|

|

市場調査レポート

商品コード

1422236

医療向けAIの世界市場:提供別、技術別、用途別、エンドユーザー別、地域別 - 予測(~2029年)Artificial Intelligence in Healthcare Market by Offering, Technology, Application, End User & Region - Global Forecast to 2029 |

||||||

|

|

|||||||

|

● お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。 詳細はお問い合わせください。 |

|||||||

| 医療向けAIの世界市場:提供別、技術別、用途別、エンドユーザー別、地域別 - 予測(~2029年) |

|

出版日: 2024年02月05日

発行: MarketsandMarkets

ページ情報: 英文 360 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の医療向けAIの市場規模は、2024年の209億米ドルから2029年までに1,484億米ドルに達し、2024年~2029年にCAGRで48.1%の成長が見込まれます。

医療向けAIへの強い注目、高齢者ケアにおけるAIベースのツールの将来性の高まり、ヒトを認識するAIシステムの開発動向の高まり、創薬、ゲノム、イメージング、診断におけるAI技術の加速が、医療向けAI市場の成長を促進します。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2029年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2029年 |

| 単位 | 10億米ドル |

| セグメント | 提供別、技術別、用途別、エンドユーザー別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

「ソフトウェア市場が予測期間に最大のシェアを占める見込みです。」

ソフトウェアセグメントは、AIプラットフォームとAIソリューションに分類されます。ソフトウェアは、医療向けAIの統合と機能性を推進する基盤となる要素です。AIの頭脳の触媒として働き、自然言語処理や深層学習などの複雑な機械学習アルゴリズムの実装を可能にします。ソフトウェアが促進する効率的なデータ取り込みと管理に支えられたこれらのアルゴリズムは、AIシステムに広範な医療データセットを分析し、価値ある知見を導き出す力を与えます。実際の利用では、ソフトウェアは診断ツール、治療の個別化、バーチャルアシスタントにおいて極めて重要な役割を果たし、疾患の発見、治療計画、患者エンゲージメントの精度を高めます。さらに、ソフトウェアは管理自動化と予測分析を通じて医療業務を最適化し、効率改善と積極的な患者ケアに寄与します。医療向けAIのバックボーンとして、ソフトウェアは患者ケアの強化、早期診断、個別化治療に向けた革新的なソリューションを提供することで、情勢を一変させます。

「予測期間に自然言語処理セグメント市場が第2位のシェアを占める見込みです。」

臨床と研究のコミュニティは、電子健康レポート、臨床ノート、病理レポートなどの非構造化、半構造化テキスト文書の効率的な管理と開発に向け、医療でNLPを広く使用しています。このアルゴリズムは、ナラティブテキストの臨床文書から健康問題を抽出し、正確に解釈するために患者の電子問題リストに含めることを提案します。NLPは、文書前処理、健康問題検出、否定検出、文書後処理の4つのステップを含みます。Babylon Health(英国)は、チャットボットが対面診察で医師がするのと同じ質問をするためのアプリとNLPアルゴリズムを開発しました。このアプリは正式な診断の概要を説明するのではなく、音声と言語処理を使って症状を抽出し、プロファイル情報を医師に転送します。NLPは、臨床データをより正確に構造化し解釈するために、医療機関から大きな需要があります。さらに、コネクテッドデバイスの利用の増加に加え、膨大な量の患者データがこの市場の成長を加速させています。

「患者データリスク分析セグメントが予測期間に大きな市場シェアを占めます。」

医療における機械学習(ML)と自然言語処理(NLP)の融合は、患者の健康に関する予測的考察に大きな進歩をもたらします。多様なデータソースを活用するMLモデルは、医療記録、臨床検査、人口統計、社会的決定要因を分析し、特定の疾病リスクのある患者を特定し、NLPアルゴリズムは臨床記録から知見を抽出し、疾病の初期兆候を発見します。このシナジーにより、治療効果やライフスタイルなどの要素を考慮した、パーソナライズされた治療計画が可能になります。MLは潜在的な増悪を予測し、積極的な介入を可能にし、NLPは遠隔モニタリングに向けリアルタイムデータを解釈します。その利点は、患者の転帰の改善、コストの削減、医療上の意思決定の強化などです。しかし、データプライバシー、アルゴリズムの偏り、透明性の必要性といった課題が、医療における倫理的で責任あるAIの導入の重要性を示しています。

当レポートでは、世界の医療向けAI市場について調査分析し、主な促進要因と抑制要因、競合情勢、将来の動向などの情報を提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

- 医療向けAI市場企業にとっての魅力的な機会

- 医療向けAI市場:提供別

- 医療向けAI市場:技術別

- 医療向けAI市場:エンドユーザー別

- 医療向けAI市場:用途別

- 医療向けAI市場:国別

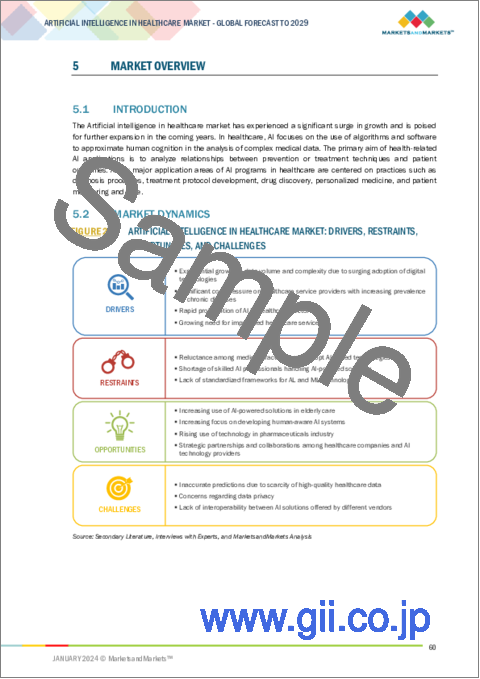

第5章 市場の概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 顧客のビジネスに影響を与える動向/混乱

- 価格分析

- 主要企業が提供するコンポーネントの平均販売価格(ASP)の動向(2020年~2029年)

- プロセッサーコンポーネント平均販売価格(ASP)の動向:地域別(2020年~2029年)

- バリューチェーン分析

- エコシステムマッピング

- 技術分析

- クラウドコンピューティング

- クラウドGPU

- 生成AI

- クラウドベースPACS

- マルチクラウド

- 特許分析

- 貿易分析

- 主な会議とイベント(2024年~2025年)

- ケーススタディ分析

- 関税、基準、規制情勢

- 規制機関、政府機関、その他の組織

- 基準

- 政府の規制

- ポーターのファイブフォース分析

- 主なステークホルダーと購入基準

第6章 医療向けAI市場:提供別

- イントロダクション

- ハードウェア

- プロセッサー

- メモリ

- ネットワーク

- ソフトウェア

- AIソリューション

- AIプラットフォーム

- サービス

- 展開・統合

- サポート・メンテナンス

第7章 医療向けAI市場:技術別

- イントロダクション

- 機械学習

- 深層学習

- 教師あり学習

- 強化学習

- 教師なし学習

- その他

- 自然言語処理

- IVR

- OCR

- パターン、画像認識

- 自動コーディング

- 分類

- テキスト分析

- 音声分析

- コンテキストアウェアコンピューティング

- デバイスコンテキスト

- ユーザーコンテキスト

- フィジカルコンテキスト

- コンピュータービジョン

第8章 医療向けAI市場:用途別

- イントロダクション

- 患者データ・リスク分析

- 入院患者ケア・病院管理

- 医用画像・診断

- ライフスタイル管理・遠隔患者モニタリング

- バーチャルアシスタント

- 創薬

- 研究

- 医療支援ロボット

- 精密医療

- 救急室・手術

- ウェアラブル

- メンタルヘルス

- サイバーセキュリティ

第9章 医療向けAI市場:エンドユーザー別

- イントロダクション

- 病院・医療提供者

- 患者

- 製薬企業・バイオテクノロジー企業

- 医療保険者

- その他

第10章 医療向けAI市場:地域別

- イントロダクション

- 北米

- 北米の不況の影響

- 米国

- カナダ

- メキシコ

- 欧州

- 欧州の不況の影響

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- アジア太平洋の不況の影響

- 中国

- 日本

- 韓国

- インド

- その他のアジア太平洋

- その他の地域

- その他の地域の不況の影響

- 南米

- GCC

- その他の中東・アフリカ

第11章 競合情勢

- 概要

- 主要企業が採用した戦略(2020年~2023年)

- 収益分析(2019年~2023年)

- 市場シェア分析(2023年)

- 企業の評価マトリクス(2023年)

- スタートアップ/中小企業(SME)の評価マトリクス(2023年)

- 競合シナリオと動向

第12章 企業プロファイル

- 主要企業

- KONINKLIJKE PHILIPS N.V.

