ADASの世界市場:PC/LCV/HCVシステムタイプ別、提供タイプ別、自動運転レベル別、安全用途別、EVタイプ別、地域別 - 予測(~2033年)

ADAS market by PC, LCV, HCV System Type (ACC, AEB, LDW, BSD), Offering Type [Hardware (Camera, Radar, LiDAR) and Software], LOA (L1, L2, L3, L4, L5), Safety Application (OCS, DashCam), EV Type, and Region - Global Forecast to 2033- 発行日

- ページ情報

- 英文 488 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 2033998

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

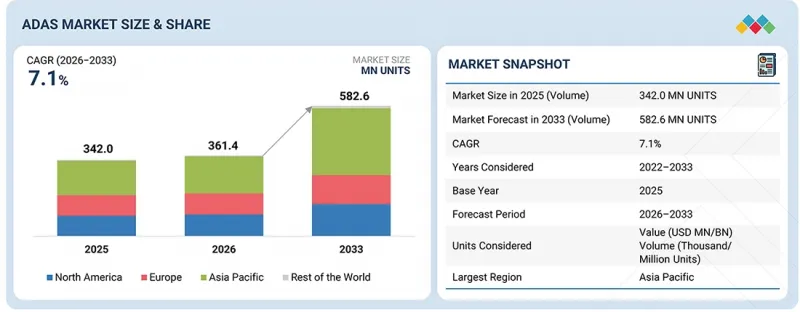

世界のADASの市場規模は、2026年の3億6,140万台から2033年までに5億8,260万台に達すると予測され、CAGRで7.1%の成長が見込まれています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2026年~2033年 |

| 基準年 | 2025年 |

| 予測期間 | 2026年~2033年 |

| 単位 | 1,000台、100万米ドル |

| セグメント | 自動車システム、提供タイプ、LOA、安全用途、EVタイプ、地域 |

| 対象地域 | アジア太平洋、欧州、北米、その他の地域 |

ADAS市場はソフトウェア主導のイノベーションへと移行しており、ユーザーフレンドリーなインターフェース、OTAアップデート、データアナリティクスに重点を置き、長期的にシステム性能を向上させています。エッジコンピューティングの進歩により、カメラやセンサーがデータをローカルで処理できるようになり、通信環境が不安定な地域でも、より迅速な意思決定と信頼性の高い動作が可能になっています。さらに、AI、機械学習、IoT、ビッグデータなどの技術の統合により、よりインテリジェントで適応性の高いシステムの開発が促進されています。安全規制の強化や、より安全な輸送手段への需要の高まりに伴い、ADASがドライバーの安全性の向上や事故の削減に寄与することから、商用車セグメントも成長が見込まれています。

2033年

2033年超音波センサーが予測期間にADAS市場を牽引すると見込まれています。

超音波センサーは、基本的な駐車支援から、死角検知、車線変更支援、ドライバーモニタリングといったより複雑な機能へと進化しています。この発達は、センサーの精度向上、小型化、その他の車両システムとの統合によって支えられており、現代の車両における安全機能の強化を可能にしています。これらのセンサーは通常、前後のバンパーに搭載され、近くの車両や障害物を検知し、最大3メートルの範囲内で効果的に機能します。ただし、斜めに位置する物体の検知や信号干渉の影響により、性能に限界が生じる場合があります。こうした課題をよそに、超音波センサーはあらゆる気象条件下で確実に機能します。Robert Bosch GmbH、Denso Corporation、Valeoといった企業が、主要OEMに超音波センサーを供給しています。例えば、Robert Bosch GmbHはBMW AGの2026 M2/M3モデル向けに超音波センサーを供給し、Denso CorporationはToyota Corporationの2026 Land Cruiser 300、Prius、Sientaモデル向けに供給しました。

