|

|

市場調査レポート

商品コード

1538583

防音材市場:素材別、最終用途産業別、地域別 - 2029年までの予測Acoustic Insulation Market by Material (Glass Wool, Rock Wool, Foamed Plastic, Elastomeric Foam), End-Use Industry (Building & Construction, Transportation, Oil & Gas, Energy & Utilities, Industrial & OEM), and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 防音材市場:素材別、最終用途産業別、地域別 - 2029年までの予測 |

|

出版日: 2024年08月19日

発行: MarketsandMarkets

ページ情報: 英文 239 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

防音材の市場規模は、2024年の162億米ドルから4.8%のCAGRで拡大し、2029年には204億米ドルに達すると予測されています。

都市化とインフラ開発が世界の防音材市場を促進しています。世界的に建設産業は主要な経済牽引役です。新興諸国では建設業はGDPの約8%に寄与していますが、先進国では約5%を占めています。中東・アフリカやアジア太平洋のような地域は、建設産業を活用して経済を前進させています。インドでは、建設セクターは主要経済セクターの中で第3位であり、農業に次いで第2位の雇用を生み出しています。都市化とインフラ整備が加速するにつれて、快適性と生産性を確保するための防音に対する需要が高まっています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2021年~2022年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 検討単位 | 金額(10億米ドル)、数量(キロトン) |

| セグメント | 素材別、最終用途産業別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

ポリスチレンとポリウレタンフォームを中心とする発泡プラスチックは、最も広範囲に適用され効率的な音響材料の1つです。発泡プラスチックは、住宅でもオフィスでも、その軽量さと防音効率の高さから多くの支持を得ています。これは、吸音性能を向上させるだけでなく、断熱性も向上させるためです。発泡プラスチックは、さまざまな建築コンセプトのスペースに簡単に取り付けることができ、環境の音響・熱パラメータを向上させるソリューションです。

防音材の最大の消費分野は建築・建設で、これは防音材の主要な最終用途であり、室内の音響的快適性を向上させ、音の迷惑を減少させるように設計された構造の実行に関与します。住環境や作業環境を向上させるという観点から、防音によって他の部屋から入ってくる空気伝播音や、部屋や建物の外から入ってくる衝撃音の影響を低減できることは知っておく価値があります。住宅では、壁、床、天井に防音材を施工することで、プライバシーを確保し、雑音を遮断することができます。オフィス、ホテル、ヘルスケア施設では、生産的で快適な作業環境、休息環境、癒しの環境を作り出すのに適しているため、構造物に防音材が必要です。さらに、防音は様々な種類の建築物における許容騒音レベルに関する法的要件に準拠する役割を果たします。つまり、建設プロジェクトでは、防音材料や防音ツールを建設プロジェクトに取り入れることで、これらの基準をカバーすることができ、建物の品質や価値を向上させることができるのです。また、防音は、最新の材料によるエネルギー性能の向上や騒音伝達の減少に基づく持続可能な解決策にも貢献します。人口の増加や大規模な建築物の出現により、建築や改築において防音間仕切りが考慮されるようになり、建築物における防音の重要性が確立されつつあります。

当レポートでは、世界の防音材市場について調査し、素材別、最終用途産業別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

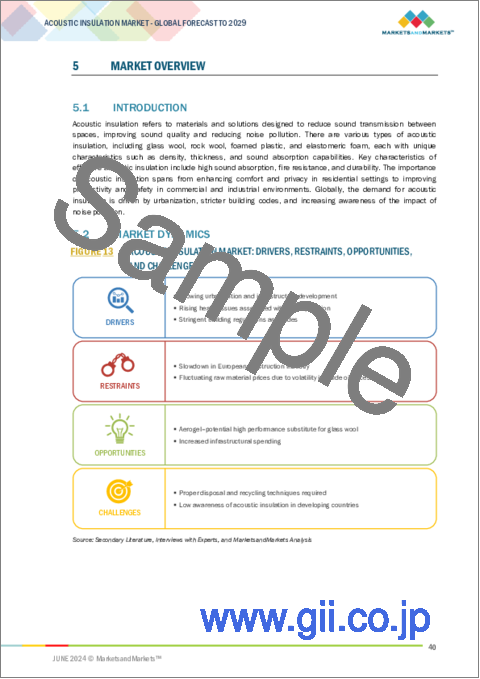

第5章 市場概要

- イントロダクション

- 市場力学

- バリューチェーン分析

- ポーターのファイブフォース分析

- 特許分析

- エコシステム/市場マップ

- 貿易分析

- 価格分析

- マクロ経済の概要と主な動向

- 技術分析

- 関税と規制状況

- 顧客のビジネスに影響を与える動向/混乱

- 2024年~2025年の主な会議とイベント

- 主な利害関係者と購入基準

- ケーススタディ分析

- 投資と資金調達のシナリオ

- 使用事例/用途別の資金調達

- AI/生成AIが防音材市場に与える影響

第6章 防音材市場(素材別)

- イントロダクション

- 発泡プラスチック

- グラスウール

- ロックウール

- エラストマーフォーム

- その他

第7章 防音材市場(最終用途産業別)

- イントロダクション

- 建築・建設

- 輸送

- 石油・ガス・石油化学

- エネルギー・ユーティリティ

- 産業用・OEM

第8章 防音材市場(地域別)

- イントロダクション

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- 南米

第9章 競合情勢

- 概要

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- 企業価値評価と財務指標

- ブランド/製品比較分析

- 企業評価マトリックス:主要参入企業、2023年

- 企業評価マトリックス:スタートアップ/中小企業、2023年

- 競合シナリオと動向

第10章 企業プロファイル

- 主要参入企業

- SAINT-GOBAIN

- KNAUF INSULATION

- ARMACELL

- SOPREMA

- ROCKWOOL A/S

- HUNTSMAN INTERNATIONAL LLC

- OWENS CORNING

- KINGSPAN GROUP

- BASF SE

- JOHNS MANVILLE

- その他の企業

- GETZNER WERKSTOFFE GMBH

- CELLOFOAM INTERNATIONAL GMBH & CO. KG

- REGUPOL GERMANY GMBH & CO. KG

- 3M

- TRELLEBORG

- L'ISOLANTE K-FLEX S.P.A.