- MICROSOFT

- SIEMENS HEALTHINEERS AG

- INTEL CORPORATION

- NVIDIA CORPORATION

- GOOGLE INC.

- GE HEALTHCARE

- MEDTRONIC

- MICRON TECHNOLOGY, INC.

- AMAZON.COM, INC.

- ORACLE

- JOHNSON & JOHNSON SERVICES, INC.

- その他の企業

- MERATIVE

- GENERAL VISION INC.

- CLOUDMEDX

- ONCORA MEDICAL

- ENLITIC, INC.

- LUNIT INC.

- QURE.AI

- TEMPUS

- COTA

- FDNA INC.

- RECURSION

- ATOMWISE INC.

- VIRGIN PULSE

- BABYLON HEALTHCARE SERVICES LTD

- MDLIVE (EVERNORTH GROUP)

- STRYKER

- QVENTUS

- SWEETCH

- SIRONA MEDICAL, INC.

- GINGER

- BIOBEAT

第13章 付録

The AI in Healthcare market is projected to grow from USD 20.9 billion in 2024 and is projected to reach USD 148.4 billion by 2029; it is expected to grow at a CAGR of 48.1% from 2024 to 2029. Strong focus on AI in Healthcare rising potential of AI-based tools for elderly care, increasing trend towards developing human-aware AI systems, and acceleration of AI technology in drug discovery, genomics, and imaging & diagnostics to fuel the growth of AI in Healthcare market.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2029 |

| Base Year | 2023 |

| Forecast Period | 2024-2029 |

| Units Considered | Value (USD Billion) |

| Segments | By Offering, Technology, Application, End User & Region |

| Regions covered | North America, Europe, Asia Pacific and RoW |

"Market for Software to hold the largest share during the forecast period."

The software segment is categorized into AI Platform and AI Solution. Software is the foundational element driving the integration and functionality of AI in healthcare. Acting as the catalyst for the AI brain, it enables the implementation of intricate machine learning algorithms such as natural language processing and deep learning. These algorithms, supported by efficient data ingestion and management facilitated by software, empower AI systems to analyze extensive medical datasets and derive valuable insights. In practical application, software plays a pivotal role in diagnostic tools, treatment personalization, and virtual assistants, enhancing the accuracy in disease detection, treatment planning, and patient engagement. Additionally, the software optimizes healthcare operations through administrative automation and predictive analytics, contributing to improved efficiency and proactive patient care. As the backbone of AI in healthcare, software transforms the landscape by offering innovative solutions for enhanced patient care, early diagnosis, and personalized treatment.

"Market for Natural Language Processing segment is projected to hold for second-largest share during the forecast timeline."

The clinical and research community widely uses NLP in healthcare for efficient managing and development of unstructured and semi-structured textual documents, including electronic health reports, clinical notes, and pathology reports. The algorithm extracts health problems from narrative text clinical documents and proposes inclusion in a patient's electronic problem list to interpret accurately. NLP involves four steps: document pre-processing, health problem detection, negation detection, and document post-processing. Babylon Health (UK) has developed an app and NLP algorithms to help a chatbot ask the same questions a doctor would ask during in-person examination. The app does not outline an official diagnosis; rather it uses speech and language processing to extract symptoms and forward the profile information to a doctor. NLP is experiencing significant demand from healthcare institutions for structuring and interpretation of clinical data more accurately. Moreover, the rising usage of connected devices, along with the massive volume of patients' data, accelerates the growth of this market.

"Market for patient data & risk analysis segment holds for major market share during the forecast period."

The convergence of machine learning (ML) and natural language processing (NLP) in healthcare offers significant advancements in predictive insights for patient health. Utilizing diverse data sources, ML models analyze medical records, lab tests, demographics, and social determinants to identify patients at risk of specific diseases, while NLP algorithms extract insights from clinical notes to spot early signs of illness. This synergy enables personalized treatment plans, considering factors like treatment response and lifestyle. ML predicts potential exacerbations, allowing proactive interventions, and NLP interprets real-time data for remote monitoring. The benefits include improved patient outcomes, reduced costs, and enhanced medical decision-making. However, challenges like data privacy, algorithmic bias, and the need for transparency underscore the importance of ethical and responsible AI implementation in healthcare.

"North America is expected to have the largest market share during the forecast period."

The healthcare sector in North America is witnessing an influx of new entrants into the Artificial Intelligence (AI) landscape, driven by cross-industry involvement and a substantial rise in venture capital investments. An example is Navina (US), a startup dedicated to an AI-driven primary care platform, securing a substantial USD 44 million in its series B funding round in October 2022. These investments propel Navina's AI and Machine Learning (ML) technology advancements. Another illustration is Tempus (US), specializing in AI-based precision medicine solutions, securing a notable USD 1.3 billion from 11 investors, including Ares Management and Google, in the same month.

Extensive primary interviews were conducted with key industry experts in the AI in Healthcare market space to determine and verify the market size for various segments and subsegments gathered through secondary research. The break-up of primary participants for the report has been shown below:

The break-up of the profile of primary participants in the AI in Healthcare market:

- By Company Type: Tier 1 - 50%, Tier 2 - 30%, and Tier 3 - 20%

- By Designation: C Level - 60%, Director Level - 30%, Others-10%

- By Region: North America - 40%, Europe - 20%, Asia Pacific - 30%, ROW- 10%

The report profiles key players in the AI in Healthcare market with their respective market ranking analysis. Prominent players profiled in this report are Koninklijke Philips N.V. (Netherlands), Microsoft (US), Siemens Healthineers AG (Germany), Intel Corporation (US), NVIDIA Corporation (US), Google Inc. (US), GE HealthCare Technologies Inc. (US), Oracle (US), and Johnson & Johnson Services, Inc. (US) among others.

Apart from this, Merative (US), General Vision, Inc., (US), CloudMedx (US), Oncora Medical (US), Enlitic (US), Lunit Inc., (South Korea), Qure.ai (India), Tempus (US), COTA (US), FDNA INC. (US), Recursion (US), Atomwise (US), Virgin Pulse (US), Babylon Health (UK), MDLIVE (US), Stryker (US), Qventus (US), Sweetch (Israel), Sirona Medical, Inc. (US), Ginger (US), Biobeat (Israel) are among a few emerging companies in the AI in Healthcare market.

Research Coverage: This research report categorizes the AI in Healthcare market based on offering, technology, application, end user, and region. The report describes the major drivers, restraints, challenges, and opportunities pertaining to the AI in Healthcare market and forecasts the same till 2029. Apart from these, the report also consists of leadership mapping and analysis of all the companies included in the AI in Healthcare ecosystem.

