AIプラットフォームの世界市場:提供別、機能性別 - 予測(~2030年)

AI Platform Market by Offering (Conversational AI, Generative AI, AI Agent, Deep Learning, Edge AI, AI API, MLOps, Data Mesh, Data Science Platforms), Functionality (Data Management, Model Development, Deployment, Training) - Global Forecast to 2030- 発行日

- ページ情報

- 英文 325 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1795416

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

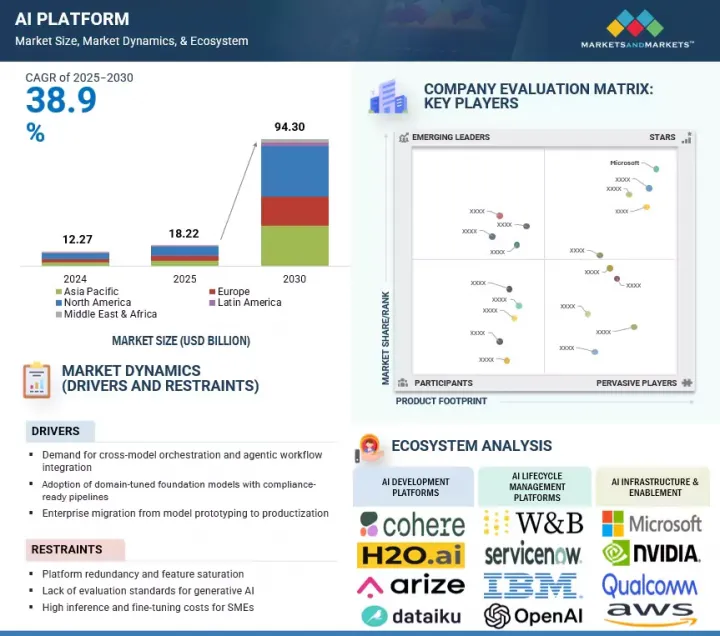

世界のAIプラットフォーム市場は急速に拡大しており、市場規模は2025年の182億2,000万米ドルから2030年までに943億米ドルに達すると予測され、予測期間にCAGRで38.9%の成長が見込まれます。

市場は、自動化需要の増加、産業(医療、金融、小売)全体におけるAIの採用の拡大、機械学習とクラウドコンピューティングの進歩によって牽引されています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2030年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2030年 |

| 単位 | 100万米ドル |

| セグメント | 提供、機能性、ユーザータイプ、エンドユーザー、地域 |

| 対象地域 | 北米、欧州、アジア太平洋、中東・アフリカ、ラテンアメリカ |

企業は効率性とデータ主導の意思決定を求め、需要をさらに促進しています。しかし、高い導入コストや規制上の課題などが足かせとなり、採用や拡張性が遅れる可能性があります。

「プラットフォームタイプ別では、AIインフラ・イネーブルメントが予測期間に2番目に高い成長率となる見込みです。」

この成長は、複雑なAIワークロードをサポートするために必要なHPCリソース、データストレージ、スケーラブルなクラウドインフラに対する需要の高まりによってもたらされます。組織は、AIモデルを効率的に訓練、展開、管理する堅牢なインフラをますます必要としています。主なコンポーネントには、GPU、データレイク、MLフレームワーク、オーケストレーションツールなどがあります。さまざまな産業でAIの採用が増加しているため、支援技術への投資が拡大しています。

「企業エンドユーザー別では、ソフトウェア技術セグメントが予測期間に最大の市場シェアを占めます。」

企業エンドユーザー別では、ソフトウェア技術セグメントが予測期間にAIプラットフォーム市場で最大の市場シェアを占める見込みです。これは主に、同部門がソフトウェア開発、サイバーセキュリティ、データアナリティクス、IT運用にいち早くAIを採用し、統合しているためです。ハイテク企業は技術革新の最前線にあり、製品の強化、顧客体験の向上、競合優位性の獲得のためにAIに多額の投資を行っています。そのインフラも、堅牢なクラウド環境やデータ処理能力などを含む、AIプラットフォームのサポートに適合しています。

さらに、この部門には熟練した専門家が揃っているため、AIソリューションの迅速な展開と拡張が可能です。その結果、ソフトウェア技術産業は、企業エンドユーザーの間でのAI採用をリードし続けています。

「北米が市場シェアでリードする一方、アジア太平洋がAIプラットフォーム市場でもっとも急成長している地域として台頭しています。」

北米の優位性は、強力な技術エコシステム、産業全体でのAIの早期採用、Google、Microsoft、IBMなどの主要AIプラットフォームプロバイダーのプレゼンスに起因します。この地域は、高額な研究開発投資、先進のインフラ、熟練した専門家の大規模なプールから利益を得ています。

一方、アジア太平洋は、デジタルトランスフォーメーションの進行、政府主導のAI戦略、中国、インド、日本での採用の拡大により、もっとも速く成長しています。急速な工業化、テックスタートアップの拡大、製造、医療、金融などの部門における自動化需要の高まりが、この成長を後押ししています。北米が成熟のペースを握る一方で、アジア太平洋は積極的な投資とイノベーションによって急速にその差を縮めています。

当レポートでは、世界のAIプラットフォーム市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要な知見

- AIプラットフォーム市場における魅力的な機会

- AIプラットフォーム市場:上位3つの機能性

- 北米のAIプラットフォーム市場:提供別、機能性別

- AIプラットフォーム市場:地域別

第5章 市場の概要と産業動向

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- AIプラットフォーム市場の進化

- サプライチェーン分析

- エコシステム分析

- 技術分析

- 主要技術

- 補完技術

- 隣接技術

- ケーススタディ分析

- ケーススタディ1:IMERYS、生産性とデータアクセスを向上させるエンタープライズAIチャットを展開

- ケーススタディ2:BASISAI、ML展開を自動化しAI開発ライフサイクルを加速

- ケーススタディ3:AT&T、AIプラットフォームを活用して不正行為を防止しネットワーク効率を向上

- ケーススタディ4:BMW、よりスマートな調達分析に向け生成AIを展開

- ケーススタディ5:MOVEWORKS、従業員のサポートを大規模に自動化するAIプラットフォームを展開

- ポーターのファイブフォース分析

- カスタマービジネスに影響を与える動向/混乱

- 規制情勢

- 規制機関、政府機関、その他の組織

- 規制:AI

- 特許分析

- 調査手法

- 特許出願件数:書類種別

- イノベーションと特許出願

- 投資と資金調達のシナリオ

- 価格設定の分析

- 平均販売価格:主要企業別(2025年)

- 参考価格分析:機能性別(2025年)

- 主な会議とイベント(2025年~2026年)

- 主なステークホルダーと購入基準

- 顧客のセグメンテーションとバイヤーのペルソナ

- 主なバイヤーのアーキタイプ

- 主な特定業界のバイヤーのセグメンテーション

- バイヤージャーニーマッピング

- テクノロジーロードマップとイノベーションの方向性

- テクノロジーロードマップと能力分野

- AIプラットフォーム能力成熟度フレームワーク

- パートナーシップとエコシステム戦略

- バイヤーにとっての重要な成功要因

第6章 AIプラットフォーム市場:提供別

- イントロダクション

- AI開発プラットフォーム

- AIライフサイクルマネジメントプラットフォーム

- AIイネーブルメントサービス

第7章 AIプラットフォーム市場:機能性別

- イントロダクション

- データ管理・準備

- モデル開発・トレーニング

- モデル展開・サービス提供

- モニタリング・メンテナンス

- モデルガバナンス・コンプライアンス

- モデルのファインチューニング・パーソナライズ

- 説明可能性・バイアスツール

- セキュリティ・プライバシー

第8章 AIプラットフォーム市場:ユーザータイプ別

- イントロダクション

- データサイエンティスト・MLエンジニア

- MLOPS/AIエンジニア

- ビジネスアナリスト・民間開発者

- AIプロダクトマネージャー

- ITクラウドアーキテクト

第9章 AIプラットフォーム市場:エンドユーザー別

- イントロダクション

- 企業

- 医療・ライフサイエンス

- BFSI

- 小売・eコマース

- 輸送・ロジスティクス

- 自動車・モビリティ

- 通信

- 政府・防衛

- エネルギー・公益事業

- 製造

- ソフトウェア・技術

- メディア・エンターテインメント

- その他の企業エンドユーザー

- 個人ユーザー

第10章 AIプラットフォーム市場:地域別

- イントロダクション

- 北米

- 北米のAIプラットフォーム市場の促進要因

- 北米のマクロ経済の見通し

- 米国

- カナダ

- 欧州

- 欧州のAIプラットフォーム市場の促進要因

- 欧州のマクロ経済の見通し

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- アジア太平洋のAIプラットフォーム市場の促進要因

- アジア太平洋のマクロ経済の見通し

- 中国

- 日本

- インド

- オーストラリア・ニュージーランド

- ASEAN

- 韓国

- その他のアジア太平洋

- 中東・アフリカ

- 中東・アフリカのAIプラットフォーム市場の促進要因

- 中東・アフリカのマクロ経済の見通し

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- トルコ

- カタール

- エジプト

- クウェート

- その他の中東・アフリカ

- ラテンアメリカ

- ラテンアメリカのAIプラットフォーム市場の促進要因

- ラテンアメリカのマクロ経済の見通し

- ブラジル

- メキシコ

- アルゼンチン

- チリ

- その他のラテンアメリカ

第11章 競合情勢

- 概要

- 主要参入企業の戦略/強み(2022年~2025年)