- DOW

- SIDERISE

- CABOT CORPORATION

- FLETCHER INSULATION

- HUSH ACOUSTICS

- PRIMACOUSTIC

- TROCELLEN

- CELLECTA

- INTERNATIONAL CELLULOSE CORPORATION

第11章 付録

List of Tables

- TABLE 1 ACOUSTIC INSULATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 2 ACOUSTIC INSULATION: ECOSYSTEM

- TABLE 3 AVERAGE SELLING PRICE OF KEY PLAYERS FOR TOP 3 END-USE INDUSTRIES (USD/KG)

- TABLE 4 PROJECTED REAL GDP GROWTH (ANNUAL PERCENTAGE CHANGE) OF KEY COUNTRIES, 2023-2029

- TABLE 5 MINIMUM PERMISSIBLE AIRBORNE SOUND INSULATION INDICES

- TABLE 6 LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 7 ACOUSTIC INSULATION MARKET: KEY CONFERENCES & EVENTS, 2024-2025

- TABLE 8 INFLUENCE OF INSTITUTIONAL BUYERS ON BUYING PROCESS FOR TOP 3 END-USE INDUSTRIES

- TABLE 9 KEY BUYING CRITERIA FOR TOP 3 END-USE INDUSTRIES

- TABLE 10 ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 11 ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- TABLE 12 ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (KILOTON)

- TABLE 13 ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (KILOTON)

- TABLE 14 ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 15 ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 16 ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 17 ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 18 VEHICLE PRODUCTION STATISTICS, BY COUNTRY, 2021-2023 (UNITS)

- TABLE 19 ACOUSTIC INSULATION MARKET, BY REGION, 2021-2023 (USD MILLION)

- TABLE 20 ACOUSTIC INSULATION MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 21 ACOUSTIC INSULATION MARKET, BY REGION, 2021-2023 (KILOTON)

- TABLE 22 ACOUSTIC INSULATION MARKET, BY REGION, 2024-2029 (KILOTON)

- TABLE 23 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 24 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 25 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 26 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 27 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 28 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- TABLE 29 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (KILOTON)

- TABLE 30 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (KILOTON)

- TABLE 31 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 32 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 33 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 34 NORTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 35 US: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 36 US: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 37 US: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 38 US: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 39 CANADA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 40 CANADA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 41 CANADA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 42 CANADA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 43 MEXICO: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 44 MEXICO: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 45 MEXICO: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 46 MEXICO: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 47 EUROPE: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 48 EUROPE: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 49 EUROPE: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 50 EUROPE: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 51 EUROPE: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 52 EUROPE: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- TABLE 53 EUROPE: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (KILOTON)

- TABLE 54 EUROPE: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (KILOTON)

- TABLE 55 EUROPE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 56 EUROPE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 57 EUROPE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 58 EUROPE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 59 GERMANY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 60 GERMANY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 61 GERMANY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 62 GERMANY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 63 FRANCE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 64 FRANCE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 65 FRANCE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 66 FRANCE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 67 UK: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 68 UK: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 69 UK: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 70 UK: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 71 ITALY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 72 ITALY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 73 ITALY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 74 ITALY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 75 SPAIN: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 76 SPAIN: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 77 SPAIN: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 78 SPAIN: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 79 NORDIC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 80 NORDIC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 81 NORDIC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 82 NORDIC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 83 BENELUX: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 84 BENELUX: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 85 BENELUX: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 86 BENELUX: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 87 POLAND: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 88 POLAND: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 89 POLAND: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 90 POLAND: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 91 SWITZERLAND: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 92 SWITZERLAND: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 93 SWITZERLAND: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 94 SWITZERLAND: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 95 REST OF EUROPE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 96 REST OF EUROPE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 97 REST OF EUROPE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 98 REST OF EUROPE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 99 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 100 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 101 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 102 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 103 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 104 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- TABLE 105 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (KILOTON)

- TABLE 106 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (KILOTON)

- TABLE 107 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 108 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 109 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 110 ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 111 CHINA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 112 CHINA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 113 CHINA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 114 CHINA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 115 JAPAN: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 116 JAPAN: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 117 JAPAN: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 118 JAPAN: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 119 SOUTH KOREA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 120 SOUTH KOREA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 121 SOUTH KOREA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 122 SOUTH KOREA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 123 INDIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 124 INDIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 125 INDIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 126 INDIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 127 AUSTRALIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 128 AUSTRALIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 129 AUSTRALIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 130 AUSTRALIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 131 ASEAN COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 132 ASEAN COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 133 ASEAN COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 134 ASEAN COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 135 REST OF ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 136 REST OF ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 137 REST OF ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 138 REST OF ASIA PACIFIC: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 139 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 140 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 141 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 142 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 143 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 144 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- TABLE 145 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (KILOTON)

- TABLE 146 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (KILOTON)

