|

|

市場調査レポート

商品コード

1537742

軍用アンテナの世界市場:技術別、用途別、周波数帯域別、プラットフォーム別、地域別 - 予測(~2029年)Military Antenna Market by Technology (Wire Antennas, Aperture Antennas, Reflector, Lens, Microstrip, Array Antennas), Application (Electronic Warfare, Navigation, Satcom, Telemetry), Frequency Band, Platform and Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 軍用アンテナの世界市場:技術別、用途別、周波数帯域別、プラットフォーム別、地域別 - 予測(~2029年) |

|

出版日: 2024年08月14日

発行: MarketsandMarkets

ページ情報: 英文 302 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

世界の軍用アンテナの市場規模は、2024年の45億米ドルから2029年までに56億米ドルに達し、2024年~2029年にCAGRで4.6%の成長が見込まれます。

軍用アンテナの数量データは、2024年の14万6,432ユニットから2029年までに18万3,921ユニットに達すると予測されます。海上用途での軍用アンテナ需要の高まり、無人地上車両向けのカスタマイズされたCOTM(Communications On The Move)の需要の増加が市場の促進要因となっています。しかし、軍用アンテナをサポートするインフラの開発と保守に関連する高いコストが、軍用アンテナ市場を抑制しています。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 単位 | 10億米ドル |

| セグメント | コンポーネント別、プラットフォーム別、技術別、用途別、周波数帯域別、POS別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

現在、北米は軍用アンテナのもっとも発達した市場で、米国がもっとも高い成長を記録しています。北米と中東でも予測期間に大きな成長が見込まれます。しかし、無線周波数の利用可能性の問題や資格のある労働力の不足は、軍用アンテナ市場の成長に影響を与える主な課題です。

「2024年に市場をリードするリフレクターコンポーネントセグメント」

リフレクターコンポーネントセグメントは、アンテナ性能の向上に重要な役割を果たすため、市場を独占すると予測されています。リフレクターは、放射パターンを調整するためにアンテナアセンブリに組み込まれ、特定の方向の信号利得を向上させるのに役立ちます。この強化は、より正確で強力な信号伝送を実現するために極めて重要です。その重要性を認識し、多くのメーカーが反射鏡の設計の改良に力を注いでいます。その目標は、性能を高めるだけでなく、組み立て時間を短縮し、製造工程をより効率的にすることです。このような技術革新と効率重視の姿勢が、市場におけるリフレクターコンポーネントセグメントの存在感を高めています。

「超高周波セグメントが予測期間に最高のCAGRで成長します。」

超高周波(SHF)アンテナは、高い周波数と正確な指向性を必要とする用途に適しています。これらの特徴により、衛星通信、レーダーシステム、地上マイクロ波リンクなどのさまざまな先進通信技術に最適です。SHFアンテナは高い周波数で動作するため、高い精度と信頼性で信号を送受信することができ、通信チャネルが堅牢で信頼できる状態を維持することができます。その結果、SHFセグメントは、これらの先端用途の厳しい要件を満たす有効性により、急速な成長を示しています。

「北米が予測期間にもっとも速く成長する見込みです。」

この急拡大は、同地域のさまざまな国の防衛軍からの先進の監視システムやレーダー技術への需要の高まりが主因です。軍事・防衛組織が能力を強化するためにこうした先進のシステムへの投資を増やしていることから、北米の軍用アンテナ市場は大きな成長が見込まれています。国家安全保障の向上と防衛インフラの近代化への注目の高まりがこの上昇基調を後押ししており、北米は軍用アンテナ市場の主要地域となっています。

当レポートでは、世界の軍用アンテナ市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 軍用アンテナ市場の企業にとって魅力的な機会

- 軍用アンテナ市場:プラットフォーム別

- 軍用アンテナ市場:コンポーネント別

- 軍用アンテナ市場:技術別

- 軍用アンテナ市場:POS別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 顧客のビジネスに影響を与える動向と混乱

- エコシステム/市場マップ

- 著名企業

- 民間企業、中小企業

- エンドユーザー

- バリューチェーン分析

- 価格分析

- プラットフォームの参考価格分析

- 地域の参考価格分析

- ケーススタディ分析

- 軍用アンテナプラットフォームの運用データ

- 主な会議とイベント(2024年~2025年)

- 貿易分析

- 輸入シナリオ

- 輸出シナリオ

- 関税と規制情勢

- 関税

- 規制機関、政府機関、その他の組織

- 主なステークホルダーと購入基準

- 技術ロードマップ

- ビジネスモデル

- 総所有コスト

- 部品表

- 技術分析

- 主要技術

- 補完技術

- 隣接技術

- 投資と資金調達のシナリオ

第6章 産業動向

- イントロダクション

- 技術動向

- RF機器の3Dプリンティング

- 軍用アンテナの小型化

- メタマテリアルアンテナの開発

- プラズマアンテナの開発

- アクティブ電子走査アレイ(AESA)の開発

- 技術分析

- メガトレンドの影響

- マルチバンド・マルチミッション(MBMM)アンテナ

- マルチプラットフォームアンチジャムGPSナビゲーションアンテナ(MAGNA)

- ハイブリッドビームフォーミング方式

- 軍用アンテナ市場に対する生成AIの影響

- イントロダクション

- 防衛部門における生成AIの採用

- 軍用アンテナプラットフォームにおける生成AIの影響

- 軍用アンテナ市場に対する生成AIの影響

- サプライチェーン分析

- 特許分析

第7章 軍用アンテナ市場:コンポーネント別

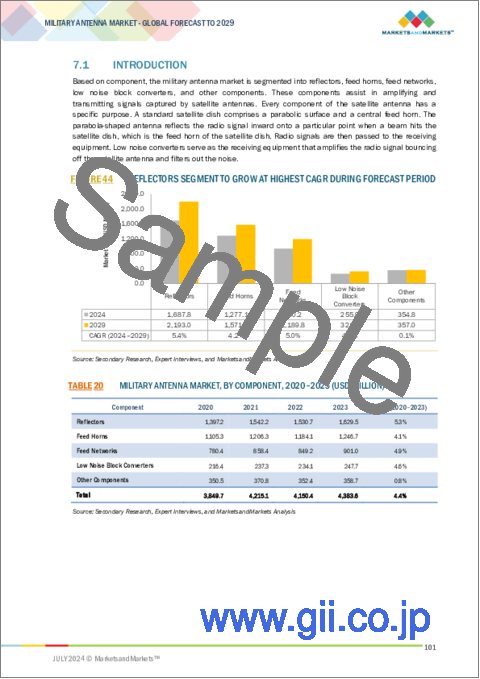

- イントロダクション

- リフレクター

- フィードホーン

- フィードネットワーク

- 低ノイズブロックコンバータ(LNBS)

