|

|

市場調査レポート

商品コード

1355381

カメラモジュールの世界市場:モジュールタイプ別、製造プロセス別、コンポーネント別、フォーカスタイプ別、インターフェース別、画素別、用途別、地域別-2028年までの予測Camera Modules Market by Component (Image Sensor, Lens Module, Voice Coil Motor, Filters), Interface (Serial, Parallel), Pixel (>7 MP,8-13 MP, <13 MP), Focus (Autofocus, Fixed), Interface (Serial, Parallel), Process and Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| カメラモジュールの世界市場:モジュールタイプ別、製造プロセス別、コンポーネント別、フォーカスタイプ別、インターフェース別、画素別、用途別、地域別-2028年までの予測 |

|

出版日: 2023年09月19日

発行: MarketsandMarkets

ページ情報: 英文 207 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界のカメラモジュールの市場規模は、2023年に433億米ドルとなり、2028年には685億米ドルに達すると予測され、予測期間中のCAGRは9.6%と見込まれています。

カメラ内蔵のスマートフォンやその他の家電製品に対する需要の増加、高解像度のカメラモジュールを必要とする拡張現実(AR)や仮想現実(VR)の人気の高まり、運転支援システムや駐車支援システムなどの車載におけるカメラの使用の増加、3Dカメラやサーマルカメラなどの新しいカメラ技術の開発がカメラモジュールの新しい用途を開拓していることが、カメラモジュール市場の成長の主な促進要因となっています。

8~13MPセグメントは、カメラモジュール市場で最大の市場シェアを占めると予想されます。8~13MPセグメントは、家電、自動車、産業、セキュリティ・監視など、あらゆる分野での技術進歩により、カメラモジュール市場で最大のシェアを占めています。また、スマートフォンの背面に複数のカメラを搭載する傾向が強まっていることも成長の要因となっています。現在、スマートフォンの背面にはデュアルカメラ、トリプルカメラ、クアドラプル・カメラが搭載されています。

スマートフォンのカメラは年々改良されています。競合他社の製品との差別化を図り、高画質画像への需要に応えるため、スマートフォンOEMメーカーは、エンドユーザーの要求を満たすため、より高品質なカメラをスマートフォンに搭載する革新的なコンポーネントの探求を続けています。いくつかのタイプは、単体のデジタルカメラで撮影された写真に匹敵するシャープで高品質な写真を生成することさえできます。複数レンズ構成は、カメラ性能を押し上げた理由のひとつです。デュアルカメラ、トリプルカメラ、クアッドカメラと呼ばれる2つ、3つ、4つのレンズを搭載したスマートフォンが一般的になりつつあります。さらに、スマートフォンの機能性と品質を向上させるため、また、フロントカメラの動向の高まりを受け、OEMメーカーは、単一のリアカメラから、デュアル、トリプル、クアッドカメラの設計に移行しつつあり、その結果、スマートフォン1台あたりの平均カメラモジュール数の採用が増加しています。スマートフォンに複数のカメラが搭載されることで、高倍率ズーム、ハイダイナミックレンジ(HDR)イメージング、ポートレートモード、3D、低照度撮影など、さまざまな新機能が可能になっています。

中国は、いくつかの要因により、カメラモジュール市場で最大の市場シェアを占めています。中国は世界の製造拠点としての地位を確立しており、費用対効果の高い生産能力と大規模な製造インフラで知られています。中国は世界最大のスマートフォン市場であり、これがスマートフォンのカメラモジュール需要を牽引しています。中国のカメラモジュールメーカーは、3Dカメラやサーマルカメラなど、新しいカメラ技術を開発するための研究開発に多額の投資を行っています。中国の製造ノウハウと規模の経済は、競争力のある価格設定と大量生産を可能にし、国内外の顧客を引き付けています。

当レポートでは、世界のカメラモジュール市場について調査し、モジュールタイプ別、製造プロセス別、コンポーネント別、フォーカスタイプ別、インターフェース別、画素別、用途別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- バリューチェーン分析

- 生態系マッピング

- 価格分析

- 顧客のビジネスに影響を与える動向/混乱

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- ケーススタディ分析

- 技術分析

- 貿易分析

- 特許分析、2018年~2022年

- 関税と規制

- 基準と規制状況

- 2023年~2024年の主要な会議とイベント

第6章 カメラモジュール市場、モジュールタイプ別

- イントロダクション

- シングルカメラモジュール

- デュアルカメラモジュール

- マルチカメラモジュール

- 3Dカメラモジュール

第7章 カメラモジュール市場、製造プロセス別

- イントロダクション

- フリップチップカメラモジュール

- チップオンボードカメラモジュール

第8章 カメラモジュール市場、コンポーネント別

- イントロダクション

- イメージセンサー

- レンズモジュール

- ボイスコイルモーター

- その他

第9章 カメラモジュール市場、フォーカスタイプ別

- イントロダクション

- オート

- 固定

第10章 カメラモジュール市場、インターフェース別

- イントロダクション

- シリアルインターフェース

- パラレルインターフェイス

第11章 カメラモジュール市場、画素別

- イントロダクション

- 7MP未満

- 8~13MP

- 13MP以上

第12章 カメラモジュール市場、用途別

- イントロダクション

- 家電

- 自動車

- 産業用

- セキュリティと監視

- その他

第13章 カメラモジュール市場、地域別

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- その他の地域

第14章 競合情勢

- 概要

- 主要参入企業が採用した戦略

- 収益分析、2018~2022年

- 市場シェア分析、2022年

- 主要企業評価マトリックス、2022年

- スタートアップ/中小企業(SMES)の評価マトリックス、2022年

- 企業のフットプリント

- 競合ベンチマーキング

- 競争シナリオと動向

第15章 企業プロファイル

- 主要参入企業

- LG INNOTEK

- OFILM

- SUNNY OPTICAL TECHNOLOGY(GROUP)COMPANY LIMITED

- HON HAI PRECISION INDUSTRY CO., LTD.

- SAMSUNG ELECTRO-MECHANICS

- CHICONY ELECTRONICS CO., LTD

- Q TECHNOLOGY(GROUP)COMPANY LIMITED

- AMS-OSRAM AG

- MCNEX CO., LTD

- TRULY INTERNATIONAL HOLDINGS LIMITED

- その他の企業

- CAMMSYS. CORP

- INTEL CORPORATION

- PRIMAX ELECTRONICS LTD.