- TABLE 147 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 148 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 149 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 150 MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 151 GCC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 152 GCC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 153 GCC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 154 GCC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 155 SAUDI ARABIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 156 SAUDI ARABIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 157 SAUDI ARABIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 158 SAUDI ARABIA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 159 UAE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 160 UAE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 161 UAE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 162 UAE: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 163 REST OF GCC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 164 REST OF GCC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 165 REST OF GCC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 166 REST OF GCC COUNTRIES: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 167 TURKEY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 168 TURKEY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 169 TURKEY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 170 TURKEY: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 171 REST OF MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 172 REST OF MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 173 REST OF MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 174 REST OF MIDDLE EAST & AFRICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 175 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (USD MILLION)

- TABLE 176 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 177 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2021-2023 (KILOTON)

- TABLE 178 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

- TABLE 179 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (USD MILLION)

- TABLE 180 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (USD MILLION)

- TABLE 181 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2021-2023 (KILOTON)

- TABLE 182 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024-2029 (KILOTON)

- TABLE 183 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 184 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 185 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 186 SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 187 BRAZIL: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 188 BRAZIL: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 189 BRAZIL: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 190 BRAZIL: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 191 ARGENTINA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 192 ARGENTINA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 193 ARGENTINA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 194 ARGENTINA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 195 REST OF SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (USD MILLION)

- TABLE 196 REST OF SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (USD MILLION)

- TABLE 197 REST OF SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2021-2023 (KILOTON)

- TABLE 198 REST OF SOUTH AMERICA: ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024-2029 (KILOTON)

- TABLE 199 THREE-YEAR REVENUE ANALYSIS OF KEY COMPANIES IN ACOUSTIC INSULATION MARKET

- TABLE 200 ACOUSTIC INSULATION MARKET: DEGREE OF COMPETITION

- TABLE 201 ACOUSTIC INSULATION MARKET: COMPANY FOOTPRINT

- TABLE 202 ACOUSTIC INSULATION MARKET: MATERIAL FOOTPRINT

- TABLE 203 ACOUSTIC INSULATION MARKET: END-USE FOOTPRINT

- TABLE 204 ACOUSTIC INSULATION MARKET: REGION FOOTPRINT

- TABLE 205 ACOUSTIC INSULATION MARKET: KEY STARTUPS/SMES

- TABLE 206 ACOUSTIC INSULATION MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- TABLE 207 ACOUSTIC INSULATION MARKET: PRODUCT LAUNCHES, JANUARY 2019-JUNE 2024

- TABLE 208 ACOUSTIC INSULATION MARKET: DEALS, JANUARY 2019-JUNE 2024

- TABLE 209 ACOUSTIC INSULATION MARKET: EXPANSIONS, JANUARY 2019-JUNE 2024

- TABLE 210 SAINT-GOBAIN: COMPANY OVERVIEW

- TABLE 211 SAINT-GOBAIN: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 212 SAINT-GOBAIN: PRODUCT LAUNCHES, JANUARY 2019-JUNE 2024

- TABLE 213 SAINT-GOBAIN: DEALS, JANUARY 2019-JUNE 2024

- TABLE 214 SAINT-GOBAIN: EXPANSIONS, JANUARY 2019-JUNE 2024

- TABLE 215 KNAUF INSULATION: COMPANY OVERVIEW

- TABLE 216 KNAUF INSULATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 217 KNAUF INSULATION: EXPANSIONS, JANUARY 2019-JUNE 2024

- TABLE 218 ARMACELL: COMPANY OVERVIEW

- TABLE 219 ARMACELL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 220 ARMACELL: PRODUCT LAUNCHES, JANUARY 2019-JUNE 2024

- TABLE 221 ARMACELL: DEALS, JANUARY 2019-JUNE 2024

- TABLE 222 ARMACELL: EXPANSIONS, JANUARY 2019-JUNE 2024

- TABLE 223 SOPREMA: COMPANY OVERVIEW

- TABLE 224 SOPREMA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 225 SOPREMA: EXPANSIONS, JANUARY 2019-JUNE 2024

- TABLE 226 ROCKWOOL A/S: COMPANY OVERVIEW

- TABLE 227 ROCKWOOL A/S: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 228 ROCKWOOL A/S: PRODUCT LAUNCHES, JANUARY 2019-JUNE 2024

- TABLE 229 ROCKWOOL A/S: DEALS, JANUARY 2019-JUNE 2024

- TABLE 230 ROCKWOOL A/S: EXPANSIONS, JANUARY 2019-JUNE 2024

- TABLE 231 HUNTSMAN INTERNATIONAL LLC: COMPANY OVERVIEW

- TABLE 232 HUNTSMAN INTERNATIONAL LLC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 233 HUNTSMAN INTERNATIONAL LLC: DEALS, JANUARY 2019-JUNE 2024

- TABLE 234 HUNTSMAN INTERNATIONAL LLC: EXPANSIONS, JANUARY 2019-JUNE 2024

- TABLE 235 OWENS CORNING: COMPANY OVERVIEW

- TABLE 236 OWENS CORNING: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 237 OWENS CORNING: PRODUCT LAUNCHES, JANUARY 2019-JUNE 2024

- TABLE 238 OWENS CORNING: DEALS, JANUARY 2019-JUNE 2024

- TABLE 239 KINGSPAN GROUP: COMPANY OVERVIEW

- TABLE 240 KINGSPAN GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 KINGSPAN GROUP: DEALS, JANUARY 2019-JUNE 2024

- TABLE 242 BASF SE: COMPANY OVERVIEW

- TABLE 243 BASF SE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 244 BASF SE: PRODUCT LAUNCHES, JANUARY 2019-JUNE 2024

- TABLE 245 JOHNS MANVILLE: COMPANY OVERVIEW

- TABLE 246 JOHNS MANVILLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 247 JOHNS MANVILLE: PRODUCT LAUNCHES, JANUARY 2019-JUNE 2024

