|

|

市場調査レポート

商品コード

1137873

自動車用アルミニウム部品高圧ダイカスト(HPDC)市場- 成長、動向、予測(2022年~2027年)Automotive Aluminum Parts High-pressure Die Casting (HPDC) Market - Growth, Trends, and Forecasts (2022 - 2027) |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 自動車用アルミニウム部品高圧ダイカスト(HPDC)市場- 成長、動向、予測(2022年~2027年) |

|

出版日: 2022年10月13日

発行: Mordor Intelligence

ページ情報: 英文 90 Pages

納期: 2~3営業日

|

- 全表示

- 概要

- 目次

自動車用アルミニウム部品高圧ダイカスト(HPDC)市場は、2021年に471億6000万米ドルと評価され、2027年末には正味評価額が624億1000万米ドルを超え、予測期間に4.78%の堅実なCAGR成長を記録すると予測されています。

COVID-19のパンデミックは、2020年前半の製造施設の閉鎖や施錠により、世界的に自動車生産台数が減少し、市場に悪影響を及ぼしました。しかし、2021年に規制が徐々に開放されたことで自動車生産は回復し、さらに安定したEV販売によって市場は再び成長を取り戻しました。

乗用車や商用車の生産台数の増加により、高圧アルミダイカストで開発された自動車部品は、その優位性から市場を牽引することが期待されます。市場成長の主な要因としては、厳しい排ガス規制や企業別平均燃費規制(CAFE)の制定、欧州地域における商用車の需要増と販売増、自動車産業の成長などが挙げられます。アルミニウムは消費量の約75.0%が再利用可能であり、再生アルミニウムは無期限にリサイクルできるため、自動車部品用高圧ダイカストとして最も普及している素材です。

政府は、米国、ドイツ、英国、インド、中国などの主要な主要国全体で補助金を提供することにより、自動車メーカーを後押しし、顧客に電気自動車の導入を奨励しています。電気モビリティの成長のこの傾向は、市場で動作するプレーヤーがバッテリーハウジング、トランスミッション部品などの様々な電気自動車部品を製造することを奨励しています。

さらに、自動車や自動車分野における鉄や鋼の代わりにアルミニウムを使用することの増加や、これらの分野における資金調達の増加は、予測期間中に高圧アルミニウムダイカスト市場の成長に有利な機会を生み出すと思われます。

主な市場動向

市場の妨げとなるアルミニウム価格の上昇

2021年の世界の自動車販売台数は約6670万台で、2020年は6380万台でした。世界のパンデミックは、自動車販売を含む世界中の経済活動に影響を与え、ウイルスの拡散を抑制するためにいくつかの国で厳格なロックダウンが実施されました。そのため、2020年の自動車販売台数は、2019年と比較して14.8%減少しました。しかし、生活が正常に戻ったことで、世界的に自動車の販売台数は増加しており、これが自動車用アルミニウム部品高圧ダイカスト市場の予測期間での成長を後押しすることになります。

乗用車の需要の増加と電動モビリティの意識の高まりにより、主要プレイヤーは現在の車両の電化に期待しています。例えば、以下の通りです。

- 2022年8月、日本の自動車メーカーであるスズキ自動車は、Hansalpurin Gujaratに電気自動車バッテリー工場を設立するために 7,300カロールインドルピー相当の戦略的投資を発表しました。この工場は、インドの次期電気自動車技術に対応した先進化学電池の製造を視野に入れています。スズキは、東芝、デンソーと共同でグジャラート州にTDSリチウムイオンバッテリーグジャラート(TDSG)を設立しており、インドにおける2番目の電気自動車用電池事業となります。

- 2022年3月、Ford Motorsは、2024年末までに欧州で3台のオール電化乗用車を投入し、2026年までに欧州地域で年間60万台以上の電気自動車を販売する目標を発表しました。

- 2022年1月、General Motorsは電気自動車の生産能力を高めるため、ミシガン州の2工場に40億米ドル以上の投資を検討していることを発表しました。GMとLGエナジーソリューションは、ランシングに25億米ドルのバッテリー施設の建設を提案しています。

