|

|

市場調査レポート

商品コード

1447710

非経口栄養バッグ市場:チャンバータイプ別、消費者別、エンドユーザー別の世界予測 2031年までParenteral Nutrition Bags Market by Chamber Type (Single-Chamber Bags, Dual-Chamber Bags, Multi-Chambered Bags), Consumer (Adults, Children), End User (Healthcare Facilities, Pharmacies & Compounding Service Providers) - Global Forecast to 2031 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 非経口栄養バッグ市場:チャンバータイプ別、消費者別、エンドユーザー別の世界予測 2031年まで |

|

出版日: 2024年03月08日

発行: Meticulous Research

ページ情報: 英文 111 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界の非経口栄養バッグ市場は、2024年から2031年にかけてCAGR 6.6%で、2031年までに12億5,000万米ドルに達すると予測されます。

本レポートでは、包括的な一次および二次調査と市場シナリオの詳細な分析に基づき、業界の主要促進要因、抑制要因、市場促進要因・課題を提供します。この市場を牽引しているのは、栄養不良の世界の有病率の上昇、未熟児出産の多さ、代謝障害の発生率の増加です。

さらに、在宅ヘルスケアの採用拡大、世界の老人人口の増加、新興経済国は、この市場に大きな成長機会をもたらしています。しかし、非経口栄養剤に関連する感染リスクに対する懸念がこの市場の成長を抑制しています。新興諸国における非経口栄養に関する認識不足は、非経口栄養バッグ市場の成長に影響を与える大きな課題です。

チャンバータイプのうち、2024年には単室式非経口栄養バッグのセグメントが非経口栄養バッグ市場で最大のシェアを占めると予想されます。シングルチャンバー型非経口栄養バッグは、非経口投与用に電解質、アミノ酸、脂質、ビタミン、炭水化物、微量元素などの栄養溶液を1つのコンパートメント内に包括的に配合・保存するように設計されています。このセグメントの大きなシェアは、1室タイプの空バッグが広く入手可能であること、1室タイプの栄養バッグの処方率が高いこと、感染のリスクが減少していること、処方ミスや投与ミスが少ないこと、2室タイプや多室タイプのバッグと比較して費用対効果が高いことなどに起因しています。

消費者の間では、2024年には成人セグメントが非経口栄養バッグ市場で最大のシェアを占めると予想されています。手術件数の増加、入院率の上昇、老人人口の増加、成人の胃腸障害有病率の増加が、同市場の最大シェアを支える要因となっています。例えば、2020年、世界疫学研究のローマ財団は、世界の40%の人々が過敏性腸症候群、機能性ディスペプシア、機能性腹痛症候群などの腸脳相互作用疾患(DGBI)に苦しんでいることを明らかにしました。こうした患者のほとんどは、必要な栄養を摂取するために非経口栄養バッグを必要とします。

エンドユーザーの中では、2024年にはヘルスケア施設セグメントが非経口栄養バッグ市場で最大のシェアを占めると予想されています。このセグメントの市場シェアが大きいのは、病気の診断や治療のために病院や診療所を訪れる患者が多いこと、病気の負担が増加していること、非経口栄養剤の処方率が関連して上昇していること、病院関連の調剤薬局に高度な調剤機器があることなどの要因によるものです。

世界の非経口栄養バッグ市場の地域別シナリオを詳細に分析することで、主要5地域の詳細な質的・量的洞察を提供します。2024年には、北米が世界の非経口栄養バッグ市場で最大のシェアを占め、次いで欧州、アジア太平洋、ラテンアメリカ、中東&アフリカが続くと予想されています。この成長の主因は、慢性疾患や感染症の流行、早産児の増加、在宅医療環境の導入拡大による非経口栄養剤の需要増です。例えば、世界保健機関(WHO)によると、2020年には約1,340万人の赤ちゃんが早産(妊娠37週未満)で生まれています。早産児は経口栄養が不可能なため、非経口的に栄養を供給する必要がある場合が多く、そのため非経口栄養の需要が増加し、市場の成長を支えています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 市場洞察