- TABLE 248 JOHNS MANVILLE: EXPANSIONS, JANUARY 2019-JUNE 2024

- TABLE 249 GETZNER WERKSTOFFE GMBH: COMPANY OVERVIEW

- TABLE 250 CELLOFOAM INTERNATIONAL GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 251 REGUPOL GERMANY GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 252 3M: COMPANY OVERVIEW

- TABLE 253 TRELLEBORG: COMPANY OVERVIEW

- TABLE 254 L'ISOLANTE K-FLEX S.P.A.: COMPANY OVERVIEW

- TABLE 255 DOW: COMPANY OVERVIEW

- TABLE 256 SIDERISE: COMPANY OVERVIEW

- TABLE 257 CABOT CORPORATION: COMPANY OVERVIEW

- TABLE 258 FLETCHER INSULATION: COMPANY OVERVIEW

- TABLE 259 HUSH ACOUSTICS: COMPANY OVERVIEW

- TABLE 260 PRIMACOUSTIC: COMPANY OVERVIEW

- TABLE 261 TROCELLEN: COMPANY OVERVIEW

- TABLE 262 CELLECTA: COMPANY OVERVIEW

- TABLE 263 INTERNATIONAL CELLULOSE CORPORATION: COMPANY OVERVIEW

List of Figures

- FIGURE 1 ACOUSTIC INSULATION MARKET: RESEARCH DESIGN

- FIGURE 2 ACOUSTIC INSULATION MARKET: BOTTOM-UP APPROACH

- FIGURE 3 ACOUSTIC INSULATION MARKET: TOP-DOWN APPROACH

- FIGURE 4 DEMAND-SIDE FORECAST PROJECTIONS

- FIGURE 5 ACOUSTIC INSULATION MARKET: DATA TRIANGULATION

- FIGURE 6 GLASS WOOL SEGMENT TO CONTINUE TO DOMINATE MARKET IN 2029

- FIGURE 7 BUILDING & CONSTRUCTION-LARGEST END-USE INDUSTRY SEGMENT IN 2024

- FIGURE 8 ASIA PACIFIC TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- FIGURE 9 EMERGING ECONOMIES TO WITNESS HIGH GROWTH

- FIGURE 10 BUILDING & CONSTRUCTION SEGMENT TO CONTINUE TO DOMINATE MARKET IN 2029

- FIGURE 11 GLASS WOOL TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 12 INDIA TO LEAD OVERALL MARKET DURING FORECAST PERIOD

- FIGURE 13 ACOUSTIC INSULATION MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 14 ACOUSTIC INSULATION MARKET: VALUE CHAIN ANALYSIS

- FIGURE 15 ACOUSTIC INSULATION MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 16 NUMBER OF GRANTED PATENTS, PATENT APPLICATIONS, AND LIMITED PATENTS

- FIGURE 17 TOP 10 COMPANIES/APPLICANTS

- FIGURE 18 ACOUSTIC INSULATION MARKET ECOSYSTEM

- FIGURE 19 IMPORT OF SLAG WOOL, ROCK WOOL, AND SIMILAR MINERAL WOOLS, INCLUDING INTERMIXTURES THEREOF, IN BULK, SHEETS, OR ROLLS, BY KEY COUNTRY, 2019-2023 (USD THOUSAND)

- FIGURE 20 EXPORT OF SLAG WOOL, ROCK WOOL, AND SIMILAR MINERAL WOOLS, INCLUDING INTERMIXTURES THEREOF, IN BULK, SHEETS, OR ROLLS, BY KEY COUNTRY, 2019-2023 (USD THOUSAND)

- FIGURE 21 AVERAGE SELLING PRICE, BY REGION (USD/KG)

- FIGURE 22 AVERAGE SELLING PRICE, BY MARKET PLAYER (USD/KG)

- FIGURE 23 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS IN ACOUSTIC INSULATION MARKET

- FIGURE 24 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 END-USE INDUSTRIES

- FIGURE 25 SUPPLIER SELECTION CRITERIA

- FIGURE 26 INVESTMENT AND FUNDING SCENARIO

- FIGURE 27 FUNDING, BY USE CASE/APPLICATION

- FIGURE 28 GLASS WOOL SEGMENT TO DOMINATE MARKET IN 2024

- FIGURE 29 BUILDING & CONSTRUCTION SEGMENT TO REGISTER HIGHEST GROWTH BETWEEN 2024 AND 2029

- FIGURE 30 INDIA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 31 NORTH AMERICA: ACOUSTIC INSULATION MARKET SNAPSHOT

- FIGURE 32 EUROPE: ACOUSTIC INSULATION MARKET SNAPSHOT

- FIGURE 33 ASIA PACIFIC: ACOUSTIC INSULATION MARKET SNAPSHOT

- FIGURE 34 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN ACOUSTIC INSULATION MARKET BETWEEN JANUARY 2019 AND JUNE 2024

- FIGURE 35 REVENUE ANALYSIS OF KEY COMPANIES IN ACOUSTIC INSULATION MARKET, 2021-2023 (USD BILLION)

- FIGURE 36 SHARES OF TOP PLAYERS IN ACOUSTIC INSULATION MARKET, 2023

- FIGURE 37 COMPANY VALUATION OF LEADING COMPANIES IN ACOUSTIC INSULATION MARKET, 2023 (USD BILLION)

- FIGURE 38 FINANCIAL METRICS OF LEADING COMPANIES IN ACOUSTIC INSULATION MARKET, 2023

- FIGURE 39 ACOUSTIC INSULATION MARKET: BRAND/PRODUCT COMPARISON

- FIGURE 40 ACOUSTIC INSULATION MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 41 ACOUSTIC INSULATION MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- FIGURE 42 SAINT-GOBAIN: COMPANY SNAPSHOT