- SONY CORPORATION

- SHENZHEN CHUANGMU TECHNOLOGY CO., LTD

- JENOPTIK

- LEOPARD IMAGING INC.

- LUXVISIONS-INNO

- HAESUNG OPTICS

- COWELL

- PARTRON

- OMNIVISION

- KYOCERA CORPORATION

- E-CON SYSTEMS

- SYNTEC OPTICS

- NAMUGA

- AAC TECHNOLOGIES

第16章 付録

The global camera modules market was valued at USD 43.3 billion in 2023 and is estimated to reach USD 68.5 billion by 2028, registering a CAGR of 9.6% during the forecast period. The increasing demand for smartphones and other consumer electronics products with built-in cameras, growing popularity of augmented reality (AR) and virtual reality (VR) applications, which require high-resolution camera modules, increasing use of cameras in automotive applications, such as driver assistance systems and parking assistance systems as well as development of new camera technologies, such as 3D cameras and thermal cameras, which are opening up new applications for camera modules. are the major driving factors for the growth of the camera modules market.

"8 - 13 MP segment is expected to account at the largest market size during the forecast period."

The 8 - 13 MP segment is expected to account largest market share in the camera modules market. , the 8 to 13 MP segment held the largest share of the camera modules market owing to the technological advancements in all the application areas such as consumer electronics, automotive, industrial, and security and surveillance. The growth is also attributed to the increasing trend of using multiple cameras on the rear side of smartphones. Nowadays, smartphones are likely to have dual, triple, or quadruple cameras located on the back..

"Smartphones from consumer electronics segment is projected to dominate the camera modules market."Smartphones are highly competitive applications owing to a large number of manufacturers. Every year, improvements are seen in smartphone cameras. To differentiate their products from that of competitors and meet the demand for high-quality images, smartphone OEMs are in the continuous process of exploring innovative components to provide better quality cameras in their phones to fulfill end-user requirements. A few types can even produce sharp, high-quality photographs comparable to those captured by standalone digital cameras. The multiple-lens configuration is one reason that has pushed camera capabilities ahead. Smartphones featuring two, three, or four lenses, referred to as dual, triple, or quad cameras, are becoming more common. Furthermore, to improve the functionality and quality of smartphones and the rising trends of front cameras, OEMs are shifting from single rear cameras to dual, triple, and quad-camera designs, which is resulting in the increasing adoption of an average number of camera modules per smartphone. The inclusion of multiple cameras in a smartphone has enabled an array of new features, including high zoom level, high dynamic range (HDR) imaging, portrait modes, 3D, and low-light photography.

"China is projected to dominate in Asia Pacific region for camera modules market"

China is having the largest market share in the camera modules market due to several factors. China has established itself as a global manufacturing hub, known for its cost-effective production capabilities and large-scale manufacturing infrastructure. China is the largest smartphone market in the world, and this is driving the demand for camera modules in smartphones. Chinese camera module manufacturers are investing heavily in research and development to develop new camera technologies, such as 3D cameras and thermal cameras. This is helping them to stay ahead of the competition and maintain their dominance in the market.China's manufacturing expertise and economies of scale enable competitive pricing and high-volume production, attracting domestic and international customers.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the camera module marketplace.

- By Company Type: Tier 1 - 45%, Tier 2 - 35%, and Tier 3 - 20%

- By Designation: C-level Executives - 35%, Directors - 25%, and Others - 40%

- By Region: North America- 20%, Europe - 25%, Asia Pacific- 45% and RoW- 10%

as LG Innotek, OFILM Group Co., Ltd., Sunny Optical Technology (Group), Hon Hai Precision Inc. Co., Ltd. (Foxconn), Chicony Electronics, Sony, Intel and Samsung Electro-Mechanics and so on are some of the key players in the camera modules market.

The study includes an in-depth competitive analysis of these key players in the camera modules market, with their company profiles, recent developments, and key market strategies.

Research Coverage

This research report categorizes the camera modules market by component, pixel, focus type , interface , application and region, and by region (North America, Europe, Asia Pacific, and RoW). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the camera modules market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; Contracts, partnerships, agreements. new product & service launches, mergers and acquisitions, and recent developments associated with the camera modules market. Competitive analysis of upcoming startups in the camera modules market ecosystem is covered in this report.

Reasons to buy this report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall camera modules market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

This new version of the report on the camera modules market includes the following:

- Market size from 2019 to 2028

- Average selling prices (ASPs) of camera modules calculated by the weighted average method

- Updated research assumptions and limitations

- Information related to trends/disruptions impacting businesses of customers, as well as information on the ecosystem of camera modules, trade analysis, tariff and regulatory analyses, technology analysis, patents analysis, and case studies pertaining to the camera modules market.

- Updated financial information until 2022 (depending on the availability) for each listed company, which helps in the easy analysis of the present status of the profiled companies in terms of their financial strength, profitability, key revenue-generating regions/countries, and the highest revenue-generating business segments.

- Recent developments that help assess market trends and growth strategies adopted by leading market players

- Key manufacturers offering camera modules; top 25 manufacturers of camera modules, which are categorized into star, pervasive, emerging leader, and participant companies based on their performance on various parameters such as product footprint, focus on product innovations, and geographic footprint.

