バルブポジショナーの世界市場:作動型別、業界別、タイプ別、地域別 - 2030年までの予測

Valve Positioner Market by Type (Pneumatic Positioners, Electro-pneumatic Positioners, Digital Positioners), Actuation (Single Acting Positioners, Double Acting Positioners), Industry (Oil & Gas, Energy & Power) and Region - Global Forecast to 2030- 発行日

- ページ情報

- 英文 218 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1795417

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

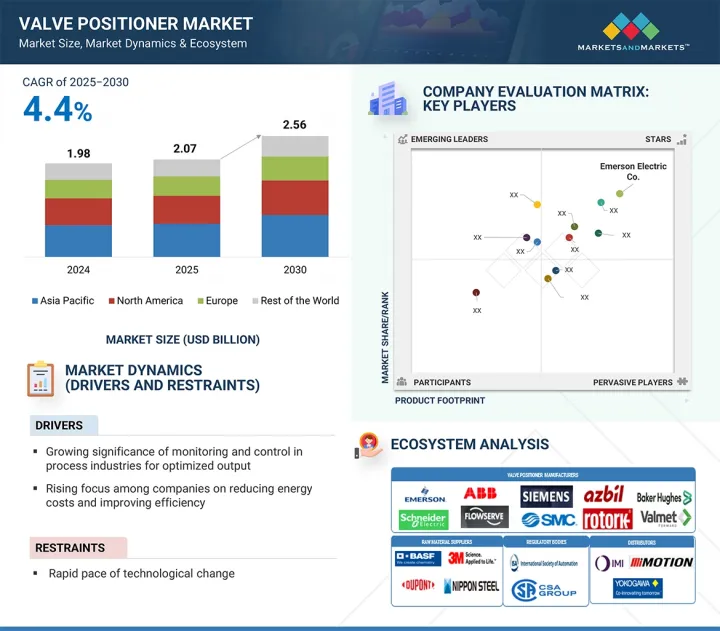

世界のバルブポジショナーの市場規模は、4.4%のCAGRで拡大し、2025年の20億7,000万米ドルから2030年には25億6,000万米ドルに成長すると予測されています。

成長の原動力となるのは、精密制御、フロープロセスの自動化、産業オペレーション全体のインテリジェントバルブ管理へのシフトに対するニーズの高まりです。産業界は、プロセスの応答性を最適化し、バルブに関連する故障を減らし、厳しい品質基準を満たすことを目指しているため、バルブポジショナーは、変動する運転条件下で一貫した性能を達成するための重要なコンポーネントになってきています。金属・鉱業、化学処理、製薬、発電などの業界では、圧力に敏感でミッションクリティカルなアプリケーションを確実に制御するために、先進的なバルブポジショナーの使用を拡大しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント別 | 作動型別、業界別、タイプ別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

さらに、頻繁にバッチが変更され、フローが変化する製造環境では、スループットを向上させ、無駄を削減するためにポジショナーが採用されています。スマート計装ネットワーク、状態監視システム、プラント制御アーキテクチャとの統合は、運用の柔軟性を高め、手動介入を減らします。適応制御、遠隔性能最適化、ライフサイクル効率化の需要が高まるにつれ、バルブポジショナーは、世界のセクターで次世代産業オートメーション戦略を可能にする役割を果たすようになると予想されます。

バルブポジショナー市場は、安全性、信頼性、エネルギー効率を優先する重要なプロセス産業での採用が拡大していることから、単動式セグメントが予測期間中に最大のシェアを占めると予測されています。石油・ガス、水・廃水処理、化学処理などの業界では、フェイルセーフ機能(空気に異常が発生した場合にバルブを所定の位置(開または閉)に自動的に戻す機能)により、単動式アクチュエータを選択するケースが増えています。この機能により、操作の安全性が確保され、危険の多い環境におけるリスクを最小限に抑えることができます。デジタルバルブポジショナーと単動アクチュエーターの統合は、精密制御、リアルタイム診断、予知保全を可能にし、このセグメントの優位性をさらに強めています。これらの利点は、システム性能を向上させるだけでなく、ダウンタイムとメンテナンスコストを削減します。さらに、単動式アクチュエーターは空気消費量が少なく、設置が容易なため、シンプルさと信頼性が不可欠な遠隔地や危険な場所に適しています。産業界が業務の合理化を図り、持続可能性の目標に沿うことを目指している中、単動アクチュエータは、コンプライアンスと業務継続性をサポートする堅牢でコスト効率の高いソリューションを提供し、市場における主導的地位を強化しています。

エネルギー・電力セクターは、発電・配電における効率的な流量制御とシステム信頼性の向上に対する需要の高まりに支えられ、2024年のバルブポジショナー市場において第2位のシェアを確保しました。世界のエネルギー消費量の増加と電力網の複雑化に伴い、電力会社は、火力、原子力、再生可能エネルギー発電所の蒸気、ガス、冷却システムの制御を最適化するために、先進的なバルブポジショナーを導入するケースが増えています。最新の電力施設は、より緊密な制御ループを可能にし、機器への機械的ストレスを軽減し、負荷管理を改善するために、スマートバルブポジショナーを採用しています。バイオマス、太陽熱、地熱などの再生可能エネルギー源への移行は、正確な流量調節の必要性をさらに強め、バルブポジショナーをプロセスの安定性と効率を確保するための重要なコンポーネントにしています。さらに、老朽化した電力インフラをアップグレードし、新たな発電能力を追加するための継続的な取り組みが世界中で進んでいることも、こうしたソリューションの採用を後押ししています。バルブポジショナーはまた、排ガス規制をサポートし、厳しいエネルギー効率規制を満たすのに役立ち、進化するエネルギー情勢において不可欠な技術としての役割を強化しています。

