|

市場調査レポート

商品コード

1689953

リン酸:市場シェア分析、産業動向・統計、成長予測(2025年~2030年)Phosphoric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

カスタマイズ可能

適宜更新あり

|

|||||||

| リン酸:市場シェア分析、産業動向・統計、成長予測(2025年~2030年) |

|

出版日: 2025年03月18日

発行: Mordor Intelligence

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

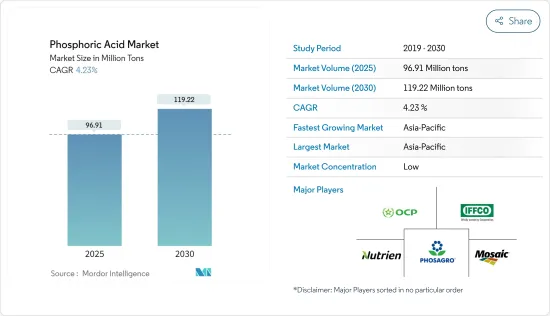

リン酸の市場規模は2025年に9,691万トンと推定され、2030年には1億1,922万トンに達すると予測され、予測期間(2025-2030年)のCAGRは4.23%です。

市場はCOVID-19の大流行によって主要な供給と製造ラインが中断され、深刻な供給不足に陥ったためマイナスの影響を受けました。リン酸の主な用途は肥料の生産です。パンデミックはまた、人々の間で食料やその他の必需品の不足を伴う作物生産の減少につながりました。パンデミックの後、市場は速度を上げ、主要産業が仕事を再開したため需要が伸びた。

主なハイライト

- リン酸の多くは肥料の原料として使用されるため、肥料業界からの需要増と飲食品業界における使用量の増加が市場需要を牽引すると予想されます。

- リン酸による健康被害と肥料価格の高騰が市場成長の妨げになると予想されます。

- とはいえ、リン酸からの希土類元素の回収や、触媒としてのキラルリン酸の商業化は、市場に有利な機会を提供すると期待されています。

- アジア太平洋地域が最も高い市場シェアを占めており、予測期間中は同地域が市場を独占する可能性が高いです。

リン酸市場の動向

市場を独占する肥料産業

- リン酸は基本的に肥料を生産するための中間体です。リン酸一アンモニウム(MAP)、リン酸二アンモニウム(DAP)、リン酸三ナトリウム(TSP)などの肥料はリン酸から生産されます。

- リン酸は、植物栄養、pH調整、石灰沈殿からの灌漑設備の浄化などに使用される多機能剤であるため、多くの肥料の主要な構成要素となっています。リン酸は植物にとって豊富なリンの供給源です。

- リン肥料は植物にとって非常に重要で、有機肥料よりも優れた働きをします。リンは植物の成熟を促進し、根の開発にも役立ちます。これは乾燥地帯では特に重要です。

- エッセンシャル・ケミカル・インダストリー(Essential Chemical Industry)によると、世界中で年間4,300万トン以上のリン酸が生産され、そのうち約90%が肥料に使用されています。

- 米国農務省海外農業局によると、中国、ロシア、米国、インド、カナダを合わせると、世界の肥料栄養素の60%以上を生産しています。ロシアと米国はそれぞれ世界の肥料の10%未満を生産し、中国は約25%を生産しています。

- 2022年9月、米国政府は国内の肥料生産を促進する5億米ドル相当のプログラムを発表し、欧州連合(EU)も同様の措置を取るよう求められています。すでに世界最大のカリ肥料供給国であるカナダは、2022年11月、他国からの出荷が止まっている隙間を埋めるため、肥料輸出を年間20%増やすと発表しました。

- 国際肥料協会(IFA)によると、中国は最大の肥料ユーザーであり、世界の肥料供給量の4分の1近くを消費しています。2022年、中国では合計5,570万トンのNPK肥料が生産されました。これは2021年には5,544万トン、2020年には5,496万トンでした。

- したがって、世界の各地域の肥料の成長動向と生産量を考慮すると、肥料産業が市場を独占する可能性が高く、その結果、予測期間中にリン酸の需要が高まると予想されます。

市場を独占するアジア太平洋地域

- アジア太平洋地域は2022年にかなりの数量シェアでリン酸市場を独占し、予測期間中もその優位性を維持すると予想されます。

- これは、中国が世界最大の肥料生産・消費国であることによる。中国、インド、東南アジア諸国などでは、リン酸の需要が継続的に増加しています。

- 中国は全体的な農業面積のおよそ7%を世界的に占め、従って世界の人口の22%に与えます。国は米、綿、ポテトおよび他を含むさまざまな穀物の最も大きい生産者、です。したがって、肥料に使用されるリン酸の需要は、同国の大規模な農業活動のおかげで急速に増加しています。

- リン酸はまた、リン酸鉄リチウム電池の生産にも広く使用されており、この分野では中国が支配的な国となっています。2022年には、中国で販売された電気自動車全体の44%がLFP電池を使用しており、次いで欧州の6%、米国とカナダの3%となっています。