- Market share analysis of various players operating in the camera modules market for 2022

- Small- and medium-sized enterprises (SME) matrix that brief some business strategies and product offerings of 15 SME players operating in the market, which are classified into four groups: progressive, dynamic, responsive companies, and starting blocks

- Brief information regarding the competitive situations and trends in the camera modules market

- The product, application, and geographic footprints of the top 25 manufacturers of camera modules Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the camera modules market

- Market Development: Comprehensive information about lucrative markets - the report analyses the camera modules market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the camera modulesmarket

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like as LG Innotek, OFILM Group Co., Ltd., Sunny Optical Technology (Group), Hon Hai Precision Inc. Co., Ltd. (Foxconn), Chicony Electronics, Sony, Intel and Samsung Electro-Mechanics, among others in the camera modules market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 CAMERA MODULES MARKET: SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

- 1.7 RECESSION IMPACT ANALYSIS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 CAMERA MODULES MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Breakdown of primaries

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Key industry insights

- 2.2 FACTOR ANALYSIS

- FIGURE 3 MARKET SIZE ESTIMATION METHODOLOGY: APPROACH 1-TOP DOWN (SUPPLY SIDE)-REVENUES GENERATED BY COMPANIES FROM SALES OF CAMERA MODULES

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- 2.3.2.1 Approach to estimate market size using top-down analysis (supply side)

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.3.1 BOTTOM-UP APPROACH

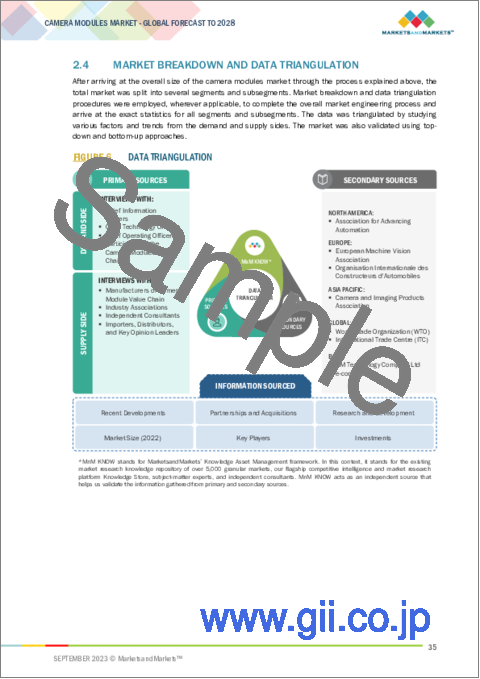

- 2.4 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 6 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 PARAMETERS CONSIDERED TO ANALYZE IMPACT OF RECESSION ON CAMERA MODULES MARKET

3 EXECUTIVE SUMMARY

- FIGURE 7 IMAGE SENSORS SEGMENT TO DOMINATE CAMERA MODULES MARKET IN 2028

- FIGURE 8 FIXED FOCUS CAMERA MODULES HELD LARGER SHARE OF CAMERA MODULES MARKET IN 2022

- FIGURE 9 CONSUMER ELECTRONICS APPLICATION REGISTERED LARGEST MARKET SIZE IN 2028

- FIGURE 10 ASIA PACIFIC ACCOUNTED FOR LARGEST SHARE OF CAMERA MODULES MARKET IN 2022

4 PREMIUM INSIGHTS

- 4.1 MAJOR OPPORTUNITIES FOR PLAYERS IN CAMERA MODULES MARKET

- FIGURE 11 GROWING DEMAND FOR CONSUMER ELECTRONICS AND FOCUS ON AUTOMOTIVE APPLICATIONS TO FUEL MARKET GROWTH FROM 2023 TO 2028

- 4.2 CAMERA MODULES MARKET, BY INTERFACE

- FIGURE 12 SERIAL INTERFACE TYPE CAMERA MODULES TO RECORD HIGHER CAGR DURING FORECAST PERIOD

- 4.3 CAMERA MODULES MARKET, BY PIXEL

- FIGURE 13 8 TO 13 MP SEGMENT TO ACCOUNT FOR LARGEST SHARE OF CAMERA MODULES MARKET IN 2028

- 4.4 CAMERA MODULES MARKET, BY APPLICATION

- FIGURE 14 AUTOMOTIVE APPLICATIONS TO EXHIBIT HIGHEST CAGR IN CAMERA MODULES MARKET DURING FORECAST PERIOD

- 4.5 CAMERA MODULES MARKET, BY REGION

- FIGURE 15 INDIA TO REGISTER HIGHEST CAGR IN CAMERA MODULES MARKET DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 16 CAMERA MODULES MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing demand for consumer electronics

- 5.2.1.2 Growing deployment of surveillance cameras to ensure public safety and security

- TABLE 1 TOTAL NUMBER OF CCTV CAMERAS INSTALLED IN TOP COUNTRIES (MILLION UNITS)

- 5.2.1.3 Rising focus on integrating ADAS and AI-powered systems to enhance vehicle and passenger safety

- FIGURE 17 COMPARISON OF YEARLY PRODUCTION OF PASSENGER CARS, 2017-2022 (MILLION UNITS)

- 5.2.1.4 Rapid advancements in camera technology

- FIGURE 18 CAMERA MODULES MARKET DRIVERS AND THEIR IMPACT

- 5.2.2 RESTRAINTS

- 5.2.2.1 Design complexities due to miniaturization of devices

- FIGURE 19 CAMERA MODULES MARKET RESTRAINTS AND THEIR IMPACT

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing use of image sensors in electronic devices

- 5.2.3.2 Emerging applications of AR and VR devices

- 5.2.3.3 Growing demand for industrial automation technologies and systems

- FIGURE 20 CAMERA MODULES MARKET OPPORTUNITIES AND THEIR IMPACT

- 5.2.4 CHALLENGES

- 5.2.4.1 Complexities associated with manufacturing processes and supply chain

- FIGURE 21 CAMERA MODULES MARKET CHALLENGES AND THEIR IMPACT

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 22 CAMERA MODULES MARKET: VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM MAPPING

- FIGURE 23 ECOSYSTEM ANALYSIS

- TABLE 2 ROLE OF PARTICIPANTS IN ECOSYSTEM

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF CAMERA MODULES OFFERED BY KEY PLAYERS

- FIGURE 24 AVERAGE SELLING PRICE OF CAMERA MODULES OFFERED BY KEY PLAYERS

- TABLE 3 AVERAGE SELLING PRICE OF CAMERA MODULES OFFERED BY KEY PLAYERS (USD)

- 5.5.2 AVERAGE SELLING PRICE TRENDS

- TABLE 4 INDICATIVE SELLING PRICE OF CAMERA MODULES, BY REGION

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 25 REVENUE SHIFTS AND NEW REVENUE POCKETS IN CAMERA MODULES MARKET

- 5.7 PORTER'S FIVE FORCES ANALYSIS

- TABLE 5 CAMERA MODULES MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 26 CAMERA MODULES MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.7.1 THREAT OF NEW ENTRANTS