アジア太平洋は、バルブポジショナー市場において最も急成長している地域であり、予測期間中に最も高いCAGRを記録すると予測されています。この急成長の背景には、工業化の拡大、インフラ開発、石油・ガス、化学、上下水道処理、発電などの主要部門における自動化技術の採用拡大があります。中国、インド、韓国、東南アジア諸国などの国々は、生産性を高め、国内および輸出需要の増加に対応するため、製造業やプロセス産業の近代化に多額の投資を行っています。この地域ではインダストリー4.0とスマート・マニュファクチャリングを推進しており、精密制御、遠隔診断、システム統合などの利点を提供するデジタルバルブポジショナーの導入が加速しています。さらに、クリーンエネルギー、効率的な水管理、産業オートメーションを支援する政府の取り組みが、市場拡大に有利な環境を作り出しています。老朽化したインフラをアップグレードし、より厳しい環境規制を満たす必要性が、高度なバルブ制御ソリューションの需要をさらに促進しています。エネルギー効率、持続可能性、運転信頼性への注目が高まる中、アジア太平洋地域はバルブポジショナー採用の重要な拠点として台頭しており、最もダイナミックで急速に発展している地域市場としての地位を牽引しています。

当レポートでは、世界のバルブポジショナー市場について調査し、作動型別、業界別、タイプ別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 顧客ビジネスに影響を与える動向/混乱

- 技術分析

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- ケーススタディ

- 貿易分析

- 特許分析

- 2025年~2026年の主な会議とイベント

- 基準と規制

- AI/生成AIがバルブポジショナー市場に与える影響

- 2025年の米国関税がバルブポジショナー市場に与える影響

第6章 バルブポジショナー市場(作動型別)

- イントロダクション

- 単動式

- 複動式

第7章 バルブポジショナー市場(業界別)

- イントロダクション

- 石油・ガス

- 水・廃水処理

- エネルギー・電力

- 化学薬品

- 紙・パルプ

- 医薬品

- 金属・鉱業

- 食品・飲料

- その他

第8章 バルブポジショナー市場(タイプ別)

- イントロダクション

- 空気圧ポジショナー

- 電空ポジショナー

- デジタルポジショナー

第9章 バルブポジショナー市場(地域別)

- イントロダクション

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- その他

- アジア太平洋

- 中国

- 日本

- インド

- その他

- その他の地域

- 中東・アフリカ

- 南米

第10章 競合情勢

- 概要

- 主要参入企業の戦略/強み、2023年~2025年

- 収益分析、2020年~2024年

- 市場シェア分析、2024年

- 競争評価マトリックス:主要参入企業の評価、2024年

- 競争評価マトリックス:スタートアップ/中小企業の評価、2024年

- 競合シナリオ

第11章 企業プロファイル

- 主要参入企業

- EMERSON ELECTRIC CO.

- ABB

- FLOWSERVE CORPORATION

- SIEMENS

- SCHNEIDER ELECTRIC

- SMC CORPORATION

- AZBIL CORPORATION

- BAKER HUGHES

- ROTORK PLC

- VALMET

- その他の企業

- SAMSONCONTROLS.NET.

- VRG CONTROLS, LLC

- FESTO SE & CO. KG(FESTO)

- BADGER METER, INC.

- CONTROLAIR

- CRANE COMPANY

- CHRISTIAN BURKERT GMBH & CO. KG

- GEMU GROUP

- DWYER INSTRUMENTS LTD

- VRC

- POWER-GENEX LTD.

- VAL CONTROLS

- BRAY INTERNATIONAL

- NIHON KOSO CO., LTD.

- SPIRAX SARCO LIMITED

第12章 付録

図表

List of Tables

- TABLE 1 VALVE POSITIONER MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 ROLE OF PLAYERS IN VALVE POSITIONER ECOSYSTEM

- TABLE 3 AVERAGE SELLING PRICES OF VALVE POSITIONERS, 2024

- TABLE 4 AVERAGE SELLING PRICE OF DIFFERENT TYPES OF VALVE POSITIONERS OFFERED BY KEY PLAYERS, 2024 (USD)

- TABLE 5 VALVE POSITIONER MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 6 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE INDUSTRIES (%)

- TABLE 7 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- TABLE 8 MITSUBISHI CHEMICAL CORPORATION USED CLOUD-BASED SERVICES WITH SMART VALVE POSITIONERS TO IMPROVE PLANT OPERATION

- TABLE 9 SIEMENS AG USED PS2 DIGITAL VALVE POSITIONER ON FEEDWATER VALVE AND STARTUP VALVE IN POWER PLANT THAT PROVIDED ACCURATE FEEDBACK INDICATION TO CONTROL ROOM

- TABLE 10 AZBIL CORPORATION IMPLEMENTED COMMUNICATION CAPABLE SVP3000 ALPHPLUS DIGITAL POSITIONERS THAT REDUCED MAINTENANCE WORKLOAD OF EASTERN PETROCHEMICAL COMPANY

- TABLE 11 IMPORT DATA FOR HS CODE 8481-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 12 EXPORT DATA FOR HS CODE 8481-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 13 LIST OF KEY PATENTS, 2024

- TABLE 14 VALVE POSITIONER MARKET: LIST OF CONFERENCES AND EVENTS, 2025-2026

- TABLE 15 STANDARDS FOR VALVE POSITIONERS

- TABLE 16 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 19 ROW: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 20 US-ADJUSTED RECIPROCAL TARIFF RATES, 2024 (USD BILLION)

- TABLE 21 KEY PRODUCT-RELATED TARIFF EFFECTIVE FOR VALVE POSITIONER MARKET, 2024

- TABLE 22 VALVE POSITIONER MARKET, BY ACTUATION, 2021-2024 (USD MILLION)

- TABLE 23 VALVE POSITIONER MARKET, BY ACTUATION, 2025-2030 (USD MILLION)

- TABLE 24 VALVE POSITIONER MARKET, BY INDUSTRY, 2021-2024 (USD MILLION)