- FIGURE 43 ARMACELL: COMPANY SNAPSHOT

- FIGURE 44 ROCKWOOL A/S: COMPANY SNAPSHOT

- FIGURE 45 HUNTSMAN INTERNATIONAL LLC: COMPANY SNAPSHOT

- FIGURE 46 OWENS CORNING: COMPANY SNAPSHOT

- FIGURE 47 KINGSPAN GROUP: COMPANY SNAPSHOT

- FIGURE 48 BASF SE: COMPANY SNAPSHOT

The acoustic insulation market is projected to reach USD 20.4 billion by 2029, at a CAGR of 4.8% from USD 16.2 billion in 2024. Urbanization and infrastructure development are propelling the global acoustic insulation market. Globally the construction industry is a major economic driver. In developing countries construction contributes about 8% to GDP, while in developed nation it accounts for around 5%. Regions like Middle East & Africa and Asia Pacific have leveraged the construction industry to propel their economies forward. In India, the construction sector is the third largest among the major economic sectors and the second-largest employment generator after agriculture. The sector's contribution to GDP is projected to be 12-15% by 2025. The National Infrastructure Pipeline (NIP), launched in 2020, is a key initiative, encompassing 9000 projects with a total initial investment of USD 1.3 trillion. Focus areas include energy (24%), roads (19%), urban development (16%), and railways (13%). In the European Union, investment in housing was 5.6% of GDP in 2021. This share varied among Member States, ranging from 7.6% in Cyprus, 7.2% in Germany and Finland, to lower percentages in Greece (1.3%), Ireland (2.1%), Latvia (2.2%), and Poland (2.3%). These investments demonstrate the critical role of construction in economic stability and growth across the region. So, as the urbanization and infrastructure development accelerate, the demand for acoustic insulation grows to ensure comfort and productivity.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2021-2022 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion), Volume (Kiloton) |

| Segments | Material, End-use Industry, and Region |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America |

"Based on type, foamed plastic segment is expected to be the second-fastest growing market during the forecast period, in terms of value."

Polymeric foam, mainly polystyrene and polyurethane foam, is one of the most extensively applied and efficient types of acoustic materials. Foamed plastic has received a lot of circulation because of its lighter weight and efficiency in soundproofing whether it is used in a house or an office. This makes the closed-cell structure as not only improves the sound absorption facility but also the additional thermal insulation. Flexible for its use foamed plastic is a solution that can be easily mounted in spaces of different architectural concepts to enhance the acoustic and thermal parameters of the environment.

"Based on end-use industry, building & construction has the largest market share during the forecast period, in terms of value."

The largest consumption area of acoustic insulation is constructions and building, which is the principal end-use for acoustic insulation and involves the execution of structures designed to improve acoustic comfort and diminish sound nuisance indoors. From the perspective of enhance living and working conditions, it worth to know that acoustic insulation allows to reduce influence of airborne noises that come from other rooms and impact noises originating outside a room or a building. In the residential buildings it is applied to walls, floor and ceilings to enable occupants be independent from any form of interference since it will offer them privacy and negate certain disturbances. Offices, hotels, and healthcare facilities need acoustic insulation for the structures because it is suitable for creating productive and comfortable environments for working, resting, or even healing. Furthermore, acoustic insulation plays the role of compliance with legal requirements that concern allowable noise levels in various kinds of constructions. This means that construction projects can cover up these standards by incorporating soundproofing materials and tools in construction projects hence improving the building quality as well as the value. Also, acoustic insulation contributes to sustainable solutions based on the improvement of energy performance provided by modern materials as well as the decrease of noise transfer. The populations increase and the emergence of large buildings and integrated are still considering acoustic partitions in constructions and reconstructions therefore establishing the significance of acoustic insulation in the building and constructions.

"Based on region, Asia Pacific is the fastest growing market for acoustic insulation in 2023, in terms of value."

The Asia Pacific region is experiencing excellent growth in the market due to several key factors. Urbanization and industrialization in countries like India, China, Southeast Asia, others have fueled extensive construction activities, increasing the demand for effective noise control solutions. Strict enforcement of noise pollution regulations across building & construction, industrial and other sectors necessitate widespread adoption of sound insulation materials to enhance acoustic comfort and reduce noise transmission. Furthermore, robust economic expansion has spurred investments in infrastructure projects such as commercial buildings, residential complexes, and transportation networks, all requiring efficient acoustic insulation to meet quality standards and improve occupant satisfaction.

In the process of determining and verifying the market size for several segments and subsegments identified through secondary research, extensive primary interviews were conducted. A breakdown of the profiles of the primary interviewees are as follows:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C-Level - 35%, Director Level - 25%, and Others - 40%

- By Region: North America - 40%, Europe - 30%, Asia Pacific - 20%, Middle East & Africa-5%, and Latin America-5%

The key players in this market are include Saint-Gobain (France), Knauf Insulation (US), Armacell (Germany), SOPREMA (France), ROCKWOOL A/S (Denmark), Huntsman International LLC (US), Owens Corning (US), Kingspan Group (Ireland), BASF SE (Germany), and Johns Manville (US).

Research Coverage

This report segments the acoustic insulation market based on material, end-use industry, and region, and provides estimations for the overall value of the market across various regions. A detailed analysis of key industry players has been conducted to provide insights into their business overviews, products and services, key strategies, new product launches, expansions, and mergers and acquisitions associated with the acoustic insulation market.