- その他のコンポーネント

第8章 軍用アンテナ市場:周波数帯域別

- イントロダクション

- HF

- VHF

- UHF

- SHF

- EHF

第9章 軍用アンテナ市場:技術別

- イントロダクション

- ワイヤーアンテナ

- 開口アンテナ

- リフレクターアンテナ

- レンズアンテナ

- マイクロストリップアンテナ

- アレイアンテナ

第10章 軍用アンテナ市場:プラットフォーム別

- イントロダクション

- 陸上

- 航空

- 海上

第11章 軍用アンテナ市場:用途別

- イントロダクション

- 監視

- 電子戦

- ナビゲーション

- 通信

- 衛星通信

- テレメトリー

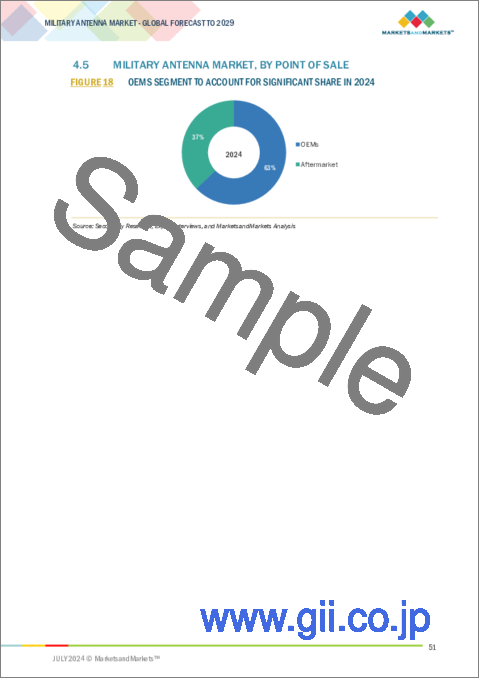

第12章 軍用アンテナ市場:POS別

- イントロダクション

- OEM

- アフターマーケット

第13章 軍用アンテナ市場:地域別

- イントロダクション

- 北米

- 北米のPESTLE分析

- 米国

- カナダ

- 欧州

- 欧州のPESTLE分析

- 英国

- フランス

- ドイツ

- イタリア

- その他の欧州

- アジア太平洋

- アジア太平洋のPESTLE分析

- インド

- 日本

- 韓国

- オーストラリア

- その他のアジア太平洋

- 中東

- 中東のPESTLE分析

- GCC

- イスラエル

- その他の地域

- その他の地域のPESTLE分析

- ラテンアメリカ

- アフリカ

第14章 競合情勢

- イントロダクション

- 主要企業戦略/有力企業

- 市場シェア分析

- 収益分析

- ブランド/製品の比較

- 企業の評価と財務指標

- 企業の評価マトリクス:主要企業(2023年)

- 企業の評価マトリクス:スタートアップ/中小企業(2023年)

- 競合シナリオと動向

第15章 企業プロファイル

- 主要企業

- L3HARRIS TECHNOLOGIES, INC.

- RTX

- BAE SYSTEMS

- THALES

- HONEYWELL INTERNATIONAL INC.

- GENERAL DYNAMICS CORPORATION

- COBHAM SATCOM

- SAAB AB

- VIASAT, INC.

- ASELSAN A.S.

- GILAT SATELLITE NETWORKS

- ROHDE & SCHWARZ

- TERMA

- NORSAT INTERNATIONAL INC.

- KYMETA CORPORATION

- ND SATCOM GMBH

- MVG

- RAMI

- その他の企業

- MICRO-ANT LLC.

- SAT-LITE TECHNOLOGIES

- DATAPATH INC.

- HANWHA PHASOR

- COMROD COMMUNICATION AS

- BARKER & WILLIAMSON

- HASCALL-DENKE

- ANTCOM

- ANTENNA PRODUCTS CORPORATION

- SOUTHWEST ANTENNAS

第16章 付録

List of Tables

- TABLE 1 USD EXCHANGE RATES, 2020-2023

- TABLE 2 ROLE OF COMPANIES IN MARKET ECOSYSTEM

- TABLE 3 INDICATIVE PRICING ANALYSIS, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 4 KEY FACTORS AFFECTING MILITARY ANTENNA PRICES

- TABLE 5 INDICATIVE PRICING ANALYSIS FOR KEY PLATFORMS, BY REGION, 2023 (USD MILLION)

- TABLE 6 VOLUME OF LAND FLEET FOR MAJOR VEHICLE TYPES, BY KEY COUNTRY, 2023

- TABLE 7 VOLUME OF NAVAL FLEET FOR MAJOR VESSEL TYPES, BY KEY COUNTRY, 2023

- TABLE 8 VOLUME OF AIRBORNE FLEET FOR MAJOR AIRCRAFT TYPES, BY KEY COUNTRY, 2023

- TABLE 9 KEY CONFERENCES & EVENTS, 2024-2025

- TABLE 10 TARIFFS FOR TRANSMISSION OR RECEPTION OF VOICE, IMAGE, OR OTHER DATA (HS CODE: 851769)

- TABLE 11 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 REST OF THE WORLD: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY PLATFORM

- TABLE 16 KEY BUYING CRITERIA, BY PLATFORM

- TABLE 17 TOTAL COST OF OWNERSHIP OF MILITARY ANTENNAS, BY PLATFORM, 2023

- TABLE 18 BILL OF MATERIALS FOR BASIC MILITARY-GRADE VHF (VERY HIGH FREQUENCY) TACTICAL ANTENNAS, 2023 (USD)

- TABLE 19 PATENT ANALYSIS, 2020-2024

- TABLE 20 MILITARY ANTENNA MARKET, BY COMPONENT, 2020-2023 (USD MILLION)

- TABLE 21 MILITARY ANTENNA MARKET, BY COMPONENT, 2024-2029 (USD MILLION)

- TABLE 22 MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2020-2023 (USD MILLION)

- TABLE 23 MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2024-2029 (USD MILLION)

- TABLE 24 MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 25 MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 26 MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 27 MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 28 GROUND: MILITARY ANTENNA MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 29 GROUND: MILITARY ANTENNA MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 30 AIRBORNE: MILITARY ANTENNA MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 31 AIRBORNE: MILITARY ANTENNA MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 32 MARINE: MILITARY ANTENNA MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 33 MARINE: MILITARY ANTENNA MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 34 MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 35 MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 36 MILITARY ANTENNA MARKET, BY POINT OF SALE, 2020-2023 (USD MILLION)

- TABLE 37 MILITARY ANTENNA MARKET, BY POINT OF SALE, 2024-2029 (USD MILLION)

- TABLE 38 MILITARY ANTENNA MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 39 MILITARY ANTENNA MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 40 NORTH AMERICA: MILITARY ANTENNA MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 41 NORTH AMERICA: MILITARY ANTENNA MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 42 NORTH AMERICA: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 43 NORTH AMERICA: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 44 NORTH AMERICA: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2020-2023 (USD MILLION)

- TABLE 45 NORTH AMERICA: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2024-2029 (USD MILLION)