- TABLE 25 VALVE POSITIONER MARKET, BY INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 26 OIL & GAS: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 27 OIL & GAS: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 28 OIL & GAS: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 29 OIL & GAS: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 30 OIL & GAS: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 31 OIL & GAS: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 32 OIL & GAS: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 33 OIL & GAS: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 34 OIL & GAS: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 35 OIL & GAS: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 36 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 37 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 38 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 39 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 40 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 41 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 42 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 43 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 44 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 45 WATER & WASTEWATER TREATMENT: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 46 ENERGY & POWER: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 47 ENERGY & POWER: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 48 ENERGY & POWER: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 49 ENERGY & POWER: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 50 ENERGY & POWER: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 51 ENERGY & POWER: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 52 ENERGY & POWER: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 53 ENERGY & POWER: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 54 ENERGY & POWER: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 55 ENERGY & POWER: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 56 CHEMICALS: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 57 CHEMICALS: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 58 CHEMICALS: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 59 CHEMICALS: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 60 CHEMICALS: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 61 CHEMICALS: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 62 CHEMICALS: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 63 CHEMICALS: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 64 CHEMICALS: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 65 CHEMICALS: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 66 PAPER & PULP: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 67 PAPER & PULP: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 68 PAPER & PULP: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 69 PAPER & PULP: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 70 PAPER & PULP: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 71 PAPER & PULP: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 72 PAPER & PULP: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 73 PAPER & PULP: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 74 PAPER & PULP: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 75 PAPER & PULP: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 76 PHARMACEUTICALS: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 77 PHARMACEUTICALS: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 78 PHARMACEUTICALS: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 79 PHARMACEUTICALS: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 80 PHARMACEUTICALS: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 81 PHARMACEUTICALS: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 82 PHARMACEUTICALS: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 83 PHARMACEUTICALS: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 84 PHARMACEUTICALS: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 85 PHARMACEUTICALS: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 86 METALS & MINING: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 87 METALS & MINING: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 88 METALS & MINING: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 89 METALS & MINING: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 90 METALS & MINING: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 91 METALS & MINING: VALVE POSITIONER MARKET IN EUROPE, 2025-2030 (USD MILLION)

- TABLE 92 METALS & MINING: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 93 METALS & MINING: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 94 METALS & MINING: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 95 METALS & MINING: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 96 FOOD & BEVERAGES: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 97 FOOD & BEVERAGES: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 98 FOOD & BEVERAGES: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 99 FOOD & BEVERAGES: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 100 FOOD & BEVERAGES: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 101 FOOD & BEVERAGES: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 102 FOOD & BEVERAGES: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 103 FOOD & BEVERAGES: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 104 FOOD & BEVERAGES: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 105 FOOD & BEVERAGES: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 106 OTHER INDUSTRIES: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 107 OTHER INDUSTRIES: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 108 OTHER INDUSTRIES: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 109 OTHER INDUSTRIES: VALVE POSITIONER MARKET IN NORTH AMERICA, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 110 OTHER INDUSTRIES: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 111 OTHER INDUSTRIES: VALVE POSITIONER MARKET IN EUROPE, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 112 OTHER INDUSTRIES: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 113 OTHER INDUSTRIES: VALVE POSITIONER MARKET IN ASIA PACIFIC, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 114 OTHER INDUSTRIES: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 115 OTHER INDUSTRIES: VALVE POSITIONER MARKET IN ROW, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 116 VALVE POSITIONER MARKET, BY TYPE, 2021-2024 (USD MILLION)

- TABLE 117 VALVE POSITIONER MARKET, BY TYPE, 2025-2030 (USD MILLION)

- TABLE 118 VALVE POSITIONER MARKET, BY TYPE, 2021-2024 (THOUSAND UNITS)

- TABLE 119 VALVE POSITIONER MARKET, BY TYPE, 2025-2030 (THOUSAND UNITS)

- TABLE 120 VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 121 VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 122 NORTH AMERICA: VALVE POSITIONER MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 123 NORTH AMERICA: VALVE POSITIONER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 124 NORTH AMERICA: VALVE POSITIONER MARKET, BY INDUSTRY, 2021-2024 (USD MILLION)

- TABLE 125 NORTH AMERICA: VALVE POSITIONER MARKET, BY INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 126 EUROPE: VALVE POSITIONER MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 127 EUROPE: VALVE POSITIONER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 128 EUROPE: VALVE POSITIONER MARKET, BY INDUSTRY, 2021-2024 (USD MILLION)

- TABLE 129 EUROPE: VALVE POSITIONER MARKET, BY INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 130 ASIA PACIFIC: VALVE POSITIONER MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 131 ASIA PACIFIC: VALVE POSITIONER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 132 ASIA PACIFIC: VALVE POSITIONER MARKET, BY INDUSTRY, 2021-2024 (USD MILLION)

- TABLE 133 ASIA PACIFIC: VALVE POSITIONER MARKET, BY INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 134 ROW: VALVE POSITIONER MARKET, BY REGION, 2021-2024 (USD MILLION)

- TABLE 135 ROW: VALVE POSITIONER MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 136 ROW: VALVE POSITIONER MARKET, BY INDUSTRY, 2021-2024 (USD MILLION)

- TABLE 137 ROW: VALVE POSITIONER MARKET, BY INDUSTRY, 2025-2030 (USD MILLION)

- TABLE 138 MIDDLE EAST & AFRICA: VALVE POSITIONER MARKET, BY GEOGRAPHY, 2021-2024 (USD MILLION)

- TABLE 139 MIDDLE EAST & AFRICA: VALVE POSITIONER MARKET, BY GEOGRAPHY, 2025-2030 (USD MILLION)

- TABLE 140 SOUTH AMERICA: VALVE POSITIONER MARKET, BY COUNTRY, 2021-2024 (USD MILLION)

- TABLE 141 SOUTH AMERICA: VALVE POSITIONER MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 142 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, JANUARY 2023-JULY 2025

- TABLE 143 VALVE POSITIONER MARKET SHARE ANALYSIS, 2024

- TABLE 144 VALVE POSITIONER MARKET: REGION FOOTPRINT

- TABLE 145 VALVE POSITIONER MARKET: TYPE FOOTPRINT

- TABLE 146 VALVE POSITIONER MARKET: INDUSTRY FOOTPRINT

- TABLE 147 VALVE POSITIONER MARKET: LIST OF KEY STARTUPS/SMES, 2024

- TABLE 148 VALVE POSITIONER MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES, 2024

