|

|

市場調査レポート

商品コード

1473753

航空機シートの世界市場:シートタイプ別、プラットフォーム別、エンドユーザー別、シート材料別、規格別、地域別 - 予測(~2029年)Aircraft Seating Market by Seat Type (Passenger Seat, Pilot, & Crew Seat), Platform (Narrow Body, Wide Body Aircraft, Business Jet, Commercial Helicopter, Light Aircraft, UAM), End-User, Seat Material, Standard and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 航空機シートの世界市場:シートタイプ別、プラットフォーム別、エンドユーザー別、シート材料別、規格別、地域別 - 予測(~2029年) |

|

出版日: 2024年04月30日

発行: MarketsandMarkets

ページ情報: 英文 427 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界の航空機シートの市場規模は、2024年の89億米ドルから2029年までに112億米ドルに達すると推定され、2024年~2029年にCAGRで4.8%の成長が予測されます。

同予測年における航空機の総座席数は、2024年の88万3,745席から2029年までに108万3,558席に達する見込みです。先進の製造技術、軽量材料、デジタルコックピットなど、シート技術の絶え間ない革新が、民間航空機と自家用機の両方で航空機シートのアップグレードへの需要を促進しています。旅客の期待や運航上の要件に後押しされ、航空機の快適性と安全性に対する需要が高まっていることが、航空機シート市場を刺激しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 単位 | 10億米ドル |

| セグメント | シートタイプ別、プラットフォーム別、エンドユーザー別、シート材料別、規格別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、その他の地域 |

「エンドユーザー別では、OEMセグメントが2024年にもっとも高い市場シェアを占める見込みです。」

OEMセグメントがもっとも高い55.1%の市場シェアを占めています。世界の民間航空機への需要の増加が、航空機シートOEM市場を牽引しています。航空機メーカーの納入率や生産率が高まるにつれ、統合型航空機シートの需要もそれに追随しています。航空企業は、全体的な運航効率を改善し、安全性を高め、乗客体験を向上させる航空機シートを求めています。航空機メーカーが競争力を維持するためには、このような運航面の強化を提供するOEMの航空機シートが不可欠となります。

「プラットフォーム別では、ナローボディ航空機セグメントが2024年にもっとも高い市場シェアを占めると推定されます。」

業界の主要企業は、この市場における新たな機会を探るため、先進の民間航空機シートの開発に積極的に取り組んでいます。ナローボディ航空機シート市場は、短・中距離便の需要の増加と格安航空企業の登場により活況を呈しています。航空企業は客室の効率と乗客の快適性を優先しており、軽量で省スペースな座席ソリューションへのニーズが高まっています。

「北米が2024年にもっとも高い市場シェアを占める見込みです。」

この地域の強力な航空産業は、大手航空企業と技術革新に牽引され、最新のシートソリューションに対する継続的な需要を育み、民間航空機への先進のシートシステムの搭載につながっています。北米の航空産業は、既存の航空機数が多いため、航空機シートのアップグレードや改修に大きな重点を置いています。航空企業や運航企業は、古い航空機の近代化ソリューションを求めており、性能の向上と進化する規制への準拠を目的とした航空機シートのメンテナンスと修理への需要を促進しています。

北米では、BoeingやAirbusなどの主要航空機メーカーが次世代航空機シートに継続的に投資しています。Boeing 737 MAXやAirbus A320neoファミリーのような先進のプラットフォームの開発により、機能や特徴を強化した航空機シートの機会が生まれています。航空機シートメーカーとBoeingやAirbusのような航空宇宙大手との戦略的パートナーシップや提携は、航空機シート市場の成長に寄与しています。共同活動は、特定の航空機モデルに合わせた革新的なシートソリューションの開発につながることが多いです。

当レポートでは、世界の航空機シート市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 航空機シート市場の企業にとって魅力的な機会

- 航空機シート市場:プラットフォーム別

- 航空機シート市場:エンドユーザー別

- 航空機シート市場:国別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- バリューチェーン分析

- 顧客のビジネスに影響を与える動向と混乱

- 技術ロードマップ

- エコシステム分析

- 著名企業

- 民間企業、中小企業

- エンドユーザー

- 総所有コスト

- ビジネスモデル

- 部品表

- 投資と資金調達のシナリオ

- 価格分析

- 参考価格分析:地域別

- 参考価格分析:プラットフォーム別

- 技術分析

- 主要技術

- 補完技術

- 規制情勢

- 貿易分析

- 主なステークホルダーと購入基準

- 主な会議とイベント(2024年)

- ユースケース分析

- 運航データ

第6章 産業動向

- イントロダクション

- 技術動向

- 先進材料

- 積層造形

- モジュラー式、再構成可能なシートデザイン

- 抗菌、耐火コーティング

- メガトレンドの影響

- インダストリー4.0

- スマートキャビン

- サプライチェーン分析

- 特許分析

第7章 航空機シート市場:エンドユーザー別

- イントロダクション

- OEM

- MRO

- アフターマーケット

第8章 航空機シート市場:プラットフォーム別

- イントロダクション

- ナローボディ航空機

- ワイドボディ航空機

- ビジネスジェット

- 地域間輸送航空機

- 民間ヘリコプター

- 一般航空

- UAM

第9章 航空機シート市場:シート材料別

- イントロダクション

- クッション材料

- 構造材料

- 室内装飾品・シートカバー

第10章 航空機シート市場:座席タイプ別

- イントロダクション

- 乗客シート

- パイロット・クルーシート

第11章 航空機シート市場:規格別

- イントロダクション

- 16G

- 21G

第12章 航空機シート市場:地域別

- イントロダクション

- 景気後退の影響の分析:地域別

- 北米

- 景気後退の影響の分析

- PESTLE分析

- 米国

- カナダ

- 欧州

- 景気後退の影響の分析

- PESTLE分析

- 英国

- フランス

- ドイツ

- イタリア

- ロシア

- その他の欧州

- アジア太平洋

- 景気後退の影響の分析

- PESTLE分析

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- 中東

- 景気後退の影響の分析

- PESTLE分析

- GCC

- その他の中東

- アフリカ

- 景気後退の影響の分析

- PESTLE分析

- 南アフリカ

- ナイジェリア

- その他のアフリカ

- ラテンアメリカ

- 景気後退の影響の分析

- PESTLE分析

- ブラジル

- メキシコ

- その他のラテンアメリカ

第13章 競合情勢

- イントロダクション

- 主な企業の戦略/有力企業(2020年~2024年)