- TABLE 46 NORTH AMERICA: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 47 NORTH AMERICA: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 48 NORTH AMERICA: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 49 NORTH AMERICA: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 50 US: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 51 US: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 52 US: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 53 US: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 54 CANADA: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 55 CANADA: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 56 CANADA: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 57 CANADA: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 58 EUROPE: MILITARY ANTENNA MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 59 EUROPE: MILITARY ANTENNA MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 60 EUROPE: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 61 EUROPE: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 62 EUROPE: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2020-2023 (USD MILLION)

- TABLE 63 EUROPE: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2024-2029 (USD MILLION)

- TABLE 64 EUROPE: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 65 EUROPE: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 66 EUROPE: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 67 EUROPE: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 68 UK: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 69 UK: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 70 UK: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 71 UK: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 72 FRANCE: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 73 FRANCE: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 74 FRANCE: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 75 FRANCE: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 76 GERMANY: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 77 GERMANY: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 78 GERMANY: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 79 GERMANY: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 80 ITALY: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 81 ITALY: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 82 ITALY: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 83 ITALY: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 84 REST OF EUROPE: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 85 REST OF EUROPE: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 86 REST OF EUROPE: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 87 REST OF EUROPE: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 88 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 89 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 90 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 91 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 92 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2020-2023 (USD MILLION)

- TABLE 93 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2024-2029 (USD MILLION)

- TABLE 94 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 95 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 96 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 97 ASIA PACIFIC: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 98 INDIA: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 99 INDIA: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 100 INDIA: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 101 INDIA: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 102 JAPAN: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 103 JAPAN: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 104 JAPAN: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 105 JAPAN: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 106 SOUTH KOREA: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 107 SOUTH KOREA: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 108 SOUTH KOREA: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 109 SOUTH KOREA: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 110 AUSTRALIA: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 111 AUSTRALIA: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 112 AUSTRALIA: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 113 AUSTRALIA: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 114 REST OF ASIA PACIFIC: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 115 REST OF ASIA PACIFIC: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 116 REST OF ASIA PACIFIC: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 117 REST OF ASIA PACIFIC: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 118 MIDDLE EAST: MILITARY ANTENNA MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 119 MIDDLE EAST: MILITARY ANTENNA MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 120 MIDDLE EAST: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 121 MIDDLE EAST: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 122 MIDDLE EAST: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2020-2023 (USD MILLION)

- TABLE 123 MIDDLE EAST: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2024-2029 (USD MILLION)

- TABLE 124 MIDDLE EAST: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 125 MIDDLE EAST: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 126 MIDDLE EAST: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 127 MIDDLE EAST: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 128 SAUDI ARABIA: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 129 SAUDI ARABIA: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 130 SAUDI ARABIA: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 131 SAUDI ARABIA: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 132 UAE: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 133 UAE: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 134 UAE: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 135 UAE: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 136 ISRAEL: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 137 ISRAEL: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 138 ISRAEL: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 139 ISRAEL: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 140 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 141 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 142 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 143 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 144 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2020-2023 (USD MILLION)

- TABLE 145 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY FREQUENCY BAND, 2024-2029 (USD MILLION)

- TABLE 146 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 147 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- TABLE 148 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 149 REST OF THE WORLD: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 150 LATIN AMERICA: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 151 LATIN AMERICA: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 152 LATIN AMERICA: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 153 LATIN AMERICA: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 154 AFRICA: MILITARY ANTENNA MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 155 AFRICA: MILITARY ANTENNA MARKET, BY PLATFORM, 2024-2029 (USD MILLION)

- TABLE 156 AFRICA: MILITARY ANTENNA MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 157 AFRICA: MILITARY ANTENNA MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 158 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2020-2024

- TABLE 159 MILITARY ANTENNA MARKET: DEGREE OF COMPETITION

- TABLE 160 COMPANY FREQUENCY BAND FOOTPRINT

- TABLE 161 COMPANY PLATFORM FOOTPRINT

- TABLE 162 COMPANY APPLICATION FOOTPRINT

- TABLE 163 COMPANY REGIONAL FOOTPRINT

- TABLE 164 DETAILED LIST OF KEY STARTUPS/SMES

- TABLE 165 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 166 MILITARY ANTENNA MARKET: PRODUCT LAUNCHES & DEVELOPMENTS, MARCH 2020-MAY 2024

- TABLE 167 MILITARY ANTENNA MARKET: DEALS, AUGUST 2020-JUNE 2024

- TABLE 168 MILITARY ANTENNA MARKET: OTHER DEVELOPMENTS, DECEMBER 2020-JUNE 2024

- TABLE 169 L3HARRIS TECHNOLOGIES, INC.: BUSINESS OVERVIEW

- TABLE 170 L3HARRIS TECHNOLOGIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 171 L3HARRIS TECHNOLOGIES, INC.: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 172 L3HARRIS TECHNOLOGIES, INC.: DEALS

- TABLE 173 L3HARRIS TECHNOLOGIES, INC.: OTHER DEVELOPMENTS

- TABLE 174 RTX: BUSINESS OVERVIEW

- TABLE 175 RTX: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 176 RTX: OTHER DEVELOPMENTS

- TABLE 177 BAE SYSTEMS: BUSINESS OVERVIEW

- TABLE 178 BAE SYSTEMS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 179 BAE SYSTEMS: DEALS

- TABLE 180 BAE SYSTEMS: OTHER DEVELOPMENTS

- TABLE 181 THALES: BUSINESS OVERVIEW

- TABLE 182 THALES: PRODUCTS /SOLUTIONS/SERVICES OFFERED

- TABLE 183 THALES: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 184 THALES: DEALS

- TABLE 185 HONEYWELL INTERNATIONAL INC.: BUSINESS OVERVIEW

- TABLE 186 HONEYWELL INTERNATIONAL INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 187 HONEYWELL INTERNATIONAL INC.: DEALS

- TABLE 188 HONEYWELL INTERNATIONAL INC.: OTHER DEVELOPMENTS

- TABLE 189 GENERAL DYNAMICS CORPORATION: BUSINESS OVERVIEW

- TABLE 190 GENERAL DYNAMICS CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 191 GENERAL DYNAMICS CORPORATION: OTHER DEVELOPMENTS

- TABLE 192 COBHAM SATCOM: BUSINESS OVERVIEW

- TABLE 193 COBHAM SATCOM: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 194 COBHAM SATCOM: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 195 COBHAM SATCOM: DEALS

- TABLE 196 COBHAM SATCOM: OTHER DEVELOPMENTS

- TABLE 197 SAAB AB: BUSINESS OVERVIEW

- TABLE 198 SAAB AB: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 199 SAAB AB: DEALS

- TABLE 200 SAAB AB: OTHER DEVELOPMENTS

- TABLE 201 VIASAT, INC.: BUSINESS OVERVIEW

- TABLE 202 VIASAT, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 203 VIASAT, INC.: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 204 VIASAT, INC.: DEALS