- 収益分析(2020年~2024年)

- 市場シェア分析(2024年)

- 製品の比較分析

- 企業の評価と財務指標

- 企業の評価マトリクス:主要企業(2024年)

- 企業の評価マトリクス:スタートアップ/中小企業(2024年)

- 企業の評価マトリクス:AIイネーブルメントサービス(2024年)

- 競合シナリオと動向

第12章 企業プロファイル

- イントロダクション

- 主要企業

- MICROSOFT

- IBM

- ORACLE

- AWS

- INTEL

- SALESFORCE

- SAP

- SERVICENOW

- NVIDIA

- OPENAI

- ALIBABA CLOUD

- HPE

- DATABRICKS

- INSIGHT

- PALANTIR

- ALTAIR

- DATAIKU

- STARTUP/SME PROFILES

- H2O.AI

- ANTHROPIC

- COHERE

- ANYSCALE

- DATAROBOT

- VITAL AI

- RAINBIRD TECHNOLOGIES

- ARIZE AI

- CALYPSOAI

- CLARIFAI

- WEIGHTS & BIASES

- ELVEX

- IGUAZIO

- MISTRAL AI

- BASETEN

- LIGHTNING AI

- PROWESS CONSULTING

- DEVTECH

- ZYXWARE TECHNOLOGIES

- FLUIDONE

- AHELIOTECH

- ORIL

- CONVERSANT SOLUTIONS

第13章 隣接市場と関連市場

- イントロダクション

- AIツールキット市場 - 世界の予測(~2028年)

- 市場の定義

- 市場の概要

- ノーコードAIプラットフォーム市場 - 世界の予測(~2029年)

- 市場の定義

- 市場の概要

第14章 付録

図表

List of Tables

- TABLE 1 UNITED STATES DOLLAR EXCHANGE RATE, 2020-2024

- TABLE 2 FACTOR ANALYSIS

- TABLE 3 GLOBAL AI PLATFORM MARKET SIZE AND GROWTH RATE, 2020-2024 (USD MILLION, Y-O-Y %)

- TABLE 4 GLOBAL AI PLATFORM MARKET SIZE AND GROWTH RATE, 2025-2030 (USD MILLION, Y-O-Y %)

- TABLE 5 AI PLATFORM MARKET: ECOSYSTEM

- TABLE 6 IMPACT OF PORTER'S FIVE FORCES ON AI PLATFORM MARKET

- TABLE 7 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 8 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 MIDDLE EAST & AFRICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 LATIN AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 PATENTS FILED, 2016-2025

- TABLE 13 LIST OF TOP PATENTS IN AI PLATFORM MARKET, 2024-2025

- TABLE 14 PRICING DATA OF AI PLATFORM MARKET, BY OFFERING

- TABLE 15 PRICING DATA OF AI PLATFORM MARKET, BY FUNCTIONALITY

- TABLE 16 AI PLATFORM MARKET: DETAILED LIST OF CONFERENCES AND EVENTS

- TABLE 17 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- TABLE 18 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 19 KEY BUYER ARCHETYPES AND DECISION INFLUENCE

- TABLE 20 INDUSTRY-SPECIFIC BUYER SEGMENTATION

- TABLE 21 TECHNOLOGY ROADMAP & CAPABILITY AREA

- TABLE 22 PARTNERSHIP TYPE AND STRATEGIC VALUE

- TABLE 23 KEY SUCCESS FACTORS FOR BUYERS

- TABLE 24 AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 25 AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 26 AI DEVELOPMENT PLATFORMS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 27 AI DEVELOPMENT PLATFORMS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 28 AI LIFECYCLE MANAGEMENT PLATFORMS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 29 AI LIFECYCLE MANAGEMENT PLATFORMS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 30 AI ENABLEMENT SERVICES: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 31 AI ENABLEMENT SERVICES: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 32 AI PLATFORM MARKET, BY FUNCTIONALITY, 2020-2024 (USD MILLION)

- TABLE 33 AI PLATFORM MARKET, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 34 DATA MANAGEMENT & PREPARATION: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 35 DATA MANAGEMENT & PREPARATION: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 36 MODEL DEVELOPMENT & TRAINING: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 37 MODEL DEVELOPMENT & TRAINING: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 38 MODEL DEPLOYMENT & SERVING: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 39 MODEL DEPLOYMENT & SERVING: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 40 MONITORING & MAINTENANCE: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 41 MONITORING & MAINTENANCE: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 42 MODEL GOVERNANCE & COMPLIANCE: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 43 MODEL GOVERNANCE & COMPLIANCE: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 44 MODEL FINE-TUNING & PERSONALIZATION: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 45 MODEL FINE-TUNING & PERSONALIZATION: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 46 EXPLAINABILITY & BIAS TOOLS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 47 EXPLAINABILITY & BIAS TOOLS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 48 SECURITY & PRIVACY: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 49 SECURITY & PRIVACY: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 50 AI PLATFORM MARKET, BY USER TYPE, 2020-2024 (USD MILLION)

- TABLE 51 AI PLATFORM MARKET, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 52 DATA SCIENTISTS & ML ENGINEERS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 53 DATA SCIENTISTS & ML ENGINEERS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 54 MLOPS/AI ENGINEERS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 55 MLOPS/AI ENGINEERS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 56 BUSINESS ANALYSTS & CITIZEN DEVELOPERS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 57 BUSINESS ANALYSTS & CITIZEN DEVELOPERS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 58 AI PRODUCT MANAGERS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 59 AI PRODUCT MANAGERS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 60 IT & CLOUD ARCHITECTS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 61 IT & CLOUD ARCHITECTS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 62 AI PLATFORM MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 63 AI PLATFORM MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 64 AI PLATFORM MARKET, BY ENTERPRISE, 2020-2024 (USD MILLION)

- TABLE 65 AI PLATFORM MARKET, BY ENTERPRISE, 2025-2030 (USD MILLION)

- TABLE 66 HEALTHCARE & LIFE SCIENCES: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 67 HEALTHCARE & LIFE SCIENCES: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 68 BFSI: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 69 BFSI: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 70 RETAIL & E-COMMERCE: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 71 RETAIL & E-COMMERCE: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 72 TRANSPORTATION & LOGISTICS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 73 TRANSPORTATION & LOGISTICS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 74 AUTOMOTIVE & MOBILITY: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 75 AUTOMOTIVE & MOBILITY: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 76 TELECOMMUNICATIONS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 77 TELECOMMUNICATIONS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 78 GOVERNMENT & DEFENSE: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 79 GOVERNMENT & DEFENSE: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 80 ENERGY & UTILITIES: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 81 ENERGY & UTILITIES: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 82 MANUFACTURING: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 83 MANUFACTURING: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 84 SOFTWARE & TECHNOLOGY: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 85 SOFTWARE & TECHNOLOGY: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 86 MEDIA & ENTERTAINMENT: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 87 MEDIA & ENTERTAINMENT: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 88 OTHER ENTERPRISE END USERS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 89 OTHER ENTERPRISE END USERS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 90 INDIVIDUAL USERS: AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 91 INDIVIDUAL USERS: AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 92 AI PLATFORM MARKET, BY REGION, 2020-2024 (USD MILLION)

- TABLE 93 AI PLATFORM MARKET, BY REGION, 2025-2030 (USD MILLION)

- TABLE 94 NORTH AMERICA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 95 NORTH AMERICA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 96 NORTH AMERICA: AI PLATFORM MARKET, BY FUNCTIONALITY, 2020-2024 (USD MILLION)

- TABLE 97 NORTH AMERICA: AI PLATFORM MARKET, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 98 NORTH AMERICA: AI PLATFORM MARKET, BY USER TYPE, 2020-2024 (USD MILLION)

