|

|

市場調査レポート

商品コード

1472067

固体バイオマス原料の世界市場:由来別、タイプ別、用途別、エンドユーザー別、地域別 - 予測(~2029年)Solid Biomass Feedstock Market by Source (Agriculture, Forest, Municipal), Type (Chips, Pellets, Briquettes), Application (Electricity, Heat, Biofuel), End User (Residential & Commercial, Industrial, Utilities) & Region - Global Forecast to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 固体バイオマス原料の世界市場:由来別、タイプ別、用途別、エンドユーザー別、地域別 - 予測(~2029年) |

|

出版日: 2024年04月19日

発行: MarketsandMarkets

ページ情報: 英文 210 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

世界の固体バイオマス原料の市場規模は、2024年の266億米ドルから2029年までに362億米ドルに達し、予測期間にCAGRで6.3%の成長が推定されます。

気候変動の緩和が急務であるという世界の意識の高まりや、政府の支援政策とインセンティブが市場を牽引しています。厳しい排出規制の実施により、市場の成長が見込まれます。さらに、化石燃料への依存を減らし、再生可能エネルギー発電に注力する必要性の高まりが、予測期間に市場を牽引する見込みです。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2019年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 単位 | 100万米ドル/10億米ドル |

| セグメント | 固体バイオマス原料市場:由来別、タイプ別、用途別、エンドユーザー別、地域別 |

| 対象地域 | アジア太平洋、北米、欧州、中東・アフリカ、南米 |

「森林廃棄物:固体バイオマス原料市場の由来別で最大のセグメント。」

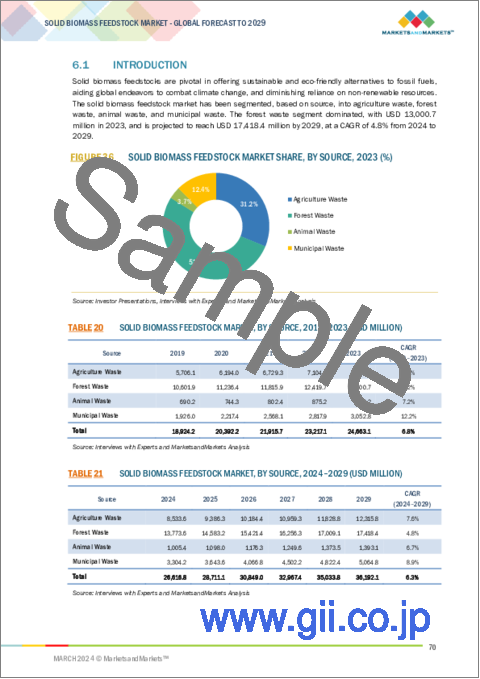

森林廃棄物セグメントが予測期間に最大のセグメントになると予測されます。農業バイオマス原料は大量に入手可能なため、バイオエネルギー需要の増加に対応できる可能性があります。森林廃棄物バイオマスをバイオエネルギー生産に利用することは、再生可能エネルギーソリューションを提供するだけでなく、森林残渣を効率的に処理し、山火事のリスクにつながりかねない余剰バイオマスの蓄積を減少させます。

タイプ別では、ペレットが予測期間に最大のセグメントになる見込みです。

世界各国の政府は、バイオマスペレットの利用を促進するために補助金やインセンティブを提供しており、再生可能エネルギー目標に沿って需要を促進しています。例えば、北米のBiomass Thermal Utilization Act(BTU Act)やインド再生可能エネルギー開発庁(IREDA)の取り組みは、バイオマスペレットの採用をさらに支援しています。

「用途別では、バイオメタンセグメントが予測期間にもっとも急成長するセグメントとなります。」

バイオメタンセグメントが予測期間に固体バイオマス原料市場でもっとも急成長するセグメントとなる見込みです。バイオメタンガスは、既存のインフラとの互換性だけでなく、環境排出と戦うために天然ガスの代替として使用することができ、需要が促進されています。

アジア太平洋が市場で最大の地域になると予測されます。

中国、日本、インドなどの各国政府は、CO2排出削減に積極的な役割を果たしており、この地域におけるバイオ燃料とバイオメタンの成長を促進しています。同地域におけるバイオ燃料とバイオメタンの採用の増加が、市場の成長を促進します。バイオ燃料、熱、電力を利用してCO2排出を削減し、エネルギー効率を向上させる取り組みは、Ministry of New and Renewable Energy(MNRE)、International Renewable Energy Agency(IRENA)、International Monetary Fund(IMF)、International Institute of Sustainable Development、Bioenergy Internationalよって支援されており、その結果、固体バイオマス原料の製造が奨励されています。

当レポートでは、世界の固体バイオマス原料市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 固体バイオマス原料市場における魅力的な機会

- 固体バイオマス原料市場:地域別

- 固体バイオマス原料市場:由来別

- 固体バイオマス原料市場:タイプ別

- 固体バイオマス原料市場:用途別

- 固体バイオマス原料市場:エンドユーザー別

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 顧客のビジネスに影響を与える動向/混乱

- サプライチェーン分析

- 原材料供給

- 原料開発

- 販売業者

- エンドユーザー

- 市場マップ

- 技術分析

- 主要技術

- 補完技術

- ケーススタディ分析

- 特許分析

- 価格設定分析

- 平均販売価格の動向:企業/タイプ別

- 平均販売価格の動向:地域別

- 貿易分析

- 輸出シナリオ

- 輸入シナリオ

- 主な会議とイベント(2024年~2025年)