- TABLE 205 VIASAT, INC.: OTHER DEVELOPMENTS

- TABLE 206 ASELSAN A.S.: BUSINESS OVERVIEW

- TABLE 207 ASELSAN A.S.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 208 ASELSAN A.S.: OTHER DEVELOPMENTS

- TABLE 209 GILAT SATELLITE NETWORKS: BUSINESS OVERVIEW

- TABLE 210 GILAT SATELLITE NETWORKS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 211 GILAT SATELLITE NETWORKS: DEALS

- TABLE 212 GILAT SATELLITE NETWORKS: OTHER DEVELOPMENTS

- TABLE 213 ROHDE & SCHWARZ: BUSINESS OVERVIEW

- TABLE 214 ROHDE & SCHWARZ: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 215 ROHDE & SCHWARZ: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 216 ROHDE & SCHWARZ: DEALS

- TABLE 217 TERMA: BUSINESS OVERVIEW

- TABLE 218 TERMA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 219 NORSAT INTERNATIONAL INC.: BUSINESS OVERVIEW

- TABLE 220 NORSAT INTERNATIONAL INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 221 NORSAT INTERNATIONAL INC.: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 222 KYMETA CORPORATION: BUSINESS OVERVIEW

- TABLE 223 KYMETA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 224 KYMETA CORPORATION: PRODUCT LAUNCHES & DEVELOPMENTS

- TABLE 225 KYMETA CORPORATION: DEALS

- TABLE 226 ND SATCOM GMBH: BUSINESS OVERVIEW

- TABLE 227 ND SATCOM GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 228 MVG: BUSINESS OVERVIEW

- TABLE 229 MVG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 230 RAMI: BUSINESS OVERVIEW

- TABLE 231 RAMI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 232 MILITARY ANTENNA MARKET: OTHER MAPPED COMPANIES

List of Figures

- FIGURE 1 RESEARCH FLOW

- FIGURE 2 MILITARY ANTENNA MARKET: RESEARCH DESIGN

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 4 IMPACT OF RUSSIA'S INVASION OF UKRAINE ON DEFENSE INDUSTRY'S MACRO FACTORS

- FIGURE 5 IMPACT OF RUSSIA-UKRAINE WAR ON MICRO FACTORS

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- FIGURE 8 DATA TRIANGULATION

- FIGURE 9 AIRBORNE SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 10 ARRAY ANTENNAS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 11 ELECTRONIC WARFARE SEGMENT TO LEAD MARKET BY 2029

- FIGURE 12 OEMS SEGMENT TO ACCOUNT FOR SIGNIFICANT SHARE BY 2029

- FIGURE 13 ASIA PACIFIC TO LEAD MARKET IN 2024

- FIGURE 14 MODERNIZATION PROGRAMS AND INCREASING PROCUREMENT OF RADAR AND AIR DEFENSE SYSTEMS TO OFFER SEVERAL UNTAPPED OPPORTUNITIES FOR MARKET GROWTH

- FIGURE 15 GROUND SEGMENT TO LEAD MARKET IN 2024

- FIGURE 16 REFLECTORS SEGMENT TO LEAD MARKET IN 2024

- FIGURE 17 ARRAY ANTENNAS SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 18 OEMS SEGMENT TO ACCOUNT FOR SIGNIFICANT SHARE IN 2024

- FIGURE 19 MILITARY ANTENNA MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 20 WORLD MILITARY EXPENDITURE, BY REGION, 2014-2024

- FIGURE 21 GLOBAL PRODUCTION VOLUME FOR MILITARY DRONES, 2018-2022

- FIGURE 22 TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 23 KEY PLAYERS IN MILITARY ANTENNA MARKET ECOSYSTEM

- FIGURE 24 VALUE CHAIN ANALYSIS

- FIGURE 25 IMPORT DATA OF RADAR APPARATUS, BY COUNTRY, 2019-2023 (USD THOUSAND)

- FIGURE 26 EXPORT DATA OF RADAR APPARATUS, BY COUNTRY, 2019-2023 (USD THOUSAND)

- FIGURE 27 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY PLATFORM

- FIGURE 28 KEY BUYING CRITERIA, BY PLATFORM

- FIGURE 29 EVOLUTION OF MILITARY ANTENNA TECHNOLOGIES

- FIGURE 30 TECHNOLOGY ROADMAP OF MILITARY ANTENNA MARKET

- FIGURE 31 EMERGING TRENDS IN MILITARY ANTENNA SYSTEMS

- FIGURE 32 BUSINESS MODELS

- FIGURE 33 TOTAL COST OF OWNERSHIP OF MILITARY ANTENNAS

- FIGURE 34 OTAL COST OF OWNERSHIP OF MILITARY ANTENNAS, 2023

- FIGURE 35 BILL OF MATERIALS FOR BASIC MILITARY-GRADE VHF (VERY HIGH FREQUENCY) TACTICAL ANTENNAS, 2023 (USD)

- FIGURE 36 US VC DEAL ACTIVITY IN AEROSPACE AND DEFENSE TECH, 2010-2022 (USD BILLION)

- FIGURE 37 USE OF GENERATIVE AI IN DEFENSE

- FIGURE 38 ADOPTION OF GENERATIVE AI IN MILITARY, BY TOP COUNTRY

- FIGURE 39 IMPACT OF GENERATIVE AI ON MILITARY ANTENNA PLATFORMS

- FIGURE 40 IMPACT OF GENERATIVE AI ON MILITARY ANTENNAS

- FIGURE 41 IMPACT OF GENERATIVE AI ON MILITARY ANTENNA MARKET

- FIGURE 42 SUPPLY CHAIN ANALYSIS

- FIGURE 43 SNAPSHOT OF PATENTS GRANTED IN LAST 10 YEARS

- FIGURE 44 REFLECTORS SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 45 SUPER HIGH FREQUENCY SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 46 ARRAY ANTENNAS SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 47 AIRBORNE SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 48 ELECTRONIC WARFARE SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 49 AFTERMARKET SEGMENT TO GROW AT SIGNIFICANT CAGR DURING FORECAST PERIOD

- FIGURE 50 ASIA PACIFIC TO ACCOUNT FOR LARGEST SHARE DURING FORECAST PERIOD

- FIGURE 51 NORTH AMERICA: MILITARY ANTENNA MARKET SNAPSHOT

- FIGURE 52 EUROPE: MILITARY ANTENNA MARKET SNAPSHOT

- FIGURE 53 ASIA PACIFIC: MILITARY ANTENNA MARKET SNAPSHOT

- FIGURE 54 MIDDLE EAST: MILITARY ANTENNA MARKET SNAPSHOT

- FIGURE 55 REST OF THE WORLD: MILITARY ANTENNA MARKET SNAPSHOT

- FIGURE 56 MARKET SHARE ANALYSIS, 2023

- FIGURE 57 REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2019-2023

- FIGURE 58 BRAND/PRODUCT COMPARISON

- FIGURE 59 FINANCIAL METRICS OF PROMINENT MARKET PLAYERS

- FIGURE 60 VALUATION OF PROMINENT MARKET PLAYERS

- FIGURE 61 MILITARY ANTENNA MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- FIGURE 62 COMPANY FOOTPRINT

- FIGURE 63 MILITARY ANTENNA MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- FIGURE 64 L3HARRIS TECHNOLOGIES, INC.: COMPANY SNAPSHOT

