軍用アンテナの市場機会、成長促進要因、産業動向分析、2025~2034年予測

Military Antenna Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750347

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

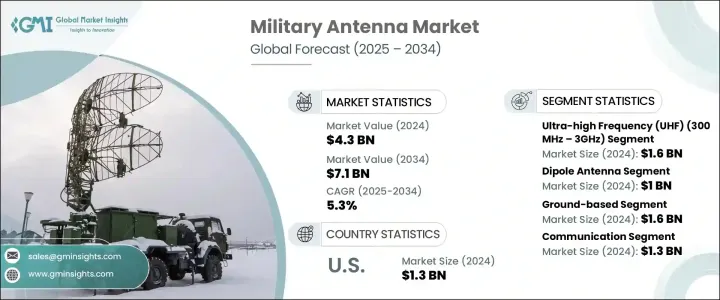

世界の軍用アンテナ市場は、2024年には43億米ドルと評価され、CAGR 5.3%で成長し、2034年には71億米ドルに達すると推定されています。

現代の軍事作戦では、陸・空・海の各領域で迅速かつ安全な通信が要求されます。相互運用性、暗号化、マルチドメイン統合への注目が高まる中、世界各国の政府は先進的なアンテナシステムへの投資を加速させています。これらの技術は、リアルタイムの戦場調整、遠隔武器システム、衛星通信をサポートします。さらに、進化する地政学的緊張と軍事近代化プログラムは、高性能でミッションクリティカルな通信コンポーネントに大きく依存する先進的プラットフォームの調達に拍車をかけています。

米国の政策決定も、市場情勢の形成に大きな役割を果たしています。トランプ政権下で中国製電子機器に課された関税は、世界のサプライチェーンに大きな影響を与えました。RFモジュール、コネクター、回路基板などの必須部品のコストは上昇し、生産スケジュールを圧迫しました。米国内の国防請負業者は調達の遅れと費用の上昇に直面し、国内サプライヤーや同盟国の製造パートナーシップに軸足を移さざるを得なくなりました。本来の目的は国家安全保障と国内能力を高めることであったが、こうした行動は一時的に重要な軍用部品へのアクセスを妨げ、国際依存の脆弱性を浮き彫りにしました。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 43億米ドル |

| 予測金額 | 71億米ドル |

| CAGR | 5.3% |

周波数セグメントの中では、超高周波(UHF)アンテナが16億米ドルの評価額で2024年の市場をリードしました。これらのアンテナは、特に密集した地形や複雑な都市景観のような信号の障害物がある地域で、高機動軍事通信システムにおいてその信頼性から広く採用されています。その運用上の柔軟性と短・中距離通信ニーズとの互換性は、複数のプラットフォームで需要を牽引し続けています。さらに、周波数プロトコルの標準化がUHF技術へのさらなる投資を促しています。

製品タイプ別ではダイポールアンテナがトップで、2024年の売上高は10億米ドル。ダイポールアンテナは、シンプルな設計、無指向性放射、幅広い周波数互換性により、モバイルおよび地上ベースの軍事プラットフォームに統合された通信システムで好ましい選択肢となっています。また、これらのアンテナはコスト効率が高く、統合が容易なため、長年のシステムや新たな配備をサポートしています。

ドイツ軍用アンテナ市場は2024年に2億4,340万米ドルを創出し、ソフトウェア定義および複数規格の通信アーキテクチャに重点を置くようになり、アダプティブで安全なアンテナシステムに対する旺盛な需要を生み出しています。この進化は、高性能で周波数適応性の高いアンテナがリアルタイムの状況認識と相互運用性に不可欠な、空中および地上の防衛プラットフォームの近代化努力によって促進されています。デジタル戦場能力と電子戦の回復力強化に向けた推進力は、先進アンテナ技術の国内研究開発を後押ししています。