乗用車の販売台数の増加に伴い、HPDCの需要も有望視されています。現在、乗用車は、その軽量性と高い引張強度のために、さまざまな自動車部品にHPDCを要求しています。アルミニウム押出企業は、売上高のバーを高める示すために多額の投資を行っています。例えば、2022年8月、ラテンアメリカ最大のアルミニウム押出機であるCuprumは、自動車分野で高圧ダイカスト技術を提供するためのアルミニウムの押出のためにヌエボレオンに新しい工場を建設するために1億米ドルの投資を発表しました。

これらの要因や前述の開発を考慮すると、乗用車部門は自動車用アルミHPDCの需要に同等の勢いをもたらすと予想されます。

北米の成長ペースが速い

世界中の多くのダイカスト部品メーカーが、自動車産業向けのアルミニウム高圧ダイカスト生産プロセスの拡大に大きく投資しています。202年から2021年にかけて、北米は米国やメキシコを中心に、Nemak、Bocar、George Fischerといった大手メーカーによる新規生産工場の投資や拡張がより多く行われている主要地域の1つとして認識されています。

この地域では、CO2排出量の増加とそれに伴うCAFEやEPAの厳しい規制により、自動車メーカーが製造工程でアルミニウムの高圧ダイカスト(HPDC)部品の採用を拡大しており、同国での市場成長の推進力となっています。

メキシコは、世界第7位の自動車メーカーの1つであり、ドイツ、日本、韓国に次ぐ第4位の自動車輸出国であることから、メキシコの自動車用ダイカスト市場は新興国であると言えます。

トヨタ、メルセデス・ベンツ(日産と共同)、アウディ、BMWなどの主要自動車メーカーがメキシコに新工場を設立しました。また、ゼネラルモーターズ、フィアット・クライスラー、ヒュンダイ、ホンダなどの自動車メーカーも、既存工場の拡張に力を入れています。また、中国から米国への自動車部品の輸入関税の引き上げが最近発表されたため、中国の自動車メーカーがメキシコでの生産拠点の拡大を計画しています。

メキシコの自動車産業の発展に伴い、Tier1、Tier2、Tier3サプライヤーの存在感が著しく高まっています。自動車部品の軽量化・高剛性化の動向に伴い、予測期間中、これらのサプライヤーはHPDCで製造されたアルミニウム部品を採用する可能性が高いと考えられます。

競合情勢

自動車用アルミニウム部品高圧ダイカスト市場は、Rheinmetall Automotive、Endurance Group、Shiloh Industries、GF Casting Solutions、Ryobi Die Casting Inc、Nemakといった大手企業が参入し、細分化が進んでいます。

事業分野や製造工場の拡大、主要地域の現地メーカーとの合弁、M&Aは、市場における競争力を維持・向上させるためにプレイヤーが採用する主要な戦略です。例えば、以下の通りです。

- 2022年8月、Minda Corporation Limitedは、アルミニウムHPDC部品も含む高圧ダイカスト部品の事業開発のために、米国、アフリカ、欧州の内燃機関および電気自動車スペースにおけるいくつかのTier1およびOEMの買収を開始したと発表しています。

その他の特典。

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリストサポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場の力学

- 市場促進要因

- 市場抑制要因

- 産業の魅力- ポーターのファイブフォース分析

- 新規参入業者の脅威

- 買い手/消費者の交渉力

- 供給企業の交渉力

- 代替品の脅威

- 競争企業間の敵対関係

第5章 市場セグメンテーション

- アプリケーションタイプ

- ボディ・イン・ホワイト

- ドアフレーム

- バッテリーハウジング

- ピラー

- ルーフ部品

- その他(フロントエンドキャリア、リインフォースメント、クロスビーム、インパネサポート)

- シャシー

- トランスミッション

- その他(サスペンション、ステアリング)

- ボディ・イン・ホワイト

- 車種別

- 乗用車

- 商用車

- 地域

- 北米

- 米国

- カナダ

- メキシコ

- その他北米地域

- 欧州

- ドイツ

- 英国

- フランス

- その他の欧州地域

- アジア太平洋地域

- 中国

- 日本

- インド

- 韓国

- その他アジア太平洋地域

- 世界のその他の地域

- ブラジル

- 南アフリカ共和国

- その他の国

- 北米

第6章 競合情勢

- ベンダーの市場シェア

- 企業プロファイル

- Georg Fischer AG

- Rheinmetall Automotive AG(KSPG AG(KS Kolbenschmidt GmbH))

- Ryobi Die Casting Inc.