- ランキング分析(2023年)

- 収益分析(2019年~2023年)

- 市場シェア分析(2023年)

- 企業評価マトリクス:主要企業(2023年)

- 企業評価マトリクス:スタートアップ/中小企業(2023年)

- 企業評価と財務指標

- ブランド/製品の比較

- 競合シナリオと動向

第14章 企業プロファイル

- 主要企業

- SAFRAN

- RAYTHEON TECHNOLOGIES

- RECARO AIRCRAFT SEATING GMBH & CO. KG

- ZIM AIRCRAFT SEATING GMBH

- STELIA AEROSPACE

- JAMCO CORPORATION

- ST ENGINEERING

- ACRO AIRCRAFT SEATING

- EXPLISEAT

- ADIENT AEROSPACE LLC

- MIRUS AIRCRAFT SEATING

- MARTIN-BAKER AIRCRAFT CO. LTD

- GEVEN SPA

- IPECO HOLDINGS LTD

- UNUM

- その他の企業

- AVIOINTERIORS S.P.A.

- THOMPSON AERO

- IACOBUCCI HF AEROSPACE

- OPTIMARES SPA

- AIRGO DESIGN

- JHAS SPA

- MOBIUS PROTECTION SYSTEMS LTD.

- ALICEBLUAERO

- TIMETOOTH TECHNOLOGIES

- MOLON LABE SEATING

第15章 付録

The Aircraft seating market is estimated to grow from USD 11.2 billion by 2029, from USD 8.9 billion in 2024, at a CAGR of 4.8% from 2024 to 2029. The total aircraft seating volume in the same forecast year is estimated to grow from 883,745 units in 2024 to 1,083,558 units in 2029. Constant innovation in seating technologies, such as advanced manufacturing techniques, lightweight materials, and digital cockpit, fuels the demand for upgraded aircraft seats across both commercial and private aircraft. The increasing demand for comfort and safety capabilities in aircraft, driven by passenger expectations and operational requirements, stimulates the market for aircraft seats.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Seat Type, Platform, End-User, Seat Material, Standard and Region |

| Regions covered | Asia Pacific, North America, Europe, Rest of the World |

"OEM segment by end user is expected to hold the highest market share in 2024."

Based on end user, the aircraft seating market is categorized into OEM, MRO, and aftermarket. The OEM segment having highest market share of 55.1%. The increasing global demand for commercial aircraft drives the aircraft seating OEM market. As aircraft manufacturers experience higher delivery and production rates, the demand for integrated aircraft seats directly follows suit. Airlines seek aircraft seats that improve overall operational efficiency, increase safety, and enhance passenger experience. OEM aircraft seats that offer such operational enhancements become crucial for aircraft manufacturers to remain competitive.

"Narrow-body Aircraft segment by platform is estimated to hold the highest market share in 2024."

Based on Platform, the market is further divided into narrow-body aircraft, wide-body aircraft, regional transport aircraft, business jet, general aviation, commercial helicopter, and UAM. Major industry players are actively engaged in developing advanced commercial aviation aircraft seats to explore emerging opportunities in this market. The narrow-body aircraft seating market is thriving due to increased demand for short to medium-haul flights and the emergence of low-cost carriers. Airlines prioritize cabin efficiency and passenger comfort, driving the need for lightweight and space-saving seating solutions.

"North America is expected to hold the highest market share in 2024."

The region's robust aviation industry, driven by major carriers and technological innovation, fosters continuous demand for modern seating solutions, leading to the incorporation of advanced seating systems in commercial aircraft. With a substantial existing fleet, the North American aviation industry places significant emphasis on aircraft seating upgrades and retrofits. Airlines and operators seek modernization solutions for older aircraft, driving the demand for maintenance and repair of aircraft seats to enhance performance and compliance with evolving regulations.

North America covers the US and Canada for market analysis. In North America, major aircraft manufacturers like Boeing and Airbus continually invest in next-generation aircraft seats. The development of advanced platforms, such as the Boeing 737 MAX and Airbus A320neo families, creates opportunities for aircraft seats with enhanced capabilities and features. The strategic partnerships and collaborations between aircraft seat manufacturers and aerospace giants like Boeing and Airbus contribute to the growth of the aircraft seating market. Joint initiatives often lead to the development of innovative seating solutions tailored to specific aircraft models.

The break-up of the profile of primary participants in the aircraft seating market:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C Level - 35%, Director Level - 25%, Others - 40%

- By Region: North America - 20%, Europe - 25%, Asia Pacific - 35%, Latin America - 5%, Middle East - 10% & Africa - 5%

Raytheon Technologies Corporation (US), Safran (France), RECARO Aircraft Seating GmbH & Co. KG (Germany), ZIM Aircraft Seating GmbH (Germany), Stelia Aerospace (France). These key players offer connectivity applicable to various sectors and have well-equipped and strong distribution networks across North America, Europe, Asia Pacific, the Middle East, Africa, and Latin America.

Research Coverage:

In terms of Solutions, the aircraft seating market is divided into Products and MRO services. The end user segment of the aircraft seating market is OEM, MRO and aftermarket.

The Platform based segmentation includes narrow-body aircraft, wide-body aircraft, regional transport aircraft, business jet, general aviation, commercial helicopter, and UAM.

Based on seat type, the aircraft seating market is further segmented into passenger seats, and pilot 7 crew seats. The seat material segment is divided into cushion materials, structure materials, upholsteries and seat cover materials.

This report segments the aircraft seating market across six key regions: North America, Europe, Asia Pacific, the Middle East, Africa and Latin America along with their respective key countries. The report's scope includes in-depth information on significant factors, such as drivers, restraints, challenges, and opportunities that influence the growth of the aircraft seating market.

A comprehensive analysis of major industry players has been conducted to provide insights into their business profiles, solutions, and services. This analysis also covers key aspects like agreements, collaborations, new product launches, contracts, expansions, acquisitions, and partnerships associated with the aircraft seating market.