世界軍用アンテナ市場の主要企業は、市場での地位を確保するため、技術革新、パートナーシップ、製品拡大に注力しています。ロッキード・マーチンとRTXは、将来の戦闘環境に対応する高度通信システムに多額の投資を行っています。ThalesとBAE Systemsは、相互運用性とモジュール性をサポートするために製品ラインを拡大しています。ViasatとL3Harris Technologiesは、衛星ベースのアンテナポートフォリオを強化しています。一方、コブハム・アドバンスト・エレクトロニック・ソリューションズとローデ・シュワルツは、生産効率を高めるために戦略的パートナーシップを結んでいます。MTIワイヤレスエッジとアントコムは、戦術的な要求に応えるコンパクトで堅牢なアンテナシステムを開発しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響

- 主要部品の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- 業界への影響要因

- 促進要因

- 世界中で国防予算が増加

- 軍隊の近代化

- 無人航空機(UAV)の成長

- 電子戦(EW)の出現

- 国境監視および偵察活動の強化

- 業界の潜在的リスク&課題

- 開発および統合コストが高め

- 複雑な規制と周波数割り当ての問題

- 促進要因

- 成長可能性分析

- 規制情勢

- テクノロジーの情勢

- 将来の市場動向

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略ダッシュボード

第5章 市場推計・予測:製品タイプ別、2021 –2034

- 主要動向

- ダイポールアンテナ

- モノポールアンテナ

- ホーンアンテナ

- ループアンテナ

- アレイアンテナ

- パッチアンテナ

- パラボラ反射アンテナ

- その他

第6章 市場推計・予測:周波数別、2021 –2034

- 主要動向

- 高周波(HF)(3~30 MHz)

- 超短波(VHF)(30~300 MHz)

- 極超短波(UHF)(300 MHz~3 GHz)

- 超高周波(SHF)(3~30GHz)

- 極超短波(EHF)(30~300GHz)

第7章 市場推計・予測:プラットフォーム別、2021 –2034

- 主要動向

- 陸軍

- 海軍

- 空挺

- 宇宙

第8章 市場推計・予測:用途別、2021 –2034

- 主要動向

- 監視と偵察

- 衛星通信

- 電子戦

- テレメトリー

- 通信

- その他

第9章 市場推計・予測:地域別、2021 –2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第10章 企業プロファイル

- Antcom

- BAE Systems

- Cobham Advanced Electronic Solutions

- Comrod Communication

- Eylex

- General Dynamics Mission Systems

- Hascall-Denke

- Honeywell International

- L3Harris Technologies

- Lockheed Martin

- MTI Wireless Edge

- Rohde and Schwarz

- RTX

- Saab

- Thales

- Viasat

目次

The Global Military Antenna Market was valued at USD 4.3 billion in 2024 and is estimated to grow at a CAGR of 5.3% to reach USD 7.1 billion by 2034, driven by the rising defense spending across multiple regions, as well as a surge in the deployment of unmanned systems. Modern military operations demand rapid, secure communication across land, air, and sea domains-requirements that make antennas central to mission success. With increased focus on interoperability, encryption, and multi-domain integration, governments worldwide are accelerating investments in advanced antenna systems. These technologies support real-time battlefield coordination, remote weapon systems, and satellite communications. Furthermore, evolving geopolitical tensions and military modernization programs fuel the procurement of advanced platforms that rely heavily on high-performance, mission-critical communication components.

U.S. policy decisions have also played a major role in reshaping the market landscape. Tariffs imposed on Chinese electronics under the Trump administration significantly impacted global supply chains. Costs of essential components like RF modules, connectors, and circuit boards escalated, straining production timelines. Defense contractors within the United States faced procurement delays and rising expenses, which forced a pivot toward domestic suppliers and allied manufacturing partnerships. While the original goal was to boost national security and domestic capability, these actions temporarily disrupted access to critical military-grade parts, highlighting the vulnerability of international dependency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.3 Billion |

| Forecast Value | $7.1 Billion |

| CAGR | 5.3% |

Among the frequency segments, ultra-high frequency (UHF) antennas led the market in 2024 with a valuation of USD 1.6 billion. These antennas are widely adopted for their reliability in high-mobility military communication systems, particularly in areas with signal obstruction like dense terrain or complex urban landscapes. Their operational flexibility and compatibility with short-to-mid-range communication needs continue to drive demand across multiple platforms. Additionally, standardized frequency protocols are encouraging further investment in UHF technologies.