- TABLE 99 NORTH AMERICA: AI PLATFORM MARKET, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 100 NORTH AMERICA: AI PLATFORM MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 101 NORTH AMERICA: AI PLATFORM MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 102 NORTH AMERICA: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2020-2024 (USD MILLION)

- TABLE 103 NORTH AMERICA: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2025-2030 (USD MILLION)

- TABLE 104 NORTH AMERICA: AI PLATFORM MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 105 NORTH AMERICA: AI PLATFORM MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 106 US: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 107 US: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 108 CANADA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 109 CANADA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 110 EUROPE: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 111 EUROPE: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 112 EUROPE: AI PLATFORM MARKET, BY FUNCTIONALITY, 2020-2024 (USD MILLION)

- TABLE 113 EUROPE: AI PLATFORM MARKET, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 114 EUROPE: AI PLATFORM MARKET, BY USER TYPE, 2020-2024 (USD MILLION)

- TABLE 115 EUROPE: AI PLATFORM MARKET, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 116 EUROPE: AI PLATFORM MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 117 EUROPE: AI PLATFORM MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 118 EUROPE: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2020-2024 (USD MILLION)

- TABLE 119 EUROPE: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2025-2030 (USD MILLION)

- TABLE 120 EUROPE: AI PLATFORM MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 121 EUROPE: AI PLATFORM MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 122 UK: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 123 UK: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 124 GERMANY: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 125 GERMANY: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 126 FRANCE: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 127 FRANCE: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 128 ITALY: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 129 ITALY: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 130 SPAIN: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 131 SPAIN: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 132 REST OF EUROPE: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 133 REST OF EUROPE: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 134 ASIA PACIFIC: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 135 ASIA PACIFIC: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 136 ASIA PACIFIC: AI PLATFORM MARKET, BY FUNCTIONALITY, 2020-2024 (USD MILLION)

- TABLE 137 ASIA PACIFIC: AI PLATFORM MARKET, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 138 ASIA PACIFIC: AI PLATFORM MARKET, BY USER TYPE, 2020-2024 (USD MILLION)

- TABLE 139 ASIA PACIFIC: AI PLATFORM MARKET, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 140 ASIA PACIFIC: AI PLATFORM MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 141 ASIA PACIFIC: AI PLATFORM MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 142 ASIA PACIFIC: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2020-2024 (USD MILLION)

- TABLE 143 ASIA PACIFIC: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2025-2030 (USD MILLION)

- TABLE 144 ASIA PACIFIC: AI PLATFORM MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 145 ASIA PACIFIC: AI PLATFORM MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 146 CHINA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 147 CHINA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 148 JAPAN: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 149 JAPAN: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 150 INDIA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 151 INDIA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 152 AUSTRALIA AND NEW ZEALAND: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 153 AUSTRALIA AND NEW ZEALAND: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 154 ASEAN: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 155 ASEAN: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 156 SOUTH KOREA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 157 SOUTH KOREA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 158 REST OF ASIA PACIFIC: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 159 REST OF ASIA PACIFIC: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 160 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 161 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 162 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY FUNCTIONALITY, 2020-2024 (USD MILLION)

- TABLE 163 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 164 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY USER TYPE, 2020-2024 (USD MILLION)

- TABLE 165 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 166 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 167 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 168 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2020-2024 (USD MILLION)

- TABLE 169 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2025-2030 (USD MILLION)

- TABLE 170 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 171 MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 172 SAUDI ARABIA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 173 SAUDI ARABIA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 174 UAE: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 175 UAE: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 176 SOUTH AFRICA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 177 SOUTH AFRICA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 178 TURKEY: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 179 TURKEY: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 180 QATAR: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 181 QATAR: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 182 EGYPT: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 183 EGYPT: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 184 KUWAIT: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 185 KUWAIT: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 186 REST OF MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 187 REST OF MIDDLE EAST & AFRICA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 188 LATIN AMERICA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 189 LATIN AMERICA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 190 LATIN AMERICA: AI PLATFORM MARKET, BY FUNCTIONALITY, 2020-2024 (USD MILLION)

- TABLE 191 LATIN AMERICA: AI PLATFORM MARKET, BY FUNCTIONALITY, 2025-2030 (USD MILLION)

- TABLE 192 LATIN AMERICA: AI PLATFORM MARKET, BY USER TYPE, 2020-2024 (USD MILLION)

- TABLE 193 LATIN AMERICA: AI PLATFORM MARKET, BY USER TYPE, 2025-2030 (USD MILLION)

- TABLE 194 LATIN AMERICA: AI PLATFORM MARKET, BY END USER, 2020-2024 (USD MILLION)

- TABLE 195 LATIN AMERICA: AI PLATFORM MARKET, BY END USER, 2025-2030 (USD MILLION)

- TABLE 196 LATIN AMERICA: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2020-2024 (USD MILLION)

- TABLE 197 LATIN AMERICA: AI PLATFORM MARKET, BY ENTERPRISE END USER, 2025-2030 (USD MILLION)

- TABLE 198 LATIN AMERICA: AI PLATFORM MARKET, BY COUNTRY, 2020-2024 (USD MILLION)

- TABLE 199 LATIN AMERICA: AI PLATFORM MARKET, BY COUNTRY, 2025-2030 (USD MILLION)

- TABLE 200 BRAZIL: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 201 BRAZIL: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 202 MEXICO: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 203 MEXICO: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 204 ARGENTINA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 205 ARGENTINA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 206 CHILE: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 207 CHILE: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 208 REST OF LATIN AMERICA: AI PLATFORM MARKET, BY OFFERING, 2020-2024 (USD MILLION)

- TABLE 209 REST OF LATIN AMERICA: AI PLATFORM MARKET, BY OFFERING, 2025-2030 (USD MILLION)

- TABLE 210 OVERVIEW OF STRATEGIES ADOPTED BY KEY AI PLATFORM VENDORS, 2022-2025

- TABLE 211 AI PLATFORM MARKET: DEGREE OF COMPETITION

- TABLE 212 REGIONAL FOOTPRINT (18 COMPANIES), 2024

- TABLE 213 OFFERING FOOTPRINT (18 COMPANIES), 2024

- TABLE 214 FUNCTIONALITY FOOTPRINT (18 COMPANIES), 2024

- TABLE 215 END USER FOOTPRINT (18 COMPANIES), 2024

- TABLE 216 AI PLATFORM MARKET: KEY STARTUPS/SMES, 2024

- TABLE 217 AI PLATFORM MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 218 AI PLATFORM MARKET: AI ENABLEMENT SERVICES, 2024

- TABLE 219 AI PLATFORM MARKET: COMPETITIVE BENCHMARKING OF AI ENABLEMENT SERVICES

- TABLE 220 AI PLATFORM MARKET: PRODUCT LAUNCHES AND ENHANCEMENTS, 2022-2025

- TABLE 221 AI PLATFORM MARKET: DEALS, 2022-2025

- TABLE 222 GOOGLE: COMPANY OVERVIEW

- TABLE 223 GOOGLE: PRODUCTS OFFERED

- TABLE 224 GOOGLE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 225 GOOGLE: DEALS

- TABLE 226 GOOGLE: EXPANSIONS

- TABLE 227 MICROSOFT: COMPANY OVERVIEW

- TABLE 228 MICROSOFT: PRODUCTS OFFERED

- TABLE 229 MICROSOFT: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 230 MICROSOFT: DEALS

- TABLE 231 IBM: COMPANY OVERVIEW

- TABLE 232 IBM: PRODUCTS OFFERED

- TABLE 233 IBM: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 234 IBM: DEALS

- TABLE 235 ORACLE: COMPANY OVERVIEW

- TABLE 236 ORACLE: PRODUCTS OFFERED

- TABLE 237 ORACLE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 238 ORACLE: DEALS

- TABLE 239 AWS: COMPANY OVERVIEW

- TABLE 240 AWS: PRODUCTS OFFERED

- TABLE 241 AWS: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 242 AWS: DEALS

- TABLE 243 INTEL: COMPANY OVERVIEW

- TABLE 244 INTEL: PRODUCTS OFFERED

- TABLE 245 INTEL: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 246 INTEL: DEALS

- TABLE 247 SALESFORCE: COMPANY OVERVIEW

- TABLE 248 SALESFORCE: PRODUCTS OFFERED

- TABLE 249 SALESFORCE: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 250 SALESFORCE: DEALS

- TABLE 251 SAP: COMPANY OVERVIEW

- TABLE 252 SAP: PRODUCTS OFFERED

- TABLE 253 SAP: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 254 SAP: DEALS