Key benefits of buying this report

This research report focuses on various levels of analysis, including industry analysis (industry trends), market ranking analysis of top players, and company profiles, which together provide an overall view of the competitive landscape, emerging and high-growth segments of the acoustic insulation market, high-growth regions, and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of key drivers (Growing urbanization and infrastructure development, rising health issues associated with noise pollution, Stringent building regulations and codes), restraints (Slowdown in European construction industry, fluctuating raw material prices due to volatility in crude oil prices), opportunities (Aerogel, potential high-performance substitutes for glass wool, increased infrastructural spending) and challenges (Proper disposable and recycling techniques required. Low awareness of acoustic insulation in developing countries).

- Market Penetration: Comprehensive information on the acoustic insulation market offered by top players in the global acoustic insulation market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the acoustic insulation market.

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the markets for acoustic insulation market across regions.

- Market Diversification: Exhaustive information about new products, untapped regions, and recent developments in the global acoustic insulation market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the acoustic insulation market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS & EXCLUSIONS OF STUDY

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION & REGIONAL SNAPSHOT

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Primary interviews from demand and supply sides

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primary interviews

- 2.1.1 SECONDARY DATA

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- 2.3 FORECAST NUMBER CALCULATION

- 2.4 DATA TRIANGULATION

- 2.5 ASSUMPTIONS

- 2.6 LIMITATIONS & RISKS ASSOCIATED WITH ACOUSTIC INSULATION MARKET

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN ACOUSTIC INSULATION MARKET

- 4.2 ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY, 2024 VS. 2029 (KILOTON)

- 4.3 ACOUSTIC INSULATION MARKET, BY MATERIAL, 2024 VS. 2029 (KILOTON)

- 4.4 ACOUSTIC INSULATION MARKET, BY COUNTRY, 2024-2029 (KILOTON)

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing urbanization and infrastructure development

- 5.2.1.2 Rising health issues associated with noise pollution

- 5.2.1.3 Stringent building regulations and codes

- 5.2.2 RESTRAINTS

- 5.2.2.1 Slowdown in European construction industry

- 5.2.2.2 Fluctuating raw material prices due to volatility in crude oil prices

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Aerogel-potential high-performance substitute for glass wool

- 5.2.3.2 Increased infrastructural spending

- 5.2.4 CHALLENGES

- 5.2.4.1 Proper disposal and recycling techniques required

- 5.2.4.2 Low awareness of acoustic insulation in developing countries

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.3.1 RAW MATERIAL SUPPLIERS

- 5.3.2 MANUFACTURERS

- 5.3.3 DISTRIBUTORS

- 5.3.4 END USERS

- 5.4 PORTER'S FIVE FORCES ANALYSIS

- 5.4.1 THREAT OF NEW ENTRANTS

- 5.4.2 THREAT OF SUBSTITUTES

- 5.4.3 BARGAINING POWER OF SUPPLIERS

- 5.4.4 BARGAINING POWER OF BUYERS

- 5.4.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.5 PATENT ANALYSIS

- 5.5.1 METHODOLOGY

- 5.5.2 DOCUMENT TYPES

- 5.5.3 PUBLICATION TRENDS IN LAST 10 YEARS

- 5.5.4 INSIGHTS

- 5.5.5 JURISDICTION ANALYSIS

- 5.5.6 TOP 10 COMPANIES/APPLICANTS

- 5.5.7 TOP 10 PATENT OWNERS IN LAST 10 YEARS

- 5.6 ECOSYSTEM/MARKET MAP

- 5.7 TRADE ANALYSIS

- 5.7.1 IMPORT SCENARIO OF SLAG WOOL, ROCK WOOL, AND SIMILAR MINERAL WOOLS, INCLUDING INTERMIXTURES THEREOF, IN BULK, SHEETS, OR ROLLS

- 5.7.2 EXPORT SCENARIO OF SLAG WOOL, ROCK WOOL, AND SIMILAR MINERAL WOOLS, INCLUDING INTERMIXTURES THEREOF, IN BULK, SHEETS, OR ROLLS

- 5.8 PRICING ANALYSIS

- 5.8.1 AVERAGE SELLING PRICE TREND, BY REGION

- 5.8.2 AVERAGE SELLING PRICE TREND OF KEY PLAYERS, BY END-USE INDUSTRY

- 5.9 MACROECONOMIC OVERVIEW AND KEY TRENDS

- 5.9.1 GDP TRENDS AND FORECASTS

- 5.10 TECHNOLOGY ANALYSIS

- 5.10.1 AEROGEL

- 5.10.2 METAMATERIAL TECHNOLOGY

- 5.10.3 BIO-BASED SUSTAINABLE MATERIALS

- 5.10.4 PHASE-CHANGE MATERIALS

- 5.11 TARIFF & REGULATORY LANDSCAPE

- 5.11.1 REGULATIONS

- 5.11.2 EUROPE

- 5.11.3 NORTH AMERICA

- 5.11.4 ASIA PACIFIC

- 5.11.5 OTHERS

- 5.11.6 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12 TRENDS/DISRUPTIONS IMPACTING CUSTOMER'S BUSINESS

- 5.13 KEY CONFERENCES & EVENTS IN 2024-2025

- 5.14 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.14.2 BUYING CRITERIA