- TABLE 149 VALVE POSITIONER MARKET: DEALS, JANUARY 2023-JULY 2025

- TABLE 150 VALVE POSITIONER MARKET: EXPANSIONS, JANUARY 2023-JULY 2025

- TABLE 151 VALVE POSITIONER MARKET: DEVELOPMENTS, JANUARY 2023-JULY 2025

- TABLE 152 EMERSON ELECTRIC CO.: COMPANY OVERVIEW

- TABLE 153 EMERSON ELECTRIC CO.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 154 EMERSON ELECTRIC CO.: DEALS

- TABLE 155 ABB: COMPANY OVERVIEW

- TABLE 156 ABB: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 157 FLOWSERVE CORPORATION: COMPANY OVERVIEW

- TABLE 158 FLOWSERVE CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 159 FLOWSERVE CORPORATION: DEVELOPMENTS

- TABLE 160 SIEMENS: COMPANY OVERVIEW

- TABLE 161 SIEMENS: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 162 SCHNEIDER ELECTRIC: COMPANY OVERVIEW

- TABLE 163 SCHNEIDER ELECTRIC: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 164 SMC CORPORATION: COMPANY OVERVIEW

- TABLE 165 SMC CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 166 AZBIL CORPORATION: COMPANY OVERVIEW

- TABLE 167 AZBIL CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 168 AZBIL CORPORATION: EXPANSIONS

- TABLE 169 BAKER HUGHES: COMPANY OVERVIEW

- TABLE 170 BAKER HUGHES: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 171 ROTORK PLC: COMPANY OVERVIEW

- TABLE 172 ROTORK PLC: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 173 ROTORK PLC: DEALS

- TABLE 174 VALMET: COMPANY OVERVIEW

- TABLE 175 VALMET: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 176 SAMSONCONTROLS.NET.: COMPANY OVERVIEW

- TABLE 177 VRG CONTROLS LLC: COMPANY OVERVIEW

- TABLE 178 FESTO SE & CO. KG (FESTO): COMPANY OVERVIEW

- TABLE 179 BADGER METER, INC.: COMPANY OVERVIEW

- TABLE 180 CONTROLAIR: COMPANY OVERVIEW

- TABLE 181 CRANE COMPANY: COMPANY OVERVIEW

- TABLE 182 CHRISTIAN BURKERT GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 183 GEMU GROUP: COMPANY OVERVIEW

- TABLE 184 DWYER INSTRUMENTS LTD: COMPANY OVERVIEW

- TABLE 185 VRC: COMPANY OVERVIEW

- TABLE 186 POWER-GENEX LTD.: COMPANY OVERVIEW

- TABLE 187 VAL CONTROLS: COMPANY OVERVIEW

- TABLE 188 BRAY INTERNATIONAL: COMPANY OVERVIEW

- TABLE 189 NIHON KOSO CO., LTD.: COMPANY OVERVIEW

- TABLE 190 SPIRAX SARCO LIMITED: COMPANY OVERVIEW

List of Figures

- FIGURE 1 VALVE POSITIONER MARKET AND REGIONAL SEGMENTATION

- FIGURE 2 VALVE POSITIONER MARKET: RESEARCH DESIGN

- FIGURE 3 VALVE POSITIONER MARKET: RESEARCH APPROACH

- FIGURE 4 VALVE POSITIONER MARKET: BOTTOM-UP APPROACH

- FIGURE 5 VALVE POSITIONER MARKET: TOP-DOWN APPROACH

- FIGURE 6 VALVE POSITIONER MARKET SIZE ESTIMATION METHODOLOGY

- FIGURE 7 DATA TRIANGULATION

- FIGURE 8 DIGITAL VALVE POSITIONER TO HOLD MAXIMUM MARKET SHARE IN 2025

- FIGURE 9 SINGLE-ACTING POSITIONERS TO ACCOUNT FOR LARGER MARKET SHARE IN 2030

- FIGURE 10 WATER & WASTEWATER TREATMENT INDUSTRY TO CAPTURE LARGEST MARKET SHARE IN 2030

- FIGURE 11 ASIA PACIFIC ACCOUNTED FOR LARGEST MARKET SHARE IN 2024

- FIGURE 12 RISING ADOPTION OF SMART VALVE POSITIONERS IN VARIOUS PLANT OPERATIONS IN PROCESS INDUSTRIES TO BOOST MARKET GROWTH

- FIGURE 13 DIGITAL POSITIONERS TO HOLD LARGEST MARKET SIZE IN 2030

- FIGURE 14 SINGLE-ACTING POSITIONERS TO SECURE LARGER MARKET SHARE IN 2030

- FIGURE 15 OIL & GAS TO DOMINATE MARKET IN 2030

- FIGURE 16 INDIA TO EXHIBIT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 17 VALVE POSITIONER MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 18 VALVE POSITIONER MARKET: IMPACT ANALYSIS OF DRIVERS

- FIGURE 19 VALVE POSITIONER MARKET: IMPACT ANALYSIS OF RESTRAINTS

- FIGURE 20 VALVE POSITIONER MARKET: IMPACT ANALYSIS OF OPPORTUNITIES

- FIGURE 21 VALVE POSITIONER MARKET: IMPACT ANALYSIS OF CHALLENGES

- FIGURE 22 VALUE CHAIN ANALYSIS: MAJOR VALUE ADDED BY ORIGINAL EQUIPMENT MANUFACTURERS

- FIGURE 23 VALVE POSITIONER ECOSYSTEM ANALYSIS

- FIGURE 24 AVERAGE SELLING PRICE OF DIFFERENT TYPES OF VALVE POSITIONERS, BY KEY PLAYER, 2024

- FIGURE 25 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 26 VALVE POSITIONER MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE INDUSTRIES

- FIGURE 28 KEY BUYING CRITERIA FOR TOP THREE INDUSTRIES

- FIGURE 29 IMPORT DATA FOR HS CODE 8481-COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024

