|

|

市場調査レポート

商品コード

1376867

鉄道車両用バッテリーの世界市場 (~2030年):タイプ・技術 (鉛蓄電池・VRLA・従来型・Ni-Cd焼結・ファイバー・ポケット・Li-ion・LFP・LTO)・先進鉄道 (完全バッテリー駆動・ハイブリッド)・車両タイプ・用途・地域別Train Battery Market by Type & Technology (Lead-acid Tubular, VRLA, Conventional; Ni-Cd Sinter, Fiber, Pocket, & Li-ion; LFP, LTO), Advanced Train (Fully Battery-Operated and Hybrid), Rolling Stock Type, Application and Region - Global Forecast to 2030 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 鉄道車両用バッテリーの世界市場 (~2030年):タイプ・技術 (鉛蓄電池・VRLA・従来型・Ni-Cd焼結・ファイバー・ポケット・Li-ion・LFP・LTO)・先進鉄道 (完全バッテリー駆動・ハイブリッド)・車両タイプ・用途・地域別 |

|

出版日: 2023年11月03日

発行: MarketsandMarkets

ページ情報: 英文 315 Pages

納期: 即納可能

|

全表示

- 概要

- 目次

報告書概要

| 調査範囲 | |

|---|---|

| 調査対象年 | 2023-2030年 |

| 基準年 | 2022年 |

| 予測期間 | 2023-2030年 |

| 単位 | 金額 (米ドル) |

| セグメント | OEバッテリータイプ・OEバッテリー技術・OE用途・OEエンジン/ヘッド・OE用途・OE先進車両タイプ・アフターマーケット車両・アフターマーケットバッテリータイプ・アフターマーケット用途・地域 |

| 対象地域 | アジア太平洋・欧州・北米・その他の地域 |

鉄道車両用バッテリーの市場規模は、2023年の2億7,700万米ドルから、予測期間中は4.6%のCAGRで推移し、2030年には3億7,800万米ドルの規模に成長すると予測されています。

市場成長の主な要因は、急速な都市化や鉄道網の拡大です。これらの要因に加え、鉄道による迅速な移動と他の交通手段に比べて低い運用コストが、世界中の政府を都市鉄道インフラへの投資に駆り立てています。鉄道網の拡大により、エネルギー貯蔵システムの需要が高まることが予想されています。

2021年現在、Urban Transport Trends and Prospects (UTTP) によると、ライトレールと路面電車の総延長は15,824kmに及びます。これらのネットワークの大半は欧州にあり、全体の58%を占め、ユーラシア大陸は22%を占めています。注目すべきは、フィンランド、英国、スイスなど、欧州の数カ国がライトレールネットワークの拡大に積極的に力を入れていることです。例えば2021年、英国政府はBlackpool Tramの延伸を承認しました。さらに、地下鉄プロジェクトの開発が進んでいることも、地下鉄システムにおけるバッテリーの需要増加に寄与しています。さらに、ロシア政府は2022年12月、総工費68億米ドルの70kmモスクワ大環状線地下鉄プロジェクトの建設を開始しました。その結果、ライトレールや路面電車網の成長と都市交通のための地下鉄システムの採用拡大が相まって、今後数年間、これらの交通手段における電池の利用が促進されると予想されています。

用途別では、補助バッテリーの部門が2023年に最大のシェアを示す見通しです。補助バッテリーシステムは、非常用照明や換気など、鉄道に不可欠なすべてのシステムにバックアップを提供します。補助バッテリーはまた、出力障害や列車分離事故などを起こさず、列車に安全性を提供します。さらに、高速鉄道への需要の増加は、非常ブレーキ、傾斜システムなどの高度な機能に対する高い需要につながっています。VRLA技術は、メンテナンスフリー、定期的な注水不要、急速充電能力、耐熱性・耐衝撃性などの技術的利点により、鉄道車両用バッテリー市場で最大のシェアを占めており、主に鉄道の補助機能に好まれています。しかし、エネルギー密度が高く、低温性能が高く、サイクル寿命が長いため、VRLA電池よりも充電回数が多くなります。したがって、ニッケルカドミウム電池のこれらの利点を考慮すると、鉄道におけるVRLA電池の需要は徐々に影響を受けると考えられています。

さらに、最新の鉄道車両は、IoT、AI、ディープラーニング、 ドライバーアドバイザリーシステム (DAS) などの先進技術を導入し、効率を向上させ、乗客体験を高めています。AC、ヒーター、ブレーキシステム、その他の車載機器などの現場機器の最適化や、資源計画、乗客体験、意思決定の改善といった要因も、補助システムバッテリーの採用率を高めると予想されています。

当レポートでは、世界の鉄道車両用バッテリーの市場を調査し、市場概要、市場影響因子および市場機会の分析、技術・特許動向、ケーススタディ、法規制環境、市場規模の推移・予測、各種区分・地域別の詳細分析、競合情勢、主要企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 顧客の事業に影響を与える動向とディスラプション

- 市場エコシステム

- バリューチェーン分析

- サプライチェーン分析

- 規制状況

- 貿易分析

- 価格分析

- 技術分析

- 特許分析

- ケーススタディ分析

- 主要な会議とイベント

- 購入基準

- 部品表

第6章 鉄道車両用バッテリー市場:用途・電池タイプ別

- スターターバッテリー

- 鉛蓄電池

- ニカド電池

- 補助バッテリー

- 鉛蓄電池

- ニカド電池

- リチウムイオン電池

第7章 鉄道車両用バッテリー市場:電池タイプ・電池技術別

- 鉛蓄電池

- 従来型鉛蓄電池

- 制御弁式鉛蓄電池

- ゲルチューブ状鉛蓄電池

- ニッケルカドミウム電池

- 焼結/PNEニッケルカドミウム電池

- ポケットプレートニッケルカドミウム電池

- ファイバー/PNEニッケルカドミウム電池

- リチウムイオン電池

- リン酸鉄リチウム電池

- チタン酸リチウム酸化物電池

- その他

第8章 鉄道車両用バッテリー市場:エンジン/ヘッド別

- ディーゼル機関車

- ディーゼルマルチユニット

- 電気機関車

- 電気マルチユニット

第9章 鉄道車両用バッテリー市場:鉄道用途別

- メトロ

- 高速鉄道

- ライトレール/路面電車/モノレール

- 客車

第10章 鉄道車両用バッテリー市場:先進鉄道タイプ別

- ハイブリッド鉄道

- 完全バッテリー鉄道

- 自動運転鉄道

第11章 鉄道車両用バッテリー市場:地域別

- アジア太平洋

- 欧州

- 北米

- その他の地域

第12章 アフターマーケット鉄道車両用バッテリー市場:車両タイプ別

- 機関車

- マルチユニット

- 客車

第13章 アフターマーケット鉄道車両用バッテリー市場:バッテリータイプ別

- 鉛蓄電池

- ニッケルカドミウム電池

第14章 アフターマーケット鉄道車両用バッテリー市場:用途別

- スターターバッテリー

- 補助バッテリー

第15章 アフターマーケット鉄道車両用バッテリー市場:地域別

- 欧州

- 北米

第16章 競合情勢

- 概要

- 市場シェア分析

- 上位上場企業/一般企業の収益分析

- 企業評価マトリックス

- 競合シナリオ

- 主要企業の戦略

- 主要なバッテリーサプライヤー:現在の製品と将来の製品計画

第17章 企業プロファイル

- 主要企業

- ENERSYS

- SAFT

- GS YUASA INTERNATIONAL LTD.

- EXIDE INDUSTRIES LTD.

- AMARA RAJA BATTERIES LIMITED

- HOPPECKE BATTERIEN GMBH & CO. KG

- SEC BATTERY

- FIRST NATIONAL BATTERY

- POWER & INDUSTRIAL BATTERY SYSTEMS GMBH

- EXIDE TECHNOLOGIES

- TOSHIBA CORPORATION

- その他の企業

- EAST PENN MANUFACTURING COMPANY

- MICROTEX ENERGY PRIVATE LIMITED

- AEG POWER SOLUTIONS

- FURUKAWA ELECTRIC CO., LTD.

- HUNAN FENGRI POWER & ELECTRIC CO., LTD.

- SHUANGDENG GROUP CO., LTD.

- COSLIGHT INDIA

- SHIELD BATTERIES LIMITED

- AKASOL AG

- DMS TECHNOLOGIES

- NATIONAL RAILWAY SUPPLY

- LECLANCHE SA

- ECOBAT

- HBL BATTERIES

- STAR BATTERY LTD.

- HITACHI, LTD.

第18章 MARKETSANDMARKETSからの提言

- アジア太平洋:バッテリー製造業者が注目する潜在市場

- 高いエネルギー密度を備えたコスト効率の高いバッテリー技術:将来のニーズ

- 総論

第19章 付録

Report Description

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2023-2030 |

| Base Year | 2022 |

| Forecast Period | 2023-2030 |

| Units Considered | Value (USD Million) |

| Segments | By Battery Type, Battery Technology, Application, engines/head, application, advanced train type, aftermarket by rolling stock, aftermarket by battery type, application, and region, and OE by Region |

| Regions covered | Asia Pacific, Europe, North America, and the Rest of the World |

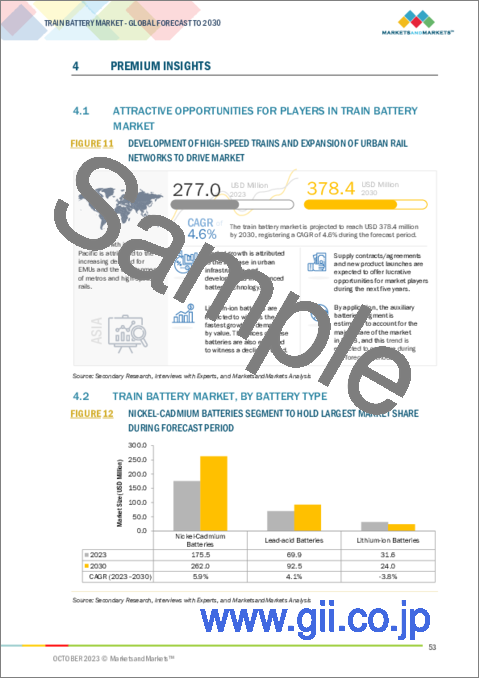

The train battery market is projected to grow from USD 277 Million in 2023 to USD 378 Million by 2030, at a CAGR of 4.6% from 2023 to 2030. The train battery market is primarily driven by factors such as rapid urbanization and the growing expansion of railway networks. Along with these factors, the swiftness of rail travel and low operational cost compared to other modes of transport are driving governments all over the globe to invest in urban rail infrastructure. The growing expansion of rail networks is expected to create a demand for energy storage systems.

As of 2021, Urban Transport Trends and Prospects (UTTP) indicates that there is a total operational network of light rails and trams spanning 15,824 kilometers. Most of these networks are situated in Europe, accounting for 58% of the total, while Eurasia constitutes 22%. Notably, several European countries, including Finland, the UK, and Switzerland, are actively focusing on expanding their light rail networks. For instance, in 2021, the UK government approved the extension of the Blackpool Tram. Additionally, the increasing development of metro projects is contributing to the rising demand for batteries in metro systems. As an example, in December 2022, the Russian government initiated the construction of the 70-km Moscow Big Circle Line metro project, with a total cost of USD 6.8 billion. Consequently, the growth of light rail and tram networks, coupled with the growing adoption of metro systems for urban transit, is expected to fuel the utilization of batteries in these modes of transportation in the upcoming years.

"The Auxiliary Batteries are expected to account for the largest market share in 2023."

The auxiliary battery systems provide backup to all essential train systems, such as emergency lighting and ventilation. Auxiliary batteries also offer safety to the train without output failure and train separation incidents. Additionally, the increase in the demand for high-speed trains is leading to the high demand for advanced features such as emergency braking, tilting systems, etc. VRLA technology holds the largest share in the train battery market due to its technical benefits such as maintenance-free operation, no periodic water filling requirement, fast charging capability, and heat & shock resistance, and is mainly preferred for auxiliary functions in railways. However, the high energy density, good low-temperature performance, and good cycle life means can be recharged more times than VRLA batteries. Hence, considering these benefits of Ni-cd batteries, the demand for VRLA batteries in railways will be impacted gradually. Moreover, the latest rolling stocks have been implementing advanced technologies such as the Internet of Things (IoT), artificial intelligence (AI), deep learning, and driver advisory systems (DAS) to improve efficiency and enhance the passenger experience. Improvements in resource planning, passenger experience, and decision-making, along with the optimization of field equipment such as ACs, heaters, braking systems, and other onboard appliances, are expected to increase the adoption rate of train batteries for these auxiliary systems.

"Passenger Coaches will dominate the train battery market during the forecast period."

Passenger coaches are railroad cars designed to carry passengers. Modern passenger coaches require auxiliary batteries for functions such as reading lights, bathroom lights, vestibule lights, door lights, emergency lights, HVACs, fans, screens, Wi-Fi, and ceiling lights. These functions depend upon the types of coaches, such as AC and non-AC coaches. In developed countries, coaches have automated doors, infotainment systems, and passenger information systems. These added features are powered through battery power packs. The battery capacity for AC coaches is higher compared to non-AC passenger coaches. Typically, the voltage capacity requirement for passenger capacity is 108V to 120V. Batteries installed in passenger coaches are used for auxiliary power backup. Based on the capacity and power output of the passenger coach, the manufacturer decides the battery chemistry. With increased travel demand, environmental concerns, government investments, improved passenger amenities, safety and reliability, high-speed rail development, intermodal connectivity, and reduced congestion, the need for passenger coaches and train batteries would grow parallelly in the coming years.

"Asia Pacific is expected to account for the largest aftermarket share in 2022."

The Asia Pacific region has the world's most extensive railway network and holds the top spot in the global count of rolling stock. Furthermore, it stands as the world's largest producer of rolling stock. This geographical concentration of major rolling stock manufacturers has notably driven the demand for train batteries.

Moreover, with the widespread urban rail network expansion and the presence of international train battery manufacturers in the region, an anticipated rise in demand is foreseen. This is further compounded by the escalating number of passengers, which will necessitate increased utilization of train batteries to enhance the overall travel experience. Rail network electrification, emission regulations, and advancements in battery technologies are expected to drive train battery aftermarket in Asia Pacific. The growing diesel engine retrofitting and refurbishment at a year-on-year rate of 5%. Further, trains operating in the Asia Pacific region are at high temperatures compared to Europe and North America due to which battery lifespan in the Asia Pacific region is less, thus the demand for battery replacement is high.

Breakdown of Primaries

In-depth interviews were conducted with CXOs, marketing directors, other innovation and technology directors, and executives from various key organizations operating in this market.

- By Company Type: Supply Side- 60%, Demand -Side- 20%, and Others - 20%

- By Designation: C Level Executives - 20%, Directors/ Vice Presidents-30%, and Others -50%

- By Region: North America - 20%, Asia Pacific- 40%, Europe - 30%, and Rest of the World - 10%

The train battery market comprises major manufacturers such as EnerSys (US), Exide Industries (India), Saft (France), Amara Raja Batteries (India), GS Yuasa Corporation (Japan), and HOPPECKE Batterien GmbH & Co.KG.

Reasearch Coverage

The study segments the train battery market and forecasts the market size based on by Application & by Battery type Starter (Lead-Acid, Nickel-Cadmium, Lithium-ion) and Auxiliary (Lead-Acid, Nickel-Cadmium, Lithium-ion, By Battery Type & Battery Technology Lead-Acid Battery (Conventional Lead Acid Battery, Valve Regulated Lead Acid Battery, Gel Tubular Lead Acid Battery) Nickel-Cadmium Battery (Sinter/PNE Ni-Cd Battery, Pocket Plate Ni-Cd Battery, Fiber/PNE Ni-Cd Battery) Lithium-ion Battery (Lithium Iron Phosphate (LFP), Lithium Titanate Oxide (LTO), and Others), By Engines/Head (Diesel Locomotives, Diesel Multiple Units (DMUs), Electric Locomotives, and Electric Multiple Units (EMUs), By Application (Metros, High-speed Trains, Light Trains/Trams/ Monorails, Passenger Coaches), By Advanced Train Type (Battery-Powered Train, and Hybrid Trains), Aftermarket by Rolling Stock (Locomotives, Multiple Units, Passenger Coaches), Aftermarket By Battery Type (lead-Acid, Nickel-Cadmium, Lithium-Ion), Aftermarket by application (starter battery, and auxiliary function battery), Aftermarket by region (Asia Pacific, Europe, and North America), and OE by region (Asia Pacific, Europe, North America and Rest of the World).

Key Benefits of Buying the Report:

This report provides insights concerning the following points:

- Country-level battery type-wise market: The report offers in-depth market sizing and forecasts for 2030 by battery types, such as lead-acid, nickel-cadmium, and lithium-ion. The market sizing for the train battery market is covered at the country and regional levels considered in this study.

- By Application & battery type: The report offers in-depth market sizing and forecasts up to 2030 by applications, such as starter and auxiliary-in-depth analysis of different battery types used in Starter and Auxiliary Applications at the regional level.

- Battery Type, by Battery Technology: The report offers in-depth market sizing and forecasts up to 2030 by battery type, such as lead-acid, nickel-cadmium, and lithium-ion. The report provides market sizing and forecasting till 2030 by battery technology under different battery types such as lead acid battery type (conventional lead-acid, Valve regulated lead-acid, and gel tubular lead-acid battery), Nickel-cadmium (Sinter/PNE Ni-Cd, Pocket Plate Ni-Cd, and Fiber/Pne Ni-Cd), and Lithium-ion (lithium iron phosphate (LFP), Lithium Titanate Oxide)

- The report provides the "Market Share" of the leading train battery market players.

- Market Development: The report provides comprehensive information about lucrative emerging markets across regions for the train battery market.

- Product Development/Innovation: The report gives detailed insights into R&D activities, upcoming technologies, and new product launches in the train battery market.

- Market Diversification: The report offers detailed information about untapped markets, investments, new products, and recent developments in the train battery market.

The report provides insights on the following pointers:

- Analysis of key drivers (Growth in adoption of autonomous and high-speed railways, Emission regulations to increase demand for energy-efficient transportation systems, and Expansion of railway networks), Restraints (High capital investment and operating cost of high-speed rail networks), Opportunities (Expansion of IOT, AI, and DAS Technologies, Improvements in Battery Technology, Retrofitting of Diesel-electric trains), Challenges (Technical Challenges related to lead-acid and lithium-ion batteries, High cost of charging infrastructure and replacement).

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the train battery market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the train battery market across different regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the train battery market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like EnerSys (US), Exide Industries (India), Saft (France), Amara Raja Batteries (India), GS Yuasa Corporation (Japan), and HOPPECKE Batterien GmbH & Co.KG. in the train battery market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 INCLUSIONS AND EXCLUSIONS

- TABLE 1 SEGMENT-WISE INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- FIGURE 1 MARKETS COVERED

- 1.3.1 REGIONS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 2 CURRENCY EXCHANGE RATES

- 1.5 STAKEHOLDERS

- 1.6 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 RESEARCH DESIGN

- FIGURE 3 RESEARCH METHODOLOGY MODEL

- 2.1.1 SECONDARY DATA

- 2.1.1.1 List of key secondary sources to estimate base numbers and market size (Locomotive & Rolling Stock)

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS

- 2.1.2.1 Sampling techniques and data collection methods

- 2.1.3 PRIMARY PARTICIPANTS

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 5 RESEARCH METHODOLOGY: HYPOTHESIS BUILDING

- 2.2.1 BOTTOM-UP APPROACH: TRAIN BATTERY MARKET, BY BATTERY TYPE AND ROLLING STOCK

- FIGURE 6 BOTTOM-UP APPROACH, BY BATTERY TYPE AND ROLLING STOCK

- 2.2.2 TOP-DOWN APPROACH: TRAIN BATTERY MARKET, BY BATTERY TECHNOLOGY

- FIGURE 7 TOP-DOWN APPROACH, BY BATTERY TECHNOLOGY

- 2.3 FACTOR ANALYSIS FOR MARKET SIZING: DEMAND AND SUPPLY SIDES

- 2.4 FACTOR ANALYSIS

- 2.5 RECESSION IMPACT

- 2.6 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 8 DATA TRIANGULATION

- 2.7 RISKS AND ASSUMPTIONS

- 2.7.1 RESEARCH ASSUMPTIONS

- 2.7.2 MARKET ASSUMPTIONS

- TABLE 3 MARKET ASSUMPTIONS: NUMBER OF BATTERIES COUNT IN EACH ROLLING STOCK

- TABLE 4 MARKET ASSUMPTIONS: NUMBER OF BATTERIES COUNT IN ADVANCED TRAINS

- TABLE 5 MARKET ASSUMPTIONS AND RISK ANALYSIS

- 2.8 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

- 3.1 REPORT SUMMARY

- FIGURE 9 TRAIN BATTERY MARKET OUTLOOK

- FIGURE 10 TRAIN BATTERY MARKET, BY REGION, 2023 VS. 2030 (USD MILLION)

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN TRAIN BATTERY MARKET

- FIGURE 11 DEVELOPMENT OF HIGH-SPEED TRAINS AND EXPANSION OF URBAN RAIL NETWORKS TO DRIVE MARKET

- 4.2 TRAIN BATTERY MARKET, BY BATTERY TYPE

- FIGURE 12 NICKEL-CADMIUM BATTERIES SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.3 TRAIN BATTERY MARKET, BY APPLICATION

- FIGURE 13 AUXILIARY BATTERIES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- 4.4 TRAIN BATTERY MARKET, BY BATTERY TECHNOLOGY

- FIGURE 14 SINTER/PNE NI-CD SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- 4.5 TRAIN BATTERY MARKET, BY ENGINE/HEAD

- FIGURE 15 ELECTRIC LOCOMOTIVES SEGMENT TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- 4.6 TRAIN BATTERY MARKET, BY RAILWAY APPLICATION

- FIGURE 16 PASSENGER COACHES SEGMENT TO HOLD LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.7 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE

- FIGURE 17 FULLY BATTERY-OPERATED TRAINS SEGMENT TO WITNESS HIGHER CAGR THAN HYBRID TRAINS SEGMENT DURING FORECAST PERIOD

- 4.8 TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK

- FIGURE 18 COACHES SEGMENT TO LEAD AFTERMARKET DURING FORECAST PERIOD

- 4.9 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE

- FIGURE 19 LEAD-ACID BATTERIES SEGMENT TO HOLD LARGER MARKET SHARE THAN NICKEL-CADMIUM BATTERIES SEGMENT DURING FORECAST PERIOD

- 4.10 TRAIN BATTERY AFTERMARKET, BY APPLICATION

- FIGURE 20 AUXILIARY BATTERIES SEGMENT TO REGISTER HIGHER CAGR THAN STARTER BATTERIES SEGMENT DURING FORECAST PERIOD

- 4.11 TRAIN BATTERY AFTERMARKET, BY REGION

- FIGURE 21 ASIA PACIFIC TO LEAD AFTERMARKET DURING FORECAST PERIOD

- 4.12 TRAIN BATTERY MARKET, BY REGION

- FIGURE 22 ASIA PACIFIC ESTIMATED TO ACCOUNT FOR LARGEST MARKET SHARE IN 2023

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 23 TRAIN BATTERY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing adoption of autonomous and high-speed railways

- FIGURE 24 LENGTH OF HIGH-SPEED RAIL LINES IN OPERATION, BY REGION, 2022

- TABLE 6 GRADE OF RAIL AUTOMATION

- TABLE 7 LIST OF SEMI-AUTONOMOUS AND AUTONOMOUS METROS

- FIGURE 25 EVOLUTION OF GOA4 INFRASTRUCTURE, 2012-2020

- 5.2.1.2 Stringent emission regulations

- FIGURE 26 TOTAL COST OF OWNERSHIP COMPARISON FOR AVERAGE US CLASS I LINE-HAUL ELECTRIC AND DIESEL FREIGHT LOCOMOTIVES, 2001-2021

- TABLE 8 RECENT DEVELOPMENTS IN BATTERY OR HYDROGEN FUEL CELL-BASED LOCOMOTIVES

- 5.2.1.3 Expansion of railway networks

- TABLE 9 UPCOMING KEY RAIL PROJECTS, BY COUNTRY

- 5.2.2 RESTRAINTS

- 5.2.2.1 High capital investment and operating cost of high-speed rail networks

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Expansion of IoT, AI, and DAS technologies

- 5.2.3.2 Improvements in battery technology

- 5.2.3.3 Retrofitting of diesel-electric trains

- 5.2.4 CHALLENGES

- 5.2.4.1 Technical challenges related to lead-acid and lithium-ion batteries

- FIGURE 27 BATTERY CHEMISTRY COMPARISON

- 5.2.4.2 High cost of charging infrastructure and replacement

- 5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.4 MARKET ECOSYSTEM

- FIGURE 28 TRAIN BATTERY MARKET ECOSYSTEM

- 5.4.1 TRAIN BATTERY MANUFACTURERS

- 5.4.2 COMPONENT/RAW MATERIAL SUPPLIERS

- 5.4.3 TRAIN OEMS

- 5.4.4 GOVERNMENT AND REGULATORY AUTHORITIES

- FIGURE 29 TRAIN BATTERY MARKET SEGMENT ECOSYSTEM

- 5.4.5 DEALERS AND DISTRIBUTORS

- 5.4.6 SERVICE & REPAIR PROVIDERS

- TABLE 10 TRAIN BATTERY MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- 5.5 VALUE CHAIN ANALYSIS

- FIGURE 30 TRAIN BATTERY MARKET: VALUE CHAIN ANALYSIS

- 5.6 SUPPLY CHAIN ANALYSIS

- FIGURE 31 TRAIN BATTERY MARKET: SUPPLY CHAIN ANALYSIS

- 5.7 REGULATORY LANDSCAPE

- TABLE 11 NORTH AMERICA: LOCOMOTIVE AND BATTERY SYSTEMS REGULATIONS

- TABLE 12 EUROPE: LOCOMOTIVE AND BATTERY SYSTEMS REGULATIONS

- TABLE 13 ASIA PACIFIC: LOCOMOTIVE AND BATTERY SYSTEMS REGULATIONS

- 5.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 14 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.8 TRADE ANALYSIS

- 5.8.1 IMPORT DATA

- 5.8.1.1 US

- TABLE 17 US: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (IMPORT VALUE %)

- 5.8.1.2 Canada

- TABLE 18 CANADA: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (IMPORT VALUE %)

- 5.8.1.3 Japan

- TABLE 19 JAPAN: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (IMPORT VALUE %)

- 5.8.1.4 India

- TABLE 20 INDIA: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (IMPORT VALUE %)

- 5.8.1.5 Germany

- TABLE 21 GERMANY: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (IMPORT VALUE %)

- 5.8.1.6 France

- TABLE 22 FRANCE: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (IMPORT VALUE %)

- 5.8.1.7 Spain

- TABLE 23 SPAIN: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (IMPORT VALUE %)

- 5.8.1.8 UK

- TABLE 24 UK: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (IMPORT VALUE %)

- 5.8.2 EXPORT DATA

- 5.8.2.1 US

- TABLE 25 US: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (EXPORT VALUE %)

- 5.8.2.2 China

- TABLE 26 CHINA: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (EXPORT VALUE %)

- 5.8.2.3 Japan

- TABLE 27 JAPAN: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (EXPORT VALUE %)

- 5.8.2.4 Germany

- TABLE 28 GERMANY: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (EXPORT VALUE %)

- 5.8.2.5 France

- TABLE 29 FRANCE: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (EXPORT VALUE %)

- 5.8.2.6 Spain

- TABLE 30 SPAIN: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (EXPORT VALUE %)

- 5.8.2.7 UK

- TABLE 31 UK: RAIL LOCOMOTIVES POWERED BY ELECTRIC ACTUATORS (BATTERIES), BY COUNTRY (EXPORT VALUE %)

- 5.8.1 IMPORT DATA

- 5.9 PRICING ANALYSIS

- 5.9.1 TRAIN BATTERY PRICING, BY REGION

- TABLE 32 AVERAGE SELLING PRICE TREND, BY REGION, 2020 VS. 2022

- 5.9.2 TRAIN BATTERY PRICING, BY BATTERY TYPE

- TABLE 33 AVERAGE SELLING PRICE TREND, BY BATTERY TYPE, 2020 VS. 2022

- 5.10 TECHNOLOGICAL ANALYSIS

- 5.10.1 OVERVIEW

- 5.10.1.1 MITRAC pulse traction batteries

- 5.10.1.2 MRX nickel batteries

- 5.10.1.3 Solid-state batteries

- 5.10.1.4 Lithium-sulfur batteries

- 5.10.1 OVERVIEW

- 5.11 PATENT ANALYSIS

- 5.12 CASE STUDY ANALYSIS

- 5.12.1 CASE STUDY 1: PROJECT OF SEPTA AND VIRIDITY ENERGY TO INCREASE OPERATIONAL EFFICIENCY WITH LESS ENERGY CONSUMPTION

- 5.12.2 CASE STUDY 2: RELIABLE AUTONOMOUS BATTERY SOLUTIONS FOR HARSH WEATHER FROM SAFT TO VR GROUP

- 5.12.3 CASE STUDY 3: EMERGENCY BATTERY SYSTEM FROM SAFT TO CHENGDU METRO

- 5.12.4 CASE STUDY 4: LITHIUM-ION BATTERY SOLUTIONS FROM SAFT TO ALSTROM TRANSPORT FOR DIFFERENT WEATHER CONDITIONS AND HIGH-VIBRATING ENVIRONMENTS

- 5.12.5 CASE STUDY 5: DEVELOPMENT OF HYBRID TRAIN FOR NON-ELECTRIFIED SUBSECTIONS OF LINE

- 5.12.6 CASE STUDY 6: ELECTRIFICATION OF RAIL MILLING TRAINS FOR EMISSION-FREE TRACK MAINTENANCE

- 5.12.7 CASE STUDY 7: PARTNERSHIP BETWEEN HITACHI AND TURNTIDE TECHNOLOGIES TO PROVIDE MORE SUSTAINABLE RAIL JOURNEYS IN UK

- 5.13 KEY CONFERENCES AND EVENTS

- 5.13.1 TRAIN BATTERY MARKET: LIST OF CONFERENCES AND EVENTS, 2023-2024

- 5.14 BUYING CRITERIA

- FIGURE 32 KEY BUYING CRITERIA FOR NICKEL-CADMIUM VS. LITHIUM-ION BATTERIES

- TABLE 34 KEY BUYING CRITERIA FOR NICKEL-CADMIUM VS. LITHIUM-ION BATTERIES

- 5.15 BILL OF MATERIALS

- FIGURE 33 COMPARISON OF BILL OF MATERIALS OF LEAD-ACID AND NI-CD BATTERIES, 2023

6 TRAIN BATTERY MARKET, BY APPLICATION & BATTERY TYPE

- 6.1 INTRODUCTION

- 6.1.1 INDUSTRY INSIGHTS

- FIGURE 34 TRAIN BATTERY MARKET, BY APPLICATION, 2023 VS. 2030 (USD MILLION)