- 規制情勢

- ポーターのファイブフォース分析

- 主なステークホルダーと購入基準

- 投資と資金調達のシナリオ

第6章 固体バイオマス原料市場:由来別

- イントロダクション

- 農業廃棄物

- 森林廃棄物

- 動物排泄物

- 都市廃棄物

第7章 固体バイオマス原料市場:タイプ別

- イントロダクション

- チップ

- ペレット

- ブリケット

- その他

第8章 固体バイオマス原料市場:用途別

- イントロダクション

- 電気

- 熱

- バイオ燃料

- バイオメタン

第9章 固体バイオマス原料市場:エンドユーザー別

- イントロダクション

- 住宅・商業

- 工業

- ユーティリティ

第10章 固体バイオマス原料市場:地域別

- イントロダクション

- アジア太平洋

- アジア太平洋に対する不況の影響

- 原料別

- タイプ別

- 用途別

- エンドユーザー別

- 国別

- 欧州

- 欧州に対する不況の影響

- 原料別

- タイプ別

- 用途別

- エンドユーザー別

- 国別

- 北米

- 北米に対する不況の影響

- 原料別

- タイプ別

- 用途別

- エンドユーザー別

- 国別

- 中東・アフリカ

- 中東・アフリカに対する不況の影響

- 原料別

- タイプ別

- 用途別

- エンドユーザー別

- 国別

- 南米

- 南米に対する不況の影響

- 原料別

- タイプ別

- 用途別

- エンドユーザー別

- 国別

第11章 競合情勢

- 概要

- 主要企業が採用した戦略(2019年~2023年)

- 市場シェア分析(2023年)

- 市場の評価フレームワーク

- 収益分析(2018年~2022年)

- ブランド/製品の比較

- 企業の評価マトリクス:主要企業(2023年)

- 企業の評価マトリクス:スタートアップ/中小企業(2023年)

- 競合シナリオと動向

第12章 企業プロファイル

- 主要企業

- DRAX GROUP PLC

- ENVIVA INC.

- ARBAFLAME

- REDAL

- ECOSTRAT INC.

- STORA ENSO

- SEGEZHA GROUP

- LIGNETICS, INC.

- RENTECH, INC.

- LAND ENERGY LTD

- SUPREME INDUSTRIES

- WISMAR PELLETS GMBH

- SHREE INDUSTRIES

- MALLARD CREEK INC

- SUBHAM INDUSTRIES

- その他の企業

- FRAM FUELS

- GILDALE FARMS

- GOMBELLA INTEGRATED SERVICES LTD.

- VALFEI PRODUCTS INC.

- FOREST CONCEPTS

- BLACKWOOD TECHNOLOGY

- JP GREEN FUELS

- GRAANUL INVEST

- VIRIDIS ENERGY INC.

- GROWMORE BIOTECH LTD

第13章 付録

The global solid biomass feedstock market is estimated to grow from USD 26.6 billion in 2024 to USD 36.2 Billion by 2029; it is expected to record a CAGR of 6.3% during the forecast period. The Growing global awareness of the urgent need to mitigate climate change, supportive government policies and incentives drive the solid biomass feedstock market. The market for solid biomass feedstock is expected to grow due to the implementation of stringent emission laws. Moreover, the increasing need to reduce the dependence on fossil fuels and focus on renewable energy for power generation is projected to drive the market during the forecast period.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2019-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Million/Billion) |

| Segments | Solid Biomass Feedstock Market by Source, Type, Application, End User, and Region. |

| Regions covered | Asia Pacific, North America, Europe, Middle East & Africa, and South America. |

"Forest Waste: The largest segment of the solid biomass feedstock market, by source. "

Based on source, the solid biomass feedstock market has been segmented into agriculture waste, forest waste, animal waste, and municipal waste. The forest waste segment is expected to be the largest segment during the forecast period. Agriculture biomass feedstock has the potential to meet the growing demand for bioenergy due to its availability in abundance. The utilization of forest waste biomass for bioenergy production not only offers a renewable energy solution but also efficiently handles forest residues, decreasing the buildup of surplus biomass that could otherwise escalate wildfire risks.

" Pellets is expected to be the largest segment during the forecast period based on type."

By type, the solid biomass feedstock market has been split into four types: chips, pellets, briquettes, and others. Governments worldwide are offering subsidies and incentives to promote biomass pellet usage, aligning with renewable energy targets to drive demand. For example, The Biomass Thermal Utilization Act (BTU Act) in North America and initiatives by the Indian Renewable Energy Development Agency (IREDA) further support biomass pellet adoption

"By application, biomethane segment is expected to be the fastest growing segment during the forecast period."

Based on the application, the solid biomass feedstock market is segmented into electricity, heat, biofuel, and biomethane. The biomethane segment is expected to be the fastest growing segment of the solid biomass feedstock market during the forecast period. Biomethane can be used as a substitute of natural gas to combat environment emission as well as existing infrastructure compatibility drives the demand for biomethane.

"Asia Pacific is expected to be the largest region in the solid biomass feedstock market."

Asia Pacific is expected to be the largest region in the solid biomass feedstock market during the forecast period. Governments in countries such as China, Japan and India are playing a proactive role in reducing CO2 emissions which fosters the growth of biofuel and biomethane in the region. The increasing adoption of biofuels and biomethane in the region drives the growth of the solid biomass feedstock market. Initiatives to reduce CO2 emissions using biofuel, heat, and electricity and improve energy efficiency are supported by the Ministry of New and Renewable Energy (MNRE), International Renewable Energy Agency (IRENA), International Monetary Fund (IMF), International Institute of Sustainable Development, Bioenergy International; as a result, manufacturing solid biomass feedstock is encouraged.

Breakdown of Primaries:

In-depth interviews have been conducted with various key industry participants, subject-matter experts, C-level executives of key market players, and industry consultants, among other experts, to obtain and verify critical qualitative and quantitative information and assess future market prospects. The distribution of primary interviews is as follows:

By Company Type: Tier 1- 65%, Tier 2- 24%, and Tier 3- 11%

By Designation: C-Level- 30%, Director Level- 25%, and Others- 45%

By Region: North America- 20%, Europe- 25%, Asia Pacific- 30%, Middle East & Africa- 15%, South America- 10%

Note: Others include sales managers, engineers, and regional managers.