- FIGURE 30 EXPORT DATA FOR HS CODE 8481 -COMPLIANT PRODUCTS, BY COUNTRY, 2020-2024

- FIGURE 31 PATENTS APPLIED AND GRANTED, 2015-2024

- FIGURE 32 KEY AI USE CASES IN VALVE POSITIONER MARKET

- FIGURE 33 SINGLE-ACTING SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 34 SCHEMATIC OF SINGLE-ACTING POSITIONERS

- FIGURE 35 SCHEMATIC OF DOUBLE-ACTING POSITIONERS

- FIGURE 36 VALVE POSITIONER MARKET, BY INDUSTRY

- FIGURE 37 WATER & WASTEWATER TREATMENT INDUSTRY TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 38 DIGITAL POSITIONERS TO GROW AT FASTEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 39 WORKING PRINCIPLE OF PNEUMATIC POSITIONERS

- FIGURE 40 SALIENT FEATURES OF ELECTRO-PNEUMATIC POSITIONER

- FIGURE 41 ADVANTAGES OF DIGITAL POSITIONERS

- FIGURE 42 VALVE POSITIONER MARKET, BY REGION

- FIGURE 43 ASIA PACIFIC TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 44 INDIA TO OFFER MOST LUCRATIVE OPPORTUNITIES DURING FORECAST PERIOD

- FIGURE 45 NORTH AMERICA: VALVE POSITIONER MARKET SNAPSHOT

- FIGURE 46 EUROPE: VALVE POSITIONER MARKET SNAPSHOT

- FIGURE 47 ASIA PACIFIC: VALVE POSITIONER MARKET SNAPSHOT

- FIGURE 48 VALVE POSITIONER MARKET: REVENUE ANALYSIS OF FIVE KEY PLAYERS, 2020-2024

- FIGURE 49 MARKET SHARE ANALYSIS OF COMPANIES OFFERING VALVE PPOSITIONERS, 2024

- FIGURE 50 VALVE POSITIONER MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 51 VALVE POSITIONER MARKET: COMPANY FOOTPRINT

- FIGURE 52 VALVE POSITIONER MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SME), 2024

- FIGURE 53 EMERSON ELECTRIC CO.: COMPANY SNAPSHOT

- FIGURE 54 ABB: COMPANY SNAPSHOT

- FIGURE 55 FLOWSERVE CORPORATION: COMPANY SNAPSHOT

- FIGURE 56 SIEMENS: COMPANY SNAPSHOT

- FIGURE 57 SCHNEIDER ELECTRIC: COMPANY SNAPSHOT

- FIGURE 58 SMC CORPORATION: COMPANY SNAPSHOT

- FIGURE 59 AZBIL CORPORATION: COMPANY SNAPSHOT

- FIGURE 60 BAKER HUGHES: COMPANY SNAPSHOT

- FIGURE 61 ROTORK PLC: COMPANY SNAPSHOT

- FIGURE 62 VALMET: COMPANY SNAPSHOT

目次

With a CAGR of 4.4%, the global valve positioner market is projected to grow from USD 2.07 billion in 2025 to USD 2.56 billion by 2030. Growth is expected to be driven by the increasing need for precision control, automation of flow processes, and the shift toward intelligent valve management across industrial operations. As industries aim to optimize process responsiveness, reduce valve-related failures, and meet stringent quality standards, valve positioners are becoming critical components in achieving consistent performance under variable operating conditions. Industries such as metals and mining, chemical processing, pharmaceuticals, and power generation are expanding the use of advanced valve positioners to ensure tight control in pressure-sensitive and mission-critical applications.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | Value (USD Billion) |

| Segments | By Type, Actuation, Industry, and Region |

| Regions covered | North America, Europe, APAC, RoW |

Additionally, manufacturing environments with frequent batch changes and variable flows adopt positioners to improve throughput and reduce waste. Integration with smart instrumentation networks, condition monitoring systems, and plant control architectures enhances operational flexibility and reduces manual intervention. As the demand for adaptive control, remote performance optimization, and lifecycle efficiency increases, valve positioners are expected to play a growing role in enabling next-generation industrial automation strategies across global sectors.

By actuation type, the single-acting segment is expected to hold the largest market share during the forecast period.

The single-acting actuation segment is projected to hold the largest share of the valve positioner market during the forecast period, driven by its growing adoption in critical process industries that prioritize safety, reliability, and energy efficiency. Industries such as oil & gas, water & wastewater treatment, and chemical processing are increasingly selecting single-acting actuators due to their fail-safe capability-automatically returning the valve to a predetermined position (open or closed) in the event of air failure. This functionality ensures operational security and minimizes risks in high-stakes environments. The integration of digital valve positioners with single-acting actuators is further strengthening the segment's dominance, enabling precise control, real-time diagnostics, and predictive maintenance. These benefits not only enhance system performance but also reduce downtime and maintenance costs. Moreover, single-acting actuators consume less air and are easier to install, making them well-suited for remote or hazardous locations where simplicity and reliability are essential. As industries aim to streamline operations and align with sustainability goals, single-acting actuation offers a robust, cost-effective solution that supports compliance and operational continuity, reinforcing its leading position in the market.

Industry

By industry, the energy and power sector is likely to hold the second-largest market share during the forecast period.

The energy and power sector secured the second-largest share in the valve positioner market during 2024, supported by the growing demand for efficient flow control and enhanced system reliability in power generation and distribution. As global energy consumption rises and power grids become more complex, utilities are increasingly implementing advanced valve positioners to optimize control over steam, gas, and cooling systems in thermal, nuclear, and renewable energy plants. Modern power facilities are adopting smart valve positioners to enable tighter control loops, reduce mechanical stress on equipment, and improve load management. The transition toward renewable energy sources-such as biomass, solar thermal, and geothermal-further strengthens the need for accurate flow regulation, making valve positioners a critical component in ensuring process stability and efficiency. Moreover, ongoing efforts to upgrade aging power infrastructure and add new generation capacity worldwide are driving the adoption of these solutions. Valve positioners also support emission control and help meet stringent energy efficiency regulations, reinforcing their role as an essential technology in the evolving energy landscape..