Reasons to buy this report:

This report serves as a valuable resource for market leaders and newcomers in the aircraft seating market, offering data that closely approximates revenue figures for both the overall market and its subsegments. It equips stakeholders with a comprehensive understanding of the competitive landscape, facilitating informed decisions to enhance their market positioning and formulating effective go-to-market strategies for Simulation. The report imparts valuable insights into the market dynamics, offering information on crucial factors such as drivers, restraints, challenges, and opportunities, enabling stakeholders to gauge the market's pulse.

The report provides insights on the following pointers:

- Analysis of the key driver (Rising aircraft deliveries and air travel demand, Technological advancements in aircraft seat manufacturing) restraint (Stringent Regulatory and certification requirements, Supply chain vulnerabilities) opportunities (Rapidly expanding global economy, Emergence of urban air mobility) and challenges (Complex design and integration of new materials, High production and procurement costs ) there are several factors that could contribute to an increase in the aircraft seating market.

- Market Penetration: Comprehensive information on aircraft seating solutions offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the aircraft seating market

- Market Development: Comprehensive information about lucrative markets - the report analyses the aircraft seating market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the aircraft seating market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the aircraft seating market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- TABLE 1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 AIRCRAFT SEATING MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 2 USD EXCHANGE RATES

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 RESEARCH PROCESS FLOW

- FIGURE 3 RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Primary sources

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Breakdown of primary interviews

- 2.2 FACTOR ANALYSIS

- 2.2.1 INTRODUCTION

- 2.2.2 DEMAND-SIDE INDICATORS

- 2.2.3 SUPPLY-SIDE INDICATORS

- 2.2.4 RECESSION IMPACT ANALYSIS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Market size estimation methodology (demand-side)

- 2.3.1.2 Market size estimation illustration-US wide-body economy aircraft seat OEM market

- FIGURE 4 BOTTOM-UP APPROACH

- 2.3.2 TOP-DOWN APPROACH

- FIGURE 5 TOP-DOWN APPROACH

- 2.3.1 BOTTOM-UP APPROACH

- 2.4 DATA TRIANGULATION

- FIGURE 6 DATA TRIANGULATION

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

- 2.7 RISK ASSESSMENT

3 EXECUTIVE SUMMARY

- FIGURE 7 NARROW-BODY AIRCRAFT TO BE LARGEST SEGMENT DURING FORECAST PERIOD

- FIGURE 8 OEM TO SECURE LEADING MARKET POSITION DURING FORECAST PERIOD

- FIGURE 9 PASSENGER SEATS TO HOLD HIGHER MARKET SHARE DURING FORECAST PERIOD

- FIGURE 10 BUSINESS CLASS TO SURPASS OTHER SEGMENTS DURING FORECAST PERIOD

- FIGURE 11 EUROPE TO BE FASTEST-GROWING MARKET DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AIRCRAFT SEATING MARKET

- FIGURE 12 INCREASE IN DEMAND FOR LIGHTER AND SAFER SEATS TO DRIVE GROWTH

- 4.2 AIRCRAFT SEATING MARKET, BY PLATFORM

- FIGURE 13 NARROW-BODY AIRCRAFT TO DOMINATE MARKET IN 2024

- 4.3 AIRCRAFT SEATING MARKET, BY END USER

- FIGURE 14 OEM TO EXHIBIT FASTEST GROWTH DURING FORECAST PERIOD

- 4.4 AIRCRAFT SEATING MARKET, BY COUNTRY

- FIGURE 15 FRANCE TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 16 AIRCRAFT SEATING MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rising aircraft deliveries and air travel demand

- FIGURE 17 AIRCRAFT DELIVERIES BY BOEING AND AIRBUS, 2019-2023

- 5.2.1.2 Technological advancements in aircraft seat manufacturing

- 5.2.2 RESTRAINTS

- 5.2.2.1 Stringent regulatory and certification requirements

- 5.2.2.2 Supply chain vulnerabilities

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rapidly expanding global economy

- 5.2.3.2 Emergence of urban air mobility

- 5.2.4 CHALLENGES

- 5.2.4.1 Complex design and integration of new materials

- 5.2.4.2 High production and procurement costs

- 5.3 VALUE CHAIN ANALYSIS

- FIGURE 18 VALUE CHAIN ANALYSIS

- 5.4 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 19 TRENDS AND DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.5 TECHNOLOGY ROADMAP

- FIGURE 20 INTRODUCTION TO TECHNOLOGY ROADMAP

- FIGURE 21 EVOLUTION OF KEY TECHNOLOGIES

- FIGURE 22 EMERGING TRENDS RELATED TO AIRCRAFT SEATS

- 5.6 ECOSYSTEM ANALYSIS

- 5.6.1 PROMINENT COMPANIES

- 5.6.2 PRIVATE AND SMALL ENTERPRISES

- 5.6.3 END USERS

- FIGURE 23 ECOSYSTEM ANALYSIS

- TABLE 3 ROLE OF COMPANIES IN ECOSYSTEM

- 5.7 TOTAL COST OF OWNERSHIP

- FIGURE 24 TOTAL COST OF OWNERSHIP OF AIRCRAFT SEATS

- TABLE 4 TOTAL COST OF OWNERSHIP OF AIRCRAFT SEATS (USD)

- 5.8 BUSINESS MODELS

- FIGURE 25 BUSINESS MODELS IN AIRCRAFT SEATING MARKET

- 5.9 BILL OF MATERIALS

- FIGURE 26 BILL OF MATERIALS FOR ECONOMY CLASS SEATS

- FIGURE 27 BILL OF MATERIALS FOR PREMIUM ECONOMY CLASS SEATS

- FIGURE 28 BILL OF MATERIALS FOR BUSINESS CLASS SEATS

- FIGURE 29 BILL OF MATERIALS FOR FIRST CLASS SEATS

- 5.10 INVESTMENT AND FUNDING SCENARIO

- 5.11 PRICING ANALYSIS

- 5.11.1 INDICATIVE PRICING ANALYSIS, BY REGION

- FIGURE 30 INDICATIVE PRICING ANALYSIS, BY REGION (USD)

- TABLE 5 INDICATIVE PRICING ANALYSIS, BY REGION (USD)

- 5.11.2 INDICATIVE PRICING ANALYSIS, BY PLATFORM

- 5.12 TECHNOLOGY ANALYSIS

- 5.12.1 KEY TECHNOLOGY

- 5.12.1.1 Butterfly seating

- 5.12.1.2 Zero gravity seats

- 5.12.2 COMPLIMENTARY TECHNOLOGY

- 5.12.2.1 Advanced sensors

- 5.12.1 KEY TECHNOLOGY

- 5.13 REGULATORY LANDSCAPE

- TABLE 6 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 MIDDLE EAST: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.14 TRADE ANALYSIS

- 5.14.1 IMPORT VALUE OF (HS CODE: 8803) PARTS OF AIRCRAFT AND SPACECRAFT OF HEADING 8801 OR 8802, N.E.S.