- TABLE 255 SERVICENOW: COMPANY OVERVIEW

- TABLE 256 SERVICENOW: PRODUCTS OFFERED

- TABLE 257 SERVICENOW: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 258 SERVICENOW: DEALS

- TABLE 259 NVIDIA: COMPANY OVERVIEW

- TABLE 260 NVIDIA: PRODUCTS OFFERED

- TABLE 261 NVIDIA: PRODUCT LAUNCHES AND ENHANCEMENTS

- TABLE 262 NVIDIA: DEALS

- TABLE 263 AI TOOLKIT MARKET, BY OFFERING, 2017-2022 (USD MILLION)

- TABLE 264 AI TOOLKIT MARKET, BY OFFERING, 2023-2028 (USD MILLION)

- TABLE 265 AI TOOLKIT MARKET, BY TECHNOLOGY, 2017-2022 (USD MILLION)

- TABLE 266 AI TOOLKIT MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 267 AI TOOLKIT MARKET, BY VERTICAL, 2017-2022 (USD MILLION)

- TABLE 268 AI TOOLKIT MARKET, BY VERTICAL, 2023-2028 (USD MILLION)

- TABLE 269 AI TOOLKIT MARKET, BY REGION, 2017-2022 (USD MILLION)

- TABLE 270 AI TOOLKIT MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 271 NO-CODE AI PLATFORMS MARKET, BY OFFERING, 2019-2023 (USD MILLION)

- TABLE 272 NO-CODE AI PLATFORMS MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 273 NO-CODE AI PLATFORMS MARKET, BY TECHNOLOGY, 2019-2023 (USD MILLION)

- TABLE 274 NO-CODE AI PLATFORMS MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 275 NO-CODE AI PLATFORMS MARKET, BY DATA MODALITY, 2019-2023 (USD MILLION)

- TABLE 276 NO-CODE AI PLATFORMS MARKET, BY DATA MODALITY, 2024-2029 (USD MILLION)

- TABLE 277 NO-CODE AI PLATFORMS MARKET, BY APPLICATION, 2019-2023 (USD MILLION)

- TABLE 278 NO-CODE AI PLATFORMS MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 279 NO-CODE AI PLATFORMS MARKET, BY VERTICAL, 2019-2023 (USD MILLION)

- TABLE 280 NO-CODE AI PLATFORMS MARKET, BY VERTICAL, 2024-2029 (USD MILLION)

- TABLE 281 NO-CODE AI PLATFORMS MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 282 NO-CODE AI PLATFORMS MARKET, BY REGION, 2024-2029 (USD MILLION)

List of Figures

- FIGURE 1 AI PLATFORM MARKET: RESEARCH DESIGN

- FIGURE 2 AI PLATFORM MARKET: DATA TRIANGULATION

- FIGURE 3 AI PLATFORM MARKET: TOP-DOWN AND BOTTOM-UP APPROACHES

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY-APPROACH 1, BOTTOM-UP (SUPPLY-SIDE): REVENUE FROM AI DEVELOPMENT PLATFORMS, AI LIFECYCLE MANAGEMENT PLATFORMS, AND AI-ENABLEMENT SERVICES

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY-APPROACH 2, BOTTOM-UP (SUPPLY-SIDE): COLLECTIVE REVENUE FROM KEY COMPANIES IN AI PLATFORM MARKET

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY-APPROACH 3, BOTTOM-UP (SUPPLY-SIDE): COLLECTIVE REVENUE FROM BUSINESS UNITS (BU) OF KEY VENDORS IN AI PLATFORM MARKET

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY-APPROACH 4, BOTTOM-UP (DEMAND-SIDE): SHARE OF AI PLATFORM THROUGH OVERALL IT SPENDING ON AI PLATFORM SOLUTIONS

- FIGURE 8 AI DEVELOPMENT PLATFORM SEGMENT TO HOLD LARGEST MARKET SIZE IN 2025

- FIGURE 9 DATA SCIENTISTS & ML ENGINEERS SEGMENT TO HOLD LARGEST MARKET SHARE IN 2025

- FIGURE 10 DATA MANAGEMENT & PREPARATION SEGMENT TO HOLD LARGEST MARKET SIZE IN 2025

- FIGURE 11 ENTERPRISE SEGMENT TO HOLD LARGEST MARKET SHARE IN 2025

- FIGURE 12 HEALTHCARE & LIFE SCIENCES TO WITNESS HIGHEST GROWTH RATE IN END USER SEGMENT DURING FORECAST PERIOD

- FIGURE 13 ASIA PACIFIC TO REGISTER FASTEST GROWTH BETWEEN 2025 AND 2030

- FIGURE 14 ACCELERATING DIGITAL INFRASTRUCTURE AND ENTERPRISE AI ADOPTION ACROSS ASIA PACIFIC TO DRIVE AI PLATFORM MARKET GROWTH

- FIGURE 15 MODEL DEPLOYMENT & SERVING SEGMENT TO ACCOUNT FOR HIGHEST GROWTH RATE DURING FORECAST PERIOD

- FIGURE 16 AI DEVELOPMENT PLATFORM AND DATA MANAGEMENT & PREPARATION TO BE LARGEST SHAREHOLDERS IN NORTH AMERICAN AI PLATFORM MARKET IN 2025

- FIGURE 17 NORTH AMERICA TO HOLD LARGEST MARKET SHARE IN 2025

- FIGURE 18 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES: AI PLATFORM MARKET

- FIGURE 19 AI PLATFORM MARKET EVOLUTION

- FIGURE 20 AI PLATFORM MARKET: SUPPLY CHAIN ANALYSIS

- FIGURE 21 KEY PLAYERS IN AI PLATFORM MARKET ECOSYSTEM

- FIGURE 22 AI PLATFORM MARKET: PORTER'S FIVE FORCES' ANALYSIS

- FIGURE 23 REVENUE SHIFT OF AI PLATFORM MARKET VENDORS

- FIGURE 24 NUMBER OF PATENTS GRANTED IN LAST 10 YEARS, 2016-2025

- FIGURE 25 REGIONAL ANALYSIS OF PATENTS GRANTED, 2016-2025

- FIGURE 26 LEADING AI PLATFORM MARKET STARTUPS, BY FUNDING VALUE AND FUNDING ROUND, 2025

- FIGURE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- FIGURE 28 KEY BUYING CRITERIA FOR TOP THREE END USERS

- FIGURE 29 AI LIFECYCLE MANAGEMENT PLATFORMS SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 30 MODEL DEPLOYMENT & SERVING TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 31 MLOPS/AI ENGINEERS SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 32 ENTERPRISES TO GROW AT HIGHER CAGR DURING FORECAST PERIOD

- FIGURE 33 HEALTHCARE & LIFE SCIENCES SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 34 NORTH AMERICA TO BE LARGEST REGIONAL MARKET DURING FORECAST PERIOD

- FIGURE 35 INDIA TO WITNESS FASTEST GROWTH DURING FORECAST PERIOD

- FIGURE 36 NORTH AMERICA: MARKET SNAPSHOT

- FIGURE 37 ASIA PACIFIC: MARKET SNAPSHOT

- FIGURE 38 TOP FIVE PUBLIC PLAYERS IN AI PLATFORM MARKET, 2020-2024 (USD MILLION)

- FIGURE 39 SHARE OF LEADING COMPANIES IN AI PLATFORM MARKET, 2024

- FIGURE 40 PRODUCT COMPARATIVE ANALYSIS

- FIGURE 41 FINANCIAL METRICS OF KEY VENDORS

- FIGURE 42 YEAR-TO-DATE (YTD) PRICE TOTAL RETURN AND 5-YEAR STOCK BETA OF KEY VENDORS

- FIGURE 43 AI PLATFORM MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2024

- FIGURE 44 COMPANY FOOTPRINT (18 COMPANIES), 2024

- FIGURE 45 AI PLATFORM MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2024

- FIGURE 46 AI PLATFORM MARKET: COMPANY EVALUATION MATRIX (AI ENABLEMENT SERVICES), 2024

- FIGURE 47 GOOGLE: COMPANY SNAPSHOT

- FIGURE 48 MICROSOFT: COMPANY SNAPSHOT

- FIGURE 49 IBM: COMPANY SNAPSHOT

- FIGURE 50 ORACLE: COMPANY SNAPSHOT

- FIGURE 51 AWS: COMPANY SNAPSHOT

- FIGURE 52 INTEL: COMPANY SNAPSHOT

- FIGURE 53 SALESFORCE: COMPANY SNAPSHOT

- FIGURE 54 SAP: COMPANY SNAPSHOT

- FIGURE 55 SERVICENOW: COMPANY SNAPSHOT

- FIGURE 56 NVIDIA: COMPANY SNAPSHOT

目次

The AI platform market is expanding rapidly, with a projected market size rising from USD 18.22 billion in 2025 to USD 94.30 billion by 2030, at a CAGR of 38.9% during the forecast period. The market is driven by the increasing demand for automation, growing adoption of AI across industries (healthcare, finance, and retail), and advancements in machine learning and cloud computing.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2030 |

| Base Year | 2024 |

| Forecast Period | 2025-2030 |

| Units Considered | USD (Million) |

| Segments | Offering, Functionality, User Type, End User, and Region |

| Regions covered | North America, Europe, Asia Pacific, Middle East & Africa, and Latin America |

Businesses seek efficiency and data-driven decision-making, further fuelling demand. However, restraints include high implementation costs and regulatory challenges, which can slow down adoption and scalability.