- 5.7.2 THREAT OF SUBSTITUTES

- 5.7.3 BARGAINING POWER OF SUPPLIERS

- 5.7.4 BARGAINING POWER OF BUYERS

- 5.7.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.8 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.8.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS

- TABLE 6 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE APPLICATIONS (%)

- 5.8.2 BUYING CRITERIA

- FIGURE 28 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- TABLE 7 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- 5.9 CASE STUDY ANALYSIS

- TABLE 8 E-CON SYSTEMS CAMERA MODULES MET SECURITY & SURVEILLANCE APPLICATION REQUIREMENTS FOR OEM

- TABLE 9 E-CON SYSTEMS PROVIDED CAMERA SYSTEM FOR IMPROVED AUDIO AND VIDEO EXPERIENCES OUTSIDE CLASSROOMS OF EDUCATIONAL CENTERS

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 KEY TECHNOLOGIES

- 5.10.1.1 CMOS technology

- 5.10.1.2 CCD technology

- 5.10.1.3 ToF technology

- 5.10.1.4 OIS technology

- 5.10.1.5 IR technology

- 5.10.2 ADJACENT TECHNOLOGIES

- 5.10.2.1 Quantum dot technology

- 5.10.1 KEY TECHNOLOGIES

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT SCENARIO

- FIGURE 29 IMPORT DATA, BY COUNTRY, 2018-2022 (USD MILLION)

- 5.11.2 EXPORT SCENARIO

- FIGURE 30 EXPORT DATA, BY COUNTRY, 2018-2022 (USD MILLION)

- 5.12 PATENT ANALYSIS, 2018-2022

- TABLE 10 PATENTS RELATED TO CAMERA MODULES

- FIGURE 31 NUMBER OF PATENTS GRANTED WORLDWIDE, 2012-2022

- TABLE 11 TOP 20 PATENT OWNERS IN US, 2012-2022

- FIGURE 32 TOP 10 COMPANIES WITH HIGHEST NUMBER OF PATENT APPLICATIONS, 2012-2022

- 5.13 TARIFFS AND REGULATIONS

- 5.13.1 TARIFFS

- 5.13.2 REGULATORY COMPLIANCE

- 5.13.2.1 Regulations

- 5.14 STANDARDS AND REGULATORY LANDSCAPE

- 5.14.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14.2 STANDARDS

- 5.14.2.1 Common safety standards related to camera modules market

- 5.15 KEY CONFERENCES AND EVENTS, 2023-2024

- TABLE 16 CAMERA MODULES MARKET: LIST OF CONFERENCES AND EVENTS

6 CAMERA MODULES MARKET, BY MODULE TYPE

- 6.1 INTRODUCTION

- FIGURE 33 CAMERA MODULES MARKET, BY MODULE TYPE

- 6.2 SINGLE CAMERA MODULES

- 6.3 DUAL CAMERA MODULES

- 6.4 MULTI-CAMERA MODULES

- 6.5 3D CAMERA MODULES

7 CAMERA MODULES MARKET, BY MANUFACTURING PROCESS

- 7.1 INTRODUCTION

- FIGURE 34 CAMERA MODULES MARKET, BY PROCESS

- 7.2 FLIP-CHIP CAMERA MODULES

- 7.2.1 GROWING DEMAND FOR COMPACT AND SLIM DEVICES WITH MULTIPLE CAMERA CONFIGURATIONS TO FUEL SEGMENTAL GROWTH

- 7.3 CHIP-ON-BOARD CAMERA MODULES

- 7.3.1 INCREASING USE IN AUTOMATION AND PRODUCT STANDARDIZATION TO CONTRIBUTE TO MARKET GROWTH

8 CAMERA MODULES MARKET, BY COMPONENT

- 8.1 INTRODUCTION

- FIGURE 35 CAMERA MODULES MARKET, BY COMPONENT

- FIGURE 36 IMAGE SENSORS SEGMENT TO EXHIBIT HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 17 CAMERA MODULES MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 18 CAMERA MODULES MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- 8.2 IMAGE SENSORS

- 8.2.1 INCREASING DEPLOYMENT IN DIGITAL CAMERAS AND SMARTPHONES FOR HIGH-QUALITY IMAGES TO CONTRIBUTE TO SEGMENTAL GROWTH

- FIGURE 37 CONSUMER ELECTRONICS APPLICATIONS TO HOLD LARGEST SHARE OF CAMERA MODULES MARKET FOR IMAGE SENSORS IN 2028

- TABLE 19 IMAGE SENSORS: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 20 IMAGE SENSORS: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.2.2 CMOS IMAGE SENSORS

- 8.2.2.1 Frontside illumination technology

- 8.2.2.2 Backside illumination technology

- 8.2.3 CCD IMAGE SENSORS

- 8.2.4 OTHER IMAGE SENSORS

- 8.2.4.1 NMOS image sensors

- 8.2.4.2 InGaAs image sensors

- 8.2.4.3 Flat-panel X-ray sensors

- 8.2.4.4 sCMOS image sensors

- 8.3 LENS MODULES

- 8.3.1 UTILIZATION FOR SAFETY AND NAVIGATION AND IN SLIM AND PORTABLE PRODUCTS TO DRIVE SEGMENT

- TABLE 21 LENS MODULES: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 22 LENS MODULES: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.4 VOICE COIL MOTORS

- 8.4.1 REQUIREMENT OF ADVANCED CAMERA FUNCTIONALITIES WITH ENHANCED IMAGE OUTPUT FROM VARIOUS APPLICATIONS TO PROPEL DEMAND

- TABLE 23 VOICE COIL MOTORS: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 24 VOICE COIL MOTORS: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 8.5 OTHER COMPONENTS

- TABLE 25 OTHER COMPONENTS: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 26 OTHER COMPONENTS: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

9 CAMERA MODULES MARKET, BY FOCUS TYPE

- 9.1 INTRODUCTION

- FIGURE 38 CAMERA MODULES MARKET, BY FOCUS TYPE

- FIGURE 39 AUTOFOCUS SEGMENT TO EXHIBIT HIGHER CAGR FROM 2023 TO 2028

- TABLE 27 CAMERA MODULES MARKET, BY FOCUS TYPE, 2019-2022 (USD MILLION)

