビルやプライムビルの賃料が上昇しています。銀行・金融サービス業界は、世界的にプレミアムオフィスの圧倒的な占有率であり続けています。

国際的な企業は、パンデミック後に企業ブランドと企業文化を活性化するために職場に注目しており、従業員が利用できるアメニティやサービスが大幅に改善されることが予想されます。1年以上にわたってオフィスへのアクセスが制限されているにもかかわらず、企業は引き続きワークプレイスを企業アイデンティティの重要な構成要素として認識しており、パンデミック後に従業員を確保し活性化させるために不可欠なものと考えています。

オフィススペース市場の競合分析

世界のオフィススペース市場は非常に競争が激しく、複数の企業が参入しています。これらの企業は、市場シェアと収益性を高めるために、戦略的な協力体制を活用しています。ベンダーは、さらなる事業拡大と成長を実行するために、連続的なM&A戦略、地域拡大、研究開発、新製品導入戦略に依存しています。

その他の特典。

- エクセル形式の市場予測(ME)シート

- アナリストによる3ヶ月間のサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

- 分析手法

- 調査フェーズ

第3章 エグゼクティブサマリー

第4章 マーケットインサイト

- 現在の市場シナリオ

- 技術動向

- 産業バリューチェーン分析

- 政府の規制と取り組み

- オフィス賃料に関する洞察

- オフィススペース計画に関する考察

- COVID-19が市場に与える影響

第5章 市場力学

- 促進要因

- 抑制要因

- 機会

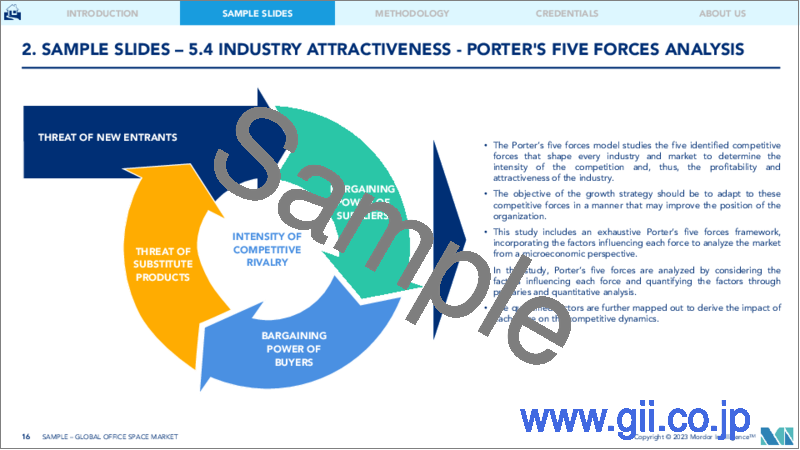

- 業界の魅力- ポーターのファイブフォース分析

- 供給企業の交渉力

- 消費者/買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

第6章 市場セグメンテーション

- 建物タイプ別

- レトロフィット

- 新築ビル

- エンドユーザー別

- IT・通信

- メディア・エンターテインメント

- 小売・消費財

- 地域別情報

- 北米

- 欧州

- アジア太平洋地域

- 世界のその他の地域

第7章 競合情勢

- 企業プロファイル

- CBRE Group Inc.

- Mitsui Fudosan Co. Ltd

- Jones Lang LaSalle Incorporated

- IWG PLC

- Regus

- WeWork

- Knotel, Inc.

- Servcorp

- The Office Group

- WOJO*

- その他の企業

第8章 市場機会と将来動向

第9章 付録

第10章 免責事項

The global office space market is expected to record a CAGR of 12% during the forecast period. Leasing momentum is back as most offices are safely implementing return-to-work. Inquiries have picked up around city centers, and so has the leasing activity. In the office space market, net absorption turned positive for the first time since the onset of the pandemic. The IT and ITeS sectors are among the prime drivers of overall leasing activity in the top cities, and bulk-hiring by these firms will influence demand for large quality office spaces.

COVID-19 is expected to influence the medium-term real estate strategy of several global office space occupiers. Renewed COVID restrictions stemming from the spread of the Delta variant impeded the recovery in some parts of the world during the third quarter, but in most countries, the economy continued to rebound. Uncertainty remains an ongoing theme; however, office spaces are now seeing signs of a demand recovery.

While leasing has declined from April 2020, some interesting trends have emerged in the office space. Occupiers, for instance, have been increasingly renewing their office spaces since April 2020, when the pandemic started. Occupiers are looking to be in new-generation offices with modern amenities with a focus on health and wellness. There will be more emphasis on flexibility, with occupiers keen to explore co-working spaces for a decentralized workforce.