Note: The tiers of the companies are defined on the basis of their total revenues as of 2022. Tier 1: > USD 1 billion, Tier 2: From USD 500 million to USD 1 billion, and Tier 3: < USD 500 million

The solid biomass feedstock market is dominated by a few major players that have a wide regional presence. The leading players in the solid biomass feedstock market are Stora Enso (Finland), Drax Group plc (UK), Segezha Group (UK), Enviva Inc. (US), and Lignetics, Inc. (US). The major strategy adopted by the players includes new partnerships, collaboration, acquisition, and investments & expansions.

Research Coverage:

The report defines, describes, and forecasts the global solid biomass feedstock market by source, type, application, end user and region. It also offers a detailed qualitative and quantitative analysis of the market. The report comprehensively reviews the major market drivers, restraints, opportunities, and challenges. It also covers various important aspects of the market. These include an analysis of the competitive landscape, market dynamics, market estimates in terms of value, and future trends in thedirect air capture market.

Key Benefits of Buying the Report

- Increasing emphasis on net zero emission and supportive government policies, and need for alternative to fossil fuels are few of the key factors driving the solid biomass feedstock market. Factors such as complexities associated with pre treatment restrain the growth of the market. The growing energy transition towards reducing carbon emission is expected to present lucrative opportunities for the players operating in the solid biomass feedstock market. The logistics and supply chain management challenges pose a major challenge for the players, especially for emerging players operating in the solid biomass feedstock market.

- Product Development/ Innovation: The solid biomass feedstock market is witnessing significant product development and innovation, driven by the growing demand for environmentally friendly, safe and sustainable products.

- Market Development: Drax Group plc collaborated with Patch to elevate its carbon credit offerings. Patch's software assists participants in the voluntary carbon market in acquiring, trading, and overseeing credits. Through the Patch Radius software solution, Drax clients can effortlessly procure various portfolios of carbon credits, including those originating from BECCS by Drax. Aligned with Drax's aspirations in carbon removal, this partnership seeks to expedite the carbon market by simplifying carbon credit transactions for businesses of all scales striving to fulfill their climate objectives.

- Market Diversification: Lignetics, Inc. launched the premium BBQ Wood Chips and BBQ Wood chunks. Premium BBQ Wood Chips and BBQ Wood Chunks are equally appealing to both, mainstream grillers and enthusiasts. Crafted from 100% natural premium hardwoods, these products are kiln-dried to deliver the desired flavors and aromas.

Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players, like include Drax Group plc (Europe), Enviva Inc. (US), Arbaflame (Norway), REDAL (Lithuania), and Ecostrat Inc. (Canada), among others in the solid biomass feedstock market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 INCLUSIONS AND EXCLUSIONS

- 1.4 MARKET SCOPE

- 1.4.1 SOLID BIOMASS FEEDSTOCK MARKET SEGMENTATION

- 1.4.2 REGIONAL SCOPE

- 1.4.3 YEARS CONSIDERED

- 1.4.4 CURRENCY

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 IMPACT OF RECESSION

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 SOLID BIOMASS FEEDSTOCK MARKET: RESEARCH DESIGN

- 2.2 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 2 DATA TRIANGULATION

- 2.3 PRIMARY AND SECONDARY RESEARCH

- 2.3.1 SECONDARY DATA

- TABLE 1 MAJOR SECONDARY SOURCES

- 2.3.1.1 Key data from secondary sources

- 2.3.2 PRIMARY DATA

- TABLE 2 PRIMARY INTERVIEW PARTICIPANTS

- 2.3.2.1 Key insights from primary sources

- 2.3.2.2 Breakdown of primaries

- FIGURE 3 BREAKDOWN OF PRIMARIES: BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.4 MARKET SIZE ESTIMATION

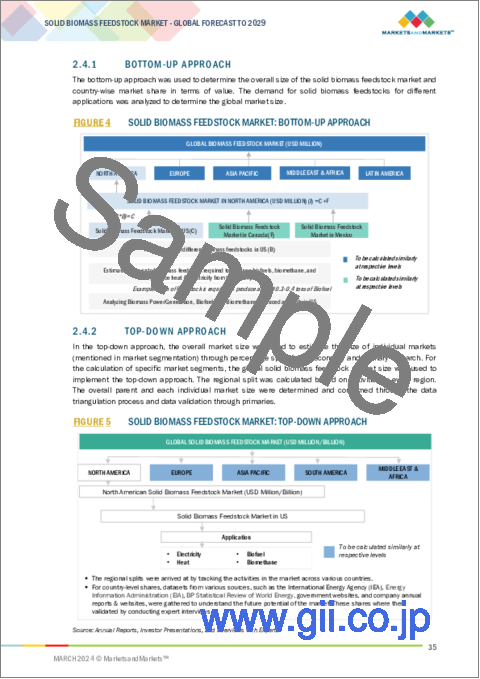

- 2.4.1 BOTTOM-UP APPROACH

- FIGURE 4 SOLID BIOMASS FEEDSTOCK MARKET: BOTTOM-UP APPROACH

- 2.4.2 TOP-DOWN APPROACH

- FIGURE 5 SOLID BIOMASS FEEDSTOCK MARKET: TOP-DOWN APPROACH

- 2.5 DEMAND-SIDE ANALYSIS

- 2.5.1 DEMAND-SIDE METRICS

- FIGURE 6 METRICS CONSIDERED TO ASSESS DEMAND FOR SOLID BIOMASS FEEDSTOCK

- 2.5.1.1 Assumptions for demand-side analysis

- 2.5.1.2 Calculations for demand-side analysis

- 2.6 SUPPLY-SIDE ANALYSIS

- 2.6.1 SUPPLY-SIDE METRICS

- FIGURE 7 KEY METRICS CONSIDERED TO ASSESS SUPPLY OF SOLID BIOMASS FEEDSTOCK

- FIGURE 8 SOLID BIOMASS FEEDSTOCK MARKET: SUPPLY-SIDE ANALYSIS

- 2.6.2 CALCULATIONS FOR SUPPLY-SIDE ANALYSIS

- 2.6.3 ASSUMPTIONS FOR SUPPLY-SIDE ANALYSIS

- 2.7 FORECAST

- 2.7.1 RISK ASSESSMENT

- 2.7.2 RECESSION IMPACT

3 EXECUTIVE SUMMARY

- TABLE 3 SOLID BIOMASS FEEDSTOCK MARKET SNAPSHOT

- FIGURE 9 ASIA PACIFIC HELD LARGEST SHARE OF SOLID BIOMASS FEEDSTOCK MARKET IN 2023

- FIGURE 10 FOREST WASTE SEGMENT TO LEAD SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, BY 2029