By Region, Asia Pacific is projected to be the fastest-growing market during the forecast period.

Asia Pacific is projected to be the fastest-growing region in the valve positioner market, registering the highest CAGR during the forecast period. This rapid growth is driven by expanding industrialization, infrastructure development, and increasing adoption of automation technologies across key sectors such as oil & gas, chemicals, water and wastewater treatment, and power generation. Countries like China, India, South Korea, and Southeast Asian nations are making significant investments in modernizing their manufacturing and process industries to enhance productivity and meet rising domestic and export demands. The region's push toward Industry 4.0 and smart manufacturing is accelerating the deployment of digital valve positioners, which offer benefits such as precise control, remote diagnostics, and system integration. Moreover, government initiatives supporting clean energy, efficient water management, and industrial automation are creating a favorable environment for market expansion. The need to upgrade aging infrastructure and meet stricter environmental regulations further fuels demand for advanced valve control solutions. With growing focus on energy efficiency, sustainability, and operational reliability, the Asia Pacific is emerging as a key hub for valve positioner adoption, driving its position as the most dynamic and rapidly advancing regional market..

Breakdown of primaries

A variety of executives from key organizations operating in the valve positioner market were interviewed in-depth, including CEOs, marketing directors, and innovation and technology directors.

- By Company Type: Tier 1 - 45%, Tier 2 - 35%, and Tier 3 - 20%

- By Designation: Directors - 45%, C-level - 30%, and Others - 25%

- By Region: North America - 45%, Europe - 25%, Asia Pacific - 20%, and RoW - 10%

Note: Other designations include sales and product managers and project engineers. The three tiers of the companies are defined based on their total revenue in 2024: Tier 1 - revenue greater than or equal to USD 1 billion; Tier 2 - revenue between USD 100 million and USD 1 billion; and Tier 3 revenue less than or equal to USD 100 million.

Major players profiled in this report are as follows:

Emerson Electric Co. (US), Siemens (Germany), ABB (Switzerland), Flowserve Corporation (US), Schneider Electric (France), SMC Corporation (Japan), Azbil Corporation (Japan), Baker Hughes (US), Rotork plc (UK), Valmet (Finland), samsoncontrols.net. (Germany), VRG Controls, LLC (US), Festo SE & Co. KG (Festo) (Germany), Badger Meter, Inc. (US), ControlAir (US), Crane Company (US), Christian Burkert GmbH & Co. KG (Germany), GEMU Group (Germany), Dwyer Instruments, LLC (US), VRC (US), POWER GENEX (South Korea), Val Controls (Denmark), Bray International (US), NIHON KOSO CO., LTD. (Japan), Spirax Sarco Limited (UK).

The study provides a detailed competitive analysis of these key players in the valve positioner market, presenting their company profiles, most recent developments, and key market strategies.

Study Coverage

In this report, the valve positioner market has been segmented based on type, actuation, industry, and region. The type segment includes digital, electro-pneumatic, and pneumatic. The actuation segment comprises single-acting and double-acting. The industry segment comprises oil & gas, energy & power, water & wastewater treatment, food & beverages, metals & mining, chemicals, pharmaceuticals, pulp & paper, and other industries. The market has been segmented into four regions - North America, Asia Pacific, Europe, and Rest of the World (RoW).

Reasons to buy the report

The report will help the leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall market and the sub-segments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the valve positioner market's pulse and provides information on key market drivers, restraints, challenges, and opportunities.

Key Benefits of Buying the Report

- Analysis of key drivers (growing significance of monitoring and control in process industries for optimized output, valve positioners are helping industries cut energy costs and improve efficiency as global energy demand continues to rise, rising adoption of smart valve positioners in various plant operations), restraints (fast-changing technology are slowing the adoption of valve positioners), opportunities (increasing focus on remote operations and decentralized plants, focus of industry players on offering improved customer service), and challenges (positioner overshoot and oversized valves hinder operation of control valves) influencing the growth of the valve positioner market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research and development activities, and new product launches in the valve positioner market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the valve positioner market across varied regions.

- Market Diversification: Exhaustive information about new products/services, untapped geographies, recent developments, and investments in the valve positioner market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Emerson Electric Co. (US), ABB (Switzerland), Siemens (Germany), Flowserve Corporation (US), Schneider Electric (France), and others.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED AND REGIONAL SCOPE

- 1.3.2 INCLUSIONS AND EXCLUSIONS

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY AND PRIMARY RESEARCH

- 2.1.2 SECONDARY DATA

- 2.1.2.1 List of key secondary sources

- 2.1.2.2 Key data from secondary sources

- 2.1.3 PRIMARY DATA

- 2.1.3.1 List of key primary interview participants

- 2.1.3.2 Breakdown of primaries

- 2.1.3.3 Key data from primary sources

- 2.1.3.4 Key industry insights

- 2.2 MARKET SIZE ESTIMATION METHODOLOGY

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- 2.2.1 BOTTOM-UP APPROACH

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RISK ANALYSIS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE GROWTH OPPORTUNITIES FOR KEY PLAYERS IN VALVE POSITIONER MARKET

- 4.2 VALVE POSITIONER MARKET, BY TYPE

- 4.3 VALVE POSITIONER MARKET, BY ACTUATION

- 4.4 VALVE POSITIONER MARKET, BY INDUSTRY

- 4.5 VALVE POSITIONER MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing significance of monitoring and control in process industries for optimized output

- 5.2.1.2 Increasing pressure to cut costs and operate more efficiently

- 5.2.1.3 Seamless integration with advanced control systems

- 5.2.2 RESTRAINTS

- 5.2.2.1 Rapid changes in industrial automation technologies

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Shift toward remote operations and decentralized facilities

- 5.2.3.2 Unlocking automation with self-powered valve positioners in remote sites

- 5.2.4 CHALLENGES

- 5.2.4.1 Challenges associated with oversized control valves and positioner overshoot