- TABLE 28 CAMERA MODULES MARKET, BY FOCUS TYPE, 2023-2028 (USD MILLION)

- 9.2 AUTOFOCUS

- 9.2.1 WIDE DEPLOYMENT IN MODERN CAMERAS TO GENERATE SHARP IMAGES IRRESPECTIVE OF DISTANCE OF OBJECTS TO DRIVE SEGMENTAL GROWTH

- TABLE 29 AUTOFOCUS: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 30 AUTOFOCUS: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 9.3 FIXED FOCUS

- 9.3.1 UTILIZATION IN CAMERAS REQUIRING INEXPENSIVE AND EASY-TO-USE FEATURES TO PROPEL MARKET

- TABLE 31 FIXED FOCUS: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 32 FIXED FOCUS: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

10 CAMERA MODULES MARKET, BY INTERFACE

- 10.1 INTRODUCTION

- FIGURE 40 CAMERA MODULES MARKET, BY INTERFACE

- FIGURE 41 SERIAL INTERFACE SEGMENT TO WITNESS HIGHER CAGR DURING FORECAST PERIOD

- TABLE 33 CAMERA MODULES MARKET, BY INTERFACE, 2019-2022 (USD MILLION)

- TABLE 34 CAMERA MODULES MARKET, BY INTERFACE, 2023-2028 (USD MILLION)

- 10.2 SERIAL INTERFACE

- 10.2.1 GROWING UTILIZATION FOR HIGH-SPEED DATA TRANSFER AND IMPROVED IMAGE QUALITY IN MODERN IMAGING AND VISION SYSTEMS TO PROPEL SEGMENT

- 10.3 PARALLEL INTERFACE

- 10.3.1 ADVANTAGES IN TERMS OF COMPACTNESS, SCALABILITY, AND POWER EFFICIENCY TO BOOST DEMAND

11 CAMERA MODULES MARKET, BY PIXEL

- 11.1 INTRODUCTION

- FIGURE 42 CAMERA MODULES MARKET, BY PIXEL

- FIGURE 43 ABOVE 13 MP SEGMENT TO RECORD HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 35 CAMERA MODULES MARKET, BY PIXEL, 2019-2022 (USD MILLION)

- TABLE 36 CAMERA MODULES MARKET, BY PIXEL, 2023-2028 (USD MILLION)

- 11.2 UP TO 7 MP

- 11.2.1 GREATER DEPLOYMENT IN AUTOMOBILES TO SUPPORT SEGMENTAL GROWTH

- TABLE 37 UP TO 7 MP: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 38 UP TO 7 MP: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.3 8 TO 13 MP

- 11.3.1 FREQUENT USE IN SMARTPHONES WITH DUAL OR TRIPLE CAMERA SETTINGS TO DRIVE MARKET

- TABLE 39 8 TO 13 MP: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 40 8 TO 13 MP: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.4 ABOVE 13 MP

- 11.4.1 RISING FOCUS ON HIGH-RESOLUTION SMARTPHONE CAMERAS AND HIGH-PERFORMANCE CAMERA MODULES FOR VARIOUS APPLICATIONS TO PROPEL SEGMENTAL GROWTH

- TABLE 41 ABOVE 13 MP: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 42 ABOVE 13 MP: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

12 CAMERA MODULES MARKET, BY APPLICATION

- 12.1 INTRODUCTION

- FIGURE 44 CAMERA MODULES MARKET, BY APPLICATION

- FIGURE 45 CONSUMER ELECTRONICS APPLICATIONS TO LEAD CAMERA MODULES MARKET IN 2028

- TABLE 43 CAMERA MODULES MARKET SHIPMENT, BY APPLICATION, 2019-2022 (MILLION UNITS)

- TABLE 44 CAMERA MODULES MARKET SHIPMENT, BY APPLICATION, 2023-2028 (MILLION UNITS)

- TABLE 45 CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 46 CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 12.2 CONSUMER ELECTRONICS

- 12.2.1 DEPLOYMENT OF MULTIPLE CAMERAS AND BETTER-QUALITY CAMERA MODULES IN SMARTPHONES TO ENHANCE CONSUMER EXPERIENCE TO DRIVE MARKET

- TABLE 47 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY SUBTYPE, 2019-2022 (USD MILLION)

- TABLE 48 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY SUBTYPE, 2023-2028 (USD MILLION)

- 12.2.2 SMARTPHONES

- 12.2.3 TABLET PCS

- 12.2.4 CAMERAS

- 12.2.5 WEARABLES

- 12.2.6 OTHER CONSUMER ELECTRONICS

- TABLE 49 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 50 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 51 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY FOCUS TYPE, 2019-2022 (USD MILLION)

- TABLE 52 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY FOCUS TYPE, 2023-2028 (USD MILLION)

- TABLE 53 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY PIXEL, 2019-2022 (USD MILLION)

- TABLE 54 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY PIXEL, 2023-2028 (USD MILLION)

- FIGURE 46 ASIA PACIFIC TO DOMINATE CAMERA MODULES MARKET FOR CONSUMER ELECTRONICS IN 2028

- TABLE 55 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 56 CONSUMER ELECTRONICS: CAMERA MODULES MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.3 AUTOMOTIVE

- 12.3.1 INCREASING DEMAND FOR SAFETY FEATURES IN VEHICLES AND GOVERNMENT MANDATES TO PUSH MARKET GROWTH

- TABLE 57 AUTOMOTIVE: CAMERA MODULES MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 58 AUTOMOTIVE: CAMERA MODULES MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 59 AUTOMOTIVE: CAMERA MODULES MARKET, BY FOCUS TYPE, 2019-2022 (USD MILLION)

- TABLE 60 AUTOMOTIVE: CAMERA MODULES MARKET, BY FOCUS TYPE, 2023-2028 (USD MILLION)

- TABLE 61 AUTOMOTIVE: CAMERA MODULES MARKET, BY PIXEL, 2019-2022 (USD MILLION)

- TABLE 62 AUTOMOTIVE: CAMERA MODULES MARKET, BY PIXEL, 2023-2028 (USD MILLION)