- もうひとつの大肥料生産国であるインドは、第2位のユーザーです。インドの使用量の多くは、インド政府による肥料への多額の補助金によって賄われています。2022会計年度には、4,200万トンを超える肥料がインドで生産されました。インドの肥料生産量は2020会計年度にピークを迎え、4,600万トンを超えました。ここ数年、公共、協同組合、民間セクターへの投資を促進する有利な政策がとられています。

- リン酸はまた、様々なコーラやジャムのような飲食品を酸性化し、ピリッとした味や酸味を提供するために飲食品産業で使用されています。米国農務省(USDA)によると、インドの食品産業は世界第3位の食品産業にランクされています。同産業はここ数年、着実な成長を遂げており、インドは世界最大の食品生産国になると予想されています。同国の食品・食料雑貨(F&G)小売市場の売上高は、2025年までに8,500億米ドルを超えると予測されています。

- したがって、上記の理由は、予測期間にわたってアジア太平洋のリン酸市場の成長を促進する可能性が高いです。

リン酸産業の概要

リン酸市場は部分的に統合されており、世界レベルでも地域レベルでも数社が活動しています。市場の主要企業(順不同)には、OCPグループ、Mosaic、PhosAgro Group of Companies、Nutrien Ltd、IFFCOなどがあります。

その他の特典:

- エクセル形式の市場予測(ME)シート

- 3ヶ月間のアナリスト・サポート

目次

第1章 イントロダクション

- 調査の前提条件

- 調査範囲

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場力学

- 市場促進要因

- 肥料産業への高い需要

- 飲食品業界における使用量の増加

- 市場抑制要因

- リン酸による健康被害

- バリューチェーン分析

- 業界の魅力度-ポーターのファイブフォース分析

- 供給企業の交渉力

- 買い手の交渉力

- 新規参入業者の脅威

- 代替品の脅威

- 競争企業間の敵対関係

- リン酸の価格動向分析(2018年~2023年)

- 技術スナップショット

第5章 市場セグメンテーション

- エンドユーザー産業別

- 肥料

- 飲食品

- 化学品

- 医薬品

- 冶金

- その他エンドユーザー産業

- 地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- その他アジア太平洋地域

- 北米

- 米国

- メキシコ

- カナダ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- その他欧州

- 南米

- ブラジル

- アルゼンチン

- その他南米

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- その他中東とアフリカ

- アジア太平洋

第6章 競合情勢

- M&A、合弁事業、提携、協定

- 市場ランキング分析

- 主要企業の戦略

- 企業プロファイル

- Aditya Birla Chemicals

- Agropolychim

- EuroChem Group

- ICL

- IFFCO

- Innophos

- J.R. Simplot Company

- Mosaic

- Nutrien Ltd

- Phosagro

- Sterlite Copper(A Unit of Vedanta Limited)

第7章 市場機会と今後の動向

- リン酸からの希土類元素の回収

- 触媒としてのキラルリン酸の商業化

The Phosphoric Acid Market size is estimated at 96.91 million tons in 2025, and is expected to reach 119.22 million tons by 2030, at a CAGR of 4.23% during the forecast period (2025-2030).

The market was negatively impacted by the COVID-19 pandemic as it disrupted the main supply and manufacturing lines, leading to acute shortages. The main use of phosphoric acid is for producing fertilizers. The pandemic also led to a decrease in crop production, accompanied by a shortage of food and other essentials among people. After the pandemic, the market picked up speed, and the demand grew as major industries got back to work.

Key Highlights

- Since most phosphoric acid is used to make fertilizer, the rising demand from the fertilizer industry and increasing usage in the food and beverage industry are expected to drive market demand.

- Health hazards caused by phosphoric acid and the high price of fertilizers are expected to hinder the market's growth.

- Nevertheless, the recovery of rare earth elements from phosphoric acid and the commercialization of chiral phosphoric acid as a catalyst are expected to offer lucrative opportunities to the market.

- Asia-Pacific accounted for the highest market share, and the region is likely to dominate the market during the forecast period.

Phosphoric Acid Market Trends

Fertilizer Industry to Dominate the Market

- Phosphoric acid is basically an intermediate used to produce fertilizers. Fertilizers like monoammonium phosphate (MAP), diammonium phosphate (DAP), and trisodium phosphate (TSP) are produced from phosphoric acid.

- Phosphoric acid forms a key component for many fertilizers as it is a multi-function agent used for plant nutrition, pH adjustment, and cleansing irrigation equipment from lime precipitation. It is a rich source of phosphorus for plants.

- Phosphorus fertilizers are extremely important for the plant and provide better activities than organic fertilizers. Phosphorus accelerates the maturation of the plant and also provides the development of the roots. This is particularly important for dry areas.

- According to the Essential Chemical Industry, annually, more than 43 million metric tons of phosphoric acid are produced worldwide, of which about 90% are used to make fertilizers.

- According to the USDA Foreign Agricultural Service, China, Russia, the United States, India, and Canada produce more than 60% of the world's fertilizer nutrients combined. Russia and the United States each produce less than 10% of global fertilizers, while China produces approximately 25%.

- In September 2022, the US government announced programs worth USD 500 million to boost domestic fertilizer production, and the European Union is being urged to take similar action. Canada, already the world's largest supplier of potash fertilizers, announced in November 2022 that it will boost its fertilizer exports by 20% annually, filling a gap left by blocked shipments from other countries.

- According to the International Fertilizer Association (IFA), China is the largest user of fertilizer, consuming nearly one-quarter of global fertilizer supplies. In 2022, a total of 55.7 million tons of NPK fertilizer was produced in China. This was 55.44 million tons in 2021 and 54.96 million tons in 2020.

- Therefore, considering the growth trends and production of fertilizers in different regions worldwide, the fertilizer industry is likely to dominate the market, which, in turn, is expected to enhance the demand for phosphoric acid during the forecast period.

Asia-Pacific Region to Dominate the Market

- The Asia-Pacific region dominated the phosphoric acid market in 2022 with a considerable volume share, and it is expected to maintain its dominance during the forecast period.

- This is due to China being the world's largest producer and consumer of fertilizer. In countries like China, India, and Southeast Asian nations, the demand for phosphoric acid has been increasing continuously.

- China accounts for approximately 7% of the overall agricultural acreage globally, thus feeding 22% of the world's population. The country is the largest producer of various crops, including rice, cotton, potatoes, and others. Hence, the demand for phosphoric acid, which is used in fertilizers, is rapidly increasing owing to the large-scale agricultural activities in the country.

- Phosphoric acid is also used extensively in the production of lithium-iron-phosphate batteries, and China is the dominant country in this field. In 2022, 44% of the total electric vehicles sold in China used LFP batteries, followed by 6% in Europe and 3% in the United States and Canada.

- India, another large fertilizer producer, is the second largest user. Much of India's usage is fueled by the Indian government's heavy subsidization of fertilizers. In the financial year 2022, over 42 million metric tons of fertilizers were produced in India. Fertilizer production in India peaked in the financial year 2020 at over 46 million metric tons. During the last few years, there has been a favorable policy facilitating investments in the public, cooperative, and private sectors.

- Phosphoric acid is also used in the food and beverage industries to acidify foods and beverages, such as various colas and jams, providing a tangy or sour taste. According to the US Department of Agriculture (USDA), the Indian food industry ranks as the third-largest food industry globally. The industry has been experiencing steady growth over the past several years, with India anticipated to become the largest food producer in the world. The country's food and grocery (F&G) retail market is projected to surpass USD 850 billion in sales by 2025.

- Hence, the reasons mentioned above are likely to fuel the growth of the phosphoric acid market in Asia-Pacific over the forecast period.

Phosphoric Acid Industry Overview

The phosphoric acid market is partially consolidated, with several companies operating on both global and regional levels. Some of the major players in the market (not in any particular order) include OCP Group, Mosaic, PhosAgro Group of Companies, Nutrien Ltd, and IFFCO, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Market Drivers

- 4.1.1 High Demand for Fertilizer Industry

- 4.1.2 Increasing Usage in the Food and Beverage Industry

- 4.2 Market Restraints

- 4.2.1 Health Hazards Caused by Phosphoric Acid

- 4.3 Industry Value Chain Analysis

- 4.4 Industry Attractiveness - Porters Five Forces Analysis

- 4.4.1 Bargaining Power of Supplier

- 4.4.2 Bargaining Power of Buyer

- 4.4.3 Threat of New Entrant

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Intensity of Competitive Rivalry

- 4.5 Price Trend Analysis of Phosphoric Acid (2018-2023)

- 4.6 Technological Snapshot

5 Market Segmentation (Market Size in Volume)

- 5.1 By End-user Industry

- 5.1.1 Fertilizer

- 5.1.2 Food and Beverages

- 5.1.3 Chemicals

- 5.1.4 Medicine

- 5.1.5 Metallurgy

- 5.1.6 Other End-user Industries

- 5.2 By Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Mexico

- 5.2.2.3 Canada

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 Italy

- 5.2.3.4 France

- 5.2.3.5 Rest of Europe

- 5.2.4 South America

- 5.2.4.1 Brazil

- 5.2.4.2 Argentina

- 5.2.4.3 Rest of South America

- 5.2.5 Middle East and Africa

- 5.2.5.1 Saudi Arabia

- 5.2.5.2 South Africa

- 5.2.5.3 Rest of Middle East and Africa

- 5.2.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Merger and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 Agropolychim

- 6.4.3 EuroChem Group

- 6.4.4 ICL

- 6.4.5 IFFCO

- 6.4.6 Innophos

- 6.4.7 J.R. Simplot Company

- 6.4.8 Mosaic

- 6.4.9 Nutrien Ltd

- 6.4.10 Phosagro

- 6.4.11 Sterlite Copper (A Unit of Vedanta Limited)

7 Market Opportunities and Future Trends

- 7.1 Recovery of Rare Earth Elements from Phosphoric Acid

- 7.2 Commercialization of Chiral Phosporic Acid as a Catalyst