"By platform type, AI infrastructure & enablement is expected to account for the second fastest growth rate during the forecast period"

By platform type, the AI infrastructure & enablement segment is expected to account for the second fastest growth rate during the forecast period in the AI platform market. This growth is driven by the rising demand for high-performance computing resources, data storage, and scalable cloud infrastructure needed to support complex AI workloads. Organizations increasingly require robust infrastructure to train, deploy, and manage AI models efficiently. Key components include GPUs, data lakes, ML frameworks, and orchestration tools. The increase in AI adoption across various industries is driving greater investment in supporting technologies.

"By enterprise end user, software & technology segment will hold the largest market share during the forecast period"

By enterprise end user, the software & technology segment is expected to hold the largest market share in the AI platform market during the forecast period. This is primarily due to the sector's early adoption and integration of AI for software development, cybersecurity, data analytics, and IT operations. Tech companies are at the forefront of innovation, investing heavily in AI to enhance product offerings, improve customer experience, and gain a competitive advantage. Their infrastructure is also well-suited to support AI platforms, including robust cloud environments and data processing capabilities.

Additionally, the availability of skilled professionals in this sector enables faster deployment and scaling of AI solutions. As a result, the software & technology industry continues to lead AI adoption among enterprise end users.

"North America leads in market share while Asia Pacific emerges as the fastest-growing region in the AI platform market"

North America leads in market share, while Asia Pacific emerges as the fastest-growing region in the AI platform market. North America's dominance is attributed to its strong technological ecosystem, early adoption of AI across industries, and presence of major AI platform providers such as Google, Microsoft, and IBM. The region benefits from high R&D investment, advanced infrastructure, and a large pool of skilled professionals.

In contrast, Asia Pacific is experiencing the fastest growth due to increasing digital transformation, government-led AI initiatives, and growing adoption in China, India, and Japan. Rapid industrialization, expanding tech startups, and rising demand for automation in sectors such as manufacturing, healthcare, and finance are driving this growth. While North America sets the pace in maturity, Asia Pacific is quickly narrowing the gap with aggressive investments and innovation.

Breakdown of Primaries

In-depth interviews were conducted with chief executive officers (CEOs), innovation and technology directors, system integrators, and executives from various key organizations operating in the AI platform market.

- By Company: Tier I - 15%, Tier II - 42%, and Tier III - 43%

- By Designation: C-Level Executives - 65%, D-Level Executives -23%, and Others - 12%

- By Region: North America - 40%, Europe - 30%, Asia Pacific - 20%, Middle East & Africa - 5%, and Latin America - 5%

The report includes a study of key players in the AI platform market. It profiles major market vendors, including Google (US), Microsoft (US), IBM (US), Intel (US), Infosys (India), Wipro (India), Salesforce (US), HPE (US), Insight (US), NVIDIA (US), Alibaba Cloud (China), AWS (US), SAP (Germany), Palantir (US), Oracle (US), ServiceNow (US), Databricks (US), OpenAI (US), Altair (US), Dataiku (US), Cohere (Canada), H2O.ai (US), Vital AI (US), Rainbird Technologies (UK), Arize AI (US), CalypsoAI (US), Clarifai (US), Anyscale (US), Weights & Biases (US), Iguazio (Israel), Mistral AI (France), Baseten (US), Lightning AI (US), and Anthropic (US).

Research Coverage

This research report categorizes the AI platform market based on offering (platform type (AI development platforms, AI lifecycle management platforms, and AI infrastructure & enablement), and deployment mode (cloud & on-premises)), functionality (data management & preparation, model development & training, model deployment & serving, monitoring & maintenance, model governance & compliance, model fine-tuning & personalization, explainability & bias tools, and security & privacy), user type (data scientists & ML engineers, MLOps/AI engineers, business analysts & citizen developers, AI product managers, and IT & cloud architects), end user (individual and enterprises (healthcare & life sciences, BFSI, retail & e-commerce, transportation & logistics, automotive & mobility, telecommunications, government & defence, energy & utilities, manufacturing, software & technology, media and entertainment, and others), and region (North America, Europe, Asia Pacific, Middle East & Africa, and Latin America).

The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the AI platform market. A detailed analysis of the key industry players was done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, and mergers and acquisitions; and recent developments associated with the AI platform market. Competitive analysis of upcoming startups in the AI platform market ecosystem was also covered in this report.

Key Benefits of Buying the Report

The report would provide the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall AI platform market and its subsegments. It would help stakeholders understand the competitive landscape and gain more insights to better their business and plan suitable go-to-market strategies. It also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights into the following pointers:

- Analysis of key drivers (Demand for cross-model orchestration and agentic workflow integration, Adoption of domain-tuned foundation models with compliance-ready pipelines, Enterprise migration from model prototyping to productization), restraints (Platform redundancy and feature saturation, Lack of evaluation standards for generative AI, High inference and fine-tuning costs for SMEs), opportunities (Fusion of AI platforms with business automation stacks, Middleware abstraction for model interoperability, Accelerating AI development with privacy-first synthetic data), and challenges (Regulatory burden on model deployment and platform fatigue from toolchain fragmentation)

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the AI platform market

- Market Development: Comprehensive information about lucrative markets - analyzing the AI Platform market across varied regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the AI platform market

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players such as Google (US), Microsoft (US), IBM (US), Intel (US), Infosys (India), Wipro (India), Salesforce (US), HPE (US), Insight (US), NVIDIA (US), Alibaba Cloud (China), AWS (US), SAP (Germany), Palantir (US), Oracle (US), ServiceNow (US), Databricks (US), OpenAI (US), Altair (US), Dataiku (US), Cohere (Canada), H2O.ai (US), Vital AI (US), Rainbird Technologies (UK), Arize AI (US), CalypsoAI (US), Clarifai (US), Anyscale (US), Weights & Biases (US), Iguazio (Israel), Mistral AI (France), Baseten (US), Lightning AI (US), and Anthropic (US).

The report also helps stakeholders understand the pulse of the AI platform market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION AND SCOPE

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of primary participants

- 2.1.2.2 Breakdown of primaries

- 2.1.2.3 Key industry insights

- 2.2 MARKET BREAKUP AND DATA TRIANGULATION

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 TOP-DOWN APPROACH

- 2.3.2 BOTTOM-UP APPROACH

- 2.4 MARKET FORECAST

- 2.5 RESEARCH ASSUMPTIONS

- 2.6 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN AI PLATFORM MARKET

- 4.2 AI PLATFORM MARKET: TOP THREE FUNCTIONALITIES

- 4.3 NORTH AMERICA: AI PLATFORM MARKET, BY OFFERING AND FUNCTIONALITY

- 4.4 AI PLATFORM MARKET, BY REGION

5 MARKET OVERVIEW AND INDUSTRY TRENDS

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Demand for cross-model orchestration and agentic workflow integration

- 5.2.1.2 Adoption of domain-tuned foundation models with compliance-ready pipelines

- 5.2.1.3 Enterprise migration from model prototyping to productization

- 5.2.2 RESTRAINTS

- 5.2.2.1 Platform redundancy and feature saturation

- 5.2.2.2 Lack of evaluation standards for generative AI

- 5.2.2.3 High inference and fine-tuning costs for SMEs

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Fusion of AI platforms with business automation stacks