- Nemak

- Endurance Technologies

- Shiloh Industries Inc.

- Pace Industries

- Brabant Alucast*

第7章 市場機会と今後の動向

The automotive aluminum parts high-pressure die casting (HPDC) market was valued at USD 47.16 billion in 2021 and is expected to surpass a net valuation of USD 62.41 billion by 2027 end, registering a solid CAGR growth of 4.78% over the forecast period.

The COVID-19 pandemic had a negative impact on the market as the shutdown of manufacturing facilities and lockdowns in the first half of 2020 resulted in a decline in vehicle production across the world. However, with the gradual opening of restrictions in 2021 vehicle production picked up and further stable EV sales help the market regain its growth.

An increase in the production of passenger cars and commercial vehicles is expected to drive the market for the automotive parts developed through high-pressure aluminum die casting owing to their advantages. Some of the major factors driving the growth of the market are the enactment of stringent emission regulations and Corporate Average Fuel Economy (CAFE) standards, an increase in the demand for commercial vehicles and sales in the European region, and the growth of the automotive industry. Approximately 75.0% of the aluminum consumed can be reused, and reclaimed aluminum can be recycled indefinitely, making it the most popular material for automotive parts high pressure die casting.

Government pushing automobile manufacturers and encouraging customers to adopt electric vehicles by providing subsidies across key major countries like the United States, Germany, United Kingdom, India, China, etc. This trend of growing electric mobility encourages players operating in the market to produce various electric vehicle components like battery housings, transmission parts, etc.

Furthermore, growth in the substitution of aluminum for iron and steel in the automotive and automobile sectors, as well as increased funding in these sectors, would create lucrative opportunities for the growth of the high-pressure aluminum die casting market during the forecast period.

Key Market Trends

Rising Aluminum Prices Hindering the Market

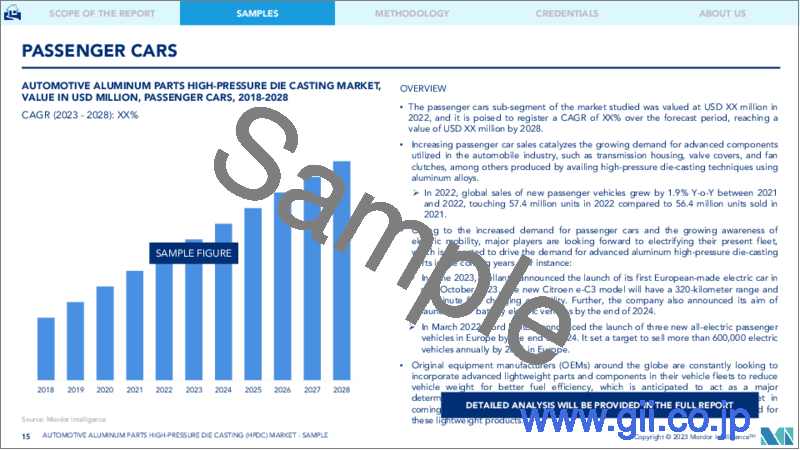

In 2021, the global car sales were around 66.7 Million, which in 2020 were 63.8 Million. The global pandemic impacted economic activities all around the world including car sales the globe, and strict lockdowns were enforced in several countries to contain the spread of the virus. Owing to this the number of cars sold in 2020 was 14.8% lower than compared in 2019. But with life returning to normalcy, the number of cars sold globally has increased which will aid the automotive aluminium parts high-pressure die casting market to grow in the forecast period.

Owing to the increase in the demand for passenger cars and the growing awareness of electric mobility, major players are looking forward to electrifying their present fleet. For instance:

- In August 2022, Japanese carmaker Suzuki Motor announced its strategic investment worth INR 7,300 crore to set up the electric vehicle battery plant at Hansalpurin Gujarat. The plant will look forward for manufacturing advanced-chemistry cell batteries for upcoming electric vehicle technology in India. This will be Suzuki's second EV battery initiative in India after TDS Lithium-Ion Battery Gujarat (TDSG), which it set up in Gujarat in collaboration with Toshiba and Denso.