- 5.14.2.1 Quality

- 5.14.2.2 Service

- 5.15 CASE STUDY ANALYSIS

- 5.15.1 KNAUF INSULATION

- 5.15.2 BASF SE

- 5.15.3 SOPREMA

- 5.16 INVESTMENT AND FUNDING SCENARIO

- 5.17 FUNDING, BY USE CASE/APPLICATION

- 5.18 IMPACT OF AI/GEN AI ON ACOUSTIC INSULATION MARKET

6 ACOUSTIC INSULATION MARKET, BY MATERIAL

- 6.1 INTRODUCTION

- 6.2 FOAMED PLASTIC

- 6.2.1 COST-EFFECTIVENESS TO AID MARKET GROWTH

- 6.3 GLASS WOOL

- 6.3.1 RISING USE IN RESIDENTIAL & COMMERCIAL APPLICATIONS TO DRIVE MARKET

- 6.4 ROCK WOOL

- 6.4.1 USED EXTENSIVELY IN SOUND INSULATION

- 6.5 ELASTOMERIC FOAM

- 6.5.1 EXCELLENT THERMAL AND ACOUSTIC PROPERTIES TO DRIVE MARKET

- 6.6 OTHER MATERIALS

7 ACOUSTIC INSULATION MARKET, BY END-USE INDUSTRY

- 7.1 INTRODUCTION

- 7.2 BUILDING & CONSTRUCTION

- 7.2.1 STRONG GROWTH IN GLOBAL CONSTRUCTION INDUSTRY TO DRIVE MARKET

- 7.3 TRANSPORTATION

- 7.3.1 HIGH PRODUCTION VOLUME IN MAJOR AUTOMOTIVE MARKETS TO DRIVE GROWTH

- 7.4 OIL & GAS AND PETROCHEMICAL

- 7.4.1 HIGH GROWTH IN EMERGING COUNTRIES TO FUEL MARKET

- 7.5 ENERGY & UTILITIES

- 7.5.1 RISING ENERGY DEMAND FROM BOTH DEVELOPED AND DEVELOPING COUNTRIES TO DRIVE MARKET

- 7.6 INDUSTRIAL & OEM

- 7.6.1 STRONG GROWTH IN MANUFACTURING AND TELECOM INDUSTRIES TO DRIVE MARKET

8 ACOUSTIC INSULATION MARKET, BY REGION

- 8.1 INTRODUCTION

- 8.2 NORTH AMERICA

- 8.2.1 US

- 8.2.1.1 Robust growth fueled by urban development and strong economic foundation

- 8.2.2 CANADA

- 8.2.2.1 Strong growth in construction industry to fuel market

- 8.2.3 MEXICO

- 8.2.3.1 Favorable demographics and increasing investments to drive market

- 8.2.1 US

- 8.3 EUROPE

- 8.3.1 GERMANY

- 8.3.1.1 Growth in industrial sector to fuel market

- 8.3.2 FRANCE

- 8.3.2.1 Increasing awareness on reducing noise levels to drive market

- 8.3.3 UK

- 8.3.3.1 Strong demand from commercial sector to propel market growth

- 8.3.4 ITALY

- 8.3.4.1 Government investments in public infrastructure to propel market

- 8.3.5 SPAIN

- 8.3.5.1 Growing focus on sustainable building practices to drive market

- 8.3.6 NORDIC COUNTRIES

- 8.3.6.1 Growing end-use industry in respective countries to drive market

- 8.3.7 BENELUX

- 8.3.7.1 Growing commercial sector to boost market growth

- 8.3.8 POLAND

- 8.3.8.1 Strong end-use industry to boost market growth

- 8.3.9 SWITZERLAND

- 8.3.9.1 Increased construction activity to propel market

- 8.3.10 REST OF EUROPE

- 8.3.1 GERMANY

- 8.4 ASIA PACIFIC

- 8.4.1 CHINA

- 8.4.1.1 Largest acoustic insulation market in Asia Pacific

- 8.4.2 JAPAN

- 8.4.2.1 Strong automotive industry to drive market growth

- 8.4.3 SOUTH KOREA

- 8.4.3.1 Strong economic growth to drive market

- 8.4.4 INDIA

- 8.4.4.1 Growth in power industry to propel market

- 8.4.5 AUSTRALIA

- 8.4.5.1 Increasing investment in construction industry to drive market

- 8.4.6 ASEAN COUNTRIES

- 8.4.6.1 Booming construction industry to drive market

- 8.4.7 REST OF ASIA PACIFIC

- 8.4.1 CHINA

- 8.5 MIDDLE EAST & AFRICA

- 8.5.1 GCC COUNTRIES

- 8.5.1.1 Saudi Arabia

- 8.5.1.1.1 High investments in construction sector to fuel market

- 8.5.1.2 UAE

- 8.5.1.2.1 Rising investments in energy and infrastructure to drive market

- 8.5.1.3 Rest of GCC countries

- 8.5.1.1 Saudi Arabia

- 8.5.2 TURKEY

- 8.5.2.1 Growth of construction industry to propel market

- 8.5.3 REST OF MIDDLE EAST & AFRICA

- 8.5.1 GCC COUNTRIES

- 8.6 SOUTH AMERICA

- 8.6.1 BRAZIL

- 8.6.1.1 Rapidly expanding economy to support market growth

- 8.6.2 ARGENTINA

- 8.6.2.1 Strong automotive industry to propel market

- 8.6.3 REST OF SOUTH AMERICA

- 8.6.1 BRAZIL

9 COMPETITIVE LANDSCAPE

- 9.1 OVERVIEW

- 9.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 9.3 REVENUE ANALYSIS

- 9.4 MARKET SHARE ANALYSIS

- 9.4.1 SAINT-GOBAIN

- 9.4.2 ROCKWOOL A/S

- 9.4.3 ARMACELL

- 9.5 COMPANY VALUATION AND FINANCIAL METRICS

- 9.6 BRAND/PRODUCT COMPARISON ANALYSIS

- 9.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 9.7.1 STARS

- 9.7.2 EMERGING LEADERS

- 9.7.3 PERVASIVE PLAYERS

- 9.7.4 PARTICIPANTS

- 9.7.5 COMPANY FOOTPRINT

- 9.7.5.1 Company footprint

- 9.7.5.2 Material footprint

- 9.7.5.3 End-use footprint

- 9.7.5.4 Region footprint

- 9.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 9.8.1 PROGRESSIVE COMPANIES