- 5.2.3.2 Middleware abstraction for model interoperability

- 5.2.3.3 Accelerating AI development with privacy-first synthetic data

- 5.2.4 CHALLENGES

- 5.2.4.1 Regulatory burden on model deployment

- 5.2.4.2 Platform fatigue from toolchain fragmentation

- 5.2.1 DRIVERS

- 5.3 EVOLUTION OF AI PLATFORM MARKET

- 5.4 SUPPLY CHAIN ANALYSIS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 AI PLATFORM MARKET, BY OFFERING

- 5.5.1.1 AI Development Platforms

- 5.5.1.2 AI Lifecycle Management Platforms

- 5.5.1.3 AI Infrastructure & Enablement

- 5.5.1 AI PLATFORM MARKET, BY OFFERING

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 KEY TECHNOLOGIES

- 5.6.1.1 Generative AI

- 5.6.1.2 Autonomous AI & Autonomous Agents

- 5.6.1.3 AutoML

- 5.6.1.4 Causal AI

- 5.6.1.5 MLOps

- 5.6.2 COMPLEMENTARY TECHNOLOGIES

- 5.6.2.1 Blockchain

- 5.6.2.2 Edge Computing

- 5.6.2.3 Cybersecurity

- 5.6.3 ADJACENT TECHNOLOGIES

- 5.6.3.1 Predictive Analytics

- 5.6.3.2 IoT

- 5.6.3.3 Big Data

- 5.6.3.4 Augmented Reality/Virtual Reality

- 5.6.1 KEY TECHNOLOGIES

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 CASE STUDY 1: IMERYS DEPLOYED ENTERPRISE AI CHAT TO BOOST PRODUCTIVITY AND DATA ACCESS

- 5.7.2 CASE STUDY 2: BASISAI AUTOMATED ML DEPLOYMENT TO SPEED UP AI DEVELOPMENT LIFECYCLE

- 5.7.3 CASE STUDY 3: AT&T LEVERAGED AI PLATFORM TO COMBAT FRAUD AND IMPROVE NETWORK EFFICIENCY

- 5.7.4 CASE STUDY 4: BMW DEPLOYED GEN AI FOR SMARTER PROCUREMENT ANALYSIS

- 5.7.5 CASE STUDY 5: MOVEWORKS DEPLOYED AI PLATFORM TO AUTOMATE EMPLOYEE SUPPORT AT SCALE

- 5.8 PORTER'S FIVE FORCES ANALYSIS

- 5.8.1 THREAT OF NEW ENTRANTS

- 5.8.2 THREAT OF SUBSTITUTES

- 5.8.3 BARGAINING POWER OF SUPPLIERS

- 5.8.4 BARGAINING POWER OF BUYERS

- 5.8.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.9 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.10 REGULATORY LANDSCAPE

- 5.10.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.10.2 REGULATIONS: ARTIFICIAL INTELLIGENCE

- 5.10.2.1 North America

- 5.10.2.1.1 SCR 17: Artificial Intelligence Bill (California)

- 5.10.2.1.2 S1103: Artificial Intelligence Automated Decision Bill (Connecticut)

- 5.10.2.1.3 National Artificial Intelligence Initiative Act (NAIIA)

- 5.10.2.1.4 The Artificial Intelligence and Data Act (AIDA) - Canada

- 5.10.2.2 Europe

- 5.10.2.2.1 The European Union (EU) - Artificial Intelligence Act (AIA)

- 5.10.2.2.2 General Data Protection Regulation (Europe)

- 5.10.2.3 Asia Pacific

- 5.10.2.3.1 Interim Administrative Measures for Generative Artificial Intelligence Services (China)

- 5.10.2.3.2 The National AI Strategy (Singapore)

- 5.10.2.3.3 The Hiroshima AI Process Comprehensive Policy Framework (Japan)

- 5.10.2.4 Middle East & Africa

- 5.10.2.4.1 The National Strategy for Artificial Intelligence (UAE)

- 5.10.2.4.2 Impact on AI Platform Market

- 5.10.2.4.3 The National Artificial Intelligence Strategy (Qatar)

- 5.10.2.4.4 Impact on AI Platform Market

- 5.10.2.4.5 The AI Ethics Principles and Guidelines (Dubai)

- 5.10.2.4.6 Impact on AI Platform Market

- 5.10.2.5 Latin America

- 5.10.2.5.1 The Santiago Declaration (Chile)

- 5.10.2.5.2 The Brazilian Artificial Intelligence Strategy (EBIA)

- 5.10.2.1 North America

- 5.11 PATENT ANALYSIS

- 5.11.1 METHODOLOGY

- 5.11.2 PATENTS FILED, BY DOCUMENT TYPE

- 5.11.3 INNOVATION AND PATENT APPLICATIONS

- 5.12 INVESTMENT AND FUNDING SCENARIO

- 5.13 PRICING ANALYSIS

- 5.13.1 AVERAGE SELLING PRICE OF OFFERING, BY KEY PLAYER, 2025

- 5.13.2 INDICATIVE PRICING ANALYSIS, BY FUNCTIONALITY, 2025

- 5.14 KEY CONFERENCES AND EVENTS (2025-2026)

- 5.15 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.15.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.15.2 BUYING CRITERIA

- 5.16 CUSTOMER SEGMENTATION & BUYER PERSONAS

- 5.16.1 KEY BUYER ARCHETYPES

- 5.16.2 KEY INDUSTRY-SPECIFIC BUYER SEGMENTATION

- 5.16.3 BUYER JOURNEY MAPPING

- 5.17 TECHNOLOGY ROADMAP & INNOVATION DIRECTIONS

- 5.17.1 TECHNOLOGY ROADMAP & CAPABILITY AREA

- 5.17.2 AI PLATFORM CAPABILITY MATURITY FRAMEWORK

- 5.18 PARTNERSHIPS & ECOSYSTEM STRATEGIES

- 5.18.1 PARTNERSHIPS & ECOSYSTEM STRATEGIES

- 5.19 KEY SUCCESS FACTORS FOR BUYERS

- 5.19.1 CHECKLIST FOR SUSTAINABLE AND STRATEGIC AI PLATFORM INVESTMENTS

6 AI PLATFORM MARKET, BY OFFERING

- 6.1 INTRODUCTION

- 6.1.1 OFFERINGS: AI PLATFORM MARKET DRIVERS

- 6.2 AI DEVELOPMENT PLATFORMS

- 6.2.1 AI DEVELOPMENT PLATFORMS EMPOWER FASTER, SCALABLE AI APPLICATION DEVELOPMENT, DRIVING INNOVATION AND OPERATIONAL EFFICIENCY ACROSS INDUSTRIES

- 6.2.2 DEEP LEARNING PLATFORMS

- 6.2.3 GENERATIVE AI PLATFORMS

- 6.2.4 CONVERSATIONAL AI PLATFORMS

- 6.2.5 EDGE AI PLATFORMS

- 6.2.6 AI AGENT PLATFORMS

- 6.2.7 ANNOTATION & DATA LABELING PLATFORMS

- 6.2.8 OPEN-SOURCE MODEL PLATFORMS

- 6.3 AI LIFECYCLE MANAGEMENT PLATFORMS

- 6.3.1 AI LIFECYCLE MANAGEMENT PLATFORMS ENSURE SCALABLE, COMPLIANT, AND RELIABLE AI DEPLOYMENTS, DRIVING ENTERPRISE READINESS FOR PRODUCTION-GRADE AI

- 6.3.2 MLOPS PLATFORMS

- 6.3.3 LLMOPS PLATFORMS

- 6.3.4 MODEL EVALUATION & GOVERNANCE PLATFORMS

- 6.3.5 DRIFT DETECTION & MONITORING PLATFORMS

- 6.3.6 EXPLAINABILITY & RESPONSIBLE AI TOOLS

- 6.4 AI ENABLEMENT SERVICES

- 6.4.1 AI ENABLEMENT SERVICES GUIDE ENTERPRISES THROUGH STRATEGY, DEPLOYMENT, AND MANAGEMENT OF AI, ACCELERATING ADOPTION WHILE REDUCING RISKS AND COMPLEXITIES