- FIGURE 11 PELLETS SEGMENT TO DOMINATE SOLID BIOMASS FEEDSTOCK MARKET BY 2029

- FIGURE 12 ELECTRICITY TO BE LARGEST APPLICATION IN SOLID BIOMASS FEEDSTOCK BY 2029

- FIGURE 13 UTILITIES SEGMENT TO BE DOMINANT END USER BY 2029

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES IN SOLID BIOMASS FEEDSTOCK MARKET

- FIGURE 14 INCREASING EMPHASIS ON RENEWABLE ENERGY TO BOOST MARKET GROWTH

- 4.2 SOLID BIOMASS FEEDSTOCK MARKET, BY REGION

- FIGURE 15 EUROPE TO WITNESS FASTEST GROWTH DURING FORECAST PERIOD

- 4.3 SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE

- FIGURE 16 FOREST WASTE TO HOLD MAJOR MARKET SHARE, BY SOURCE, BY 2029

- 4.4 SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE

- FIGURE 17 PELLETS SEGMENT TO COMMAND SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, BY 2029

- 4.5 SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION

- FIGURE 18 ELECTRICITY SEGMENT TO DOMINATE SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, BY 2029

- 4.6 SOLID BIOMASS FEEDSTOCK MARKET, BY END USER

- FIGURE 19 UTILITIES SEGMENT TO HOLD LARGEST MARKET SHARE, BY END USER, BY 2029

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 20 SOLID BIOMASS FEEDSTOCK MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Growing environmental concerns

- FIGURE 21 GLOBAL CO2 EMISSION FROM ENERGY COMBUSTION AND INDUSTRIAL PROCESSES, 2012-2022

- 5.2.1.2 Growing demand for biofuels

- FIGURE 22 GLOBAL BIOFUEL DEMAND, 2023-2028

- 5.2.2 RESTRAINTS

- 5.2.2.1 Complexities associated with pre-treatment of solid biomass feedstock

- 5.2.2.2 High costs associated with feedstock

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing emphasis on waste management

- 5.2.3.2 High depletion rate of fossil fuels

- FIGURE 23 GLOBAL CONSUMPTION OF FOSSIL FUELS, 2012-2022

- 5.2.4 CHALLENGES

- 5.2.4.1 Challenges associated with logistics and supply chain management

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 24 SOLID BIOMASS FEEDSTOCK MARKET: TRENDS/DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 SUPPLY CHAIN ANALYSIS

- FIGURE 25 SOLID BIOMASS FEEDSTOCK MARKET: SUPPLY CHAIN ANALYSIS

- 5.4.1 RAW MATERIAL SUPPLY

- 5.4.2 FEEDSTOCK DEVELOPMENT

- 5.4.3 DISTRIBUTORS

- 5.4.4 END USERS

- 5.5 MARKET MAP

- FIGURE 26 SOLID BIOMASS FEEDSTOCK MARKET MAPPING

- TABLE 4 COMPANIES AND THEIR ROLE IN SOLID BIOMASS FEEDSTOCK ECOSYSTEM

- FIGURE 27 SOLID BIOMASS FEEDSTOCK MARKET: ECOSYSTEM MAPPING

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 KEY TECHNOLOGIES

- 5.6.1.1 Crushing

- 5.6.1.2 Grinding

- 5.6.1.3 Drying

- 5.6.1.4 Separation

- 5.6.2 COMPLIMENTARY TECHNOLOGIES

- 5.6.2.1 Storage and Handling

- 5.6.1 KEY TECHNOLOGIES

- 5.7 CASE STUDY ANALYSIS

- 5.7.1 COOP GROUP IMPLEMENTS SUSTAINABLE ENERGY PRACTICES TO PRODUCE INDUSTRIAL HEAT

- 5.7.1.1 Challenges

- 5.7.1.2 Solution

- 5.7.2 OPPORTUNITIES FOR POWER GENERATION USING WOODY BIOMASS IN VIETNAM

- 5.7.2.1 Overview

- 5.7.1 COOP GROUP IMPLEMENTS SUSTAINABLE ENERGY PRACTICES TO PRODUCE INDUSTRIAL HEAT

- 5.8 PATENT ANALYSIS

- FIGURE 28 SOLID BIOMASS FEEDSTOCK MARKET: PATENTS APPLIED AND GRANTED, 2013-2023

- 5.8.1 MAJOR PATENTS

- TABLE 5 SOLID BIOMASS FEEDSTOCK MARKET: MAJOR PATENTS, 2019-2023

- 5.9 PRICING ANALYSIS

- 5.9.1 AVERAGE SELLING PRICE TREND, BY COMPANY & TYPE

- TABLE 6 COST SUMMARY FOR SOLID BIOMASS FEEDSTOCK TYPE, BY COMPANY

- 5.9.2 AVERAGE SELLING PRICE TREND, BY REGION

- TABLE 7 COST SUMMARY FOR SOLID BIOMASS FEEDSTOCK, BY REGION (USD/TON)

- FIGURE 29 AVERAGE SELLING PRICE TREND, BY REGION, 2019-2029 (USD/TON)