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.5 PRICING ANALYSIS

- 5.5.1 AVERAGE SELLING PRICE OF DIFFERENT TYPES OF VALVE POSITIONERS, BY KEY PLAYER, 2024

- 5.6 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 KEY TECHNOLOGIES

- 5.7.1.1 Digital communication protocols

- 5.7.1.2 Position feedback sensors

- 5.7.2 ADJACENT TECHNOLOGIES

- 5.7.2.1 SCADA

- 5.7.3 COMPLEMENTARY TECHNOLOGIES

- 5.7.3.1 Digital twin

- 5.7.1 KEY TECHNOLOGIES

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 THREAT OF NEW ENTRANTS

- 5.8.2 THREAT OF SUBSTITUTES

- 5.8.3 BARGAINING POWER OF SUPPLIERS

- 5.8.4 BARGAINING POWER OF BUYERS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.9.2 BUYING CRITERIA

- 5.10 CASE STUDIES

- 5.11 TRADE ANALYSIS

- 5.11.1 IMPORT DATA (HS CODE 8481)

- 5.11.2 EXPORT DATA (HS CODE 8481)

- 5.12 PATENT ANALYSIS

- 5.13 KEY CONFERENCES AND EVENTS, 2025-2026

- 5.14 STANDARDS AND REGULATIONS

- 5.14.1 STANDARDS

- 5.14.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.15 IMPACT OF AI/GENERATIVE AI ON VALVE POSITIONER MARKET

- 5.15.1 INTRODUCTION

- 5.15.2 IMPACT OF AI ON VALVE POSITIONER MARKET

- 5.15.3 TOP USE CASES AND MARKET POTENTIAL

- 5.16 IMPACT OF 2025 US TARIFF ON VALVE POSITIONER MARKET

- 5.16.1 INTRODUCTION

- 5.16.2 KEY TARIFF RATES

- 5.16.3 PRICE IMPACT ANALYSIS

- 5.16.4 IMPACT ON COUNTRY/REGION

- 5.16.4.1 US

- 5.16.4.2 Europe

- 5.16.4.3 Asia Pacific

- 5.16.5 IMPACT ON INDUSTRIES

6 VALVE POSITIONER MARKET, BY ACTUATION

- 6.1 INTRODUCTION

- 6.2 SINGLE-ACTING

- 6.2.1 EASY WORKING MECHANISM TO FUEL MARKET GROWTH

- 6.3 DOUBLE-ACTING

- 6.3.1 GROWING DEMAND FOR COMPACT-SIZE VALVES TO DRIVE MARKET

7 VALVE POSITIONER MARKET, BY INDUSTRY

- 7.1 INTRODUCTION

- 7.2 OIL & GAS

- 7.2.1 EMPHASIS ON REDUCING OPERATIONAL COSTS AND ENHANCE EFFICIENCY OF PLANTS TO DRIVE MARKET

- 7.3 WATER & WASTEWATER TREATMENT

- 7.3.1 RISING DEMAND FOR EFFECTIVE WATER MANAGEMENT ACROSS ENERGY AND URBAN INFRASTRUCTURE SECTORS TO FUEL MARKET GROWTH

- 7.4 ENERGY & POWER

- 7.4.1 INCREASING INVESTMENTS IN ENERGY SECTORS TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

- 7.5 CHEMICALS

- 7.5.1 RISING FOCUS ON BOOSTING CHEMICAL PLANT SAFETY TO FUEL MARKET GROWTH

- 7.6 PAPER & PULP

- 7.6.1 ADOPTION OF DIGITALIZED PROCESSES TO OFFER LUCRATIVE GROWTH OPPORTUNITIES

- 7.7 PHARMACEUTICALS

- 7.7.1 STRINGENT REGULATORY GUIDELINES AND INCREASING COMPLEXITIES IN PRODUCT LINES TO BOOST DEMAND

- 7.8 METALS & MINING

- 7.8.1 INCREASING PRESSURE TO OPTIMIZE PROCESSES AND REDUCE UNPLANNED DOWNTIME TO SUPPORT MARKET GROWTH

- 7.9 FOOD & BEVERAGES

- 7.9.1 RISING SUSTAINABLE INTENSIFICATION OF AGRICULTURE TO BOOST PRODUCTIVITY TO FUEL MARKET GROWTH

- 7.10 OTHER INDUSTRIES

8 VALVE POSITIONER MARKET, BY TYPE

- 8.1 INTRODUCTION

- 8.2 PNEUMATIC POSITIONERS

- 8.2.1 ABILITY TO WORK EFFICIENTLY IN ADVERSE ENVIRONMENTAL CONDITIONS TO BOOST DEMAND

- 8.3 ELECTRO-PNEUMATIC POSITIONERS

- 8.3.1 ABILITY TO OFFER SOLUTIONS WITHOUT SIGNIFICANT INFRASTRUCTURE OR WORKFORCE TRAINING UPGRADES TO FUEL MARKET GROWTH

- 8.4 DIGITAL POSITIONERS

- 8.4.1 RISING DEMAND FOR AUTOMATED AND DATA-DRIVEN PLANT OPERATIONS TO FOSTER MARKET GROWTH

9 VALVE POSITIONER MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.2 NORTH AMERICA

- 9.2.1 US

- 9.2.1.1 Growing investment in automation technologies to drive market

- 9.2.2 CANADA

- 9.2.2.1 Emphasis on improving water and wastewater infrastructure to foster market growth

- 9.2.3 MEXICO

- 9.2.3.1 Focus on expanding electricity generation, transmission, and distribution infrastructure to support market growth

- 9.2.1 US

- 9.3 EUROPE

- 9.3.1 UK

- 9.3.1.1 Rising focus digital automation to offer lucrative growth opportunities

- 9.3.2 GERMANY

- 9.3.2.1 Development of national hydrogen core network to foster market growth

- 9.3.3 FRANCE

- 9.3.3.1 Increasing demand for precision control technologies across energy sector to fuel market growth

- 9.3.4 REST OF EUROPE

- 9.3.1 UK

- 9.4 ASIA PACIFIC

- 9.4.1 CHINA

- 9.4.1.1 Emphasis on industrial modernization to boost demand

- 9.4.2 JAPAN

- 9.4.2.1 Need to optimize flow regulation and pressure control in fuel-based power plants to support market growth