- FIGURE 31 IMPORT DATA, BY COUNTRY, 2019-2022 (USD THOUSAND)

- TABLE 12 IMPORT DATA, BY COUNTRY, 2019-2022 (USD THOUSAND)

- 5.14.2 EXPORT VALUE OF (HS CODE: 8803) PARTS OF AIRCRAFT AND SPACECRAFT OF HEADING 8801 OR 8802, N.E.S.

- FIGURE 32 EXPORT DATA, BY COUNTRY, 2019-2022 (USD THOUSAND)

- TABLE 13 EXPORT DATA, BY COUNTRY, 2019-2022 (USD THOUSAND)

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 33 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF AIRCRAFT SEATS, BY PLATFORM

- TABLE 14 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS OF AIRCRAFT SEATS, BY PLATFORM (%)

- 5.15.2 BUYING CRITERIA

- FIGURE 34 KEY BUYING CRITERIA FOR AIRCRAFT SEATS, BY SEAT TYPE

- TABLE 15 KEY BUYING CRITERIA FOR AIRCRAFT SEATS, BY SEAT TYPE

- 5.16 KEY CONFERENCES AND EVENTS, 2024

- TABLE 16 KEY CONFERENCES AND EVENTS, 2024

- 5.17 USE CASE ANALYSIS

- 5.17.1 ESSENCE BY ELEATHER

- 5.17.2 AIRTEK BY JPA DESIGN

- 5.17.3 KNEE-RESCUE SEAT BY B/E AEROSPACE

- 5.17.4 INTERSPACE LITE BY UNIVERSAL MOVEMENT

- 5.18 OPERATIONAL DATA

- 5.18.1 NEW AIRCRAFT DELIVERIES

- TABLE 17 GLOBAL AIRCRAFT DELIVERIES, BY PLATFORM, 2020-2029 (UNITS)

- 5.18.2 ACTIVE AIRCRAFT FLEETS

- TABLE 18 GLOBAL ACTIVE AIRCRAFT FLEET, BY PLATFORM, 2020-2029 (UNITS)

- TABLE 19 ACTIVE AIRCRAFT FLEETS, BY REGION, 2020-2029 (UNITS)

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TECHNOLOGY TRENDS

- 6.2.1 ADVANCED MATERIALS

- 6.2.2 ADDITIVE MANUFACTURING

- 6.2.3 MODULAR AND RECONFIGURABLE SEAT DESIGNS

- 6.2.4 ANTIMICROBIAL AND FLAME-RETARDANT COATINGS

- 6.3 IMPACT OF MEGATRENDS

- 6.3.1 INDUSTRY 4.0

- 6.3.2 SMART CABIN

- 6.4 SUPPLY CHAIN ANALYSIS

- FIGURE 35 SUPPLY CHAIN ANALYSIS

- 6.5 PATENT ANALYSIS

- FIGURE 36 PATENT ANALYSIS

- TABLE 20 PATENT ANALYSIS

7 AIRCRAFT SEATING MARKET, BY END USER

- 7.1 INTRODUCTION

- FIGURE 37 AIRCRAFT SEATING MARKET, BY END USER, 2024-2029

- TABLE 21 AIRCRAFT SEATING MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 22 AIRCRAFT SEATING MARKET, BY END USER, 2024-2029 (USD MILLION)

- TABLE 23 AIRCRAFT SEAT VOLUME, BY END USER, 2024-2029 (UNITS)

- 7.2 OEM

- 7.2.1 INCREASING AIRCRAFT ORDERS TO DRIVE GROWTH

- 7.3 MRO

- 7.3.1 RISING DEMAND FOR SEAT MAINTENANCE AND REPAIR BY AIRLINES TO DRIVE GROWTH

- 7.4 AFTERMARKET

- 7.4.1 ONGOING UPGRADES OF AIRCRAFT SEATS TO ENHANCE CUSTOMER EXPERIENCE TO DRIVE GROWTH

8 AIRCRAFT SEATING MARKET, BY PLATFORM

- 8.1 INTRODUCTION

- FIGURE 38 AIRCRAFT SEATING MARKET, BY PLATFORM, 2024-2029

- TABLE 24 AIRCRAFT SEATING MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 25 AIRCRAFT SEATING MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 26 AIRCRAFT VOLUME, BY PLATFORM, 2024-2029 (UNITS)

- 8.2 NARROW-BODY AIRCRAFT

- 8.2.1 FOCUS ON REDUCING AIRCRAFT WEIGHT TO DRIVE GROWTH

- 8.3 WIDE-BODY AIRCRAFT

- 8.3.1 SURGE IN DEMAND FOR ULTRA-LONG-RANGE TRAVEL TO DRIVE GROWTH

- 8.4 BUSINESS JET

- 8.4.1 DEVELOPMENTS IN AIRCRAFT SEAT ARCHITECTURE TO DRIVE GROWTH

- 8.5 REGIONAL TRANSPORT AIRCRAFT

- 8.5.1 INCREASED DEMAND FOR COMFORTABLE AND COST-EFFECTIVE REGIONAL AIR TRAVEL TO DRIVE GROWTH

- 8.6 COMMERCIAL HELICOPTER

- 8.6.1 WIDE SCOPE OF APPLICATIONS TO DRIVE GROWTH

- 8.7 GENERAL AVIATION

- 8.7.1 RISING USE OF AIRCRAFT IN AGRICULTURE TO DRIVE GROWTH

- 8.8 UAM

- 8.8.1 INNOVATIONS IN AIR MOBILITY TO DRIVE GROWTH

9 AIRCRAFT SEATING MARKET, BY SEAT MATERIAL

- 9.1 INTRODUCTION

- FIGURE 39 AIRCRAFT SEATING MARKET, BY SEAT MATERIAL, 2024-2029

- TABLE 27 AIRCRAFT SEATING MARKET, BY SEAT MATERIAL, 2020-2023 (USD MILLION)