Occupiers are using the current favorable market dynamics to negotiate renewals. They are looking at more flexibility in leases too. Occupiers' decisions are quicker than last year, with a focus on new-generation offices. Re-entry of employees has started in various countries, with many companies planning to get back more employees from January 2022. This will prompt occupiers to make leasing decisions quicker. Corporates will face a challenge to design and modify existing office spaces to support a company's established culture while following the new health protocols and yet promoting social interaction and collaboration.

Office Space Market Trends

Increase in Office Space Vacancy Rate

Overall sentiment and activity in office markets across the world are improving, although at differing speeds. Third-quarter of 2021, global leasing volumes were higher than a year ago. However, they remained 25% lower than Q3 2019, showing that the recovery, although underway, is far from over. All regions are below Q3 2019 volumes. The global net absorption turned positive in the third quarter of 2021 for the first time since the onset of the pandemic.

Vacancy continued its upward trajectory in Q3 2021, adding 30bps over the quarter to 14.6%. This is the slowest rate of increase since the onset of the pandemic. Following delays to project completion, 2022 is anticipated to be the peak of the development cycle. The picture fluctuates significantly by region. In the United States, development completions are expected to hit a high point this year and then slow appreciably next year, while in Europe and Asia-Pacific, the pipeline continues to grow into 2022 by 24% and 13%, respectively. This will add to the upward pressure on vacancy rates over the coming months.

Increase in Office Space Rent

Office re-entry rates still vary significantly by country but are now starting to rise around the world. This is important, as before new space requirements are cemented, corporates need more evidence of how hybrid office and remote work impacts their demand profile. Tenant-friendly conditions persist in most markets, with landlords eager to attract tenants. However, rents for premium or prime buildings have increased in some markets as occupiers increasingly look for quality. The banking and financial services industry continues to be the dominant occupier of premium office space globally.

International businesses are looking to their workplaces to revitalize their corporate brand and culture after the pandemic, which will see significantly improved amenities and services available for employees. Despite over a year of restricted access to offices, businesses continue to identify workplaces as an essential component of their corporate identity and vital to retaining and reinvigorating employees post-pandemic.

Office Space Market Competitor Analysis

The global office space market is highly competitive and consists of several players. These companies are leveraging on strategic collaborative initiatives to increase their market share and profitability. Vendors depend on successive merger and acquisition strategies, geography expansion, research and development, and new product introduction strategies to execute further business expansion and growth.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

- 2.1 Analysis Methodology

- 2.2 Research Phases

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Current Market Scenario

- 4.2 Technological Trends

- 4.3 Industry Value Chain Analysis

- 4.4 Government Regulations and Initiatives

- 4.5 Insights into Office Rents

- 4.6 Insights into Office Space Planning

- 4.7 Impact of COVID-19 on the Market

5 MARKET DYNAMICS

- 5.1 Drivers

- 5.2 Restraints

- 5.3 Opportunities

- 5.4 Industry Attractiveness - Porter's Five Forces Analysis

- 5.4.1 Bargaining Power of Suppliers

- 5.4.2 Bargaining Power of Consumers/Buyers

- 5.4.3 Threat of New Entrants

- 5.4.4 Threat of Substitute Products

- 5.4.5 Intensity of Competitive Rivalry

6 MARKET SEGMENTATION

- 6.1 By Building Type

- 6.1.1 Retrofits

- 6.1.2 New Buildings

- 6.2 By End User

- 6.2.1 IT and Telecommunications

- 6.2.2 Media and Entertainment

- 6.2.3 Retail and Consumer Goods

- 6.3 By Geography

- 6.3.1 North America

- 6.3.2 Europe

- 6.3.3 Asia-Pacific

- 6.3.4 Rest of the World

7 COMPETITIVE LANDSCAPE

- 7.1 Overview (Market Concentration and Major Players)

- 7.2 Company Profiles

- 7.2.1 CBRE Group Inc.

- 7.2.2 Mitsui Fudosan Co. Ltd

- 7.2.3 Jones Lang LaSalle Incorporated

- 7.2.4 IWG PLC

- 7.2.5 Regus

- 7.2.6 WeWork

- 7.2.7 Knotel, Inc.

- 7.2.8 Servcorp

- 7.2.9 The Office Group

- 7.2.10 WOJO*

- 7.3 Other Companies