- 9.4.3 INDIA

- 9.4.3.1 Government-led initiatives to boost adoption of automation components to fuel market growth

- 9.4.4 REST OF ASIA PACIFIC

- 9.4.1 CHINA

- 9.5 ROW

- 9.5.1 MIDDLE EAST & AFRICA

- 9.5.1.1 GCC

- 9.5.1.1.1 Adoption of Industry 4.0 technologies to offer lucrative growth opportunities

- 9.5.1.2 Africa & Rest of Middle East

- 9.5.1.1 GCC

- 9.5.2 SOUTH AMERICA

- 9.5.2.1 Brazil

- 9.5.2.1.1 Expanding public utilities and improving service reliability to support market growth

- 9.5.2.2 Rest of South America

- 9.5.2.1 Brazil

- 9.5.1 MIDDLE EAST & AFRICA

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2023-2025

- 10.3 REVENUE ANALYSIS, 2020-2024

- 10.4 MARKET SHARE ANALYSIS, 2024

- 10.5 COMPETITIVE EVALUATION MATRIX, 2024

- 10.5.1 STARS

- 10.5.2 EMERGING LEADERS

- 10.5.3 PERVASIVE PLAYERS

- 10.5.4 PARTICIPANTS

- 10.5.5 VALVE POSITIONER MARKET: COMPANY FOOTPRINT

- 10.5.5.1 Company footprint

- 10.5.5.2 Region footprint

- 10.5.5.3 Type footprint

- 10.5.5.4 Industry footprint

- 10.6 COMPANY EVALUAITON MATRIX: STARTUPS/SMES EVALUATION, 2024

- 10.6.1 PROGRESSIVE COMPANIES

- 10.6.2 RESPONSIVE COMPANIES

- 10.6.3 DYNAMIC COMPANIES

- 10.6.4 STARTING BLOCKS

- 10.6.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 10.6.5.1 List of key startups/SMEs

- 10.6.5.2 Competitive benchmarking of key startups/SMEs

- 10.7 COMPETITIVE SCENARIO

- 10.7.1 DEALS

- 10.7.2 EXPANSIONS

- 10.7.3 DEVELOPMENTS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- 11.1.1 EMERSON ELECTRIC CO.

- 11.1.1.1 Business overview

- 11.1.1.2 Products/Services/Solutions offered

- 11.1.1.3 Recent developments

- 11.1.1.3.1 Emerson Electric Co.: Deals

- 11.1.1.4 MnM view

- 11.1.1.4.1 Key strengths/Right to win

- 11.1.1.4.2 Strategic choices

- 11.1.1.4.3 Weaknesses/Competitive threats

- 11.1.2 ABB

- 11.1.2.1 Business overview

- 11.1.2.2 Products/Services/Solutions offered

- 11.1.2.3 MnM view

- 11.1.2.3.1 Key strengths/Right to win

- 11.1.2.3.2 Strategic choices

- 11.1.2.3.3 Weaknesses/Competitive threats

- 11.1.3 FLOWSERVE CORPORATION

- 11.1.3.1 Business overview

- 11.1.3.2 Products/Services/Solutions offered

- 11.1.3.3 Recent developments

- 11.1.3.3.1 Flowserve Corporation: Developments

- 11.1.3.4 MnM view

- 11.1.3.4.1 Key strengths/Right to win

- 11.1.3.4.2 Strategic choices

- 11.1.3.4.3 Weaknesses/Competitive threats

- 11.1.4 SIEMENS

- 11.1.4.1 Business overview

- 11.1.4.2 Products/Services/Solutions offered

- 11.1.4.3 MnM view

- 11.1.4.3.1 Key strengths/Right to win

- 11.1.4.3.2 Strategic choices

- 11.1.4.3.3 Weaknesses/Competitive threats

- 11.1.5 SCHNEIDER ELECTRIC

- 11.1.5.1 Business overview

- 11.1.5.2 Products/Services/Solutions offered

- 11.1.5.3 MnM view

- 11.1.5.3.1 Key strengths/Right to win

- 11.1.5.3.2 Strategic choices

- 11.1.5.3.3 Weaknesses/Competitive threats

- 11.1.6 SMC CORPORATION

- 11.1.6.1 Business overview

- 11.1.6.2 Products/Services/Solutions offered

- 11.1.7 AZBIL CORPORATION

- 11.1.7.1 Business overview

- 11.1.7.2 Products/Services/Solutions offered

- 11.1.7.3 Recent developments

- 11.1.7.3.1 Azbil Corporation: Expansions

- 11.1.8 BAKER HUGHES

- 11.1.8.1 Business overview

- 11.1.8.2 Products/Services/Solutions offered

- 11.1.9 ROTORK PLC

- 11.1.9.1 Business overview

- 11.1.9.2 Products/Services/Solutions offered

- 11.1.9.3 Recent developments

- 11.1.9.3.1 Rotork Plc: Deals

- 11.1.10 VALMET

- 11.1.10.1 Business overview

- 11.1.10.2 Products/Services/Solutions offered

- 11.1.1 EMERSON ELECTRIC CO.

- 11.2 OTHER PLAYERS

- 11.2.1 SAMSONCONTROLS.NET.

- 11.2.2 VRG CONTROLS, LLC

- 11.2.3 FESTO SE & CO. KG (FESTO)

- 11.2.4 BADGER METER, INC.

- 11.2.5 CONTROLAIR

- 11.2.6 CRANE COMPANY

- 11.2.7 CHRISTIAN BURKERT GMBH & CO. KG

- 11.2.8 GEMU GROUP

- 11.2.9 DWYER INSTRUMENTS LTD

- 11.2.10 VRC

- 11.2.11 POWER-GENEX LTD.

- 11.2.12 VAL CONTROLS

- 11.2.13 BRAY INTERNATIONAL

- 11.2.14 NIHON KOSO CO., LTD.

- 11.2.15 SPIRAX SARCO LIMITED

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 AVAILABLE CUSTOMIZATIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 218 Pages

- 納期

- 即納可能