- TABLE 28 AIRCRAFT SEATING MARKET, BY SEAT MATERIAL, 2024-2029 (USD MILLION)

- 9.2 CUSHION MATERIALS

- TABLE 29 CUSHION MATERIALS: AIRCRAFT SEATING MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 30 CUSHION MATERIALS: AIRCRAFT SEATING MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 9.2.1 POLYURETHANE

- 9.2.1.1 Optimal density and durability to drive growth

- 9.2.2 POLYETHYLENE

- 9.2.2.1 Impact resistance and recyclability to drive growth

- 9.2.3 NEOPRENE

- 9.2.3.1 Flame retardant capabilities to drive growth

- 9.2.4 OTHERS

- 9.3 STRUCTURE MATERIALS

- TABLE 31 STRUCTURE MATERIALS: AIRCRAFT SEATING MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 32 STRUCTURE MATERIALS: AIRCRAFT SEATING MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 9.3.1 ALUMINUM

- 9.3.1.1 Ease of fabrication and corrosion resistance to drive growth

- 9.3.2 CARBON FIBER

- 9.3.2.1 Excellent strength-to-weight ratio to drive growth

- 9.3.3 FIBERGLASS

- 9.3.3.1 Robust mechanical properties to drive growth

- 9.3.4 OTHERS

- 9.4 UPHOLSTERIES & SEAT COVERS

- TABLE 33 UPHOLSTERIES & SEAT COVERS: AIRCRAFT SEATING MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 34 UPHOLSTERIES & SEAT COVERS: AIRCRAFT SEATING MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 9.4.1 FABRIC

- 9.4.1.1 Easy moisture absorption to drive growth

- 9.4.2 VINYL

- 9.4.2.1 Water and stain-resistant properties to drive growth

- 9.4.3 LEATHER

- 9.4.3.1 Sustainability and longevity to drive growth

10 AIRCRAFT SEATING MARKET, BY SEAT TYPE

- 10.1 INTRODUCTION

- FIGURE 40 AIRCRAFT SEATING MARKET, BY SEAT TYPE, 2024-2029

- TABLE 35 AIRCRAFT SEATING MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 36 AIRCRAFT SEATING MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 37 AIRCRAFT SEAT VOLUME, BY SEAT TYPE, 2024-2029 (USD MILLION)

- 10.2 PASSENGER SEATS

- FIGURE 41 PREMIUM ECONOMY CLASS TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- TABLE 38 PASSENGER SEATS: AIRCRAFT SEATING MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 39 PASSENGER SEATS: AIRCRAFT SEATING MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.2.1 FIRST CLASS

- TABLE 40 FIRST CLASS AIRCRAFT SEATING MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 41 FIRST CLASS AIRCRAFT SEATING MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- 10.2.1.1 First class seat components

- TABLE 42 FIRST CLASS AIRCRAFT SEATING MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 43 FIRST CLASS AIRCRAFT SEATING MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- 10.2.1.1.1 Structures

- 10.2.1.1.2 Foams

- 10.2.1.1.3 Actuators

- 10.2.1.1.4 Electrical fittings

- 10.2.1.1.5 Others

- 10.2.1.2 First class seat materials

- TABLE 44 FIRST CLASS AIRCRAFT SEATING MARKET, BY MATERIAL, 2020-2023 (USD MILLION)

- TABLE 45 FIRST CLASS AIRCRAFT SEATING MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- 10.2.1.2.1 Cushion materials

- 10.2.1.2.2 Structure materials

- 10.2.1.2.3 Upholsteries & seat covers

- 10.2.2 BUSINESS CLASS

- TABLE 46 BUSINESS CLASS AIRCRAFT SEATING MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 47 BUSINESS CLASS AIRCRAFT SEATING MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- 10.2.2.1 Business class seat components

- TABLE 48 BUSINESS CLASS AIRCRAFT SEATING MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 49 BUSINESS CLASS AIRCRAFT SEATING MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- 10.2.2.1.1 Structures

- 10.2.2.1.2 Foams

- 10.2.2.1.3 Actuators

- 10.2.2.1.4 Electrical fittings

- 10.2.2.1.5 Others

- 10.2.2.2 Business class seat materials

- TABLE 50 BUSINESS CLASS AIRCRAFT SEATING MARKET, BY MATERIAL, 2020-2023 (USD MILLION)

- TABLE 51 BUSINESS CLASS AIRCRAFT SEATING MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- 10.2.2.2.1 Cushion materials

- 10.2.2.2.2 Structure materials

- 10.2.2.2.3 Upholsteries & seat covers

- 10.2.3 PREMIUM ECONOMY CLASS

- TABLE 52 PREMIUM ECONOMY CLASS AIRCRAFT SEATING MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 53 PREMIUM ECONOMY CLASS AIRCRAFT SEATING MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- 10.2.3.1 Premium economy class seat components

- TABLE 54 PREMIUM ECONOMY CLASS AIRCRAFT SEATING MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 55 PREMIUM ECONOMY CLASS AIRCRAFT SEATING MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- 10.2.3.1.1 Structures

- 10.2.3.1.2 Foams

- 10.2.3.1.3 Actuators

- 10.2.3.1.4 Electrical fittings

- 10.2.3.1.5 Others

- 10.2.3.2 Premium economy class seat materials

- TABLE 56 PREMIUM ECONOMY CLASS AIRCRAFT SEATING MARKET, BY MATERIAL, 2020-2023 (USD MILLION)

- TABLE 57 PREMIUM ECONOMY CLASS AIRCRAFT SEATING MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- 10.2.3.2.1 Cushion materials

- 10.2.3.2.2 Structure materials

- 10.2.3.2.3 Upholsteries & seat covers

- 10.2.4 ECONOMY CLASS

- TABLE 58 ECONOMY CLASS AIRCRAFT SEATING MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 59 ECONOMY CLASS AIRCRAFT SEATING MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- 10.2.4.1 Economy class seat components