- FIGURE 47 AUTOMOTIVE MARKET IN EUROPE TO LEAD CAMERA MODULES MARKET IN 2028

- TABLE 63 AUTOMOTIVE: CAMERA MODULES MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 64 AUTOMOTIVE: CAMERA MODULES MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.3.2 BY FUNCTION

- 12.3.2.1 ADAS

- 12.3.2.2 Viewing & Others

- TABLE 65 AUTOMOTIVE: CAMERA MODULES MARKET, BY FUNCTION, 2019-2022 (USD MILLION)

- TABLE 66 AUTOMOTIVE: CAMERA MODULES MARKET, BY FUNCTION, 2023-2028 (USD MILLION)

- 12.3.3 BY VIEW TYPE

- 12.3.3.1 Rear view

- 12.3.3.2 Front view and others

- TABLE 67 AUTOMOTIVE: CAMERA MODULES MARKET, BY VIEW TYPE, 2019-2022 (USD MILLION)

- TABLE 68 AUTOMOTIVE: CAMERA MODULES MARKET, BY VIEW TYPE, 2023-2028 (USD MILLION)

- 12.3.4 BY VEHICLE TYPE

- 12.3.4.1 Passenger

- 12.3.4.2 Commercial

- TABLE 69 AUTOMOTIVE: CAMERA MODULES MARKET, BY VEHICLE TYPE, 2019-2022 (USD MILLION)

- TABLE 70 AUTOMOTIVE: CAMERA MODULES MARKET, BY VEHICLE TYPE, 2023-2028 (USD MILLION)

- 12.4 INDUSTRIAL

- 12.4.1 USEFULNESS IN PRODUCTION MONITORING, MEASUREMENT TASKS, AND QUALITY CONTROL TO FUEL SEGMENTAL GROWTH

- 12.4.2 MACHINE VISION

- 12.4.3 ROBOTIC VISION

- TABLE 71 INDUSTRIAL: CAMERA MODULES MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 72 INDUSTRIAL: CAMERA MODULES MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 73 INDUSTRIAL: CAMERA MODULES MARKET, BY FOCUS TYPE, 2019-2022 (USD MILLION)

- TABLE 74 INDUSTRIAL: CAMERA MODULES MARKET, BY FOCUS TYPE, 2023-2028 (USD MILLION)

- TABLE 75 INDUSTRIAL: CAMERA MODULES MARKET, BY PIXEL, 2019-2022 (USD MILLION)

- TABLE 76 INDUSTRIAL: CAMERA MODULES MARKET, BY PIXEL, 2023-2028 (USD MILLION)

- TABLE 77 INDUSTRIAL: CAMERA MODULES MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 78 INDUSTRIAL: CAMERA MODULES MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.5 SECURITY & SURVEILLANCE

- 12.5.1 AVAILABILITY OF SPECIALIZED SURVEILLANCE CAMERAS WITH AI-BASED OBJECT DETECTION AND HIGH-RESOLUTION SENSORS TO CONTRIBUTE TO RISING DEMAND

- 12.5.2 PUBLIC PLACES AND INFRASTRUCTURES

- 12.5.3 COMMERCIAL & RESIDENTIAL

- TABLE 79 SECURITY & SURVEILLANCE: CAMERA MODULES MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 80 SECURITY & SURVEILLANCE: CAMERA MODULES MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 81 SECURITY & SURVEILLANCE: CAMERA MODULES MARKET, BY FOCUS TYPE, 2019-2022 (USD MILLION)

- TABLE 82 SECURITY & SURVEILLANCE: CAMERA MODULES MARKET, BY FOCUS TYPE, 2023-2028 (USD MILLION)

- TABLE 83 SECURITY & SURVEILLANCE: CAMERA MODULES MARKET, BY PIXEL, 2019-2022 (USD MILLION)

- TABLE 84 SECURITY & SURVEILLANCE: CAMERA MODULES MARKET, BY PIXEL, 2023-2028 (USD MILLION)

- TABLE 85 SECURITY & SURVEILLANCE: CAMERA MODULES MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 86 SECURITY & SURVEILLANCE: CAMERA MODULES MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.6 OTHER APPLICATIONS

- 12.6.1 HEALTHCARE

- 12.6.1.1 Endoscopy

- 12.6.1.2 Ophthalmology

- 12.6.1.3 Other healthcare applications

- 12.6.2 AEROSPACE & DEFENSE

- 12.6.2.1 Aerial and marine surveillance

- 12.6.2.2 Border surveillance & military operations

- TABLE 87 OTHER APPLICATIONS: CAMERA MODULES MARKET, BY COMPONENT, 2019-2022 (USD MILLION)

- TABLE 88 OTHER APPLICATIONS: CAMERA MODULES MARKET, BY COMPONENT, 2023-2028 (USD MILLION)

- TABLE 89 OTHER APPLICATIONS: CAMERA MODULES MARKET, BY FOCUS TYPE, 2019-2022 (USD MILLION)

- TABLE 90 OTHER APPLICATIONS: CAMERA MODULES MARKET, BY FOCUS TYPE, 2023-2028 (USD MILLION)

- TABLE 91 OTHER APPLICATIONS: CAMERA MODULES MARKET, BY PIXEL, 2019-2022 (USD MILLION)

- TABLE 92 OTHER APPLICATIONS: CAMERA MODULES MARKET, BY PIXEL, 2023-2028 (USD MILLION)

- TABLE 93 OTHER APPLICATIONS: CAMERA MODULES MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 94 OTHER APPLICATIONS: CAMERA MODULES MARKET, BY REGION, 2023-2028 (USD MILLION)

- 12.6.1 HEALTHCARE

13 CAMERA MODULES MARKET, BY REGION

- 13.1 INTRODUCTION

- FIGURE 48 CAMERA MODULES MARKET, BY REGION

- TABLE 95 CAMERA MODULES MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 96 CAMERA MODULES MARKET, BY REGION, 2023-2028 (USD MILLION)

- 13.2 NORTH AMERICA

- 13.2.1 IMPACT OF RECESSION ON CAMERA MODULES MARKET IN NORTH AMERICA

- FIGURE 49 NORTH AMERICA: CAMERA MODULES MARKET SNAPSHOT

- TABLE 97 NORTH AMERICA: CAMERA MODULES MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 98 NORTH AMERICA: CAMERA MODULES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 99 NORTH AMERICA: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 100 NORTH AMERICA: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 13.2.2 US