- In March 2022, Ford Motors announced to include three all-electric passenger vehicles in Europe by the end of 2024 and set a target to sell more than 600,000 electric vehicles annually by 2026 in the Europe region.

- In January 2022, General Motors announced considering investing more than USD 4 billion in two Michigan factories to increase its electric car manufacturing capacity. GM and LG Energy Solution have proposed constructing a USD 2.5 billion battery facility in Lansing.

With rising sales of the passenger car segment, demand for HPDC is witnessing promising growth. Nowadays, passenger car demanding HPDC in their different car components owing to their lightweight features and higher tensile strength. Aluminium extrusion companies are investing heavily to witness elevate sales bars. For instance, in August 2022, Cuprum who is the Latin America's largest aluminium extruder announced the investment of USD 100 million to build a new plant in Nuevo Leon for extrusion of aluminium to offer high pressure die casting technology in the automotive sector.

Considering these factors and aforementioned developments, passenger car segmented is expected to provide equivalent momentum to the demand for automotive aluminium HPDC.

North America Growing at a Faster Pace

Many die casting parts manufacturers across the world have significantly invested in the expansion of the aluminum high-pressure die-casting production process for the automotive industry. During 202-2021, North America has been recognized as one of the major regions with a larger number of investments and expansions of new production plants by major manufacturers like Nemak, Bocar, and George Fischer, mainly in the United States and Mexico.

Increased CO2 emissions and subsequent stringent CAFE and EPA regulations in the region are forcing automakers to employ high-pressure die casting (HPDC) parts of aluminum more extensively in their manufacturing processes, acting as a propellant for the market's growth in the country.

The Mexican automotive die casting market is emerging, as the country is one of the largest vehicle manufacturers and seventh-largest car manufacturers in the world, as well as is the fourth-largest car exporter, behind Germany, Japan, and South Korea.

Key automakers, like Toyota, Mercedes-Benz (with Nissan), Audi, and BMW established new factories in Mexico. Other automakers, like General Motors, Fiat-Chrysler, Hyundai, and Honda are focusing on expanding their existing factories. Additionally, Chinese automobile manufacturers are planning to expand their production bases in Mexico, owing to the recent announcement of an increase in import tariff on auto parts from China to the United States.

Owing to the growing Mexican automotive industry, the presence of tier 1, tier 2, and tier 3 suppliers have been significantly increasing. With the rising trend of lightweight and robust automotive parts, the above suppliers are likely to adopt aluminum parts manufactured through HPDC, during the forecast period.

Competitive Landscape

The automotive aluminum parts high pressure die casting market is fragmented, as major players, like Rheinmetall Automotive, Endurance Group, Shiloh Industries, GF Casting Solutions, Ryobi Die Casting Inc., and Nemak.

Expansion of business segments and manufacturing plants, joint ventures with local manufacturers in key geographies, and mergers and acquisitions are the key strategies adopted by the players to maintain and improve their competitive position in the market. For instance,

- In August 2022, Minda Corporation Limited has announced that it has initiated acquisition of several Tier1 and OEMs in the internal combustion engine and electric vehicles space in United States, Africa, and Europe for developing business for high pressure die cast parts which includes aluminium HPDC parts as well.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Application Type

- 5.1.1 Body-in-white

- 5.1.1.1 Door Frames

- 5.1.1.2 Battery Housing

- 5.1.1.3 Pillar

- 5.1.1.4 Roof Components

- 5.1.1.5 Others (Front-end Carriers, Reinforcement, Cross Beams, and Instrument Panel Support)

- 5.1.2 Chassis

- 5.1.3 Transmission

- 5.1.4 Other Components (Suspension and Steering)

- 5.1.1 Body-in-white

- 5.2 Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Commercial Vehicles

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Rest of the World

- 5.3.4.1 Brazil

- 5.3.4.2 South Africa

- 5.3.4.3 Other Countries

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

- 6.2 Company Profiles

- 6.2.1 Georg Fischer AG

- 6.2.2 Rheinmetall Automotive AG (KSPG AG (KS Kolbenschmidt GmbH))

- 6.2.3 Ryobi Die Casting Inc.

- 6.2.4 Nemak

- 6.2.5 Endurance Technologies

- 6.2.6 Shiloh Industries Inc.

- 6.2.7 Pace Industries

- 6.2.8 Brabant Alucast*