- TABLE 60 ECONOMY CLASS AIRCRAFT SEATING MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 61 ECONOMY CLASS AIRCRAFT SEATING MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- 10.2.4.1.1 Structures

- 10.2.4.1.2 Foams

- 10.2.4.1.3 Others

- 10.2.4.2 Economy class seat materials

- TABLE 62 ECONOMY CLASS AIRCRAFT SEATING MARKET, BY MATERIAL, 2020-2023 (USD MILLION)

- TABLE 63 ECONOMY CLASS AIRCRAFT SEATING MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- 10.2.4.2.1 Cushion materials

- 10.2.4.2.2 Structure materials

- 10.2.4.2.3 Upholsteries & seat covers

- 10.3 PILOT & CREW SEATS

- FIGURE 42 PILOT SEATS TO BE FASTEST-GROWING SEGMENT DURING FORECAST PERIOD

- TABLE 64 PILOT & CREW SEATS: AIRCRAFT SEATING MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 65 PILOT & CREW SEATS: AIRCRAFT SEATING MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.3.1 PILOT SEATS

- TABLE 66 PILOT SEATS: AIRCRAFT SEATING MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 67 PILOT SEATS: AIRCRAFT SEATING MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- 10.3.1.1 Pilot seat components

- TABLE 68 PILOT AIRCRAFT SEATING MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 69 PILOT AIRCRAFT SEATING MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- 10.3.1.1.1 Structures

- 10.3.1.1.2 Foams

- 10.3.1.1.3 Actuators

- 10.3.1.1.4 Electrical fittings

- 10.3.1.1.5 Others

- 10.3.1.2 Pilot seat materials

- TABLE 70 PILOT AIRCRAFT SEATING MARKET, BY MATERIAL, 2020-2023 (USD MILLION)

- TABLE 71 PILOT AIRCRAFT SEATING MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- 10.3.1.2.1 Cushion materials

- 10.3.1.2.2 Structure materials

- 10.3.1.2.3 Upholsteries & seat covers

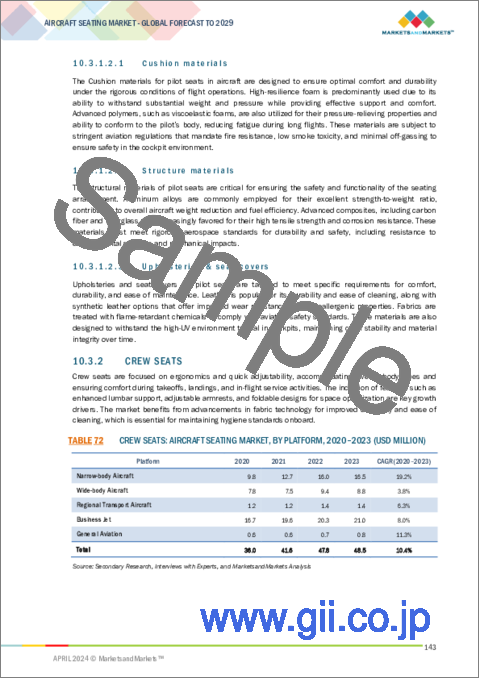

- 10.3.2 CREW SEATS

- TABLE 72 CREW SEATS: AIRCRAFT SEATING MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 73 CREW SEATS: AIRCRAFT SEATING MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- 10.3.2.1 Crew seat components

- TABLE 74 CREW AIRCRAFT SEATING MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 75 CREW AIRCRAFT SEATING MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- 10.3.2.1.1 Structures

- 10.3.2.1.2 Foams

- 10.3.2.1.3 Actuators

- 10.3.2.1.4 Electrical fittings

- 10.3.2.1.5 Others

- 10.3.2.2 Crew seat materials

- TABLE 76 CREW AIRCRAFT SEATING MARKET, BY MATERIAL, 2020-2023 (USD MILLION)

- TABLE 77 CREW AIRCRAFT SEATING MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- 10.3.2.2.1 Cushion materials

- 10.3.2.2.2 Structure materials

- 10.3.2.2.3 Upholsteries & seat covers

11 AIRCRAFT SEATING MARKET, BY STANDARD

- 11.1 INTRODUCTION

- 11.2 16G

- 11.3 21G

12 AIRCRAFT SEATING MARKET, BY REGION

- 12.1 INTRODUCTION

- FIGURE 43 AIRCRAFT SEATING MARKET, BY REGION, 2024-2029

- TABLE 78 AIRCRAFT SEATING MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 79 AIRCRAFT SEATING MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 80 AIRCRAFT SEAT VOLUME, BY REGION, 2024-2029 (UNITS)

- 12.2 REGIONAL RECESSION IMPACT ANALYSIS

- 12.3 NORTH AMERICA

- FIGURE 44 NORTH AMERICA: AIRCRAFT SEATING MARKET SNAPSHOT

- 12.3.1 RECESSION IMPACT ANALYSIS

- 12.3.2 PESTLE ANALYSIS

- TABLE 81 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 82 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 83 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 84 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 85 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 86 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 87 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 88 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 89 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 90 NORTH AMERICA: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 91 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 92 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 93 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 94 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 95 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 96 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 97 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 98 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 99 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 100 NORTH AMERICA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 101 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 102 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 103 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 104 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 105 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 106 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 107 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 108 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 109 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 110 NORTH AMERICA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.3.3 US

- 12.3.3.1 Significant presence of aircraft seat manufacturers to drive growth

- TABLE 111 US: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 112 US: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 113 US: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 114 US: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 115 US: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 116 US: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 117 US: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 118 US: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 119 US: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 120 US: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 121 US: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 122 US: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 123 US: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 124 US: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 125 US: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 126 US: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 127 US: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 128 US: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 129 US: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 130 US: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 131 US: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 132 US: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 133 US: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 134 US: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.3.4 CANADA

- 12.3.4.1 Increasing R&D investments in aviation industry to drive growth

- TABLE 135 CANADA: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 136 CANADA: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 137 CANADA: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 138 CANADA: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 139 CANADA: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 140 CANADA: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 141 CANADA: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 142 CANADA: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 143 CANADA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 144 CANADA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 145 CANADA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 146 CANADA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 147 CANADA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 148 CANADA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 149 CANADA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 150 CANADA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 151 CANADA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 152 CANADA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 153 CANADA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 154 CANADA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 155 CANADA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 156 CANADA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 157 CANADA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 158 CANADA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.4 EUROPE