- 13.2.2.1 Rising focus on automobile safety and technologically advanced consumer electronics to create market growth opportunities

- 13.2.3 CANADA

- 13.2.3.1 Government mandates to increase safety of vehicles to drive market

- 13.2.4 MEXICO

- 13.2.4.1 Increasing foreign direct investments to provide growth opportunities

- 13.3 EUROPE

- FIGURE 50 EUROPE: CAMERA MODULES MARKET SNAPSHOT

- TABLE 101 EUROPE: CAMERA MODULES MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 102 EUROPE: CAMERA MODULES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 103 EUROPE: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 104 EUROPE: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 13.3.1 IMPACT OF RECESSION ON CAMERA MODULES MARKET IN EUROPE

- 13.3.2 GERMANY

- 13.3.2.1 Focus on premium automotive manufacturing to provide opportunities for market growth

- 13.3.3 FRANCE

- 13.3.3.1 Increasing demand and popularity of autonomous vehicles to support market expansion

- 13.3.4 UK

- 13.3.4.1 Presence of premium vehicle companies to fuel market growth

- 13.3.5 ITALY

- 13.3.5.1 Growing adoption of digital technologies to drive market

- 13.3.6 REST OF EUROPE

- 13.4 ASIA PACIFIC

- FIGURE 51 ASIA PACIFIC: CAMERA MODULES MARKET SNAPSHOT

- TABLE 105 ASIA PACIFIC: CAMERA MODULES MARKET, BY COUNTRY, 2019-2022 (USD MILLION)

- TABLE 106 ASIA PACIFIC: CAMERA MODULES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 107 ASIA PACIFIC: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 108 ASIA PACIFIC: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 13.4.1 IMPACT OF RECESSION ON CAMERA MODULES MARKET IN ASIA PACIFIC

- 13.4.2 CHINA

- 13.4.2.1 Elevated demand for automotive and consumer electronics products to boost market

- 13.4.3 JAPAN

- 13.4.3.1 Market dominance in automobiles, robotics, & biotechnology to propel adoption of camera modules

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Presence of leading smartphone and automotive players to drive demand for camera modules

- 13.4.5 REST OF ASIA PACIFIC

- 13.5 ROW

- TABLE 109 ROW: CAMERA MODULES MARKET, BY REGION, 2019-2022 (USD MILLION)

- TABLE 110 ROW: CAMERA MODULES MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 111 ROW: CAMERA MODULES MARKET, BY APPLICATION, 2019-2022 (USD MILLION)

- TABLE 112 ROW: CAMERA MODULES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 13.5.1 IMPACT OF RECESSION ON CAMERA MODULES MARKET IN ROW

- 13.5.2 SOUTH AMERICA

- 13.5.2.1 Rising use of cameras in vehicles for 360° view and ADAS to support market growth

- 13.5.3 MIDDLE EAST & AFRICA

- 13.5.3.1 Strict security & surveillance regulations to propel adoption of cameras

14 COMPETITIVE LANDSCAPE

- 14.1 OVERVIEW

- 14.2 STRATEGIES ADOPTED BY KEY PLAYERS

- TABLE 113 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN CAMERA MODULES MARKET

- 14.3 REVENUE ANALYSIS, 2018-2022

- FIGURE 52 FIVE-YEAR REVENUE ANALYSIS OF TOP THREE PLAYERS IN CAMERA MODULES MARKET

- 14.4 MARKET SHARE ANALYSIS, 2022

- TABLE 114 CAMERA MODULES MARKET: MARKET SHARE ANALYSIS

- FIGURE 53 MARKET SHARE OF KEY PLAYERS, 2022

- 14.5 KEY COMPANY EVALUATION MATRIX, 2022

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- FIGURE 54 CAMERA MODULES MARKET (GLOBAL): KEY COMPANY EVALUATION MATRIX, 2022

- 14.6 STARTUPS/SMALL AND MEDIUM-SIZED ENTERPRISES (SMES) EVALUATION MATRIX, 2022

- 14.6.1 PROGRESSIVE COMPANIES

- 14.6.2 RESPONSIVE COMPANIES

- 14.6.3 DYNAMIC COMPANIES

- 14.6.4 STARTING BLOCKS

- FIGURE 55 CAMERA MODULES MARKET (GLOBAL): STARTUPS/SMES EVALUATION MATRIX, 2022

- 14.7 COMPANY FOOTPRINT

- TABLE 115 OVERALL COMPANY FOOTPRINT

- TABLE 116 COMPANY FOOTPRINT, BY COMPONENT

- TABLE 117 COMPANY FOOTPRINT, BY APPLICATION

- TABLE 118 COMPANY FOOTPRINT, BY REGION

- 14.8 COMPETITIVE BENCHMARKING

- TABLE 119 CAMERA MODULES MARKET: LIST OF KEY STARTUPS/SMES

- 14.9 COMPETITIVE SCENARIOS AND TRENDS

- TABLE 120 CAMERA MODULES MARKET: PRODUCT LAUNCHES, 2021-2023

- TABLE 121 CAMERA MODULES MARKET: DEALS, 2021-2023

- TABLE 122 CAMERA MODULES MARKET: OTHERS, 2021-2023

15 COMPANY PROFILES

- (Business overview, Product/Solution/Service offered, Recent developments & MnM View)**

- 15.1 KEY PLAYERS

- 15.1.1 LG INNOTEK

- TABLE 123 LG INNOTEK: COMPANY OVERVIEW

- FIGURE 56 LG INNOTEK: COMPANY SNAPSHOT

- TABLE 124 LG INNOTEK: PRODUCT/SOLUTION/SERVICE OFFERINGS

- TABLE 125 LG INNOTEK: PRODUCT LAUNCHES

- TABLE 126 LG INNOTEK: DEALS

- 15.1.2 OFILM

- TABLE 127 OFILM: COMPANY OVERVIEW

- TABLE 128 OFILM: PRODUCT/SOLUTION/SERVICE OFFERINGS

- 15.1.3 SUNNY OPTICAL TECHNOLOGY (GROUP) COMPANY LIMITED

- TABLE 129 SUNNY OPTICAL TECHNOLOGY (GROUP) COMPANY LIMITED: COMPANY OVERVIEW

- FIGURE 57 SUNNY OPTICAL TECHNOLOGY (GROUP) COMPANY LIMITED: COMPANY SNAPSHOT

- TABLE 130 SUNNY OPTICAL TECHNOLOGY (GROUP) COMPANY LIMITED: PRODUCT/SOLUTION/SERVICE OFFERINGS

- 15.1.4 HON HAI PRECISION INDUSTRY CO., LTD.