- 9.8.2 RESPONSIVE COMPANIES

- 9.8.3 DYNAMIC COMPANIES

- 9.8.4 STARTING BLOCKS

- 9.8.5 COMPETITIVE BENCHMARKING

- 9.9 COMPETITIVE SCENARIO AND TRENDS

- 9.9.1 PRODUCT LAUNCHES

- 9.9.2 DEALS

- 9.9.3 EXPANSIONS

10 COMPANY PROFILES

- 10.1 KEY PLAYERS

- 10.1.1 SAINT-GOBAIN

- 10.1.1.1 Business overview

- 10.1.1.2 Products/Solutions/Services offered

- 10.1.1.3 Recent developments

- 10.1.1.3.1 Product launches

- 10.1.1.3.2 Deals

- 10.1.1.3.3 Expansions

- 10.1.1.4 MnM view

- 10.1.1.4.1 Key strengths

- 10.1.1.4.2 Strategic choices

- 10.1.1.4.3 Weaknesses and competitive threats

- 10.1.2 KNAUF INSULATION

- 10.1.2.1 Business overview

- 10.1.2.2 Products/Solutions/Services offered

- 10.1.2.3 Recent developments

- 10.1.2.3.1 Expansions

- 10.1.2.4 MnM view

- 10.1.2.4.1 Key strengths

- 10.1.2.4.2 Strategic choices

- 10.1.2.4.3 Weaknesses and competitive threats

- 10.1.3 ARMACELL

- 10.1.3.1 Business overview

- 10.1.3.2 Products/Solutions/Services offered

- 10.1.3.3 Recent developments

- 10.1.3.3.1 Product Launches

- 10.1.3.3.2 Deals

- 10.1.3.3.3 Expansions

- 10.1.3.4 MnM view

- 10.1.3.4.1 Key strengths

- 10.1.3.4.2 Strategic choices

- 10.1.3.4.3 Weaknesses and competitive threats

- 10.1.4 SOPREMA

- 10.1.4.1 Business overview

- 10.1.4.2 Products/Solutions/Services offered

- 10.1.4.3 Recent developments

- 10.1.4.3.1 Expansions

- 10.1.4.4 MnM view

- 10.1.4.4.1 Key strengths

- 10.1.4.4.2 Strategic choices

- 10.1.4.4.3 Weaknesses and competitive threats

- 10.1.5 ROCKWOOL A/S

- 10.1.5.1 Business overview

- 10.1.5.2 Products/Solutions/Services offered

- 10.1.5.3 Recent developments

- 10.1.5.3.1 Product launches

- 10.1.5.3.2 Deals

- 10.1.5.3.3 Expansions

- 10.1.5.4 MnM view

- 10.1.5.4.1 Key strengths

- 10.1.5.4.2 Strategic choices

- 10.1.5.4.3 Weaknesses and competitive threats

- 10.1.6 HUNTSMAN INTERNATIONAL LLC

- 10.1.6.1 Business overview

- 10.1.6.2 Products/Solutions/Services offered

- 10.1.6.3 Recent developments

- 10.1.6.3.1 Deals

- 10.1.6.3.2 Expansions

- 10.1.6.4 MnM view

- 10.1.7 OWENS CORNING

- 10.1.7.1 Business overview

- 10.1.7.2 Products/Solutions/Services offered

- 10.1.7.3 Recent developments

- 10.1.7.3.1 Product launches

- 10.1.7.3.2 Deals

- 10.1.7.4 MnM view

- 10.1.8 KINGSPAN GROUP

- 10.1.8.1 Business overview

- 10.1.8.2 Products/Solutions/Services offered

- 10.1.8.3 Recent developments

- 10.1.8.3.1 Deals

- 10.1.8.4 MnM view

- 10.1.9 BASF SE

- 10.1.9.1 Business overview

- 10.1.9.2 Products/Solutions/Services offered

- 10.1.9.3 Recent developments

- 10.1.9.3.1 Product Launches

- 10.1.9.4 MnM view

- 10.1.10 JOHNS MANVILLE

- 10.1.10.1 Business overview

- 10.1.10.2 Products/Solutions/Services offered

- 10.1.10.3 Recent developments

- 10.1.10.3.1 Product launches

- 10.1.10.3.2 Expansions

- 10.1.10.4 MnM view

- 10.1.1 SAINT-GOBAIN

- 10.2 OTHER PLAYERS

- 10.2.1 GETZNER WERKSTOFFE GMBH

- 10.2.2 CELLOFOAM INTERNATIONAL GMBH & CO. KG

- 10.2.3 REGUPOL GERMANY GMBH & CO. KG

- 10.2.4 3M

- 10.2.5 TRELLEBORG

- 10.2.6 L'ISOLANTE K-FLEX S.P.A.

- 10.2.7 DOW

- 10.2.8 SIDERISE

- 10.2.9 CABOT CORPORATION

- 10.2.10 FLETCHER INSULATION

- 10.2.11 HUSH ACOUSTICS

- 10.2.12 PRIMACOUSTIC

- 10.2.13 TROCELLEN

- 10.2.14 CELLECTA

- 10.2.15 INTERNATIONAL CELLULOSE CORPORATION

11 APPENDIX

- 11.1 DISCUSSION GUIDE

- 11.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 11.3 CUSTOMIZATION OPTIONS

- 11.4 RELATED REPORTS

- 11.5 AUTHOR DETAILS