バッテリー式電気自動車(BEV)が予測期間にADAS市場の最大のシェアを占める見込みです。

バッテリー式電気自動車(BEV)は、集中型かつソフトウェア定義の電気/電子(E/E)アーキテクチャに基づいて構築されており、これにより先進のADAS機能と高速通信ネットワークのシームレスな統合が可能となります。自動車メーカーはBEVを技術重視の車両として位置付けており、AEB、ACC、ハイウェイアシストなどのADAS機能を、標準装備またはサブスクリプションベースの機能として提供することがよくあります。これらの車両は、センサーフュージョンやリアルタイム処理をサポートする高性能コンピューティングプラットフォームや、ドメイン/ゾーンコントローラーを採用しています。ICE車とは異なり、BEVには従来の設計上の制約がないため、カメラ、レーダー、LiDARを含むスケーラブルなセンサー構成を容易に統合できます。さらに、BEVはOTAアップデートとの親和性が高く、車両の販売後もADAS機能を継続的に改良することが可能です。車両の安全性に対する規制当局の関心の高まりや、インテリジェントコネクテッド車に対する消費者需要の増加が、BEVにおけるADASの採用をさらに後押ししています。さらに、レーダーやLiDARと組み合わせたディープラーニングベースのビジョンシステムの採用により、AEBなどのADAS機能の精度と全体的な性能が向上しています。BMW、BYD、Mercedes-Benz、AudiなどのOEMは、先進の安全機能や運転支援機能を備えた電気自動車を投入しています。例えば2026年4月、CheryはExeed EX7を発売しました。このモデルには、インテリジェントドライビングに用いる長距離高精度LiDARやミリ波レーダーを含む27個の高性能センサーと、Nvidia Orin-Yチップが搭載されています。前述のすべての要因が、BEVにおけるADASの採用を後押ししています。

当レポートでは、世界のADAS市場について調査分析し、主な促進要因と抑制要因、製品開発とイノベーション、競合情勢に関する知見を提供しています。

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要な知見

- ADAS市場における企業にとって魅力的な機会

- ADAS市場:自動運転レベル別

- ADAS市場:乗用車システムタイプ別

- ADAS市場:小型商用車システムタイプ別

- ADAS市場:大型商用車システムタイプ別

- ADAS市場:電気自動車タイプ別

- ADAS市場:提供タイプ別

- ADAS市場:安全用途別

- ADAS市場:地域別

第4章 市場の概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 市場力学の影響の分析

- アンメットニーズとホワイトスペース

- ADAS市場におけるアンメットニーズ

- ホワイトスペースの機会

- 相互接続された市場と部門横断的な機会

- 相互接続された市場

- 部門横断的な機会

- Tier 1/2/3企業による戦略的な動き

第5章 業界動向

- マクロ経済指標

- GDPの動向と予測

- 世界のADAS市場の動向

- 世界の自動運転車業界の動向

- カスタマービジネスに影響を与える動向/混乱

- 価格設定の分析

- カメラユニットの平均販売価格の動向:地域別(2023年~2025年)

- LiDARの平均販売価格の動向:地域別(2023年~2025年)

- レーダーセンサーの平均販売価格の動向:地域別(2023年~2025年)

- 超音波センサーの平均販売価格の動向:地域別(2023年~2025年)

- エコシステム分析

- OEM

- Tier 1サプライヤー

- 自動運転車開発者

- ソフトウェア・システムプロバイダー

- LiDARシステムプロバイダー

- レーダーシステムプロバイダー

- カメラサプライヤー

- プロセッサー(SoC)メーカー

- センサーコンポーネントサプライヤー

- サプライチェーン分析

- ケーススタディ分析

- 投資と資金調達のシナリオ

- サプライヤー分析

- 半自動運転車/自動運転車の開発と展開

- レベル3

- レベル4・レベル5

- レベル2/レベル3とレベル4の自動運転スタックの主な違い

- モビリティ・トラック輸送におけるレベル4への進歩

- 貿易分析

- 輸入データ

- 輸出データ

- エネルギー市場の混乱

- 経営コストへの影響

- 市場需要の変化

- サプライチェーンとローカライゼーションの影響

- 戦略的市場の見通し

- EU・インド貿易協定の影響の分析

- EU関税

- インドへの輸入

- インドからの輸出

第6章 技術の進歩

- 特許分析

- 技術分析

- 主要技術

- 補完技術

- 隣接技術

- 技術/製品ロードマップ

- 短期:基盤構築と初期商業化(2026年~2027年)

- 中期:拡大と標準化(2028年~2030年)

- 長期:大規模な商業化と破壊的変化(2031年~2035年以降)

- AI/生成AIの影響

- 主なユースケースと市場の将来性

- メーカーが従うベストプラクティス

- AI導入に関するケーススタディ

- 相互接続されたエコシステムと市場企業の影響

- 顧客のAI採用に対する準備状況

第7章 規制情勢と持続可能性への取り組み

- 地域の規制と遵守事項

- 規制機関、政府機関、その他の組織

- 主要規制

- 持続可能性への取り組み

- 炭素排出とエコ用途

- 持続可能性への影響と規制政策構想

- 認証、ラベル表示、環境基準

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 購買プロセスにおける主なステークホルダーとその評価基準