- FIGURE 45 EUROPE: AIRCRAFT SEATING MARKET SNAPSHOT

- 12.4.1 RECESSION IMPACT ANALYSIS

- 12.4.2 PESTLE ANALYSIS

- TABLE 159 EUROPE: AIRCRAFT SEATING OEM MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 160 EUROPE: AIRCRAFT SEATING OEM MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 161 EUROPE: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 162 EUROPE: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 163 EUROPE: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 164 EUROPE: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 165 EUROPE: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 166 EUROPE: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 167 EUROPE: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 168 EUROPE: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 169 EUROPE: AIRCRAFT SEATING MRO MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 170 EUROPE: AIRCRAFT SEATING MRO MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 171 EUROPE: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 172 EUROPE: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 173 EUROPE: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 174 EUROPE: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 175 EUROPE: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 176 EUROPE: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 177 EUROPE: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 178 EUROPE: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 179 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 180 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 181 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 182 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 183 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 184 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 185 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 186 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 187 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 188 EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.4.3 UK

- 12.4.3.1 Innovations in seat design to drive growth

- TABLE 189 UK: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 190 UK: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 191 UK: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 192 UK: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 193 UK: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 194 UK: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 195 UK: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 196 UK: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 197 UK: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 198 UK: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 199 UK: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 200 UK: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 201 UK: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 202 UK: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 203 UK: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 204 UK: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.4.4 FRANCE

- 12.4.4.1 Rising demand for lightweight seats to drive growth

- TABLE 205 FRANCE: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 206 FRANCE: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 207 FRANCE: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 208 FRANCE: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 209 FRANCE: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 210 FRANCE: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 211 FRANCE: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 212 FRANCE: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 213 FRANCE: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 214 FRANCE: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 215 FRANCE: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 216 FRANCE: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 217 FRANCE: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 218 FRANCE: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 219 FRANCE: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 220 FRANCE: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 221 FRANCE: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 222 FRANCE: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 223 FRANCE: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 224 FRANCE: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 225 FRANCE: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 226 FRANCE: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 227 FRANCE: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 228 FRANCE: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.4.5 GERMANY

- 12.4.5.1 Need for improved passenger comfort on long-haul flights to drive growth

- TABLE 229 GERMANY: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 230 GERMANY: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 231 GERMANY: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 232 GERMANY: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 233 GERMANY: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 234 GERMANY: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 235 GERMANY: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 236 GERMANY: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 237 GERMANY: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 238 GERMANY: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 239 GERMANY: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 240 GERMANY: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 241 GERMANY: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 242 GERMANY: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 243 GERMANY: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 244 GERMANY: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 245 GERMANY: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 246 GERMANY: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 247 GERMANY: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 248 GERMANY: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 249 GERMANY: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 250 GERMANY: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 251 GERMANY: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 252 GERMANY: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.4.6 ITALY

- 12.4.6.1 Emphasis on regular cabin upgrades to drive growth

- TABLE 253 ITALY: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 254 ITALY: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 255 ITALY: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 256 ITALY: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 257 ITALY: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 258 ITALY: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 259 ITALY: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 260 ITALY: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 261 ITALY: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 262 ITALY: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 263 ITALY: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 264 ITALY: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 265 ITALY: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 266 ITALY: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 267 ITALY: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 268 ITALY: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 269 ITALY: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 270 ITALY: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 271 ITALY: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 272 ITALY: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 273 ITALY: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 274 ITALY: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 275 ITALY: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 276 ITALY: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.4.7 RUSSIA

- 12.4.7.1 Surge in aircraft operations to drive growth

- TABLE 277 RUSSIA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 278 RUSSIA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 279 RUSSIA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 280 RUSSIA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 281 RUSSIA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 282 RUSSIA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 283 RUSSIA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 284 RUSSIA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 285 RUSSIA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 286 RUSSIA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 287 RUSSIA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 288 RUSSIA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 289 RUSSIA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 290 RUSSIA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 291 RUSSIA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 292 RUSSIA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.4.8 REST OF EUROPE

- TABLE 293 REST OF EUROPE: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 294 REST OF EUROPE: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 295 REST OF EUROPE: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 296 REST OF EUROPE: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 297 REST OF EUROPE: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 298 REST OF EUROPE: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 299 REST OF EUROPE: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 300 REST OF EUROPE: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 301 REST OF EUROPE: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 302 REST OF EUROPE: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 303 REST OF EUROPE: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 304 REST OF EUROPE: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 305 REST OF EUROPE: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 306 REST OF EUROPE: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 307 REST OF EUROPE: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 308 REST OF EUROPE: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 309 REST OF EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 310 REST OF EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 311 REST OF EUROPE: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 312 REST OF EUROPE: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 313 REST OF EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 314 REST OF EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 315 REST OF EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 316 REST OF EUROPE: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.5 ASIA PACIFIC

- FIGURE 46 ASIA PACIFIC: AIRCRAFT SEATING MARKET SNAPSHOT

- 12.5.1 RECESSION IMPACT ANALYSIS

- 12.5.2 PESTLE ANALYSIS

- TABLE 317 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 318 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 319 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 320 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 321 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 322 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 323 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 324 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 325 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 326 ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 327 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 328 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 329 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 330 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 331 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 332 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 333 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 334 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 335 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 336 ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 337 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 338 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 339 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 340 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 341 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 342 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 343 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 344 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 345 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 346 ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.5.3 CHINA

- 12.5.3.1 Rapid adoption of lightweight aircraft to drive growth

- TABLE 347 CHINA: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 348 CHINA: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 349 CHINA: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 350 CHINA: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 351 CHINA: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 352 CHINA: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 353 CHINA: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 354 CHINA: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 355 CHINA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 356 CHINA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 357 CHINA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 358 CHINA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 359 CHINA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 360 CHINA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 361 CHINA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 362 CHINA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 363 CHINA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 364 CHINA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 365 CHINA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 366 CHINA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 367 CHINA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 368 CHINA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 369 CHINA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 370 CHINA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.5.4 INDIA