- FIGURE 65 RTX: COMPANY SNAPSHOT

- FIGURE 66 BAE SYSTEMS: COMPANY SNAPSHOT

- FIGURE 67 THALES: COMPANY SNAPSHOT

- FIGURE 68 HONEYWELL INTERNATIONAL INC.: COMPANY SNAPSHOT

- FIGURE 69 GENERAL DYNAMICS CORPORATION: COMPANY SNAPSHOT

- FIGURE 70 SAAB AB: COMPANY SNAPSHOT

- FIGURE 71 VIASAT, INC.: COMPANY SNAPSHOT

- FIGURE 72 ASELSAN A.S.: COMPANY SNAPSHOT

- FIGURE 73 GILAT SATELLITE NETWORKS: COMPANY SNAPSHOT

The military antenna market is projected to reach USD 5.6 billion by 2029, from USD 4.5 billion in 2024, at a CAGR of 4.6% from 2024 to 2029. The military antenna volume data is projected to grow from 146,432 units in 2024 to 183,921 units by 2029. The rising demand for military antennas in maritime use, and increasing demand for customized communication-on-the-move solutions for unmanned ground vehicles are factors to drive the market. However, the High costs associated with the development and maintenance of infrastructure to support military antennas are restraining the military antenna market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Component, Platform, Technology, Frequency Band, Application, Point of Sale, and Region |

| Regions covered | North America, Europe, APAC, RoW |

Currently, North America is the most developed market for military antennas, with the US registering the highest growth. During the forecast period, the market is also projected to witness significant growth in North America and Middle East. However, radio spectrum availability issues and the lack of a qualified workforce are key challenges affecting the growth of the military antenna market.

"Reflectors Component segment to lead the market in 2024"

The reflectors component segment is expected to dominate the market because of their critical role in enhancing antenna performance. Reflectors are integrated into antenna assemblies to adjust the radiation pattern, which helps improve signal gain in specific directions. This enhancement is crucial for achieving more precise and stronger signal transmission. Recognizing their importance, many manufacturers are concentrating on refining reflector designs. Their goal is to not only boost performance but also reduce assembly time, making the production process more efficient. This focus on innovation and efficiency is driving the prominence of the reflectors component segment in the market..

"Super High Frequency segment to grow at highest CAGR during the forecast period"

The Super High Frequency (SHF) antennas are well-suited for applications that require high frequency and precise directionality. These features make them perfect for a range of advanced communication technologies, such as satellite communications, radar systems, and terrestrial microwave links. By operating at high frequencies, SHF antennas are able to transmit and receive signals with great accuracy and reliability, ensuring that communication channels remain robust and dependable. As a result, the SHF segment is experiencing rapid growth, driven by its effectiveness in meeting the demanding requirements of these cutting-edge applications..

" The North America region is forecasted to grow at the fastest rate during the forecast period"

The North American region is anticipated to experience the quickest growth over the forecast period. This rapid expansion is largely attributed to the rising demand for advanced surveillance systems and radar technologies from the defense forces across various countries in the region. As military and defense organizations increasingly invest in these sophisticated systems to enhance their capabilities, the market for military antennas in North America is expected to see significant growth. The focus on improving national security and modernizing defense infrastructure is driving this upward trend, making North America a key player in the military antenna market.

In-depth interviews have been conducted with chief executive officers (CEOs), Directors, and other executives from various key organizations operating in the authentication and brand protection marketplace.

- By Company Type: Tier 1 - 45%, Tier 2 - 35%, and Tier 3 - 20%

- By Designation: C-level Executives - 35%, Directors - 25%, and Others - 40%

- By Region: North America- 30%, Europe - 20%, Asia Pacific- 45% and Middle East- 5%

L3Harris Technologies, Inc. (US), RTX (US), BAE Systems (UK), Thales (France), and Honeywell International Inc. (US) are some of the leading players operating in the military antenna market.

Research Coverage

The study covers the military antenna market across various segments and subsegments. It aims at estimating the size and growth potential of this market across different segments. This study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their solutions and business offerings, recent developments undertaken by them, and key market strategies adopted by them.

Key benefits of buying this report: This report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall military antenna market and its subsegments. The report covers the entire ecosystem of the military antenna market. It will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report will also help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- * Analysis of key Drivers (Growing Adoption of Electronically Steered Phased Array Antennas, Rising demand for military antennas in maritime use, Increasing demand for customized communication-on-the-Move solutions for unmanned ground vehicles, and Increasing the defense budget of emerging countries), restrains (High costs associated with the development and maintenance of infrastructure to support military antennas, and Issues associated with poor transmission of signals), and challenges (Electromagnetic compatibility-related challenges of satellite antennas and System requirements and design constraints) influencing the growth of the market.

- Product Development/Innovation: Detailed Insights on upcoming technologies, R&D activities, and new products/solutions launched in the market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the military antenna market across varied regions

- Market Diversification: Exhaustive information about new solutions, recent developments, and investments in the military antenna market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like L3Harris Technologies, Inc. (US), RTX (US), BAE Systems (UK), Thales (France), and Honeywell International Inc. (US) among others in the military antenna market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKET SEGMENTATION

- 1.3.2 INCLUSIONS & EXCLUSIONS

- 1.4 YEARS CONSIDERED

- 1.5 CURRENCY CONSIDERED

- 1.6 SUMMARY OF CHANGES

- 1.7 STAKEHOLDERS

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key insights from primary sources

- 2.1.2.3 Breakdown of primaries

- 2.1.1 SECONDARY DATA

- 2.2 FACTOR ANALYSIS

- 2.2.1 INTRODUCTION

- 2.2.2 DEMAND-SIDE INDICATORS

- 2.2.3 SUPPLY-SIDE INDICATORS

- 2.2.3.1 Naval forces incorporating advanced military antennas

- 2.3 IMPACT OF RUSSIA-UKRAINE WAR ON MILITARY ANTENNA MARKET

- 2.3.1 IMPACT OF RUSSIA'S INVASION OF UKRAINE ON DEFENSE INDUSTRY'S MACRO FACTORS

- 2.3.2 IMPACT OF RUSSIA'S INVASION OF UKRAINE ON DEFENSE INDUSTRY'S MICRO FACTORS

- 2.4 MARKET SIZE ESTIMATION

- 2.5 RESEARCH APPROACH & METHODOLOGY

- 2.5.1 BOTTOM-UP APPROACH

- 2.5.1.1 Military antenna market for OEMs

- 2.5.1.2 Military antenna market for aftermarket

- 2.5.1.3 Military antenna market size

- 2.5.2 TOP-DOWN APPROACH

- 2.5.1 BOTTOM-UP APPROACH

- 2.6 DATA TRIANGULATION

- 2.7 RESEARCH ASSUMPTIONS

- 2.8 RISK ASSESSMENT

- 2.9 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN MILITARY ANTENNA MARKET