- 5.10 TRADE ANALYSIS

- 5.10.1 EXPORT SCENARIO

- TABLE 8 EXPORT DATA FOR HS CODE 382510-MUNICIPAL WASTE, BY COUNTRY, 2020-2022 (USD THOUSAND)

- FIGURE 30 EXPORT DATA FOR HS CODE 382510-MUNICIPAL WASTE, BY COUNTRY, 2020-2022 (USD THOUSAND)

- 5.10.2 IMPORT SCENARIO

- TABLE 9 IMPORT DATA FOR HS CODE 382510-MUNICIPAL WASTE, BY COUNTRY, 2020-2022 (USD THOUSAND)

- FIGURE 31 IMPORT DATA FOR HS CODE 382510-MUNICIPAL WASTE, BY COUNTRY, 2020-2022 (USD THOUSAND)

- 5.11 KEY CONFERENCES AND EVENTS, 2024-2025

- TABLE 10 SOLID BIOMASS FEEDSTOCK MARKET: CONFERENCES AND EVENTS, 2024-2025

- 5.12 REGULATORY LANDSCAPE

- 5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 13 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 MIDDLE EAST AND AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 SOUTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 SOLID BIOMASS FEEDSTOCK MARKET: REGULATIONS & POLICIES

- 5.13 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 32 SOLID BIOMASS FEEDSTOCK MARKET: PORTER'S FIVE FORCES ANALYSIS

- TABLE 17 SOLID BIOMASS FEEDSTOCK MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.13.1 THREAT OF SUBSTITUTES

- 5.13.2 BARGAINING POWER OF SUPPLIERS

- 5.13.3 BARGAINING POWER OF BUYERS

- 5.13.4 THREAT OF NEW ENTRANTS

- 5.13.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 33 SOLID BIOMASS FEEDSTOCK MARKET: INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS

- TABLE 18 SOLID BIOMASS FEEDSTOCK MARKET: INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP END USERS (%)

- 5.14.2 BUYING CRITERIA

- FIGURE 34 SOLID BIOMASS FEEDSTOCK MARKET: KEY BUYING CRITERIA FOR TOP END USERS

- TABLE 19 SOLID BIOMASS FEEDSTOCK MARKET: KEY BUYING CRITERIA FOR TOP END USERS

- 5.15 INVESTMENT AND FUNDING SCENARIO

- FIGURE 35 INVESTMENT AND FUNDING SCENARIO

6 SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE

- 6.1 INTRODUCTION

- FIGURE 36 SOLID BIOMASS FEEDSTOCK MARKET SHARE, BY SOURCE, 2023 (%)

- TABLE 20 SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 21 SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 6.2 AGRICULTURE WASTE

- 6.2.1 ABUNDANT AVAILABILITY TO DRIVE MARKET

- TABLE 22 AGRICULTURE WASTE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 23 AGRICULTURE WASTE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.3 FOREST WASTE

- 6.3.1 INCREASING ADOPTION OF AI FOR ENHANCED EFFICIENCY TO BOOST MARKET GROWTH

- TABLE 24 FOREST WASTE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 25 FOREST WASTE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.4 ANIMAL WASTE

- 6.4.1 GROWING NEED TO MANAGE ANIMAL WASTE CONTRIBUTES TO SEGMENT GROWTH

- TABLE 26 ANIMAL WASTE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 27 ANIMAL WASTE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.5 MUNICIPAL WASTE

- 6.5.1 GOVERNMENT INITIATIVES TO MANAGE MUNICIPAL WASTE THROUGH BIOENERGY SOLUTIONS

- TABLE 28 MUNICIPAL WASTE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 29 MUNICIPAL WASTE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.5.2 INDUSTRIAL WASTE

- 6.5.3 SOLID WASTE

7 SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE

- 7.1 INTRODUCTION

- FIGURE 37 SOLID BIOMASS FEEDSTOCK MARKET SHARE, BY TYPE, 2023 (%)

- TABLE 30 SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2019-2023 (MILLION TONS)

- TABLE 31 SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2024-2029 (MILLION TONS)

- TABLE 32 SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 33 SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 7.2 CHIPS

- 7.2.1 GROWING RELIANCE ON CHIPS FOR ENERGY AND HEATING IN RESIDENTIAL & COMMERCIAL APPLICATIONS

- TABLE 34 CHIPS: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 35 CHIPS: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.3 PELLETS

- 7.3.1 FAVORABLE GOVERNMENT POLICIES TO DRIVE SEGMENT GROWTH

- TABLE 36 PELLETS: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 37 PELLETS: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.4 BRIQUETTES

- 7.4.1 NEED FOR ALTERNATIVE TO FOSSIL FUELS TO BOOST SEGMENT

- TABLE 38 BRIQUETTES: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 39 BRIQUETTES: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 7.5 OTHERS

- 7.5.1 NEED FOR EFFICIENT HANDLING AND STORAGE OF BIOMASS FEEDSTOCK LIKELY TO DRIVE MARKET

- TABLE 40 OTHERS: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 41 OTHERS: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

8 SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- FIGURE 38 SOLID BIOMASS FEEDSTOCK MARKET SHARE, BY APPLICATION, 2023 (%)

- TABLE 42 SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2019-2023 (USD MILLION)

- TABLE 43 SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 8.2 ELECTRICITY

- 8.2.1 GLOBAL NET-ZERO EMISSION GOALS TO DRIVE GROWTH

- TABLE 44 ELECTRICITY: SOLID BIOMASS MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 45 ELECTRICITY: SOLID BIOMASS MARKET, BY REGION, 2024-2029 (USD MILLION)

- 8.3 HEAT

- 8.3.1 NEED FOR SUSTAINABLE HEATING SOLUTIONS TO BOOST SEGMENT

- TABLE 46 HEAT: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 47 HEAT: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 8.4 BIOFUEL