Key Benefits of Buying the Report The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall AI in Healthcare market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Generation of large and complex healthcare datasets, Pressing need to reduce healthcare costs, Improving computing power and declining hardware cost, Rising number of partnerships and collaborations among different domains in healthcare sector, and Growing need for improvised healthcare services due to imbalance between healthcare workforce and patients) influencing the growth of the AI in Healthcare market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the AI in Healthcare market.

- Market Development: Comprehensive information about lucrative markets - the report analysis the AI in Healthcare market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the AI in Healthcare market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like Koninklijke Philips N.V. (Netherlands), Microsoft (US), Siemens Healthineers AG (Germany), Intel Corporation (US), NVIDIA Corporation (US) among others in the AI in Healthcare market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 REGIONAL SCOPE

- 1.3.3 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNITS CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.9 IMPACT OF RECESSION

- FIGURE 1 GDP GROWTH PROJECTION DATA FOR MAJOR ECONOMIES, 2021-2023

- 1.10 GDP GROWTH PROJECTION UNTIL 2024 FOR MAJOR ECONOMIES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of major secondary sources

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 List of key interview participants

- 2.1.2.2 Key data from primary sources

- 2.1.2.3 Key industry insights

- 2.1.2.4 Breakdown of primaries

- 2.1.3 SECONDARY AND PRIMARY RESEARCH

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 3 RESEARCH FLOW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET SIZE ESTIMATION

- FIGURE 4 MARKET SIZE ESTIMATION METHODOLOGY (SUPPLY SIDE): REVENUE GENERATED BY COMPANIES FROM ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET

- 2.2.1 BOTTOM-UP APPROACH

- 2.2.1.1 Approach to estimate market size using bottom-up analysis (demand side)

- FIGURE 5 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH

- FIGURE 6 MARKET SIZE ESTIMATION METHODOLOGY: BOTTOM-UP APPROACH (DEMAND SIDE): REVENUE GENERATED FROM ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER

- 2.2.2 TOP-DOWN APPROACH

- 2.2.2.1 Approach to estimate market size using top-down analysis (supply side)

- FIGURE 7 MARKET SIZE ESTIMATION METHODOLOGY: TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- FIGURE 8 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RISK ASSESSMENT

- 2.6 PARAMETERS CONSIDERED TO ANALYZE RECESSION IMPACT ON STUDIED MARKET

- 2.7 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

- FIGURE 9 SOFTWARE SEGMENT TO HOLD LARGEST MARKET SHARE IN 2029

- FIGURE 10 MACHINE LEARNING SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- FIGURE 11 PATIENTS SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 MEDICAL IMAGING & DIAGNOSTICS SEGMENT TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 13 NORTH AMERICA ACCOUNTED FOR LARGEST MARKET SHARE OF GLOBAL ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET IN 2023

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN AI IN HEALTHCARE MARKET

- FIGURE 14 INCREASING ADOPTION OF AI-BASED TOOLS IN HEALTHCARE FACILITIES TO CREATE LUCRATIVE OPPORTUNITIES FOR MARKET PLAYERS

- 4.2 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING

- FIGURE 15 SOFTWARE SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2024

- 4.3 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TECHNOLOGY

- FIGURE 16 MACHINE LEARNING TECHNOLOGY TO COMMAND MARKET FROM 2023 TO 2029

- 4.4 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER

- FIGURE 17 HOSPITALS & HEALTHCARE PROVIDERS SEGMENT TO LEAD MARKET THROUGHOUT FORECAST PERIOD

- 4.5 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION

- FIGURE 18 MEDICAL IMAGING & DIAGNOSTICS SEGMENT TO REGISTER HIGHEST GROWTH DURING FORECAST PERIOD

- 4.6 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY COUNTRY

- FIGURE 19 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET IN MEXICO TO GROW AT HIGHEST CAGR FROM 2024 TO 2029

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 20 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- FIGURE 21 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: DRIVERS AND THEIR IMPACT

- 5.2.1.1 Exponential growth in data volume and complexity due to surging adoption of digital technologies

- 5.2.1.2 Significant cost pressure on healthcare service providers with increasing prevalence of chronic diseases

- 5.2.1.3 Rapid proliferation of AI in healthcare sector

- 5.2.1.4 Growing need for improvised healthcare services

- 5.2.2 RESTRAINTS

- FIGURE 22 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: RESTRAINTS AND THEIR IMPACT

- 5.2.2.1 Reluctance among medical practitioners to adopt AI-based technologies

- 5.2.2.2 Shortage of skilled AI professionals handling AI-powered solutions

- 5.2.2.3 Lack of standardized frameworks for AL and ML technologies

- 5.2.3 OPPORTUNITIES

- FIGURE 23 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: OPPORTUNITIES AND THEIR IMPACT

- 5.2.3.1 Increasing use of AI-powered solutions in elderly care

- 5.2.3.2 Increasing focus on developing human-aware AI systems

- 5.2.3.3 Rising use of technology in pharmaceuticals industry

- 5.2.3.4 Strategic partnerships and collaborations among healthcare companies and AI technology providers

- 5.2.4 CHALLENGES

- FIGURE 24 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: CHALLENGES AND THEIR IMPACT

- 5.2.4.1 Inaccurate predictions due to scarcity of high-quality healthcare data

- 5.2.4.2 Concerns regarding data privacy

- FIGURE 25 DATA BREACHES IN HEALTHCARE SECTOR, 2019-2023

- 5.2.4.3 Lack of interoperability between AI solutions offered by different vendors

- FIGURE 26 CHALLENGES ASSOCIATED WITH HEALTHCARE DATA INTEROPERABILITY

- 5.3 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- FIGURE 27 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESSES

- 5.4 PRICING ANALYSIS

- 5.4.1 AVERAGE SELLING PRICE (ASP) TREND OF COMPONENTS OFFERED BY KEY PLAYERS, 2020-2029

- FIGURE 28 AVERAGE SELLING PRICE (ASP) OF PROCESSOR COMPONENTS OFFERED BY KEY PLAYERS

- TABLE 1 AVERAGE SELLING PRICE (ASP) OF PROCESSOR COMPONENTS OFFERED BY KEY PLAYERS

- 5.4.2 AVERAGE SELLING PRICE (ASP) TREND OF PROCESSOR COMPONENTS, BY REGION, 2020-2029

- FIGURE 29 AVERAGE SELLING PRICE (ASP) TREND OF PROCESSOR COMPONENTS, BY REGION, 2020-2029

- 5.5 VALUE CHAIN ANALYSIS

- FIGURE 30 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: VALUE CHAIN ANALYSIS

- 5.6 ECOSYSTEM MAPPING

- FIGURE 31 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: ECOSYSTEM MAPPING

- TABLE 2 COMPANIES AND THEIR ROLES IN ARTIFICIAL INTELLIGENCE IN HEALTHCARE ECOSYSTEM

- 5.7 TECHNOLOGY ANALYSIS

- 5.7.1 CLOUD COMPUTING

- 5.7.2 CLOUD GPU

- 5.7.3 GENERATIVE AI

- 5.7.4 CLOUD-BASED PACS

- 5.7.5 MULTI-CLOUD

- 5.8 PATENT ANALYSIS

- TABLE 3 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: INNOVATIONS AND PATENT REGISTRATIONS

- FIGURE 32 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: PATENTS GRANTED, 2013-2023

- FIGURE 33 TOP 10 PATENT OWNERS IN LAST 10 YEARS, 2013-2023

- TABLE 4 TOP PATENT OWNERS IN ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET IN LAST 10 YEARS