- 4.2 MILITARY ANTENNA MARKET, BY PLATFORM

- 4.3 MILITARY ANTENNA MARKET, BY COMPONENT

- 4.4 MILITARY ANTENNA MARKET, BY TECHNOLOGY

- 4.5 MILITARY ANTENNA MARKET, BY POINT OF SALE

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growing adoption of electronically steered phased array antennas

- 5.2.1.2 Rising demand for military antennas in maritime use

- 5.2.1.3 Increasing demand for customized communication-on-the-move solutions for unmanned ground vehicles

- 5.2.1.4 Increasing defense budget of emerging countries

- 5.2.2 RESTRAINTS

- 5.2.2.1 High costs associated with development and maintenance of infrastructure to support military antennas

- 5.2.2.2 Issues associated with poor transmission of signals

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Development of ultra-compact communication terminals for advanced ground combat vehicles

- 5.2.3.2 Demand for high data rate transmission

- 5.2.3.3 Rise in adoption of unmanned vehicles

- 5.2.4 CHALLENGES

- 5.2.4.1 Electromagnetic compatibility-related challenges of satellite antennas

- 5.2.4.2 System requirements and design constraints

- 5.2.1 DRIVERS

- 5.3 TRENDS & DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 ECOSYSTEM/MARKET MAP

- 5.4.1 PROMINENT COMPANIES

- 5.4.2 PRIVATE AND SMALL ENTERPRISES

- 5.4.3 END USERS

- 5.5 VALUE CHAIN ANALYSIS

- 5.6 PRICING ANALYSIS

- 5.6.1 INDICATIVE PRICING ANALYSIS FOR PLATFORMS

- 5.6.1.1 Factors affecting prices of military antennas

- 5.6.2 INDICATIVE PRICING ANALYSIS FOR REGIONS

- 5.6.1 INDICATIVE PRICING ANALYSIS FOR PLATFORMS

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 CHELTON DEVELOPED NEW SECTOR ANTENNA SOLUTION TO MEET ROYAL AUSTRALIAN NAVY'S REQUIREMENTS FOR SHIP-BORNE, SHIP-TO-AIR NATO LINK16 DATA-LINK SYSTEMS

- 5.7.2 CHELTON DEVELOPED ADVANCED BODY-WORN ANTENNA SYSTEM FOR THALES UK FIST PROGRAMME TO ADDRESS COMMUNICATION RELIABILITY ISSUES FACED BY SOLDIERS

- 5.7.3 SATCOM GLOBAL SELECTED AND DEPLOYED INTELLIAN NX SYSTEMS TO DELIVER MAXIMUM PERFORMANCE ON ITS AURA VSAT SERVICE

- 5.7.4 GOGO CONDUCTED FLIGHT TESTS WITH ITS KU-BAND SATELLITE ANTENNA TECHNOLOGY TO DELIVER HIGH-RATE DATA TRANSFERABILITY TO PASSENGERS TRAVELING ON AIRLINES

- 5.8 OPERATIONAL DATA FOR MILITARY ANTENNA PLATFORMS

- 5.9 KEY CONFERENCES & EVENTS, 2024-2025

- 5.10 TRADE ANALYSIS

- 5.10.1 IMPORT SCENARIO

- 5.10.2 EXPORT SCENARIO

- 5.11 TARIFF & REGULATORY LANDSCAPE

- 5.11.1 TARIFFS

- 5.11.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.12.2 BUYING CRITERIA

- 5.13 TECHNOLOGY ROADMAP

- 5.14 BUSINESS MODELS

- 5.15 TOTAL COST OF OWNERSHIP

- 5.16 BILL OF MATERIALS

- 5.17 TECHNOLOGY ANALYSIS

- 5.17.1 KEY TECHNOLOGIES

- 5.17.1.1 Electronically steered phased array antennas (ESPAs)

- 5.17.1.2 Ultra high frequency (UHF) and super high frequency (SHF) antennas

- 5.17.1.3 MIMO (Multiple Inputs Multiple Outputs) antennas

- 5.17.2 COMPLEMENTARY TECHNOLOGIES

- 5.17.2.1 Advanced signal processing

- 5.17.2.2 Secure communication protocols

- 5.17.2.3 Power management systems

- 5.17.3 ADJACENT TECHNOLOGIES

- 5.17.3.1 Unmanned systems

- 5.17.3.2 Cybersecurity solutions

- 5.17.3.3 Satellite communication (SATCOM)

- 5.17.1 KEY TECHNOLOGIES

- 5.18 INVESTMENT & FUNDING SCENARIO

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TECHNOLOGY TRENDS

- 6.2.1 3D PRINTING OF RF EQUIPMENT

- 6.2.2 MINIATURIZATION OF MILITARY ANTENNAS

- 6.2.3 DEVELOPMENT OF METAMATERIAL ANTENNAS

- 6.2.4 DEVELOPMENT OF PLASMA ANTENNAS

- 6.2.5 DEVELOPMENT OF ACTIVE ELECTRONICALLY SCANNED ARRAY (AESA)

- 6.3 TECHNOLOGY ANALYSIS

- 6.4 IMPACT OF MEGATRENDS

- 6.4.1 DEVELOPMENT OF SMART ANTENNAS

- 6.5 MULTI-BAND, MULTI-MISSION (MBMM) ANTENNA

- 6.6 MULTI-PLATFORM ANTI-JAM GPS NAVIGATION ANTENNA (MAGNA)

- 6.7 HYBRID BEAMFORMING METHODS

- 6.8 IMPACT OF GENERATIVE AI ON MILITARY ANTENNA MARKET

- 6.8.1 INTRODUCTION

- 6.8.2 ADOPTION OF GENERATIVE AI IN DEFENSE SECTOR

- 6.8.3 IMPACT OF GENERATIVE AI ON MILITARY ANTENNA PLATFORMS

- 6.8.4 IMPACT OF GENERATIVE AI ON MILITARY ANTENNA MARKET

- 6.9 SUPPLY CHAIN ANALYSIS

- 6.10 PATENT ANALYSIS

7 MILITARY ANTENNA MARKET, BY COMPONENT

- 7.1 INTRODUCTION

- 7.2 REFLECTORS

- 7.2.1 INNOVATION IN REFLECTOR DESIGN TO ASSEMBLE TIME TO ENCOURAGE MARKET EXPANSION

- 7.3 FEED HORNS

- 7.3.1 FEED HORNS ARE USED AS PRIMARY RADIATOR TO FEED REFLECTOR ANTENNA OR AS SEPARATE ANTENNA

- 7.4 FEED NETWORKS

- 7.4.1 FEED NETWORKS ENSURE EFFICIENT SIGNAL AND TRANSMISSION AND RECEPTION IN COMPLEX COMMUNICATION SYSTEMS

- 7.5 LOW NOISE BLOCK CONVERTERS (LNBS)