Dipole antennas topped the product type segment, generating revenues of USD 1 billion in 2024. Their simple design, omnidirectional radiation, and broad frequency compatibility make them a preferred option in communication systems integrated into mobile and ground-based military platforms. These antennas are also cost-efficient and easy to integrate, supporting long-standing systems and new deployments.

Germany Military Antenna Market generated USD 243.4 million in 2024, driven by advancing its focus on software-defined and multi-standard communication architectures, creating robust demand for adaptive and secure antenna systems. This evolution is fueled by modernization efforts across both aerial and terrestrial defense platforms, where high-performance, frequency-agile antennas are essential for real-time situational awareness and interoperability. The push toward digital battlefield capabilities and enhanced electronic warfare resilience encourages domestic R&D in advanced antenna technologies.

Leading companies in the Global Military Antenna Market focus on innovation, partnerships, and product expansion to secure their market position. Lockheed Martin and RTX invest heavily in advanced communication systems for future combat environments. Thales and BAE Systems are expanding their product lines to support interoperability and modularity. Viasat and L3Harris Technologies are strengthening their satellite-based antenna portfolios. Meanwhile, Cobham Advanced Electronic Solutions and Rohde & Schwarz are forming strategic partnerships to increase production efficiency. MTI Wireless Edge and Antcom are developing compact, rugged antenna systems to meet tactical demands.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Increased defense budgets worldwide

- 3.3.1.2 Modernization of armed forces

- 3.3.1.3 Growth in unmanned aerial vehicles (UAVs)

- 3.3.1.4 Emergence of electronic warfare (EW)

- 3.3.1.5 Increase in border surveillance and reconnaissance activities

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High development and integration costs

- 3.3.2.2 Complex regulatory and frequency allocation issues

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 (USD Million & Million Units)

- 5.1 Key trends

- 5.2 Dipole antenna

- 5.3 Monopole antennas

- 5.4 Horn antennas

- 5.5 Loop antenna

- 5.6 Array antenna

- 5.7 Patch antennas

- 5.8 Parabolic reflector antennas

- 5.9 Others

Chapter 6 Market Estimates and Forecast, By Frequency Band, 2021 – 2034 (USD Million & Million Units)

- 6.1 Key trends

- 6.2 High frequency (HF) (3–30 MHz)

- 6.3 Very high frequency (VHF) (30–300 MHz)

- 6.4 Ultra high frequency (UHF) (300 MHz–3 GHz)

- 6.5 Super high frequency (SHF) (3–30 GHz)

- 6.6 Extremely high frequency (EHF) (30–300 GHz)

Chapter 7 Market Estimates and Forecast, By Platform, 2021 – 2034 (USD Million & Million Units)

- 7.1 Key trends

- 7.2 Ground-based

- 7.3 Naval

- 7.4 Airborne

- 7.5 Space

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Million Units)

- 8.1 Key trends

- 8.2 Surveillance & reconnaissance

- 8.3 Satcom

- 8.4 Electronic warfare

- 8.5 Telemetry

- 8.6 Communication

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Antcom

- 10.2 BAE Systems

- 10.3 Cobham Advanced Electronic Solutions

- 10.4 Comrod Communication

- 10.5 Eylex

- 10.6 General Dynamics Mission Systems

- 10.7 Hascall-Denke

- 10.8 Honeywell International

- 10.9 L3Harris Technologies

- 10.10 Lockheed Martin

- 10.11 MTI Wireless Edge

- 10.12 Rohde and Schwarz

- 10.13 RTX

- 10.14 Saab

- 10.15 Thales

- 10.16 Viasat

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 170 Pages

- 納期

- 2~3営業日