- 6.4.2 STRATEGIC AI PLANNING

- 6.4.3 MODEL DEVELOPMENT & DEPLOYMENT

- 6.4.4 MODEL IMPLEMENTATION & MAINTENANCE

- 6.4.5 DISCOVERY AND EVALUATION

7 AI PLATFORM MARKET, BY FUNCTIONALITY

- 7.1 INTRODUCTION

- 7.1.1 FUNCTIONALITIES: AI PLATFORM MARKET DRIVERS

- 7.2 DATA MANAGEMENT & PREPARATION

- 7.2.1 ENABLE ACCURATE, COMPLIANT, AND SCALABLE AI PROJECTS WITH STRONG DATA MANAGEMENT AND PREPARATION TOOLS

- 7.3 MODEL DEVELOPMENT & TRAINING

- 7.3.1 ACCELERATE AI INNOVATION WITH EFFICIENT, SCALABLE, AND COLLABORATIVE MODEL DEVELOPMENT AND TRAINING CAPABILITIES

- 7.4 MODEL DEPLOYMENT & SERVING

- 7.4.1 ENSURE RELIABLE, FLEXIBLE, AND REAL-TIME AI DELIVERY WITH ADVANCED MODEL DEPLOYMENT AND SERVING FUNCTIONALITIES

- 7.5 MONITORING & MAINTENANCE

- 7.5.1 MAINTAIN HIGH-PERFORMING, RISK-RESILIENT AI SYSTEMS WITH PROACTIVE MONITORING AND MAINTENANCE TOOLS

- 7.6 MODEL GOVERNANCE & COMPLIANCE

- 7.6.1 ENSURE RESPONSIBLE, AUDITABLE, AND COMPLIANT AI OPERATIONS WITH EMBEDDED GOVERNANCE FUNCTIONALITIES

- 7.7 MODEL FINE-TUNING & PERSONALIZATION

- 7.7.1 ACHIEVE HIGHER ACCURACY AND PERSONALIZATION WITH EFFICIENT FINE-TUNING AND CUSTOMIZATION FUNCTIONALITIES

- 7.8 EXPLAINABILITY & BIAS TOOLS

- 7.8.1 ENHANCE AI TRUSTWORTHINESS AND FAIRNESS WITH ADVANCED EXPLAINABILITY AND BIAS MITIGATION TOOLS

- 7.9 SECURITY & PRIVACY

- 7.9.1 SECURE AI DEPLOYMENTS WITH PRIVACY-PRESERVING TECHNOLOGIES AND ROBUST CYBERSECURITY PROTECTIONS

8 AI PLATFORM MARKET, BY USER TYPE

- 8.1 INTRODUCTION

- 8.1.1 USER TYPES: AI PLATFORM MARKET DRIVERS

- 8.1.2 DATA SCIENTISTS & ML ENGINEERS

- 8.1.2.1 Building differentiated models using open frameworks and proprietary data

- 8.1.3 MLOPS/AI ENGINEERS

- 8.1.3.1 Automating lifecycle management for scalable model operations

- 8.1.4 BUSINESS ANALYSTS & CITIZEN DEVELOPERS

- 8.1.4.1 Unlocking business value through no-code AI enablement

- 8.1.5 AI PRODUCT MANAGERS

- 8.1.5.1 Connecting model performance to product and customer impact

- 8.1.6 IT & CLOUD ARCHITECTS

- 8.1.6.1 Deploying secure, compliant infrastructure for enterprise-scale AI

9 AI PLATFORM MARKET, BY END USER

- 9.1 INTRODUCTION

- 9.1.1 END USERS: AI PLATFORM MARKET DRIVERS

- 9.2 ENTERPRISES

- 9.2.1 HEALTHCARE & LIFE SCIENCES

- 9.2.1.1 AI platforms transforming healthcare and life sciences by enhancing diagnostics, accelerating drug development, and enabling personalized, data-driven care delivery

- 9.2.1.2 Healthcare providers

- 9.2.1.3 Pharmaceuticals & biotech sector

- 9.2.1.4 Medtech

- 9.2.2 BFSI

- 9.2.2.1 BFSI organizations leveraging AI platforms to drive intelligent automation, enhance fraud prevention, and offer personalized financial services at scale

- 9.2.2.2 Banking

- 9.2.2.3 Financial services

- 9.2.2.4 Insurance

- 9.2.3 RETAIL & E-COMMERCE

- 9.2.3.1 Retail & e-commerce firms use AI platforms to personalize customer journeys, streamline operations, and drive smarter inventory and pricing decisions.

- 9.2.4 TRANSPORTATION & LOGISTICS

- 9.2.4.1 AI enhances fleet efficiency and real-time supply chain visibility

- 9.2.5 AUTOMOTIVE & MOBILITY

- 9.2.5.1 AI platforms transforming automotive industry by enabling autonomous features, predictive maintenance, and real-time vehicle intelligence

- 9.2.6 TELECOMMUNICATIONS

- 9.2.6.1 Telecom companies use AI platforms to automate network management, enable predictive maintenance, and deploy intelligent customer services

- 9.2.7 GOVERNMENT & DEFENSE

- 9.2.7.1 AI platforms enabling governments and defense agencies to build secure, scalable AI solutions for intelligence, public safety, and operational planning

- 9.2.8 ENERGY & UTILITIES

- 9.2.8.1 AI platforms help energy and utility providers optimize grid operations, forecast demand, and manage assets through centralized, scalable model deployment

- 9.2.8.2 Oil and gas

- 9.2.8.3 Power generation

- 9.2.8.4 Utilities

- 9.2.9 MANUFACTURING

- 9.2.9.1 AI platforms enable manufacturers to automate production, predict equipment failures, and improve quality control

- 9.2.9.2 Discrete manufacturing

- 9.2.9.3 Process manufacturing

- 9.2.10 SOFTWARE & TECHNOLOGY

- 9.2.10.1 AI platforms accelerating model development, testing, and deployment for tech firms building intelligent applications

- 9.2.11 MEDIA & ENTERTAINMENT

- 9.2.11.1 AI platforms help media companies personalize content, automate editing, and optimize distribution

- 9.2.12 OTHER ENTERPRISE END USERS

- 9.2.1 HEALTHCARE & LIFE SCIENCES

- 9.3 INDIVIDUAL USERS

- 9.3.1 AI PLATFORMS EMPOWER INDIVIDUAL USERS WITH TOOLS FOR LOW-CODE MODEL BUILDING, DATA EXPLORATION, AND PERSONAL AUTOMATION

10 AI PLATFORM MARKET, BY REGION

- 10.1 INTRODUCTION

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: AI PLATFORM MARKET DRIVERS

- 10.2.2 NORTH AMERICA: MACROECONOMIC OUTLOOK

- 10.2.3 US

- 10.2.3.1 Federal mandates and hyperscaler innovation drive enterprise-grade AI platform adoption

- 10.2.4 CANADA

- 10.2.4.1 Ethical AI leadership and public-sector investments fuel Canada's pragmatic platform growth

- 10.3 EUROPE

- 10.3.1 EUROPE: AI PLATFORM MARKET DRIVERS

- 10.3.2 EUROPE: MACROECONOMIC OUTLOOK

- 10.3.3 UK

- 10.3.3.1 UK blends AI safety leadership with targeted platform deployment in health and finance

- 10.3.4 GERMANY

- 10.3.4.1 Germany integrates AI platforms into smart manufacturing via deep industrial digitalization

- 10.3.5 FRANCE

- 10.3.5.1 France prioritizes sovereign AI platforms with open-source momentum and industrial backing

- 10.3.6 ITALY

- 10.3.6.1 Driving integration of climate and environmental risks into financial governance in Italy

- 10.3.7 SPAIN

- 10.3.7.1 Spain champions inclusive AI platforms through public-sector innovation and smart logistics

- 10.3.8 REST OF EUROPE

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: AI PLATFORM MARKET DRIVERS

- 10.4.2 ASIA PACIFIC: MACROECONOMIC OUTLOOK

- 10.4.3 CHINA

- 10.4.3.1 China scales sovereign AI platforms across industries under national compute and LLM push

- 10.4.4 JAPAN

- 10.4.4.1 Japan focuses on trusted, explainable AI platforms for aging society and industrial resilience

- 10.4.5 INDIA

- 10.4.5.1 India advances inclusive, mobile-first AI platforms for public health, agriculture, and education

- 10.4.6 AUSTRALIA & NEW ZEALAND

- 10.4.6.1 Australia and New Zealand embed ethics and sustainability into government-led AI platforms

- 10.4.7 ASEAN

- 10.4.7.1 ASEAN scales modular AI platforms via SME enablement and regional policy coordination

- 10.4.8 SOUTH KOREA

- 10.4.8.1 South Korea drives enterprise-grade AI platforms with edge inferencing and HyperCLOVA integration

- 10.4.9 REST OF ASIA PACIFIC

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 MIDDLE EAST & AFRICA: AI PLATFORM MARKET DRIVERS

- 10.5.2 MIDDLE EAST & AFRICA: MACROECONOMIC OUTLOOK

- 10.5.3 SAUDI ARABIA

- 10.5.3.1 Sovereign AI investments and Arabic LLMs drive platform adoption across sectors

- 10.5.4 UNITED ARAB EMIRATES (UAE)