- 7.5.1 USAGE OF LNBS IN MILITARY SATCOMS TO DRIVE GROWTH

- 7.6 OTHER COMPONENTS

8 MILITARY ANTENNA MARKET, BY FREQUENCY BAND

- 8.1 INTRODUCTION

- 8.2 HIGH FREQUENCY (HF)

- 8.2.1 RAPID INNOVATION IN SECURE, RESILIENT MILITARY COMMUNICATION TECHNOLOGY TO DRIVE GROWTH

- 8.3 VERY HIGH FREQUENCY (VHF)

- 8.3.1 RISING DEMAND FOR VHF FREQUENCY ANTENNAS TO DRIVE MARKET

- 8.4 ULTRA HIGH FREQUENCY (UHF)

- 8.4.1 TECHNOLOGICAL ADVANCEMENTS AND INCREASED DEMAND FOR RELIABLE COMMUNICATION SYSTEMS TO DRIVE MARKET

- 8.5 SUPER HIGH FREQUENCY (SHF)

- 8.5.1 ENHANCED DATA TRANSMISSION CAPABILITIES OVER LONG DISTANCES TO FUEL MARKET GROWTH

- 8.6 EXTREMELY HIGH FREQUENCY (EHF)

- 8.6.1 INCREASING DEMAND FOR SECURE AND HIGH-CAPACITY COMMUNICATION SYSTEMS TO BOOST MARKET GROWTH

9 MILITARY ANTENNA MARKET, BY TECHNOLOGY

- 9.1 INTRODUCTION

- 9.2 WIRE ANTENNAS

- 9.2.1 NEED FOR REAL-TIME DATA SHARING AND COORDINATION AMONG MILITARY UNITS TO DRIVE MARKET

- 9.2.2 DIPOLE ANTENNAS

- 9.2.3 MONOPOLE ANTENNAS

- 9.2.4 LOOP ANTENNAS

- 9.2.5 HELIX ANTENNAS

- 9.3 APERTURE ANTENNAS

- 9.3.1 INCREASING INVESTMENTS TO ENHANCE ANTENNA TECHNOLOGY TO BOOST GROWTH

- 9.3.2 WAVEGUIDE ANTENNAS

- 9.3.3 HORN ANTENNAS

- 9.4 REFLECTOR ANTENNAS

- 9.4.1 ADVANCEMENTS IN SATELLITE COMMUNICATION TECHNOLOGY TO DRIVE GROWTH

- 9.4.2 PARABOLIC REFLECTOR ANTENNAS

- 9.4.3 CORNER REFLECTOR ANTENNAS

- 9.5 LENS ANTENNAS

- 9.5.1 TECHNOLOGICAL ADVANCEMENTS TO CREATE OPPORTUNITIES FOR GROWTH

- 9.5.2 DELAY LENS ANTENNAS

- 9.5.3 FAST LENS ANTENNAS

- 9.6 MICROSTRIP ANTENNAS

- 9.6.1 DEVELOPMENT OF BROADBAND STACKED PATCH ANTENNAS TO CREATE OPPORTUNITIES FOR GROWTH

- 9.6.2 CIRCULAR MICROSTRIP ANTENNAS

- 9.6.3 RECTANGULAR MICROSTRIP ANTENNAS

- 9.7 ARRAY ANTENNAS

- 9.7.1 PHASED ARRAY ANTENNA SYSTEMS ARE USED IN NAVAL AND AIRBORNE PLATFORMS

- 9.7.2 YAGI-UDA ARRAY ANTENNAS

- 9.7.3 MICROSTRIP PATCH ARRAY ANTENNAS

- 9.7.4 APERTURE ARRAY ANTENNAS

- 9.7.5 SLOTTED-WAVEGUIDE ARRAY ANTENNAS

10 MILITARY ANTENNA MARKET, BY PLATFORM

- 10.1 INTRODUCTION

- 10.2 GROUND

- 10.2.1 VEHICLE

- 10.2.1.1 Necessity for enhanced communication capabilities in military vehicles to support market growth

- 10.2.2 BASE STATION

- 10.2.2.1 Geopolitical rivalry to drive demand for sophisticated and advanced military base station antennas

- 10.2.3 SOLDIER

- 10.2.3.1 Technological developments in advanced communication solutions to enhance operational efficiency

- 10.2.3.2 Manpack

- 10.2.3.3 Handheld

- 10.2.3.4 Body worn

- 10.2.4 UNMANNED GROUND VEHICLE

- 10.2.4.1 Increased investment in research and development to drive market

- 10.2.1 VEHICLE

- 10.3 AIRBORNE

- 10.3.1 AIRCRAFT

- 10.3.1.1 Need for advanced, reliable, and efficient radar systems to fuel growth

- 10.3.2 UNMANNED AERIAL VEHICLE

- 10.3.2.1 Growing need for robust and high-performance antennas to boost growth

- 10.3.3 MISSILE

- 10.3.3.1 Advancements in missile technology to boost market growth

- 10.3.1 AIRCRAFT

- 10.4 MARINE

- 10.4.1 SHIPBOARD

- 10.4.1.1 Demand for robust, versatile antennas to support complex maritime operations to spur demand

- 10.4.2 SUBMARINE

- 10.4.2.1 Need for improving operational effectiveness and situational awareness in maritime defense to propel demand

- 10.4.3 UNMANNED MARINE VEHICLE

- 10.4.3.1 Need for enhanced UMV operational capabilities to drive demand

- 10.4.1 SHIPBOARD

11 MILITARY ANTENNA MARKET, BY APPLICATION

- 11.1 INTRODUCTION

- 11.2 SURVEILLANCE

- 11.2.1 INCREASING DEMAND FOR ADVANCED RADAR AND MONITORING SYSTEMS TO DRIVE GROWTH

- 11.3 ELECTRONIC WARFARE

- 11.3.1 INCREASED MILITARY FOCUS ON ENHANCING COMMUNICATION INFRASTRUCTURE AND CAPABILITIES TO SPUR DEMAND

- 11.4 NAVIGATION

- 11.4.1 INCREASE IN AIRSPACE CONGESTION TO CREATE NEED FOR ADVANCED MILITARY ANTENNAS FOR SAFE FLIGHT

- 11.5 COMMUNICATION

- 11.5.1 NEED FOR COMPACT HARDWARE SYSTEMS FOR LONG-RANGE COMMUNICATION CAPABILITIES TO DRIVE MARKET

- 11.6 SATCOM

- 11.6.1 INCREASING DEMAND FOR CUSTOMIZED SATCOM-ON-THE-MOVE SOLUTIONS TO PROPEL DEMAND

- 11.7 TELEMETRY

- 11.7.1 INCREASED USE OF TELEMETRY IN MILITARY TO DRIVE MARKET

12 MILITARY ANTENNA MARKET, BY POINT OF SALE

- 12.1 INTRODUCTION

- 12.2 OEMS

- 12.2.1 INCREASE IN PROCUREMENT OF MILITARY VEHICLES TO DRIVE SEGMENT GROWTH

- 12.3 AFTERMARKET

- 12.3.1 NEED FOR UPGRADING EXISTING FLEET OF MILITARY VEHICLES TO FUEL MARKET

13 MILITARY ANTENNA MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 NORTH AMERICA: PESTLE ANALYSIS

- 13.2.2 US

- 13.2.2.1 Increased spending by US defense organizations to fuel market growth

- 13.2.3 CANADA

- 13.2.3.1 Modernization of defense capabilities to enhance communication systems to drive market