- 5.9 TRADE ANALYSIS

- FIGURE 34 IMPORT DATA FOR HS CODE 854231-COMPLIANT PRODUCTS, BY COUNTRY, 2018-2022 (USD MILLION)

- FIGURE 35 EXPORT DATA FOR HS CODE 854231-COMPLIANT PRODUCTS, BY COUNTRY, 2018-2022 (USD MILLION)

- 5.10 KEY CONFERENCES AND EVENTS, 2024-2025

- TABLE 5 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: LIST OF CONFERENCES AND EVENTS, 2024-2025

- 5.11 CASE STUDY ANALYSIS

- 5.11.1 BIOBEAT LAUNCHED HOME-BASED REMOTE PATIENT MONITORING KIT DURING PEAK WAVE OF COVID-19

- 5.11.2 MICROSOFT COLLABORATED WITH CLEVELAND CLINIC TO APPLY PREDICTIVE AND ADVANCED ANALYTICS TO IDENTIFY POTENTIAL AT-RISK PATIENTS UNDER ICU CARE

- 5.11.3 TGEN COLLABORATED WITH INTEL CORPORATION AND DELL TECHNOLOGIES TO ASSIST PHYSICIANS AND RESEARCHERS ACCELERATE DIAGNOSIS AND TREATMENT AT LOWER COST

- 5.11.4 INSILICO DEVELOPED ML-POWERED TOOLS FOR DRUG IDENTIFICATION AND CHEMISTRY42 FOR NOVEL COMPOUND DESIGN

- 5.11.5 GE HEALTHCARE IMPROVED PATIENT OUTCOMES BY REDUCING WORKFLOW PROCESSING TIME USING MEDICAL IMAGING DATA

- 5.12 TARIFFS, STANDARDS, AND REGULATORY LANDSCAPE

- TABLE 6 MFN TARIFF FOR HS CODE 854231-COMPLIANT PRODUCTS EXPORTED BY US, 2022

- TABLE 7 MFN TARIFF FOR HS CODE 854231-COMPLIANT PRODUCTS EXPORTED BY CHINA, 2022

- TABLE 8 MFN TARIFF FOR HS CODE 854231-COMPLIANT PRODUCTS EXPORTED BY GERMANY, 2022

- 5.12.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 9 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 11 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 12 ROW: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.12.2 STANDARDS

- 5.12.2.1 ISO 22399:2020

- 5.12.2.2 IEC 62366:2015

- 5.12.2.3 Health Insurance Portability and Accountability Act (HIPAA)

- 5.12.2.4 EU General Data Protection Regulation (GDPR)

- 5.12.2.5 Fast Healthcare Interoperability Resources (HL7 FHIR)

- 5.12.2.6 Medical Device Regulation

- 5.12.2.7 World Health Organization Artificial intelligence for Health Guide

- 5.12.2.8 Algorithmic Justice League framework for assessing AI in healthcare

- 5.12.3 GOVERNMENT REGULATIONS

- 5.12.3.1 US

- 5.12.3.2 Europe

- 5.12.3.3 China

- 5.12.3.4 Japan

- 5.12.3.5 India

- 5.13 PORTER'S FIVE FORCES ANALYSIS

- TABLE 13 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: PORTER'S FIVE FORCES ANALYSIS

- FIGURE 36 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.13.1 THREAT OF NEW ENTRANTS

- 5.13.2 THREAT OF SUBSTITUTES

- 5.13.3 BARGAINING POWER OF SUPPLIERS

- 5.13.4 BARGAINING POWER OF BUYERS

- 5.13.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.14 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.14.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 37 INFLUENCE OF KEY STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- TABLE 14 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE END USERS

- 5.14.2 BUYING CRITERIA

- FIGURE 38 KEY BUYING CRITERIA FOR TOP THREE END USERS

- TABLE 15 KEY BUYING CRITERIA FOR TOP THREE END USERS

6 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING

- 6.1 INTRODUCTION

- FIGURE 39 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING

- FIGURE 40 SOFTWARE SEGMENT TO DOMINATE MARKET DURING FORECAST PERIOD

- TABLE 16 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 17 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- 6.2 HARDWARE

- TABLE 18 HARDWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 19 HARDWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 20 HARDWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 21 HARDWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.2.1 PROCESSOR

- 6.2.1.1 Need for real-time processing of patient data to boost demand

- TABLE 22 PROCESSOR: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (MILLION UNITS)

- TABLE 23 PROCESSOR: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (MILLION UNITS)

- TABLE 24 PROCESSOR: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 25 PROCESSOR: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 6.2.1.2 MPUs/CPUs

- TABLE 26 CASE STUDY: PHILIPS COLLABORATED WITH INTEL CORPORATION TO OPTIMIZE AI INFERENCING HEALTHCARE WORKLOADS ON INTEL XEON SCALABLE PROCESSORS USING OPENVINO TOOLKIT

- 6.2.1.3 GPUs

- TABLE 27 CASE STUDY: DEEPPHARMA PLATFORM, OFFERED BY INSILICO, EQUIPPED WITH ADVANCED DEEP LEARNING TECHNIQUES, HELPS ANALYZE MULTI-OMICS DATA AND TISSUE-SPECIFIC PATHWAY ACTIVATION PROFILES

- 6.2.1.4 FPGAs

- TABLE 28 CASE STUDY: INTEL CORPORATION, IN COLLABORATION WITH BROAD INSTITUTE, DEVELOPED BIGSTACK** 2.0 TO MEET EVOLVING DEMANDS OF GENOMICS RESEARCH

- 6.2.1.5 ASICs

- 6.2.2 MEMORY

- 6.2.2.1 Increasing demand for real-time medical image analysis and diagnosis support systems to drive market

- TABLE 29 CASE STUDY: HUAWEI ASSISTED TOULOUSE UNIVERSITY HOSPITAL WITH OCEANSTOR ALL-FLASH SOLUTION THAT OFFERS LOW LATENCY AND SIMPLIFIED OPERATIONS AND MAINTENANCE MANAGEMENT

- 6.2.3 NETWORK

- 6.2.3.1 Growing need for remote patient monitoring and precision medicine to foster segmental growth

- TABLE 30 NETWORK: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 31 NETWORK: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 6.3 SOFTWARE

- TABLE 32 SOFTWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 33 SOFTWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 34 SOFTWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 35 SOFTWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.3.1 AI SOLUTION

- 6.3.1.1 Integration of non-procedural languages into AI solutions to accelerate segmental growth

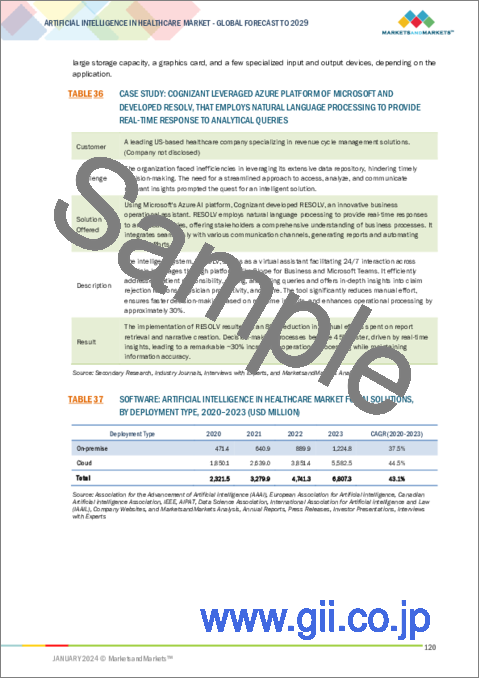

- TABLE 36 CASE STUDY: COGNIZANT LEVERAGED AZURE PLATFORM OF MICROSOFT AND DEVELOPED RESOLV, THAT EMPLOYS NATURAL LANGUAGE PROCESSING TO PROVIDE REAL-TIME RESPONSE TO ANALYTICAL QUERIES

- TABLE 37 SOFTWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET FOR AI SOLUTIONS, BY DEPLOYMENT TYPE, 2020-2023 (USD MILLION)

- TABLE 38 SOFTWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET FOR AI SOLUTIONS, BY DEPLOYMENT TYPE, 2024-2029 (USD MILLION)

- 6.3.1.2 On-premises

- TABLE 39 CASE STUDY: GE HEALTHCARE ENHANCED ON-PREMISES CAPABILITY WITH SCYLLADB'S PROJECT ALTERNATOR

- 6.3.1.3 Cloud

- TABLE 40 CASE STUDY: TAKEDA COLLABORATED WITH DELOITTE TO EMPLOY DEEP MINER TOOLKIT FOR RAPID DEVELOPMENT AND TESTING OF PREDICTIVE MODELS

- 6.3.2 AI PLATFORM

- 6.3.2.1 Increasing applications in development of toolkits for healthcare solutions to drive market

- TABLE 41 CASE STUDY: CAYUGA MEDICAL CENTER SOUGHT SIMPLE CDI SOFTWARE SOLUTION TO IMPROVE WORKFLOWS AND REDUCE COSTS

- TABLE 42 SOFTWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET FOR AI PLATFORMS, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 43 SOFTWARE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET FOR AI PLATFORMS, BY TYPE, 2024-2029 (USD MILLION)

- 6.3.2.2 Machine learning framework

- 6.3.2.3 Application program interface

- 6.4 SERVICES

- TABLE 44 SERVICES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 45 SERVICES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (USD MILLION)

- TABLE 46 SERVICES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 47 SERVICES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- 6.4.1 DEPLOYMENT & INTEGRATION

- 6.4.1.1 Enhanced patient care along with streamlines workflows to drive demand

- 6.4.2 SUPPORT & MAINTENANCE

- 6.4.2.1 Need to evaluate performance and maintain operational stability to drive market

7 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- FIGURE 41 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TECHNOLOGY

- FIGURE 42 MACHINE LEARNING TECHNOLOGY TO LEAD MARKET DURING FORECAST PERIOD

- TABLE 48 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TECHNOLOGY, 2020-2023 (USD MILLION)

- TABLE 49 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TECHNOLOGY, 2024-2029 (USD MILLION)

- 7.2 MACHINE LEARNING

- TABLE 50 CASE STUDY: IN COLLABORATION WITH INTEL AND APOQLAR, THEBLUE.AI INTRODUCED BLUW.GDPR. EQUIPPED WITH ML ALGORITHMS ACCELERATED BY OPENVINO TOOLKIT

- TABLE 51 MACHINE LEARNING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 52 MACHINE LEARNING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 7.2.1 DEEP LEARNING

- 7.2.1.1 Rising applications in voice recognition, fraud detection, and recommendation engines to drive market

- TABLE 53 WINNING HEALTH TECHNOLOGY INTRODUCED AI MEDICAL IMAGING SOLUTION BASED ON AMAX DEEP LEARNING ALL-IN-ONE TO REDUCE OVERALL MODEL INFERENCE TIME FROM OVER 0.5 HOURS TO LESS THAN 2 MINUTES FOR AI-AIDED DIAGNOSTIC IMAGING OF PULMONARY NODULES

- 7.2.2 SUPERVISED LEARNING

- 7.2.2.1 Contribution to clinical decision-making and enhancing personalized medications to boost demand

- 7.2.3 REINFORCEMENT LEARNING

- 7.2.3.1 Enhanced diagnostic accuracy in medical imaging analysis to fuel market growth

- 7.2.4 UNSUPERVISED LEARNING

- 7.2.4.1 Ability to uncover hidden patterns and handle unlabeled data challenges to boost demand

- 7.2.5 OTHERS

- 7.3 NATURAL LANGUAGE PROCESSING

- TABLE 54 CASE STUDY: MARUTI TECHLABS ASSISTED UKHEALTH WITH ML MODEL FOR AUTOMATIC DATA EXTRACTION AND CLASSIFICATION

- TABLE 55 NATURAL LANGUAGE PROCESSING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 56 NATURAL LANGUAGE PROCESSING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 7.3.1 IVR

- 7.3.1.1 Enhanced operational efficiency and optimized clinical support to drive market

- 7.3.2 OCR

- 7.3.2.1 Reduced errors in data entry and streamlined administrative processes to spur demand

- 7.3.3 PATTERN AND IMAGE RECOGNITION

- 7.3.3.1 Optimized therapeutic outcomes and development of personal medication to foster segmental growth

- 7.3.4 AUTO CODING

- 7.3.4.1 Contribution to cost-saving and optimization of coding processes to drive market

- 7.3.5 CLASSIFICATION AND CATEGORIZATION

- 7.3.5.1 Accurate prediction of disease outcomes to boost demand

- 7.3.6 TEXT ANALYTICS

- 7.3.6.1 Significant contribution to drug discovery by examining extensive datasets of scientific literature to boost demand

- 7.3.7 SPEECH ANALYTICS

- 7.3.7.1 Contribution to sentiment analysis by assessing tone of patient conversations to boost demand

- 7.4 CONTEXT-AWARE COMPUTING

- TABLE 57 CONTEXT-AWARE COMPUTING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2020-2023 (USD MILLION)

- TABLE 58 CONTEXT-AWARE COMPUTING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY TYPE, 2024-2029 (USD MILLION)

- 7.4.1 DEVICE CONTEXT

- 7.4.1.1 Ability to offer comprehensive view of patient data to boost demand

- 7.4.2 USER CONTEXT

- 7.4.2.1 Better predictive analysis for disease prevention to foster segmental growth

- 7.4.3 PHYSICAL CONTEXT

- 7.4.3.1 Ability to address individualized needs based on surrounding environment to boost market

- 7.5 COMPUTER VISION

- 7.5.1 ENHANCED PRECISION WITH 3D VISUALIZATIONS AND PERSONALIZED PROCEDURES TO FOSTER SEGMENTAL GROWTH

- TABLE 59 CASE STUDY: PUNKTUM COLLABORATED WITH MAYO CLINIC TO DEVELOP CUTTING-EDGE DEEP LEARNING-BASED MODEL FOCUSED ON COMPUTER VISION FOR ACCURATE CLASSIFICATION OF ISCHEMIC STROKE ORIGINS

8 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION

- 8.1 INTRODUCTION

- FIGURE 43 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION

- FIGURE 44 MEDICAL IMAGING & DIAGNOSTICS SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE IN 2029

- TABLE 60 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 61 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- 8.2 PATIENT DATA & RISK ANALYSIS

- 8.2.1 CONVERGENCE OF ML AND NLP TO OFFER LUCRATIVE GROWTH OPPORTUNITIES FOR PLAYERS

- TABLE 62 CASE STUDY: MAYO CLINIC PARTNERED WITH GOOGLE TO IMPLEMENT AI MODELS AND ENHANCE PATIENT CARE

- TABLE 63 PATIENT DATA & RISK ANALYSIS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 64 PATIENT DATA & RISK ANALYSIS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 65 PATIENT DATA & RISK ANALYSIS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 66 PATIENT DATA & RISK ANALYSIS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.3 IN-PATIENT CARE & HOSPITAL MANAGEMENT

- 8.3.1 EASE OF PATIENT SCHEDULING WITH CHATBOTS AND VIRTUAL ASSISTANTS TO DRIVE MARKET

- TABLE 67 CASE STUDY: PROMINENT MULTISPECIALTY HOSPITAL EMPLOYED ADOBE XD TO PREVENT RESOURCE WASTAGE AND ENHANCE EFFICIENCY

- TABLE 68 IN-PATIENT CARE & HOSPITAL MANAGEMENT: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 69 IN-PATIENT CARE & HOSPITAL MANAGEMENT: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 70 IN-PATIENT CARE & HOSPITAL MANAGEMENT: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 71 IN-PATIENT CARE & HOSPITAL MANAGEMENT: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.4 MEDICAL IMAGING & DIAGNOSTICS

- 8.4.1 ACCESSIBILITY IN MEDICAL IMAGING AND WORKFLOW OPTIMIZATION TO FOSTER SEGMENTAL GROWTH

- TABLE 72 CASE STUDY: PHILIPS TRANSFORMED HEALTHCARE WITH AWS-POWERED AI SOLUTIONS

- TABLE 73 MEDICAL IMAGING & DIAGNOSTICS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 74 MEDICAL IMAGING & DIAGNOSTICS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 75 MEDICAL IMAGING & DIAGNOSTICS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 76 MEDICAL IMAGING & DIAGNOSTICS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.5 LIFESTYLE MANAGEMENT & REMOTE PATIENT MONITORING

- 8.5.1 ENHANCED PATIENT COMPLIANCE THROUGH BEHAVIORAL ANALYSIS TO BOOST DEMAND

- TABLE 77 LIFESTYLE MANAGEMENT & REMOTE PATIENT MONITORING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 78 LIFESTYLE MANAGEMENT & REMOTE PATIENT MONITORING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 79 LIFESTYLE MANAGEMENT & REMOTE PATIENT MONITORING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 80 LIFESTYLE MANAGEMENT & REMOTE PATIENT MONITORING: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.6 VIRTUAL ASSISTANTS

- 8.6.1 ABILITY TO OFFER SIMPLIFIED COMPLEX MEDICAL INFORMATION TO DRIVE MARKET

- TABLE 81 CASE STUDY: OSF COLLABORATED WITH GYANT TO IMPLEMENT CLARE, AI VIRTUAL CARE NAVIGATION ASSISTANT, BOOSTING DIGITAL HEALTH TRANSFORMATION

- TABLE 82 VIRTUAL ASSISTANT: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 83 VIRTUAL ASSISTANT: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 84 VIRTUAL ASSISTANT: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 85 VIRTUAL ASSISTANT: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.7 DRUG DISCOVERY

- 8.7.1 ACCELERATED IDENTIFICATION OF POTENTIAL DRUG CANDIDATES TO BOOST DEMAND

- TABLE 86 CASE STUDY: AZOTHBIO UTILIZED RESCALE'S PLATFORM TO ENHANCE R&D AGILITY

- TABLE 87 DRUG DISCOVERY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 88 DRUG DISCOVERY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 89 DRUG DISCOVERY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 90 DRUG DISCOVERY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.8 RESEARCH

- 8.8.1 GROWING IMPORTANCE IN ANALYSIS OF SEQUENCE AND FUNCTIONAL PATTERNS FROM SEQUENCE DATABASES TO ACCELERATE DEMAND

- TABLE 91 RESEARCH: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 92 RESEARCH: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 93 RESEARCH: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 94 RESEARCH: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.9 HEALTHCARE ASSISTANCE ROBOTS

- 8.9.1 USE TO REVOLUTIONIZE PATIENT CARE BY STREAMLINING TASKS AND ENABLING REAL-TIME DATA ANALYSIS AND ENHANCE HEALTHCARE EXPERIENCES TO DRIVE MARKET

- TABLE 95 HEALTHCARE ASSISTANCE ROBOTS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 96 HEALTHCARE ASSISTANCE ROBOTS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 97 HEALTHCARE ASSISTANCE ROBOTS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 98 HEALTHCARE ASSISTANCE ROBOTS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.10 PRECISION MEDICINES

- 8.10.1 PERSONALIZED HEALTHCARE BY STREAMLINING CLINICAL TRIALS TO ACCELERATE DEMAND

- TABLE 99 PRECISION MEDICINE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 100 PRECISION MEDICINE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 101 PRECISION MEDICINE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 102 PRECISION MEDICINE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.11 EMERGENCY ROOMS & SURGERIES

- 8.11.1 QUICK IDENTIFICATION OF LIFE-THREATENING PATHOLOGIES TO FOSTER SEGMENTAL GROWTH

- TABLE 103 EMERGENCY ROOMS & SURGERIES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 104 EMERGENCY ROOMS & SURGERIES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 105 EMERGENCY ROOMS & SURGERIES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 106 EMERGENCY ROOMS & SURGERIES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.12 WEARABLES

- 8.12.1 PERSONALIZED TREATMENT STRATEGIES AND REAL-TIME INSIGHTS TO BOOST DEMAND

- TABLE 107 CASE STUDY: KENSCI COLLABORATED WITH MICROSOFT TO ASSIST US NATIONAL GOVERNMENT IN IDENTIFYING PATIENTS WITH COPD

- TABLE 108 WEARABLES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 109 WEARABLES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 110 WEARABLES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 111 WEARABLES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.13 MENTAL HEALTH

- 8.13.1 PRESSING NEED TO DETECT DEPRESSION AND IDENTIFY SUICIDE RISKS THROUGH TEXT ANALYSIS TO DRIVE MARKET

- TABLE 112 MENTAL HEALTH: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 113 MENTAL HEALTH: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 114 MENTAL HEALTH: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 115 MENTAL HEALTH: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 8.14 CYBERSECURITY

- 8.14.1 PREVENTION OF INFILTRATION ATTEMPTS AND ENHANCED SPEED OF THREAT DETECTION TO BOOST DEMAND

- TABLE 116 CASE STUDY: SNORKEL FLOW CREATED HIGH-ACCURACY ML MODELS TO OVERCOME HAND-LABELING CHALLENGES

- TABLE 117 CYBERSECURITY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 118 CYBERSECURITY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 119 CYBERSECURITY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 120 CYBERSECURITY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

9 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER

- 9.1 INTRODUCTION

- FIGURE 45 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER

- FIGURE 46 HOSPITALS & HEALTHCARE PROVIDERS TO HOLD LARGEST MARKET SHARE IN 2029

- TABLE 121 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 122 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 9.2 HOSPITALS & HEALTHCARE PROVIDERS

- 9.2.1 INCREASING USE IN MINING MEDICAL DATA AND STUDYING GENOMICS-BASED DATA FOR PERSONALIZED MEDICINE TO BOOST MARKET GROWTH

- TABLE 123 CASE STUDY: UNIVERSITY COLLEGE LONDON, KING'S COLLEGE LONDON, AND NATIONAL HEALTH SERVICE COLLABORATION RESULTED IN DEVELOPMENT OF COGSTACK, THAT REVOLUTIONIZED HEALTHCARE DATA UTILIZATION

- TABLE 124 HOSPITALS & HEALTHCARE PROVIDERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 125 HOSPITALS & HEALTHCARE PROVIDERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 126 HOSPITALS & HEALTHCARE PROVIDERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 127 HOSPITALS & HEALTHCARE PROVIDERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- 9.3 PATIENTS

- 9.3.1 RISE IN USE OF AI IN MENTAL HEALTH SUPPORT APPLICATIONS THROUGH CHATBOTS AND VIRTUAL THERAPISTS TO BOOST MARKET GROWTH

- TABLE 128 CASE STUDY: COGNIZANT PARTNERED WITH ONE OF CLIENTS TO ENHANCE CALLER SELF-SERVICE AND IMPROVE MEMBER EXPERIENCE METRICS

- TABLE 129 PATIENTS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 130 PATIENTS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 131 PATIENTS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 132 PATIENTS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- 9.4 PHARMACEUTICALS & BIOTECHNOLOGY COMPANIES

- 9.4.1 GROWING PARTNERSHIPS AMONG PLAYERS TO OFFER LUCRATIVE GROWTH OPPORTUNITIES TO PLAYERS

- TABLE 133 CASE STUDY: AZURE MACHINE LEARNING-BASED INTELLIGENT SYSTEM ASSISTED LEADING PHARMA COMPANY TO AUTO-CLASSIFY PRODUCTS INTO MARKET-RELATED CATEGORIES THAT BOOSTED OPERATIONAL EFFICIENCY

- TABLE 134 PHARMACEUTICALS & BIOTECHNOLOGY COMPANIES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 135 PHARMACEUTICALS & BIOTECHNOLOGY COMPANIES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 136 PHARMACEUTICALS & BIOTECHNOLOGY COMPANIES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 137 PHARMACEUTICALS & BIOTECHNOLOGY COMPANIES: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- 9.5 HEALTHCARE PAYERS

- 9.5.1 FAST AND ACCURATE CLAIM PROCESSING AND ENHANCED FRAUD DETECTION BENEFITS TO BOOST DEMAND

- TABLE 138 HEALTHCARE PAYERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 139 HEALTHCARE PAYERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 140 HEALTHCARE PAYERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 141 HEALTHCARE PAYERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- 9.6 OTHERS

- TABLE 142 OTHERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 143 OTHERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 144 OTHERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 145 OTHERS: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

10 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION

- 10.1 INTRODUCTION

- FIGURE 47 ASIA PACIFIC TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- TABLE 146 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 147 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- 10.2 NORTH AMERICA

- 10.2.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 48 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET SNAPSHOT

- FIGURE 49 US TO DOMINATE NORTH AMERICAN ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET IN 2029

- TABLE 148 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 149 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 150 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 151 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 152 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 153 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 154 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 155 NORTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.2.2 US

- 10.2.2.1 High healthcare spending in US to drive market

- TABLE 156 US: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 157 US: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.2.3 CANADA

- 10.2.3.1 Government-led initiatives to support deployment of AI in healthcare sector to boost demand

- TABLE 158 CANADA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 159 CANADA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.2.4 MEXICO

- 10.2.4.1 Increasing private sector investments in AI healthcare technologies to drive market

- TABLE 160 MEXICO: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 161 MEXICO: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3 EUROPE

- 10.3.1 EUROPE: RECESSION IMPACT

- FIGURE 50 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET SNAPSHOT

- FIGURE 51 REST OF EUROPE TO EXHIBIT HIGHEST CAGR IN EUROPEAN ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET DURING FORECAST PERIOD

- TABLE 162 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 163 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 164 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 165 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 166 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 167 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 168 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 169 EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.2 GERMANY

- 10.3.2.1 Rising healthcare data generation to drive market

- TABLE 170 GERMANY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 171 GERMANY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.3 UK

- 10.3.3.1 Targeted treatment with increased success rates to fuel market growth

- TABLE 172 UK: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 173 UK: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.4 FRANCE

- 10.3.4.1 Focus on telemedicine and chronic disease management to drive market

- TABLE 174 FRANCE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 175 FRANCE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.5 ITALY

- 10.3.5.1 Rising geriatric population to drive market

- TABLE 176 ITALY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 177 ITALY: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.6 SPAIN

- 10.3.6.1 Growing partnerships between technology firms and healthcare providers to boost demand

- TABLE 178 SPAIN: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 179 SPAIN: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.3.7 REST OF EUROPE

- TABLE 180 REST OF EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 181 REST OF EUROPE: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4 ASIA PACIFIC

- 10.4.1 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 52 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET SNAPSHOT

- FIGURE 53 CHINA TO EXHIBIT HIGHEST CAGR IN ASIA PACIFIC ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET DURING FORECAST PERIOD

- TABLE 182 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 183 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY COUNTRY, 2024-2029 (USD MILLION)

- TABLE 184 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 185 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 186 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 187 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 188 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 189 ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.2 CHINA

- 10.4.2.1 Government-led measures to expedite integration of AI into healthcare sector to drive market

- TABLE 190 CHINA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 191 CHINA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.3 JAPAN

- 10.4.3.1 Increasing number of AI-driven start-ups manufacturing diagnostic and therapeutic tools to fuel market growth

- TABLE 192 JAPAN: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 193 JAPAN: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.4 SOUTH KOREA

- 10.4.4.1 Increasing incidence of cancer to drive market

- TABLE 194 SOUTH KOREA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 195 SOUTH KOREA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.5 INDIA

- 10.4.5.1 Developing IT infrastructure and AI-friendly government initiatives to spur market growth

- TABLE 196 INDIA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 197 INDIA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.4.6 REST OF ASIA PACIFIC

- TABLE 198 REST OF ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 199 REST OF ASIA PACIFIC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5 ROW

- 10.5.1 ROW: RECESSION IMPACT

- FIGURE 54 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET SNAPSHOT

- FIGURE 55 SOUTH AMERICA TO DOMINATE ROW MARKET IN 2029

- TABLE 200 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 201 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY REGION, 2024-2029 (USD MILLION)

- TABLE 202 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2020-2023 (USD MILLION)

- TABLE 203 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY OFFERING, 2024-2029 (USD MILLION)

- TABLE 204 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2020-2023 (USD MILLION)

- TABLE 205 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY APPLICATION, 2024-2029 (USD MILLION)

- TABLE 206 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 207 ROW: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5.2 SOUTH AMERICA

- 10.5.2.1 High investments in healthcare IT to drive market

- TABLE 208 SOUTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 209 SOUTH AMERICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5.3 GCC

- 10.5.3.1 Rising focus on technological advancements in healthcare sector to drive market

- TABLE 210 GCC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 211 GCC: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

- 10.5.4 REST OF MIDDLE EAST & AFRICA

- 10.5.4.1 Growing investments in information and communication technologies to boost demand

- TABLE 212 REST OF MIDDLE EAST & AFRICA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 213 REST OF MEA: ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET, BY END USER, 2024-2029 (USD MILLION)

11 COMPETITIVE LANDSCAPE

- 11.1 OVERVIEW

- 11.2 STRATEGIES ADOPTED BY MAJOR PLAYERS, 2020-2023

- TABLE 214 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: OVERVIEW OF STRATEGIES DEPLOYED BY KEY PLAYERS, 2020-2023

- 11.3 REVENUE ANALYSIS, 2019-2023

- FIGURE 56 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: REVENUE ANALYSIS OF TOP FIVE PLAYERS, 2019-2023

- 11.4 MARKET SHARE ANALYSIS, 2023

- FIGURE 57 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET SHARE ANALYSIS, 2023

- TABLE 215 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET SHARE ANALYSIS, 2023

- 11.5 COMPANY EVALUATION MATRIX, 2023

- 11.5.1 STARS

- 11.5.2 EMERGING LEADERS

- 11.5.3 PERVASIVE PLAYERS

- 11.5.4 PARTICIPANTS

- FIGURE 58 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: COMPANY EVALUATION MATRIX, 2023

- 11.5.5 COMPANY FOOTPRINT

- TABLE 216 OVERALL COMPANY FOOTPRINT

- TABLE 217 COMPANY OFFERING FOOTPRINT

- TABLE 218 COMPANY END USER FOOTPRINT

- TABLE 219 COMPANY REGION FOOTPRINT

- 11.6 START-UP/SMALL AND MEDIUM-SIZED ENTERPRISE (SME) EVALUATION MATRIX, 2023

- 11.6.1 PROGRESSIVE COMPANIES

- 11.6.2 RESPONSIVE COMPANIES

- 11.6.3 DYNAMIC COMPANIES

- 11.6.4 STARTING BLOCKS

- FIGURE 59 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: START-UP/SME EVALUATION MATRIX, 2023

- TABLE 220 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: LIST OF KEY START-UPS/SMES

- 11.6.5 COMPETITIVE BENCHMARKING

- TABLE 221 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: COMPETITIVE BENCHMARKING OF KEY START-UPS/SMES

- 11.7 COMPETITIVE SCENARIOS AND TRENDS

- 11.7.1 PRODUCT LAUNCHES

- TABLE 222 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: PRODUCT LAUNCHES, 2020 - 2023

- 11.7.2 DEALS

- TABLE 223 ARTIFICIAL INTELLIGENCE IN HEALTHCARE MARKET: DEALS, 2020 - 2023

12 COMPANY PROFILES

- 12.1 KEY PLAYERS

- (Business overview, Products /Solutions/Services offered, Recent developments, Product launches, MnM view, Key strengths/Right to win, Strategic choices made, and Weaknesses and Competitive threats)**

- 12.1.1 KONINKLIJKE PHILIPS N.V.

- TABLE 224 KONINKLIJKE PHILIPS N.V.: COMPANY OVERVIEW

- FIGURE 60 KONINKLIJKE PHILIPS N.V.: COMPANY SNAPSHOT

- TABLE 225 KONINKLIJKE PHILIPS N.V.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 226 KONINKLIJKE PHILIPS N.V.: PRODUCT LAUNCHES

- TABLE 227 KONINKLIJKE PHILIPS N.V.: DEALS

- TABLE 228 KONINKLIJKE PHILIPS N.V.: OTHERS

- 12.1.2 MICROSOFT

- TABLE 229 MICROSOFT: COMPANY OVERVIEW

- FIGURE 61 MICROSOFT: COMPANY SNAPSHOT

- TABLE 230 MICROSOFT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 231 MICROSOFT: PRODUCT LAUNCHES

- TABLE 232 MICROSOFT: DEALS

- TABLE 233 MICROSOFT: OTHERS

- 12.1.3 SIEMENS HEALTHINEERS AG

- TABLE 234 SIEMENS HEALTHINEERS AG: COMPANY OVERVIEW

- FIGURE 62 SIEMENS HEALTHINEERS AG: COMPANY SNAPSHOT

- TABLE 235 SIEMENS HEALTHINEERS AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 236 SIEMENS HEALTHINEERS AG: PRODUCT LAUNCHES

- TABLE 237 SIEMENS HEALTHINEERS AG: DEALS

- TABLE 238 SIEMENS HEALTHINEERS AG: OTHERS

- 12.1.4 INTEL CORPORATION

- TABLE 239 INTEL CORPORATION: COMPANY OVERVIEW

- FIGURE 63 INTEL CORPORATION: COMPANY SNAPSHOT

- TABLE 240 INTEL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 241 INTEL CORPORATION: PRODUCT LAUNCHES

- TABLE 242 INTEL CORPORATION: DEALS

- TABLE 243 INTEL CORPORATION: OTHERS

- 12.1.5 NVIDIA CORPORATION

- TABLE 244 NVIDIA CORPORATION: COMPANY OVERVIEW

- FIGURE 64 NVIDIA CORPORATION: COMPANY SNAPSHOT

- TABLE 245 NVIDIA CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 246 NVIDIA CORPORATION: PRODUCT LAUNCHES

- TABLE 247 NVIDIA CORPORATION: DEALS

- TABLE 248 NVIDIA CORPORATION: OTHERS

- 12.1.6 GOOGLE INC.

- TABLE 249 GOOGLE INC.: COMPANY OVERVIEW

- FIGURE 65 GOOGLE INC.: COMPANY SNAPSHOT

- TABLE 250 GOOGLE INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 251 GOOGLE INC.: PRODUCT LAUNCHES

- TABLE 252 GOOGLE INC.: DEALS

- TABLE 253 GOOGLE INC.: OTHERS

- 12.1.7 GE HEALTHCARE

- TABLE 254 GE HEALTHCARE: COMPANY OVERVIEW

- FIGURE 66 GE HEALTHCARE: COMPANY SNAPSHOT

- TABLE 255 GE HEALTHCARE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 256 GE HEALTHCARE: PRODUCT LAUNCHES

- TABLE 257 GE HEALTHCARE: DEALS

- 12.1.8 MEDTRONIC

- TABLE 258 MEDTRONIC: COMPANY OVERVIEW

- FIGURE 67 MEDTRONIC: COMPANY SNAPSHOT

- TABLE 259 MEDTRONIC: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 260 MEDTRONIC: DEALS

- 12.1.9 MICRON TECHNOLOGY, INC.

- TABLE 261 MICRON TECHNOLOGY, INC.: COMPANY OVERVIEW

- FIGURE 68 MICRON TECHNOLOGY, INC.: COMPANY SNAPSHOT

- TABLE 262 MICRON TECHNOLOGY, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 263 MICRON TECHNOLOGY, INC: .PRODUCT LAUNCHES

- TABLE 264 MICRON TECHNOLOGY, INC.: DEALS

- 12.1.10 AMAZON.COM, INC.

- TABLE 265 AMAZON.COM, INC.: COMPANY OVERVIEW

- FIGURE 69 AMAZON.COM, INC.: COMPANY SNAPSHOT

- TABLE 266 AMAZON.COM, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 267 AMAZON.COM, INC.: PRODUCT LAUNCHES

- TABLE 268 AMAZON.COM, INC.: DEALS

- 12.1.11 ORACLE

- TABLE 269 ORACLE: COMPANY OVERVIEW

- FIGURE 70 ORACLE: COMPANY SNAPSHOT

- TABLE 270 ORACLE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 271 ORACLE: PRODUCT LAUNCHES

- TABLE 272 ORACLE: DEALS

- 12.1.12 JOHNSON & JOHNSON SERVICES, INC.

- TABLE 273 JOHNSON & JOHNSON SERVICES, INC.: COMPANY OVERVIEW

- FIGURE 71 JOHNSON & JOHNSON SERVICES, INC.: COMPANY SNAPSHOT

- TABLE 274 JOHNSON & JOHNSON SERVICES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 275 JOHNSON & JOHNSON SERVICES, INC.: DEALS

- 12.2 OTHER PLAYERS

- 12.2.1 MERATIVE

- 12.2.2 GENERAL VISION INC.

- 12.2.3 CLOUDMEDX

- 12.2.4 ONCORA MEDICAL

- 12.2.5 ENLITIC, INC.

- 12.2.6 LUNIT INC.

- 12.2.7 QURE.AI

- 12.2.8 TEMPUS

- 12.2.9 COTA

- 12.2.10 FDNA INC.

- 12.2.11 RECURSION

- 12.2.12 ATOMWISE INC.

- 12.2.13 VIRGIN PULSE

- 12.2.14 BABYLON HEALTHCARE SERVICES LTD

- 12.2.15 MDLIVE (EVERNORTH GROUP)

- 12.2.16 STRYKER

- 12.2.17 QVENTUS

- 12.2.18 SWEETCH

- 12.2.19 SIRONA MEDICAL, INC.

- 12.2.20 GINGER

- 12.2.21 BIOBEAT

- *Details on Business overview, Products /Solutions/Services offered, Recent developments, Product launches, MnM view, Key strengths/Right to win, Strategic choices made, and Weaknesses and Competitive threats might not be captured in case of unlisted companies.

13 APPENDIX

- 13.1 DISCUSSION GUIDE

- 13.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 13.3 CUSTOMIZATION OPTIONS

- 13.4 RELATED REPORTS

- 13.5 AUTHOR DETAILS