- 10.5.4.1 Innovation hubs and sovereign cloud investments accelerate AI platform commercialization

- 10.5.5 SOUTH AFRICA

- 10.5.5.1 Telecom-driven edge AI and enterprise digitalization expand platform opportunities

- 10.5.6 TURKEY

- 10.5.6.1 Public AI initiatives and academic R&D spur demand for ML platforms and edge AI

- 10.5.7 QATAR

- 10.5.7.1 State-driven AI adoption focuses on Arabic NLP and smart city platforms

- 10.5.8 EGYPT

- 10.5.8.1 AI platform adoption tied to public sector digitalization and telecom-led edge deployments

- 10.5.9 KUWAIT

- 10.5.9.1 Digital government initiatives drive demand for conversational AI and LLM platforms

- 10.5.10 REST OF MIDDLE EAST & AFRICA

- 10.6 LATIN AMERICA

- 10.6.1 LATIN AMERICA: AI PLATFORM MARKET DRIVERS

- 10.6.2 LATIN AMERICA: MACROECONOMIC OUTLOOK

- 10.6.3 BRAZIL

- 10.6.3.1 Digital government initiatives and enterprise AI investments drive platform commercialization

- 10.6.4 MEXICO

- 10.6.4.1 Financial services and public digitalization initiatives accelerate AI platform deployment

- 10.6.5 ARGENTINA

- 10.6.5.1 Public sector AI adoption and academic partnerships foster platform experimentation

- 10.6.6 CHILE

- 10.6.6.1 Public innovation programs and cloud expansion stimulate AI platform adoption

- 10.6.7 REST OF LATIN AMERICA

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2022-2025

- 11.3 REVENUE ANALYSIS, 2020-2024

- 11.4 MARKET SHARE ANALYSIS, 2024

- 11.4.1 MARKET RANKING ANALYSIS

- 11.5 PRODUCT COMPARATIVE ANALYSIS

- 11.5.1 PRODUCT COMPARATIVE ANALYSIS OF AI PLATFORMS

- 11.6 COMPANY VALUATION AND FINANCIAL METRICS

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2024

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- 11.7.5 COMPANY FOOTPRINT: KEY PLAYERS, 2024

- 11.7.5.1 Company Footprint

- 11.7.5.2 Regional Footprint

- 11.7.5.3 Offering Footprint

- 11.7.5.4 Functionality Footprint

- 11.7.5.5 End User Footprint

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2024

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2024

- 11.8.5.1 Detailed list of key startups/SMEs

- 11.8.5.2 Competitive benchmarking of key startups/SMEs

- 11.9 COMPANY EVALUATION MATRIX: AI ENABLEMENT SERVICES, 2024

- 11.9.1 PROGRESSIVE COMPANIES

- 11.9.2 RESPONSIVE COMPANIES

- 11.9.3 DYNAMIC COMPANIES

- 11.9.4 STARTING BLOCKS

- 11.9.5 COMPETITIVE BENCHMARKING: AI ENABLEMENT SERVICES, 2024

- 11.9.5.1 Detailed list of key AI enablement services

- 11.9.5.2 Competitive benchmarking of AI enablement services

- 11.10 COMPETITIVE SCENARIO AND TRENDS

- 11.10.1 PRODUCT LAUNCHES AND ENHANCEMENTS

- 11.10.2 DEALS

12 COMPANY PROFILES

- 12.1 INTRODUCTION

- 12.2 MAJOR PLAYERS

- 12.2.1 GOOGLE

- 12.2.1.1 Business overview

- 12.2.1.2 Products offered

- 12.2.1.3 Recent developments

- 12.2.1.4 MnM view

- 12.2.1.4.1 Key strengths/Right to win

- 12.2.1.4.2 Strategic choices

- 12.2.1.4.3 Weaknesses and competitive threats

- 12.2.2 MICROSOFT

- 12.2.2.1 Business overview

- 12.2.2.2 Products offered

- 12.2.2.3 Recent developments

- 12.2.2.4 MnM view

- 12.2.2.4.1 Key strengths/Right to win

- 12.2.2.4.2 Strategic choices

- 12.2.2.4.3 Weaknesses and competitive threats

- 12.2.3 IBM

- 12.2.3.1 Business overview

- 12.2.3.2 Products offered

- 12.2.3.3 Recent developments

- 12.2.3.4 MnM view

- 12.2.3.4.1 Key strengths/Right to win

- 12.2.3.4.2 Strategic choices

- 12.2.3.4.3 Weaknesses and competitive threats

- 12.2.4 ORACLE

- 12.2.4.1 Business overview

- 12.2.4.2 Products offered

- 12.2.4.3 Recent developments

- 12.2.4.4 MnM view

- 12.2.4.4.1 Key strengths/Right to win

- 12.2.4.4.2 Strategic choices

- 12.2.4.4.3 Weaknesses and competitive threats

- 12.2.5 AWS

- 12.2.5.1 Business overview

- 12.2.5.2 Products offered

- 12.2.5.3 Recent developments

- 12.2.5.4 MnM view

- 12.2.5.4.1 Key strengths/Right to win

- 12.2.5.4.2 Strategic choices

- 12.2.5.4.3 Weaknesses and competitive threats

- 12.2.6 INTEL

- 12.2.6.1 Business overview

- 12.2.6.2 Products offered

- 12.2.6.3 Recent developments

- 12.2.7 SALESFORCE

- 12.2.7.1 Business overview

- 12.2.7.2 Products offered

- 12.2.7.3 Recent developments

- 12.2.8 SAP

- 12.2.8.1 Business overview

- 12.2.8.2 Products offered

- 12.2.8.3 Recent developments

- 12.2.9 SERVICENOW

- 12.2.9.1 Business overview

- 12.2.9.2 Products offered

- 12.2.9.3 Recent developments

- 12.2.10 NVIDIA

- 12.2.10.1 Business overview

- 12.2.10.2 Products offered

- 12.2.10.3 Recent developments

- 12.2.11 OPENAI

- 12.2.12 ALIBABA CLOUD

- 12.2.13 HPE

- 12.2.14 DATABRICKS

- 12.2.15 INSIGHT

- 12.2.16 PALANTIR

- 12.2.17 ALTAIR

- 12.2.18 DATAIKU

- 12.2.1 GOOGLE

- 12.3 STARTUP/SME PROFILES

- 12.3.1 H2O.AI

- 12.3.2 ANTHROPIC

- 12.3.3 COHERE

- 12.3.4 ANYSCALE

- 12.3.5 DATAROBOT

- 12.3.6 VITAL AI

- 12.3.7 RAINBIRD TECHNOLOGIES

- 12.3.8 ARIZE AI

- 12.3.9 CALYPSOAI

- 12.3.10 CLARIFAI

- 12.3.11 WEIGHTS & BIASES

- 12.3.12 ELVEX

- 12.3.13 IGUAZIO

- 12.3.14 MISTRAL AI

- 12.3.15 BASETEN

- 12.3.16 LIGHTNING AI

- 12.3.17 PROWESS CONSULTING

- 12.3.18 DEVTECH

- 12.3.19 ZYXWARE TECHNOLOGIES

- 12.3.20 FLUIDONE

- 12.3.21 AHELIOTECH

- 12.3.22 ORIL

- 12.3.23 CONVERSANT SOLUTIONS

13 ADJACENT AND RELATED MARKETS

- 13.1 INTRODUCTION

- 13.2 AI TOOLKIT MARKET - GLOBAL FORECAST TO 2028

- 13.2.1 MARKET DEFINITION

- 13.2.2 MARKET OVERVIEW

- 13.2.2.1 AI toolkit market, by offering

- 13.2.2.2 AI toolkit market, by technology

- 13.2.2.3 AI toolkit market, by vertical

- 13.2.2.4 AI toolkit market, by region

- 13.3 NO-CODE AI PLATFORMS MARKET - GLOBAL FORECAST TO 2029

- 13.3.1 MARKET DEFINITION

- 13.3.2 MARKET OVERVIEW

- 13.3.2.1 No-code AI platforms market, by offering

- 13.3.2.2 No-code AI platforms market, by technology

- 13.3.2.3 No-code AI platforms market, by data modality

- 13.3.2.4 No-code AI platforms market, by application

- 13.3.2.5 No-code AI platforms market, by vertical

- 13.3.2.6 No-code AI platforms market, by region

14 APPENDIX

- 14.1 DISCUSSION GUIDE

- 14.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 14.3 CUSTOMIZATION OPTIONS

- 14.4 RELATED REPORTS

- 14.5 AUTHOR DETAILS

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 325 Pages

- 納期

- 即納可能