- 13.3 EUROPE

- 13.3.1 EUROPE: PESTLE ANALYSIS

- 13.3.2 UK

- 13.3.2.1 Long-term investment plan for modernizing military communications to boost market

- 13.3.3 FRANCE

- 13.3.3.1 Need for reliable and interoperable communication solutions to drive growth

- 13.3.4 GERMANY

- 13.3.4.1 Focus on providing comprehensive military assistance to Ukraine to boost growth

- 13.3.5 ITALY

- 13.3.5.1 Plans to procure advanced antennas to develop MALE drones to spur market demand

- 13.3.6 REST OF EUROPE

- 13.4 ASIA PACIFIC

- 13.4.1 ASIA PACIFIC: PESTLE ANALYSIS

- 13.4.2 INDIA

- 13.4.2.1 Technological developments in advanced radar technology to drive market

- 13.4.3 JAPAN

- 13.4.3.1 Increased use of satellites and SATCOM equipment for carrying out surveillance activities to propel growth

- 13.4.4 SOUTH KOREA

- 13.4.4.1 Country's strategic priorities and evolving defense needs to fuel market

- 13.4.5 AUSTRALIA

- 13.4.5.1 Need for upgrading military vehicles to drive market

- 13.4.6 REST OF ASIA PACIFIC

- 13.5 MIDDLE EAST

- 13.5.1 MIDDLE EAST: PESTLE ANALYSIS

- 13.5.2 GCC

- 13.5.2.1 Saudi Arabia

- 13.5.2.1.1 Increasing deployment of military antennas for communication and navigation activities to propel market

- 13.5.2.2 UAE

- 13.5.2.2.1 Production of advanced radar technologies to drive market growth

- 13.5.2.1 Saudi Arabia

- 13.5.3 ISRAEL

- 13.5.3.1 Rapid development of latest technologies to boost market

- 13.6 REST OF THE WORLD

- 13.6.1 REST OF THE WORLD: PESTLE ANALYSIS

- 13.6.2 LATIN AMERICA

- 13.6.2.1 Need for addressing regional security challenges to boost growth

- 13.6.3 AFRICA

- 13.6.3.1 Demand for secure and efficient communication systems to fuel market

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 MARKET SHARE ANALYSIS

- 14.4 REVENUE ANALYSIS

- 14.5 BRAND/PRODUCT COMPARISON

- 14.6 COMPANY VALUATION AND FINANCIAL METRICS

- 14.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 14.7.1 STARS

- 14.7.2 EMERGING LEADERS

- 14.7.3 PERVASIVE PLAYERS

- 14.7.4 PARTICIPANTS

- 14.7.5 COMPANY FOOTPRINT

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING

- 14.9 COMPETITIVE SCENARIO & TRENDS

- 14.9.1 PRODUCT LAUNCHES & DEVELOPMENTS

- 14.9.2 DEALS

- 14.9.3 OTHER DEVELOPMENTS

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 L3HARRIS TECHNOLOGIES, INC.

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.3.1 Product launches & developments

- 15.1.1.3.2 Deals

- 15.1.1.3.3 Other developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Right to win

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses & competitive threats

- 15.1.2 RTX

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.3.1 Other developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Right to win

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses & competitive threats

- 15.1.3 BAE SYSTEMS

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.3.1 Deals

- 15.1.3.3.2 Other developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Right to win

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses & competitive threats

- 15.1.4 THALES

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.3.1 Product launches & developments

- 15.1.4.3.2 Deals

- 15.1.4.4 MnM view

- 15.1.4.4.1 Right to win

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses & competitive threats

- 15.1.5 HONEYWELL INTERNATIONAL INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.3.1 Deals

- 15.1.5.3.2 Other developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Right to win

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses & competitive threats

- 15.1.6 GENERAL DYNAMICS CORPORATION

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.6.3.1 Other developments

- 15.1.7 COBHAM SATCOM

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.7.3.1 Product launches & developments

- 15.1.7.3.2 Deals

- 15.1.7.3.3 Other developments

- 15.1.8 SAAB AB

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.8.3.1 Deals

- 15.1.8.3.2 Other developments

- 15.1.9 VIASAT, INC.

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.9.3 Recent developments

- 15.1.9.3.1 Product launches & developments

- 15.1.9.3.2 Deals

- 15.1.9.3.3 Other developments

- 15.1.10 ASELSAN A.S.

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Solutions/Services offered

- 15.1.10.3 Recent developments

- 15.1.10.3.1 Other developments

- 15.1.11 GILAT SATELLITE NETWORKS

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.11.3.1 Deals

- 15.1.11.3.2 Other developments

- 15.1.12 ROHDE & SCHWARZ

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.12.3.1 Product launches & developments

- 15.1.12.3.2 Deals

- 15.1.13 TERMA

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.14 NORSAT INTERNATIONAL INC.

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.14.3.1 Product launches & developments

- 15.1.15 KYMETA CORPORATION

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.15.3.1 Product launches & developments

- 15.1.15.3.2 Deals

- 15.1.16 ND SATCOM GMBH

- 15.1.16.1 Business overview

- 15.1.16.2 Products/Solutions/Services offered

- 15.1.17 MVG

- 15.1.17.1 Business overview

- 15.1.17.2 Products/Solutions/Services offered

- 15.1.18 RAMI

- 15.1.18.1 Business overview

- 15.1.18.2 Products/Solutions/Services offered

- 15.1.1 L3HARRIS TECHNOLOGIES, INC.

- 15.2 OTHER PLAYERS

- 15.2.1 MICRO-ANT LLC.

- 15.2.2 SAT-LITE TECHNOLOGIES

- 15.2.3 DATAPATH INC.

- 15.2.4 HANWHA PHASOR

- 15.2.5 COMROD COMMUNICATION AS

- 15.2.6 BARKER & WILLIAMSON

- 15.2.7 HASCALL-DENKE

- 15.2.8 ANTCOM

- 15.2.9 ANTENNA PRODUCTS CORPORATION

- 15.2.10 SOUTHWEST ANTENNAS

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 ANNEXURE A: DEFENSE PROGRAM MAPPING

- 16.3 ANNEXURE B: OTHER MAPPED COMPANIES

- 16.4 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.5 CUSTOMIZATION OPTIONS

- 16.6 RELATED REPORTS

- 16.7 AUTHOR DETAILS