- 12.5.4.1 Expanding passenger travel to drive growth

- TABLE 371 INDIA: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 372 INDIA: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 373 INDIA: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 374 INDIA: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 375 INDIA: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 376 INDIA: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 377 INDIA: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 378 INDIA: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 379 INDIA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 380 INDIA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 381 INDIA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 382 INDIA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 383 INDIA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 384 INDIA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 385 INDIA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 386 INDIA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 387 INDIA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 388 INDIA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 389 INDIA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 390 INDIA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 391 INDIA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 392 INDIA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 393 INDIA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 394 INDIA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.5.5 JAPAN

- 12.5.5.1 Availability of low-cost raw materials to drive growth

- TABLE 395 JAPAN: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 396 JAPAN: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 397 JAPAN: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 398 JAPAN: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 399 JAPAN: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 400 JAPAN: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 401 JAPAN: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 402 JAPAN: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 403 JAPAN: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 404 JAPAN: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 405 JAPAN: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 406 JAPAN: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 407 JAPAN: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 408 JAPAN: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 409 JAPAN: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 410 JAPAN: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 411 JAPAN: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 412 JAPAN: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 413 JAPAN: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 414 JAPAN: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 415 JAPAN: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 416 JAPAN: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 417 JAPAN: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 418 JAPAN: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.5.6 SOUTH KOREA

- 12.5.6.1 Ongoing replacement of aging aircraft to drive growth

- TABLE 419 SOUTH KOREA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 420 SOUTH KOREA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 421 SOUTH KOREA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 422 SOUTH KOREA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 423 SOUTH KOREA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 424 SOUTH KOREA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 425 SOUTH KOREA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 426 SOUTH KOREA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 427 SOUTH KOREA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 428 SOUTH KOREA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 429 SOUTH KOREA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 430 SOUTH KOREA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 431 SOUTH KOREA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 432 SOUTH KOREA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 433 SOUTH KOREA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 434 SOUTH KOREA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.5.7 AUSTRALIA

- 12.5.7.1 Procurement of new aircraft to meet domestic demand to drive growth

- TABLE 435 AUSTRALIA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 436 AUSTRALIA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 437 AUSTRALIA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 438 AUSTRALIA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 439 AUSTRALIA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 440 AUSTRALIA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 441 AUSTRALIA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 442 AUSTRALIA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 443 AUSTRALIA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 444 AUSTRALIA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 445 AUSTRALIA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 446 AUSTRALIA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 447 AUSTRALIA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 448 AUSTRALIA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 449 AUSTRALIA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 450 AUSTRALIA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.5.8 REST OF ASIA PACIFIC

- TABLE 451 REST OF ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 452 REST OF ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 453 REST OF ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 454 REST OF ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 455 REST OF ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 456 REST OF ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 457 REST OF ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 458 REST OF ASIA PACIFIC: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 459 REST OF ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 460 REST OF ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 461 REST OF ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 462 REST OF ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 463 REST OF ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 464 REST OF ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 465 REST OF ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 466 REST OF ASIA PACIFIC: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 467 REST OF ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 468 REST OF ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 469 REST OF ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 470 REST OF ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 471 REST OF ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 472 REST OF ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 473 REST OF ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 474 REST OF ASIA PACIFIC: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.6 MIDDLE EAST

- 12.6.1 RECESSION IMPACT ANALYSIS

- 12.6.2 PESTLE ANALYSIS

- FIGURE 47 MIDDLE EAST: AIRCRAFT SEATING MARKET SNAPSHOT

- TABLE 475 MIDDLE EAST: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 476 MIDDLE EAST: AIRCRAFT SEATING OEM MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 477 MIDDLE EAST: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 478 MIDDLE EAST: AIRCRAFT SEATING OEM MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 479 MIDDLE EAST: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 480 MIDDLE EAST: AIRCRAFT SEATING OEM MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 481 MIDDLE EAST: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 482 MIDDLE EAST: AIRCRAFT SEATING OEM MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 483 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 484 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 485 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 486 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 487 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 488 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 489 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 490 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 491 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 492 MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 493 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 494 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 495 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 496 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 497 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 498 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 499 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 500 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 501 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 502 MIDDLE EAST: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.6.3 GULF COOPERATION COUNCIL (GCC)

- 12.6.3.1 UAE

- 12.6.3.1.1 Surge in year-round air passenger traffic to drive growth

- 12.6.3.1 UAE

- TABLE 503 UAE: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 504 UAE: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 505 UAE: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 506 UAE: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 507 UAE: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 508 UAE: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 509 UAE: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 510 UAE: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 511 UAE: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 512 UAE: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 513 UAE: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 514 UAE: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 515 UAE: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 516 UAE: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 517 UAE: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 518 UAE: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.6.3.2 Saudi Arabia

- 12.6.3.2.1 Vision 2030 program to drive growth

- 12.6.3.2 Saudi Arabia

- TABLE 519 SAUDI ARABIA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 520 SAUDI ARABIA: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 521 SAUDI ARABIA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 522 SAUDI ARABIA: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 523 SAUDI ARABIA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 524 SAUDI ARABIA: AIRCRAFT SEATING MRO MARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 525 SAUDI ARABIA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 526 SAUDI ARABIA: AIRCRAFT SEATING MRO MARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 527 SAUDI ARABIA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 528 SAUDI ARABIA: AIRCRAFT SEATING AFTERMARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 529 SAUDI ARABIA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 530 SAUDI ARABIA: AIRCRAFT SEATING AFTERMARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 531 SAUDI ARABIA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 532 SAUDI ARABIA: AIRCRAFT SEATING AFTERMARKET, BY PASSENGER SEAT TYPE, 2024-2029 (USD MILLION)

- TABLE 533 SAUDI ARABIA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 534 SAUDI ARABIA: AIRCRAFT SEATING AFTERMARKET, BY PILOT & CREW SEAT TYPE, 2024-2029 (USD MILLION)

- 12.6.4 REST OF MIDDLE EAST

- TABLE 535 REST OF MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 536 REST OF MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 537 REST OF MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2020-2023 (USD MILLION)

- TABLE 538 REST OF MIDDLE EAST: AIRCRAFT SEATING MRO MARKET, BY SEAT TYPE, 2024-2029 (USD MILLION)