- 購買プロセスにおける主なステークホルダー

- 購入基準

- 採用障壁と内部課題

- さまざまなエンドユーザー/最終用途産業におけるアンメットニーズ

第9章 乗用車向けADAS市場:システムタイプ別

- アダプティブクルーズコントロール(ACC)

- アダプティブフロントライト(AFL)

- 自動緊急ブレーキ(AEB)

- 死角検知(BSD)

- クロストラフィックアラート(CTA)

- ドライバーモニタリングシステム(DMS)

- 前方衝突警報(FCW)

- インテリジェント駐車支援(IPA)

- 車線逸脱警報(LDW)

- 暗視システム(NVS)

- 道路標識認識(RSR)

- タイヤ空気圧モニタリングシステム(TPMS)

- 渋滞運転支援(TJA)

- 重要な知見

第10章 小型商用車向けADAS市場:システムタイプ別

- アダプティブクルーズコントロール(ACC)

- アダプティブフロントライト(AFL)

- 自動緊急ブレーキ(AEB)

- 死角検知(BSD)

- クロストラフィックアラート(CTA)

- ドライバーモニタリングシステム(DMS)

- 前方衝突警報(FCW)

- インテリジェント駐車支援(IPA)

- 車線逸脱警報(LDW)

- 暗視システム(NVS)

- 道路標識認識(RSR)

- タイヤ空気圧モニタリングシステム(TPMS)

- 渋滞運転支援(TJA)

- 重要な知見

第11章 大型商用車向けADAS市場:システムタイプ別

- アダプティブクルーズコントロール(ACC)

- 自動緊急ブレーキ(AEB)

- 死角検知(BSD)

- 前方衝突警報(FCW)

- インテリジェント駐車支援(IPA)

- 車線逸脱警報(LDW)

- 渋滞運転支援(TJA)

- 重要な知見

第12章 ADAS市場:電気自動車タイプ別

- バッテリー式電気自動車(BEV)

- ハイブリッド電気自動車(HEV)

- プラグインハイブリッド電気自動車(PHEV)

- 燃料電池電気自動車(FCEV)

- 重要な知見

第13章 ADAS市場:自動運転レベル別

- L1

- L2

- L3

- L4

- L5

- 重要な知見

第14章 ADAS市場、提供タイプ

- ハードウェア提供

- カメラユニット

- LiDAR

- レーダーセンサー

- 超音波センサー

- ECU

- ソフトウェア提供

- OEM提供:ソフトウェア別

- ミドルウェア

- アプリケーションソフトウェア

- オペレーティングシステム

- 業界の主要動向

第15章 ADAS市場:安全用途別

- 乗員分類システム

- ドライブレコーダー

- 侵入検知

- 重要な知見

第16章 ADAS市場:地域別

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- タイ

- インドネシア

- その他のアジア太平洋

- 欧州

- ドイツ

- フランス

- イタリア

- スペイン

- ロシア

- 英国

- トルコ

- その他の欧州

- 北米

- 米国

- カナダ

- メキシコ

- その他の地域

- ブラジル

- 南アフリカ

- イラン

第17章 競合情勢

- 概要

- 主要参入企業の戦略/強み

- 主要企業の市場シェア分析(2025年)

- 上場非公開/公開会社の収益の分析(2025年)

- 企業の評価と財務指標

- ブランド/製品の比較

- 企業の評価マトリクス:主要企業(2025年)

- 企業の評価マトリクス:スタートアップ/中小企業(2025年)

- 競合シナリオ

第18章 企業プロファイル

- 主要企業

- ROBERT BOSCH GMBH

- AUMOVIO SE

- ZF FRIEDRICHSHAFEN AG

- DENSO CORPORATION

- MAGNA INTERNATIONAL INC.

- MOBILEYE

- APTIV

- VALEO

- HYUNDAI MOBIS

- NVIDIA CORPORATION

- NXP SEMICONDUCTORS

- AUTOLIV

- ASTEMO LTD.

- HORIZON ROBOTICS INC.

- ADVANCED MICRO DEVICES, INC.

- FICOSA INTERNACIONAL SA

- その他の主要企業

- AISIN CORPORATION

- RENESAS ELECTRONICS CORPORATION

- INFINEON TECHNOLOGIES AG

- HELLA GMBH & CO. KGAA

- TEXAS INSTRUMENTS INCORPORATED

- SAMSUNG

- GENTEX CORPORATION

- BLACKBERRY LIMITED

- MICROCHIP TECHNOLOGY INC.

- VEONEER US SAFETY SYSTEMS, LLC.

- PANASONIC AUTOMOTIVE SYSTEMS CO., LTD.

第19章 調査手法

第20章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 488 Pages

- 納期

- 即納可能