- TABLE 131 HON HAI PRECISION INDUSTRY CO., LTD.: COMPANY OVERVIEW

- FIGURE 58 HON HAI PRECISION INDUSTRY CO., LTD.: COMPANY SNAPSHOT

- TABLE 132 HON HAI PRECISION INDUSTRY CO., LTD.: PRODUCT/SOLUTION/SERVICE OFFERINGS

- TABLE 133 HON HAI PRECISION INDUSTRY CO., LTD.: DEALS

- 15.1.5 SAMSUNG ELECTRO-MECHANICS

- TABLE 134 SAMSUNG ELECTRO-MECHANICS: COMPANY OVERVIEW

- FIGURE 59 SAMSUNG ELECTRO-MECHANICS: COMPANY SNAPSHOT

- TABLE 135 SAMSUNG ELECTRO-MECHANICS: PRODUCT/SOLUTION/SERVICE OFFERINGS

- TABLE 136 SAMSUNG ELECTRO-MECHANICS: PRODUCT LAUNCHES

- 15.1.6 CHICONY ELECTRONICS CO., LTD

- TABLE 137 CHICONY ELECTRONICS CO., LTD: COMPANY OVERVIEW

- FIGURE 60 CHICONY ELECTRONICS CO., LTD: COMPANY SNAPSHOT

- TABLE 138 CHICONY ELECTRONICS CO., LTD: PRODUCT/SOLUTION/SERVICE OFFERINGS

- 15.1.7 Q TECHNOLOGY (GROUP) COMPANY LIMITED

- TABLE 139 Q TECHNOLOGY (GROUP) COMPANY LIMITED: COMPANY OVERVIEW

- TABLE 140 Q TECHNOLOGY (GROUP) COMPANY LIMITED: PRODUCT/SOLUTION/SERVICE OFFERINGS

- 15.1.8 AMS-OSRAM AG

- TABLE 141 AMS-OSRAM AG: COMPANY OVERVIEW

- FIGURE 61 AMS-OSRAM AG: COMPANY SNAPSHOT

- TABLE 142 AMS-OSRAM AG: PRODUCT/SOLUTION/SERVICE OFFERINGS

- TABLE 143 AMS-OSRAM AG: PRODUCT LAUNCHES

- 15.1.9 MCNEX CO., LTD

- TABLE 144 MCNEX CO., LTD: COMPANY OVERVIEW

- FIGURE 62 MCNEX CO., LTD: COMPANY SNAPSHOT

- TABLE 145 MCNEX CO., LTD: PRODUCT/SOLUTION/SERVICE OFFERINGS

- TABLE 146 MCNEX CO., LTD: PRODUCT LAUNCHES

- 15.1.10 TRULY INTERNATIONAL HOLDINGS LIMITED

- TABLE 147 TRULY INTERNATIONAL HOLDINGS LIMITED: COMPANY OVERVIEW

- FIGURE 63 TRULY INTERNATIONAL HOLDINGS LIMITED: COMPANY SNAPSHOT

- TABLE 148 TRULY INTERNATIONAL HOLDINGS LIMITED: PRODUCT/SOLUTION/SERVICE OFFERINGS

- *Details on Business overview, Product/Solution/Service offered, Recent developments & MnM View might not be captured in case of unlisted companies.

- 15.2 OTHER PLAYERS

- 15.2.1 CAMMSYS. CORP

- TABLE 149 CAMMSYS. CORP: COMPANY OVERVIEW

- 15.2.2 INTEL CORPORATION

- TABLE 150 INTEL CORPORATION: COMPANY OVERVIEW

- 15.2.3 PRIMAX ELECTRONICS LTD.

- TABLE 151 PRIMAX ELECTRONICS LTD.: COMPANY OVERVIEW

- 15.2.4 SONY CORPORATION

- TABLE 152 SONY CORPORATION: COMPANY OVERVIEW

- 15.2.5 SHENZHEN CHUANGMU TECHNOLOGY CO., LTD

- TABLE 153 SHENZHEN CM TECHNOLOGY CO., LTD: COMPANY OVERVIEW

- 15.2.6 JENOPTIK

- TABLE 154 JENOPTIK: COMPANY OVERVIEW

- 15.2.7 LEOPARD IMAGING INC.

- TABLE 155 LEOPARD IMAGING INC.: COMPANY OVERVIEW

- 15.2.8 LUXVISIONS-INNO

- TABLE 156 LUXVISIONS-INNO: COMPANY OVERVIEW

- 15.2.9 HAESUNG OPTICS

- TABLE 157 HAESUNG OPTICS: COMPANY OVERVIEW

- 15.2.10 COWELL

- TABLE 158 COWELL: COMPANY OVERVIEW

- 15.2.11 PARTRON

- TABLE 159 PARTRON: COMPANY OVERVIEW

- 15.2.12 OMNIVISION

- TABLE 160 OMNIVISION: COMPANY OVERVIEW

- 15.2.13 KYOCERA CORPORATION

- TABLE 161 KYOCERA CORPORATION: COMPANY OVERVIEW

- 15.2.14 E-CON SYSTEMS

- TABLE 162 E-CON SYSTEMS: COMPANY OVERVIEW

- 15.2.15 SYNTEC OPTICS

- TABLE 163 SYNTEC OPTICS: COMPANY OVERVIEW

- 15.2.16 NAMUGA

- TABLE 164 NAMUGA: COMPANY OVERVIEW

- 15.2.17 AAC TECHNOLOGIES

- TABLE 165 AAC TECHNOLOGIES: COMPANY OVERVIEW

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS