ガスセンサーの世界市場:製品別、出力タイプ別、接続方式別、技術別、タイプ別、最終用途別、地域別 - 2033年までの予測

Gas Sensor Market By Gas Type (Oxygen, Carbon Monoxide, Carbon Dioxide, Volatile Organic Compounds, Hydrocarbons), Technology (Electrochemical, Infrared, Solid-State/Metal-Oxide-Semiconductors), Output Type, Connectivity- Global Forecast to 2033- 発行日

- ページ情報

- 英文 310 Pages

- 納期

-

即納可能

営業時間内にお支払方法などの確認が取れ次第、Eメールにて納品となります。営業時間: 9:00am - 6:00pm (土日祝除く)。

- 商品コード

- 1936012

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

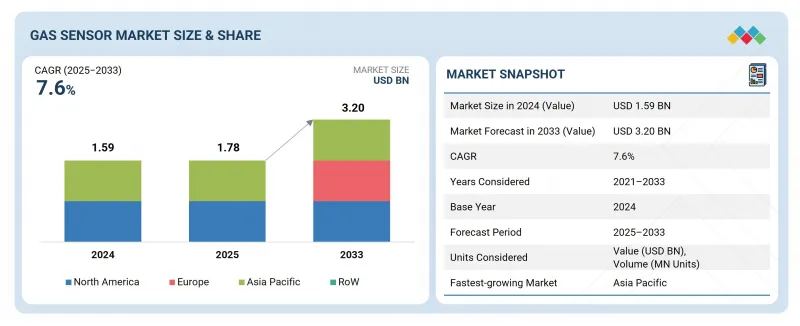

世界のガスセンサーの市場規模は、2025年の17億8,000万米ドルから2033年までに32億米ドルへ成長し、2025年から2033年までの年間平均成長率(CAGR)は7.6%と予測されています。

この成長は、石油・ガス、化学、鉱業、電力などの主要産業における需要増加によって牽引されています。さらに、IoT(モノのインターネット)、ビルオートメーション、および近代的な制御システムの進歩により、小型化されたワイヤレスガスセンサーの需要が高まっています。これらのセンサーは、低消費電力、高性能、小型サイズが評価されています。

| 調査範囲 | |

|---|---|

| 調査対象期間 | 2020年~2033年 |

| 基準年 | 2024年 |

| 予測期間 | 2025年~2033年 |

| 対象単位 | 金額(10億米ドル) |

| セグメント | 製品別、出力タイプ別、接続方式別、技術別、タイプ別、最終用途別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

さらに、スマートフォンやウェアラブルデバイスへのガスセンサーの統合により、環境や大気中の空気質を継続的に監視することが可能となり、今後数年間で需要が拡大すると予想されます。

「出力タイプ別では、デジタルセグメントが予測期間中に最も高いCAGRで成長する見込みです」

ガスセンサー市場のデジタルセグメントは、より高度でインテリジェント、かつ接続方式を備えたガス検知ソリューションへの需要増加により、より高いCAGRを記録すると予想されます。デジタルガスセンサーは、アナログ式と比較して、精度向上、スマートシステムとの接続方式、高度な信号処理機能など、複数の利点を提供します。産業分野におけるデジタル化やモノのインターネット(IoT)技術の採用が進むにつれ、デジタルネットワークへの接続、遠隔データ送信、自動化システムへの統合が可能なガスセンサーの需要が高まっています。

有線セグメントは、確立されたインフラと産業用途における信頼性から、市場全体でより大きなシェアを占めています。有線ガスセンサーは、安定した継続的なデータ伝送が不可欠であり、電源供給と接続方式が確保されている環境で一般的に使用されます。製造業、石油化学、自動車、医療などの産業では、耐久性と制御システムへの直接接続方式から有線センサーが好まれ、正確かつ途切れないデータ監視が保証されます。有線ガスセンサーは、無線技術に影響を与える可能性のある干渉や信号損失の問題を受けにくいことから、特定の用途においてより安全で安定していると見なされることが多いです。

予測期間中、中国はアジア太平洋におけるガスセンサー市場での優位性を維持すると見込まれます。同国では、プロセス産業(特に化学製品製造や石油精製)および電力発電などの公益事業が、ガスセンサーの主要な需要源であり続けるでしょう。石油・ガス、インフラ、上下水道処理などの分野が、ガスセンサー市場の成長を牽引すると予測されています。さらに、大気汚染の健康への影響に関する一般の認識が高まっていることも、ガスセンサーを搭載したスマート空気質モニター、スマートバンド、空気清浄機、空気清浄装置の需要を後押ししています。

Honeywell International Inc.(米国)、MSA Safety Incorporated(米国)、 Amphenol Corporation(米国)、Figaro Engineering Inc.(日本)、Alphasense(英国)、Sensirion AG(スイス)、Process Sensing Technologies(英国)、ams-OSRAM AG(オーストリア)、MEMBRAPOR(スイス)、Senseair AB(米国)などが、ガスセンサー市場の主要企業です。

本調査では、ガスセンサー市場におけるこれらの主要企業について、詳細な競合分析に加え、企業プロファイル、最近の動向、主要な市場戦略を掲載しています。

調査範囲:

当調査レポートでは、ガスセンサー市場を出力タイプ別、接続方式別、製品タイプ別、技術別、タイプ別、最終用途別、地域別に分析しています。当レポートでは、ガスセンサー市場における主要な市場促進要因、抑制要因、課題、機会を概説し、2033年までの予測を提供します。また、ガスセンサーエコシステム内の全企業に関するリーダーシップマッピングと分析も含まれています。

当レポート購入の主なメリット

当レポートは、ガスセンサー市場全体およびそのサブセグメントの推定収益額を提供することで、市場リーダーや新規参入企業を支援します。利害関係者が競合情勢を理解し、自社のビジネスをより良い位置付けに導き、効果的な市場参入戦略を策定するための洞察を得るのに役立ちます。さらに、主要な促進要因、抑制要因、課題、機会を含む市場の動向に関する情報を提供します。

当レポートは以下のポイントに関する洞察を提供します:

- 主要な促進要因(石油・ガス、化学、鉱業、電力セクターにおける需要増加、健康安全規制の実施、HVACシステムや大気質モニターへのガスセンサーの統合、自動運転車需要の急増)機会(モノのインターネット、クラウドコンピューティング、ビッグデータ技術の統合、民生用電子機器での採用拡大、小型無線ガスセンサーの需要増加)、課題(複雑な製造プロセス)がガスセンサー市場の成長に与える影響について

- 製品開発/イノベーション:ガスセンサー市場における今後の技術動向、研究開発活動、最新製品・サービスのリリースに関する詳細な分析

- 市場開発:収益性の高い市場に関する包括的な情報- 当レポートでは、様々な地域におけるガスセンサー市場を分析しています

- 市場の多様化:新製品・サービス、未開拓地域、最近の動向、ガスセンサー市場への投資に関する包括的な情報

- 競合評価:主要企業 - Honeywell International Inc.(米国)、MSA Safety Incorporated(米国)、Amphenol Corporation(米国)、Figaro Engineering Inc(日本)、Alphasense(英国)、Sensirion AG(スイス)、Process Sensing Technologies(英国)、ams-オスラムAG(オーストリア)、MEMBRAPOR(スイス)、Senseair AB(米国)など、ガスセンサー市場における主要企業の市場シェア、成長戦略、サービス提供内容に関する詳細な分析

よくあるご質問

目次

第1章 イントロダクション

第2章 エグゼクティブサマリー

第3章 重要考察

第4章 市場概要

- 市場力学

- アンメットニーズと空白

- 相互接続された市場と分野横断的な機会

- ティア1/2/3企業の戦略的動き

- 市場力学

第5章 業界動向

- ポーターのファイブフォース分析

- マクロ経済指標

- バリューチェーン分析

- エコシステム分析

- 価格分析

- 貿易分析

- 2025年~2026年の主な会議とイベント

- 顧客のビジネスに影響を与える動向/ディスラプション

- 2024年と2025年の投資と資金調達のシナリオ

- ケーススタディ分析

- 2025年の米国関税の影響

第6章 技術の進歩、AIによる影響、特許、イノベーション、そして将来の応用

- 技術の進歩

- 技術/製品ロードマップ

- 特許分析

- AIがガスセンサーに与える影響

第7章 規制状況

- 規制機関、政府機関、その他の組織

- ガスセンサーに関する規格および規制

- 標準

第8章 顧客情勢と購買行動

- 意思決定プロセス

- 主要な利害関係者と購入基準

- 採用障壁と内部課題

- さまざまなエンドユーザーからのアンメットニーズ

第9章 ガスセンサー市場(製品別)

- ガス分析装置とモニター

- ガス検知器

- 空気質モニター

- 空気清浄機

- HVACシステム

- 医療機器

- 消費者向けデバイス

第10章 ガスセンサ市場(出力タイプ別)

- アナログ

- デジタル

第11章 ガスセンサー市場(接続方式別)

- 有線

- 無線

第12章 ガスセンサー市場(技術別)

- 電気化学

- 光イオン化検出

- 固体/金属酸化物半導体

- 触媒

- 赤外線

- レーザ

- ジルコニア

- ホログラフィック

- その他

第13章 ガスセンサー市場(タイプ別)

- 酸素

- 一酸化炭素

- 二酸化炭素

- アンモニア

- 塩素

- 硫化水素

- 窒素酸化物

- 揮発性有機化合物

- メタン

- 炭化水素

- 水素

第14章 ガスセンサー市場(最終用途別)

- 自動車・輸送

- スマートシティとビルオートメーション

- 石油・ガス

- 水・廃水処理

- 食品・飲料

- 発電所

- 医療

- 金属・化学品

- 鉱業

- 家電

- 政府・規制機関

第15章 ガスセンサー市場(地域別)

- 北米

- 北米のマクロ経済見通し

- 米国

- カナダ

- メキシコ

- 欧州

- 欧州のマクロ経済見通し

- 英国

- ドイツ

- フランス

- イタリア

- その他

- アジア太平洋

- アジア太平洋のマクロ経済見通し

- 中国

- 日本

- インド

- 韓国

- その他

- その他の地域

- その他の地域のマクロ経済見通し

- 中東・アフリカ

- 南米

第16章 競合情勢

- 概要

- 主要参入企業の戦略/強み、2021年~2025年

- 市場シェア分析、2024年

- 収益分析、2020年~2024年

- 企業評価と財務指標

- ブランド/製品比較

- 企業評価マトリックス:主要参入企業、2024年

- 企業評価マトリックス:スタートアップ/中小企業、2024年

- 競合シナリオ

第17章 企業プロファイル

- 主要参入企業

- HONEYWELL INTERNATIONAL INC.

- MSA SAFETY INCORPORATED

- AMPHENOL CORPORATION

- SENSIRION AG

- AMS-OSRAM AG

- FIGARO ENGINEERING INC.

- ALPHASENSE

- PROCESS SENSING TECHNOLOGIES

- MEMBRAPOR

- SENSEAIR AB(ASAHI KASEI MICRODEVICES)

- NISSHA CO., LTD.

- FUJI ELECTRIC CO., LTD.

- RENESAS ELECTRONICS CORPORATION

- DANFOSS

- GASERA LTD.

- INFINEON TECHNOLOGIES AG

- その他の企業

- NITERRA CO., LTD.

- BREEZE TECHNOLOGIES

- ELICHENS

- BOSCH SENSORTEC GMBH

- EDINBURGH SENSORS

- GASTEC CORPORATION

- NEMOTO & CO., LTD.

- SPEC SENSORS

- SIA MIPEX

- CUBIC SENSOR AND INSTRUMENT CO., LTD.

- WINSEN

第18章 調査手法

第19章 付録

- 発行日

- 発行

- MarketsandMarkets

- ページ情報

- 英文 310 Pages

- 納期

- 即納可能