- 8.4.1 FAVORABLE GOVERNMENT POLICIES DRIVE USE OF BIOFUEL

- 8.4.2 BIODIESEL

- 8.4.3 BIOETHANOL

- 8.4.4 RENEWABLE DIESEL

- 8.4.5 BIOJET FUEL

- TABLE 48 BIOFUEL: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 49 BIOFUEL: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 8.5 BIOMETHANE

- 8.5.1 EXISTING INFRASTRUCTURE COMPATIBILITY LIKELY TO BOOST DEMAND FOR BIOMETHANE

- TABLE 50 BIOMETHANE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 51 BIOMETHANE: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

9 SOLID BIOMASS FEEDSTOCK MARKET, BY END USER

- 9.1 INTRODUCTION

- FIGURE 39 SOLID BIOMASS FEEDSTOCK MARKET SHARE, BY END USER, 2023 (%)

- TABLE 52 SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 53 SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2024-2029 (USD MILLION)

- 9.2 RESIDENTIAL & COMMERCIAL

- 9.2.1 GROWING NEED FOR SUSTAINABLE HEATING SOLUTIONS DRIVES MARKET

- TABLE 54 RESIDENTIAL & COMMERCIAL: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 55 RESIDENTIAL & COMMERCIAL: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 9.3 INDUSTRIAL

- 9.3.1 INCREASING NEED FOR CLEAN ENERGY IN INDUSTRIAL SETTINGS TO BOOST MARKET

- TABLE 56 INDUSTRIAL: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 57 INDUSTRIAL: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- 9.4 UTILITIES

- 9.4.1 GROWING NEED FOR ADOPTION OF RENEWABLE ENERGY TO DRIVE SEGMENT

- TABLE 58 UTILITIES: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 59 UTILITIES: SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

10 SOLID BIOMASS FEEDSTOCK MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 40 SOLID BIOMASS FEEDSTOCK MARKET IN EUROPE TO REGISTER HIGHEST CAGR FROM 2024 TO 2029

- TABLE 60 SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (USD MILLION)

- TABLE 61 SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 62 SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2019-2023 (MILLION TONS)

- TABLE 63 SOLID BIOMASS FEEDSTOCK MARKET, BY REGION, 2024-2029 (MILLION TONS)

- 10.2 ASIA PACIFIC

- FIGURE 41 ASIA PACIFIC: REGIONAL SNAPSHOT (2023)

- 10.2.1 ASIA PACIFIC: RECESSION IMPACT

- 10.2.2 BY SOURCE

- TABLE 64 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 65 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.2.3 BY TYPE

- TABLE 66 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 67 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.2.4 BY APPLICATION

- TABLE 68 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2019-2023 (USD MILLION)

- TABLE 69 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.2.5 BY END USER

- TABLE 70 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 71 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.2.6 BY COUNTRY

- TABLE 72 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 73 ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 10.2.6.1 China

- 10.2.6.1.1 Emphasis on harnessing agricultural and forest waste for feedstock to drive market

- 10.2.6.1.2 By source

- 10.2.6.1 China

- TABLE 74 CHINA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 75 CHINA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.2.6.2 India

- 10.2.6.2.1 Acceleration of clean energy adoption to drive market growth

- 10.2.6.2.2 By source

- 10.2.6.2 India

- TABLE 76 INDIA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 77 INDIA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.2.6.3 Japan

- 10.2.6.3.1 Ongoing net-zero carbon emission initiatives by government - key driver

- 10.2.6.3.2 By source

- 10.2.6.3 Japan

- TABLE 78 JAPAN: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 79 JAPAN: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.2.6.4 Australia

- 10.2.6.4.1 Higher demand for renewable energy resources to boost growth

- 10.2.6.4.2 By source

- 10.2.6.4 Australia

- TABLE 80 AUSTRALIA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 81 AUSTRALIA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.2.6.5 Thailand

- 10.2.6.5.1 Increasing focus on minimizing carbon footprint to stimulate market growth

- 10.2.6.5.2 By source

- 10.2.6.5 Thailand

- TABLE 82 THAILAND: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 83 THAILAND: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.2.6.6 Rest of Asia Pacific

- 10.2.6.6.1 By source

- 10.2.6.6 Rest of Asia Pacific

- TABLE 84 REST OF ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 85 REST OF ASIA PACIFIC: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.3 EUROPE

- 10.3.1 EUROPE: RECESSION IMPACT

- FIGURE 42 EUROPE: REGIONAL SNAPSHOT (2023)

- 10.3.2 BY SOURCE

- TABLE 86 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 87 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.3.3 BY TYPE

- TABLE 88 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 89 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.3.4 BY APPLICATION

- TABLE 90 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2019-2023 (USD MILLION)

- TABLE 91 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.3.5 BY END USER

- TABLE 92 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 93 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.6 BY COUNTRY

- TABLE 94 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 95 EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 10.3.6.1 Germany

- 10.3.6.1.1 Increasing focus on reducing greenhouse gas emissions to drive market

- 10.3.6.1.2 By source

- 10.3.6.1 Germany

- TABLE 96 GERMANY: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 97 GERMANY: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.3.6.2 UK

- 10.3.6.2.1 Increasing focus on net-zero emission goals - key market booster

- 10.3.6.2.2 By source

- 10.3.6.2 UK

- TABLE 98 UK: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 99 UK: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.3.6.3 France

- 10.3.6.3.1 Increasing utilization of biomass for electricity production and heating purposes

- 10.3.6.3.2 By source

- 10.3.6.3 France

- TABLE 100 FRANCE: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 101 FRANCE: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.3.6.4 Italy

- 10.3.6.4.1 Growing role in European market through targets, plans, and investments for renewable energy expansion

- 10.3.6.4.2 By source

- 10.3.6.4 Italy

- TABLE 102 ITALY: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 103 ITALY: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.3.6.5 Sweden

- 10.3.6.5.1 Innovative strategy for sustainability in renewable energy to boost market

- 10.3.6.5.2 By source

- 10.3.6.5 Sweden

- TABLE 104 SWEDEN: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 105 SWEDEN: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.3.6.6 Russia

- 10.3.6.6.1 Biomass exports to drive renewable energy growth

- 10.3.6.6.2 By source

- 10.3.6.6 Russia

- TABLE 106 RUSSIA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 107 RUSSIA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.3.6.7 Rest of Europe

- 10.3.6.7.1 By source

- 10.3.6.7 Rest of Europe

- TABLE 108 REST OF EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 109 REST OF EUROPE: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.4 NORTH AMERICA

- FIGURE 43 NORTH AMERICA: REGIONAL SNAPSHOT (2023)

- 10.4.1 NORTH AMERICA: RECESSION IMPACT

- 10.4.2 BY SOURCE

- TABLE 110 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 111 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.4.3 BY TYPE

- TABLE 112 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 113 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.4.4 BY APPLICATION

- TABLE 114 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2019-2023 (USD MILLION)

- TABLE 115 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.4.5 BY END USER

- TABLE 116 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 117 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.6 BY COUNTRY

- TABLE 118 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 119 NORTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 10.4.6.1 US

- 10.4.6.1.1 Favorable government policies and incentives to drive market

- 10.4.6.1.2 By source

- 10.4.6.1 US

- TABLE 120 US: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 121 US: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.4.6.2 Canada

- 10.4.6.2.1 Government support for adoption of renewable energy to boost market

- 10.4.6.2.2 By source

- 10.4.6.2 Canada

- TABLE 122 CANADA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 123 CANADA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.4.6.3 Mexico

- 10.4.6.3.1 Increasing renewable electricity generation using solid biomass feedstock - key driver

- 10.4.6.3.2 By source

- 10.4.6.3 Mexico

- TABLE 124 MEXICO: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 125 MEXICO: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.5 MIDDLE EAST & AFRICA

- 10.5.1 MIDDLE EAST & AFRICA: RECESSION IMPACT

- 10.5.2 BY SOURCE

- TABLE 126 MIDDLE EAST & ARICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 127 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.5.3 BY TYPE

- TABLE 128 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 129 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.5.4 BY APPLICATION

- TABLE 130 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2019-2023 (USD MILLION)

- TABLE 131 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.5.5 BY END USER

- TABLE 132 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 133 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5.6 BY COUNTRY

- TABLE 134 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 135 MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 10.5.6.1 GCC countries

- 10.5.6.1.1 Saudi Arabia

- 10.5.6.1.2 UAE

- 10.5.6.1.3 Other GCC countries

- 10.5.6.1.4 By source

- 10.5.6.1 GCC countries

- TABLE 136 GCC COUNTRIES: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 137 GCC COUNTRIES: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.5.6.2 Rest of Middle East & Africa

- 10.5.6.2.1 Increasing shift toward bioenergy to drive market growth

- 10.5.6.2.2 By source

- 10.5.6.2 Rest of Middle East & Africa

- TABLE 138 REST OF MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 139 REST OF MIDDLE EAST & AFRICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.6 SOUTH AMERICA

- 10.6.1 SOUTH AMERICA: RECESSION IMPACT

- 10.6.2 BY SOURCE

- TABLE 140 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 141 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.6.3 BY TYPE

- TABLE 142 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2019-2023 (USD MILLION)

- TABLE 143 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 10.6.4 BY APPLICATION

- TABLE 144 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2019-2023 (USD MILLION)

- TABLE 145 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 10.6.5 BY END USER

- TABLE 146 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2019-2023 (USD MILLION)

- TABLE 147 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.6.6 BY COUNTRY

- TABLE 148 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2019-2023 (USD MILLION)

- TABLE 149 SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- 10.6.6.1 Brazil

- 10.6.6.1.1 Rising shift toward biomass energy to drive growth of market

- 10.6.6.1.2 By source

- 10.6.6.1 Brazil

- TABLE 150 BRAZIL: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 151 BRAZIL: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.6.6.2 Argentina

- 10.6.6.2.1 Abundance of biomass resources - key growth driver

- 10.6.6.2.2 By source

- 10.6.6.2 Argentina

- TABLE 152 ARGENTINA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 153 ARGENTINA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.6.6.3 Chile

- 10.6.6.3.1 Government incentive schemes to promote growth of feedstock

- 10.6.6.3.2 By source

- 10.6.6.3 Chile

- TABLE 154 CHILE: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 155 CHILE: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

- 10.6.6.4 Rest of South America

- 10.6.6.4.1 By source

- 10.6.6.4 Rest of South America

- TABLE 156 REST OF SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2019-2023 (USD MILLION)

- TABLE 157 REST OF SOUTH AMERICA: SOLID BIOMASS FEEDSTOCK MARKET, BY SOURCE, 2024-2029 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 STRATEGIES ADOPTED BY KEY PLAYERS, 2019-2023

- TABLE 158 SOLID BIOMASS FEEDSTOCK MARKET: OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS, 2019-2023

- 11.3 MARKET SHARE ANALYSIS, 2023

- FIGURE 44 MARKET SHARE ANALYSIS OF TOP PLAYERS, 2023

- 11.4 MARKET EVALUATION FRAMEWORK

- TABLE 160 MARKET EVALUATION FRAMEWORK 2019-2023

- 11.5 REVENUE ANALYSIS, 2018-2022

- FIGURE 45 SOLID BIOMASS FEEDSTOCK MARKET: SEGMENTAL REVENUE ANALYSIS, 2018-2022

- 11.5.1 COMPANY VALUATION AND FINANCIAL METRICS

- FIGURE 46 COMPANY VALUATION

- FIGURE 47 FINANCIAL METRICS

- 11.6 BRAND/PRODUCT COMPARISON

- 11.7 COMPANY EVALUATION MATRIX: KEY PLAYERS, 2023

- 11.7.1 STARS

- 11.7.2 EMERGING LEADERS

- 11.7.3 PERVASIVE PLAYERS

- 11.7.4 PARTICIPANTS

- FIGURE 48 SOLID BIOMASS FEEDSTOCK MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), 2023

- 11.7.5 COMPANY FOOTPRINT, KEY PLAYERS, 2023

- 11.7.5.1 Company footprint

- FIGURE 49 SOLID BIOMASS FEEDSTOCK: PRODUCT FOOTPRINT

- FIGURE 50 SOLID BIOMASS FEEDSTOCK: MARKET FOOTPRINT

- 11.7.5.2 Region footprint

- TABLE 161 SOLID BIOMASS FEEDSTOCK: REGION FOOTPRINT

- 11.7.5.3 Source footprint

- TABLE 162 SOLID BIOMASS FEEDSTOCK MARKET: SOURCE FOOTPRINT

- 11.7.5.4 Type footprint

- TABLE 163 SOLID BIOMASS FEEDSTOCK MARKET: TYPE FOOTPRINT

- 11.7.5.5 Application footprint

- TABLE 164 SOLID BIOMASS FEEDSTOCK MARKET: APPLICATION FOOTPRINT

- 11.7.5.6 End user footprint

- TABLE 165 SOLID BIOMASS FEEDSTOCK MARKET: END USER FOOTPRINT

- 11.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES, 2023

- 11.8.1 PROGRESSIVE COMPANIES

- 11.8.2 RESPONSIVE COMPANIES

- 11.8.3 DYNAMIC COMPANIES

- 11.8.4 STARTING BLOCKS

- FIGURE 51 SOLID BIOMASS FEEDSTOCK MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), 2023

- 11.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

- 11.8.5.1 Key startups/SMES

- TABLE 166 SOLID BIOMASS FEEDSTOCK MARKET: KEY STARTUPS/SMES

- 11.8.5.2 Competitive benchmarking of key startups/SMES

- TABLE 167 SOLID BIOMASS FEEDSTOCK MARKET: COMPETITIVE BENCHMARKING OF STARTUPS/SMES

- 11.9 COMPETITIVE SCENARIOS AND TRENDS

- 11.9.1 PRODUCT LAUNCHES

- TABLE 168 SOLID BIOMASS FEEDSTOCK MARKET: PRODUCT LAUNCHES, JANUARY 2019-DECEMBER 2023

- 11.9.2 DEALS

- TABLE 169 SOLID BIOMASS FEEDSTOCK MARKET: DEALS, JANUARY 2019-DECEMBER 2023

- 11.9.3 EXPANSIONS

- TABLE 170 SOLID BIOMASS FEEDSTOCK MARKET: EXPANSIONS, JANUARY 2019-DECEMBER 2023

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- (Business overview, Products/Solutions/Services offered, Recent developments, MnM view, Right to win, Strategic choices made, and Weaknesses and Competitive threats)**

- 12.1.1 DRAX GROUP PLC

- FIGURE 52 DRAX GROUP PLC: COMPANY SNAPSHOT

- 12.1.2 ENVIVA INC.

- FIGURE 53 ENVIVA INC.: COMPANY SNAPSHOT

- 12.1.3 ARBAFLAME

- TABLE 181 ARBAFLAME: DEALS

- TABLE 182 ARBAFLAME: EXPANSIONS

- 12.1.4 REDAL

- TABLE 183 REDAL: BUSINESS OVERVIEW

- TABLE 184 REDAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.5 ECOSTRAT INC.

- TABLE 186 ECOSTRAT INC.: BUSINESS OVERVIEW

- TABLE 187 ECOSTRAT INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.6 STORA ENSO

- FIGURE 54 STORA ENSO: COMPANY SNAPSHOT

- 12.1.7 SEGEZHA GROUP

- TABLE 190 SEGEZHA GROUP: BUSINESS OVERVIEW

- FIGURE 55 SEGEZHA GROUP: COMPANY SNAPSHOT

- 12.1.8 LIGNETICS, INC.

- TABLE 192 LIGNETICS, INC.: BUSINESS OVERVIEW

- TABLE 193 LIGNETICS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.9 RENTECH, INC.

- TABLE 195 RENTECH, INC.: BUSINESS OVERVIEW

- 12.1.10 LAND ENERGY LTD

- TABLE 197 LAND ENERGY LTD: BUSINESS OVERVIEW

- TABLE 198 LAND ENERGY LTD: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.11 SUPREME INDUSTRIES

- TABLE 199 SUPREME INDUSTRIES: BUSINESS OVERVIEW

- 12.1.12 WISMAR PELLETS GMBH

- TABLE 201 WISMAR PELLETS GMBH: BUSINESS OVERVIEW

- 12.1.13 SHREE INDUSTRIES

- TABLE 204 SHREE INDUSTRIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 12.1.14 MALLARD CREEK INC

- 12.1.15 SUBHAM INDUSTRIES

- TABLE 207 SUBHAM INDUSTRIES: BUSINESS OVERVIEW

- 12.2 OTHER PLAYERS

- 12.2.1 FRAM FUELS

- 12.2.2 GILDALE FARMS

- 12.2.3 GOMBELLA INTEGRATED SERVICES LTD.

- 12.2.4 VALFEI PRODUCTS INC.

- 12.2.5 FOREST CONCEPTS

- 12.2.6 BLACKWOOD TECHNOLOGY

- 12.2.7 JP GREEN FUELS

- 12.2.8 GRAANUL INVEST

- 12.2.9 VIRIDIS ENERGY INC.

- 12.2.10 GROWMORE BIOTECH LTD

- *Details on Business overview, Products/Solutions/Services offered, Recent developments, MnM view, Right to win, Strategic choices made, and Weaknesses and Competitive threats might not be captured in case of unlisted companies.

13 APPENDIX

- 13.1 INSIGHTS FROM INDUSTRY EXPERTS

- 13.2 DISCUSSION GUIDE

- 13.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.4 CUSTOMIZATION OPTIONS

- 13.5 RELATED REPORTS

- 13.6 AUTHOR DETAILS