- 市場

- 概要

- 市場成長への影響要因

- 市場力学の影響分析

- 要因分析

- 主要動向

- 在宅ヘルスケアの採用拡大

- 非経口用途におけるエチレン酢酸ビニル(EVA)の使用拡大

- 規制分析

- 北米

- 米国

- カナダ

- 欧州

- アジア太平洋

- 中国

- 日本

- インド

- ラテンアメリカ

- ブラジル

- メキシコ

- 中東・アフリカ

- 北米

- ポーターのファイブフォース分析

第5章 非経口栄養バッグ市場:チャンバータイプ別

- 概要

- シングルチャンバー型非経口栄養バッグ

- デュアルチャンバー型非経口栄養バッグ

- マルチチャンバー型非経口栄養バッグ

第6章 非経口栄養バッグ市場:消費者別

- 概要

- 成人

- 小児

第7章 非経口栄養バッグ市場:エンドユーザー別

- 概要

- ヘルスケア施設

- 薬局・調剤サービスプロバイダー

第8章 非経口栄養バッグ市場:地域別

- 概要

- 北米

- 欧州

- アジア太平洋

- ラテンアメリカ

- 中東・アフリカ

第9章 競合分析

- 概要

- 製品ポートフォリオ分析

- 競合ベンチマーキング

第10章 企業プロファイル

- B. Braun SE

- Baxter International, Inc.

- Fresenius Kabi Ag(A Subsidiary of Fresenius SE & Co. KGaA)

- GVS S.p.A.

- Grifols, S.A.

- Technoflex

- RENOLIT SE

- Valmed s.r.l.

- HEMEDIS GmbH

- INFRA Srl

- Beijing L&Z Medical Technology Development Co., Ltd.

- Boen Healthcare Co., Ltd

- AdvaCare Pharma

- Diffuplast S.r.l.

第11章 付録

- Table 1 Healthcare Expenditure as a Percentage of GDP, by Country, 2020 Vs. 2021 (%)

- Table 2 Number of Physicians Per 1,000 Population, by Country, 2020

- Table 3 Infant Mortality Rates (Deaths Per 1,000 Live Births), by Country, 2010 Vs. 2019 Vs. 2021

- Table 4 Global Prevalence of Undernourishment (% of Population), by Country, 2021

- Table 5 Canada: Medical Device Approval Procedures, by Class

- Table 6 China: Medical Device Approval Procedures, by Class

- Table 7 Rest of APAC: Authorities Regulating Medical Devices, by Country

- Table 8 Brazil: Medical Device Approval Procedures, by Class

- Table 9 Rest of Latin America: Medical Device Regulatory Systems

- Table 10 South Africa: Medical Device Approval Procedures, by Class

- Table 11 Global Parenteral Nutrition Bags Market, by Chamber Type, 2022-2031 (USD Million)

- Table 12 Global Single-Chamber Parenteral Nutrition Bags Market, by Region, 2022-2031 (USD Million)

- Table 13 Global Dual-Chamber Parenteral Nutrition Bags Market, by Region, 2022-2031 (USD Million)

- Table 14 Global Multi-Chambered Parenteral Nutrition Bags Market, by Region, 2022-2031 (USD Million)

- Table 15 Global Parenteral Nutrition Bags Market, by Consumer, 2022-2031 (USD Million)

- Table 16 Global Parenteral Nutrition Bags Market for Adults, by Region, 2022-2031(USD Million)

- Table 17 Global Parenteral Nutrition Bags Market for Children, by Region, 2022-2031 (USD Million)

- Table 18 Global Parenteral Nutrition Bags Market, by End User, 2022-2031 (USD Million)

- Table 19 Global Parenteral Nutrition Bags Market for Healthcare Facilities, by Region, 2022-2031 (USD Million)

- Table 20 Global Parenteral Nutrition Bags Market for Pharmacies & Compounding Service Providers, by Region, 2022-2031 (USD Million)

- Table 21 Global Parenteral Nutrition Bags Market, by Region, 2022-2031 (USD Million)

- Table 22 North America: Parenteral Nutrition Bags Market, by Chamber Type, 2022-2031 (USD Million)

- Table 23 North America: Parenteral Nutrition Bags Market, by Consumer, 2022-2031(USD Million)

- Table 24 North America: Parenteral Nutrition Bags Market, by End User, 2022-2031 (USD Million)

- Table 25 Europe: Parenteral Nutrition Bags Market, by Chamber Type, 2022-2031 (USD Million)

- Table 26 Europe: Parenteral Nutrition Bags Market, by Consumer, 2022-2031 (USD Million)

- Table 27 Europe: Parenteral Nutrition Bags Market, by End User, 2022-2031 (USD Million)

- Table 28 Asia-Pacific: Parenteral Nutrition Bags Market, by Chamber Type, 2022-2031 (USD Million)

- Table 29 Asia-Pacific: Parenteral Nutrition Bags Market, by Consumer, 2022-2031 (USD Million)

- Table 30 Asia-Pacific: Parenteral Nutrition Bags Market, by End User, 2022-2031 (USD Million)

- Table 31 Latin America: Parenteral Nutrition Bags Market, by Chamber Type, 2022-2031 (USD Million)

- Table 32 Latin America: Parenteral Nutrition Bags Market, by Consumer, 2022-2031 (USD Million)

- Table 33 Latin America: Parenteral Nutrition Bags Market, by End User, 2022-2031 (USD Million)

- Table 34 Middle East & Africa: Parenteral Nutrition Bags Market, by Chamber Type, 2022-2031 (USD Million)

- Table 35 Middle East & Africa: Parenteral Nutrition Bags Market, by Consumer, 2022-2031 (USD Million)

- Table 36 Middle East & Africa: Parenteral Nutrition Bags Market, by End User, 2022-2031 (USD Million)

- Table 37 Product Portfolio Analysis

LIST OF FIGURES

- Figure 1 Research Process

- Figure 2 Secondary Sources Referenced for this Study

- Figure 3 Primary Research Techniques

- Figure 4 Key Executives Interviewed

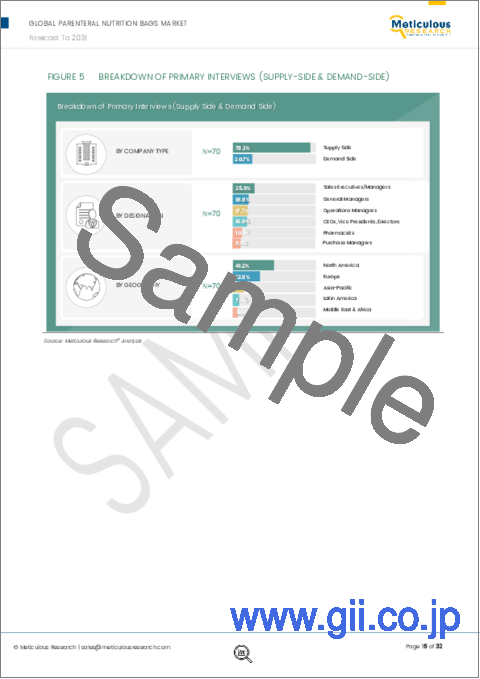

- Figure 5 Breakdown of Primary Interviews (Supply-Side & Demand-Side)

- Figure 6 Market Sizing and Growth Forecast Approach

- Figure 7 Global Parenteral Nutrition Bags Market, by Chamber Type, 2024 Vs. 2031 (USD Million)

- Figure 8 Global Parenteral Nutrition Bags Market, by Consumer, 2024 Vs. 2031 (USD Million)

- Figure 9 Global Parenteral Nutrition Bags Market, by End User, 2024 Vs. 2031 (USD Million)

- Figure 10 Parenteral Nutrition Bags Market, by Geography

- Figure 11 Impact Analysis of Market Dynamics

- Figure 12 Percentage of Population Aged 65 Years or Over, by Region, 2022 Vs. 2030 (%)

- Figure 13 Global Estimated Number of New Cancer Cases, 2020-2040 (In Million)

- Figure 14 U.S. FDA Regulatory Pathways

- Figure 15 India: Medical Device Regulatory Pathway

- Figure 16 Porter's Five Forces Analysis

- Figure 17 Global Parenteral Nutrition Bags Market, by Chamber Type, 2024 Vs. 2031 (USD Million)

- Figure 18 Global Parenteral Nutrition Bags Market, by Consumer, 2024 Vs. 2031 (USD Million)

- Figure 19 Global Parenteral Nutrition Bags Market, by End User, 2024 Vs. 2031 (USD Million)

- Figure 20 Global Parenteral Nutrition Bags Market, by Region, 2024 Vs. 2031 (USD Million)

- Figure 21 North America: Parenteral Nutrition Bags Market Snapshot

- Figure 22 Europe: Parenteral Nutrition Bags Market Snapshot

- Figure 23 Asia-Pacific: Parenteral Nutrition Bags Market Snapshot

- Figure 24 Latin America: Parenteral Nutrition Bags Market Snapshot

- Figure 25 Middle East & Africa: Parenteral Nutrition Bags Market Snapshot

- Figure 26 Parenteral Nutrition Bags Market: Competitive Benchmarking (Based on Chamber Type)

- Figure 27 Parenteral Nutrition Bags Market: Competitive Benchmarking (Based on Geography)

- Figure 28 B. Braun SE: Financial Overview (2022)

- Figure 29 Baxter International, Inc.: Financial Overview (2023)

- Figure 30 Fresenius Se & Co. KGaA: Financial Overview (2022)

- Figure 31 GVS S.p.A.: Financial Overview (2022)

- Figure 32 Grifols, S.A.: Financial Overview (2022)

- Figure 33 RENOLIT SE: Financial Overview (2022)

The global parenteral nutrition bags market is projected to reach $1.25 billion by 2031, at a CAGR of 6.6% from 2024 to 2031.

Following a comprehensive primary and secondary study and an in-depth analysis of the market scenario, this report provides the key drivers, restraints, challenges, and opportunities of the industry. This market is driven by the rising global prevalence of malnutrition, the large number of premature births, and the increasing incidence of metabolic disorders.

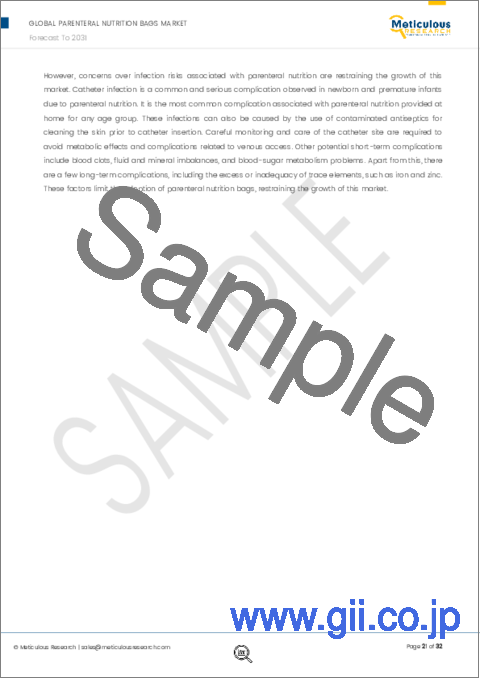

Furthermore, the growing adoption of home healthcare, the rising global geriatric population, and emerging economies provide significant growth opportunities for this market. However, concerns over the infection risks associated with parenteral nutrition restrain the growth of this market. The lack of awareness regarding parenteral nutrition in developing countries is a major challenge impacting the growth of the parenteral nutrition bags market.

Among chamber types, in 2024, the single-chamber parenteral nutrition bags segment is expected to account for the largest share of the parenteral nutrition bags market. Single-chamber parenteral nutrition bags are designed to compound and store a comprehensive blend of nutritional solutions, including electrolytes, amino acids, lipids, vitamins, carbohydrates, and trace elements within a single compartment for parenteral administration. The large share of the segment is attributed to the wide availability of single-chamber empty bags, high rate of prescription for single-chamber nutrition bags, decreased risk of infection, less prescription & administration errors, and cost-effectiveness as compared to dual or multi-chambered bags.

Among consumers, in 2024, the adults segment is expected to account for the largest share of the parenteral nutrition bags market. The rising number of surgeries, rising hospitalization rates, the growth of the geriatric population, and the increasing prevalence of gastrointestinal disorders among adults are factors supporting the largest share of the market. For instance, in 2020, the Rome Foundation of Global Epidemiology Study revealed that 40% of people worldwide suffer from diseases of the gut-brain interaction (DGBIs), such as irritable bowel syndrome, functional dyspepsia, and functional abdominal pain syndrome, among others. Most of these patients would require parenteral nutrition bags for the intake of the required nutrition.

Among end users, in 2024, the healthcare facilities segment is expected to account for the largest share of the parenteral nutrition bags market. The large market share of this segment is attributed to factors such as a large number of patients visiting hospitals and clinics for disease diagnosis and treatment, growing disease burden, an associated rise in the rates of prescription for parenteral nutrition, and the presence of advanced compounding equipment in the hospital associated compounding pharmacies.

An in-depth analysis of the geographical scenario of the global parenteral nutrition bags market provides detailed qualitative and quantitative insights for the five major geographies: North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. In 2024, North America is expected to account for the largest share of the global parenteral nutrition bags market, followed by Europe, Asia-Pacific, Latin America, and the Middle East & Africa. This growth is primarily driven by the growing demand for parenteral nutrition due to the prevalence of chronic & infectious diseases, the rising number of premature births, and the growing adoption of home healthcare settings. For instance, according to the World Health Organization (WHO), in 2020, approximately 13.4 million babies were born preterm (before the completion of 37 weeks of gestation). Preterm babies often require nutrients that need to be provided parenterally since oral nutrition is not possible, therefore increasing the demand for parenteral nutrition and supporting the growth of the market.

The key players operating in the global parenteral nutrition bags market are B. Braun SE (Germany), Baxter International, Inc. (U.S.), Fresenius Kabi AG (Germany), GVS S,p.A. (Italy), Grifols, S.A. (Spain), Technolflex (France), RENOLIT Healthcare (Germany), Valmed s.r.l (Italy), HEMEDIS GmbH (Germany), INFRA Srl (Italy), Beijing L&Z Medical Technology Development Co., Ltd.(China), Boen Healthcare Co., Ltd. (China), AdvaCare Pharma (U.S.), and Diffuplast S.r.l. (Italy).

Scope of the Report:

Parenteral Nutrition Bags Market Assessment-by Chamber Type

- Single-Chamber Parenteral Nutrition Bags

- Dual-Chamber Parenteral Nutrition Bags

- Multi-Chambered Parenteral Nutrition Bags

Parenteral Nutrition Bags Market Assessment-by Consumer

- Adults

- Children

Parenteral Nutrition Bags Market Assessment-by End User

- Healthcare Facilities

- Pharmacies and Compounding Service Providers

Parenteral Nutrition Bags Market-by Geography

- North America

- Europe

- Asia-Pacific (APAC)

- Latin America

- Middle East & Africa

TABLE OF CONTENTS

1. Introduction

- 1.1. Market Definition and Scope

- 1.2. Market Ecosystem

- 1.3. Currency and Limitations

- 1.4. Key Stakeholders

2. Research Methodology

- 2.1. Research Approach

- 2.2. Process of Data Collection and Validation

- 2.2.1. Secondary Research

- 2.2.2. Primary Research/Interviews With Key Opinion Leaders of the Industry

- 2.3. Market Sizing and Forecasting

- 2.3.1. Market Size Estimation Approach

- 2.3.2. Growth Forecast Approach

- 2.4. Assumptions for the Study

3. Executive Summary

4. Market Insights

- 4.1. Overview

- 4.2. Factors Affecting Market Growth

- 4.2.1. Impact Analysis of Market Dynamics

- 4.2.2. Factor Analysis

- 4.3. Key Trends

- 4.3.1. Growing Adoption of Home Healthcare

- 4.3.2. Growing Use of Ethylene Vinyl Acetate (EVA) in Parenteral Applications

- 4.4. Regulatory Analysis

- 4.4.1. North America

- 4.4.1.1. U.S.

- 4.4.1.2. Canada

- 4.4.2. Europe

- 4.4.3. Asia-Pacific

- 4.4.3.1. China

- 4.4.3.2. Japan

- 4.4.3.3. India

- 4.4.4. Latin America

- 4.4.4.1. Brazil

- 4.4.4.2. Mexico

- 4.4.5. Middle East & Africa

- 4.4.1. North America

- 4.5. Porter's Five Forces Analysis

- 4.5.1. Bargaining Power of Suppliers

- 4.5.2. Bargaining Power of Buyers

- 4.5.3. Threat of Substitutes

- 4.5.4. Threat of New Entrants

- 4.5.5. Degree of Competition

5. Parenteral Nutrition Bags Market Assessment- by Chamber Type

- 5.1. Overview

- 5.2. Single-chamber Parenteral Nutrition Bags

- 5.3. Dual-chamber Parenteral Nutrition Bags

- 5.4. Multi-chambered Parenteral Nutrition Bags

6. Parenteral Nutrition Bags Market Assessment-by Consumer

- 6.1. Overview

- 6.2. Adults

- 6.3. Children

7. Parenteral Nutrition Bags Market Assessment-by End User

- 7.1. Overview

- 7.2. Healthcare Facilities

- 7.3. Pharmacies & Compounding Service Providers

8. Parenteral Nutrition Bags Market Assessment-by Geography

- 8.1. Overview

- 8.2. North America

- 8.3. Europe

- 8.4. Asia-Pacific

- 8.5. Latin America

- 8.6. Middle East & Africa

9. Competition Analysis

- 9.1. Overview

- 9.2. Product Portfolio Analysis

- 9.3. Competitive Benchmarking

10. Company Profiles

- 10.1. B. Braun SE

- 10.2. Baxter International, Inc.

- 10.3. Fresenius Kabi Ag (A Subsidiary of Fresenius SE & Co. KGaA)

- 10.4. GVS S.p.A.

- 10.5. Grifols, S.A.

- 10.6. Technoflex

- 10.7. RENOLIT SE

- 10.8. Valmed s.r.l.

- 10.9. HEMEDIS GmbH

- 10.10. INFRA Srl

- 10.11. Beijing L&Z Medical Technology Development Co., Ltd.

- 10.12. Boen Healthcare Co., Ltd

- 10.13. AdvaCare Pharma

- 10.14. Diffuplast S.r.l.

11. Appendix

- 11.1. Available Customization

- 11.2. Related Reports