- TABLE 35 TRAIN BATTERY MARKET, BY APPLICATION, 2018-2022 (UNITS)

- TABLE 36 TRAIN BATTERY MARKET, BY APPLICATION, 2023-2030 (UNITS)

- TABLE 37 TRAIN BATTERY MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 38 TRAIN BATTERY MARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- 6.2 STARTER BATTERIES

- TABLE 39 STARTER BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 40 STARTER BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 41 STARTER BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 42 STARTER BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 6.2.1 LEAD-ACID BATTERIES

- 6.2.1.1 Easy transportation and value for cost to increase demand in rail sector

- TABLE 43 LEAD-ACID: STARTER BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 44 LEAD-ACID: STARTER BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 45 LEAD-ACID: STARTER BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 46 LEAD-ACID: STARTER BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.2.2 NI-CD BATTERIES

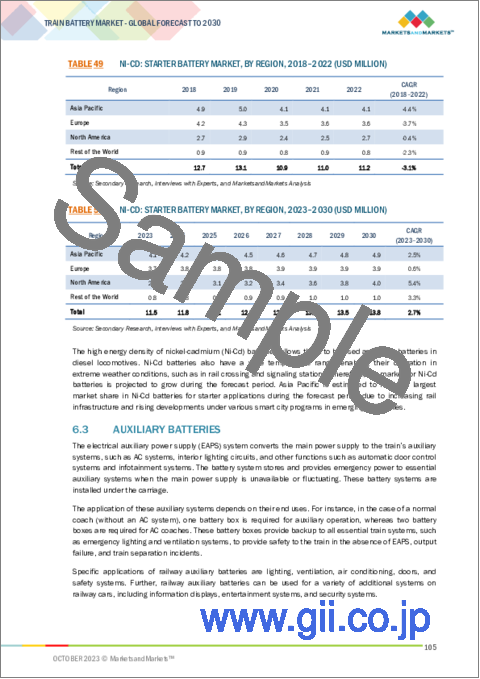

- 6.2.2.1 Uninterruptible power supply and high current supply for diesel starting motors to drive demand

- TABLE 47 NI-CD: STARTER BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 48 NI-CD: STARTER BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 49 NI-CD: STARTER BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 50 NI-CD: STARTER BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3 AUXILIARY BATTERIES

- TABLE 51 AUXILIARY BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 52 AUXILIARY BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 53 AUXILIARY BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 54 AUXILIARY BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 6.3.1 LEAD-ACID BATTERIES

- 6.3.1.1 Cost competitiveness and durability to increase demand in rail sector

- TABLE 55 LEAD-ACID: AUXILIARY BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 56 LEAD-ACID: AUXILIARY BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 57 LEAD-ACID: AUXILIARY BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 58 LEAD-ACID: AUXILIARY BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3.2 NI-CD BATTERIES

- 6.3.2.1 High energy density, longer lifespan, and ability to deliver high currents to increase market penetration

- TABLE 59 NI-CD: AUXILIARY BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 60 NI-CD: AUXILIARY BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 61 NI-CD: AUXILIARY BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 62 NI-CD: AUXILIARY BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 6.3.3 LITHIUM-ION BATTERIES

- 6.3.3.1 Fast charging time, longer lifespan, and high energy density to drive adoption in rolling stock

- TABLE 63 LITHIUM-ION: AUXILIARY BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 64 LITHIUM-ION: AUXILIARY BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 65 LITHIUM-ION: AUXILIARY BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 66 LITHIUM-ION: AUXILIARY BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

7 TRAIN BATTERY MARKET, BY BATTERY TYPE & BATTERY TECHNOLOGY

- 7.1 INTRODUCTION

- 7.1.1 INDUSTRY INSIGHTS

- FIGURE 35 TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023 VS. 2030 (USD MILLION)

- TABLE 67 TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 68 TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 69 TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 70 TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 7.2 LEAD-ACID BATTERIES

- TABLE 71 LEAD-ACID BATTERY MARKET, BY BATTERY TECHNOLOGY, 2018-2022 (UNITS)

- TABLE 72 LEAD-ACID BATTERY MARKET, BY BATTERY TECHNOLOGY, 2023-2030 (UNITS)

- 7.2.1 CONVENTIONAL LEAD-ACID BATTERIES

- 7.2.1.1 Growing popularity of VRLA batteries to impact demand for conventional lead-acid batteries

- TABLE 73 CONVENTIONAL LEAD-ACID BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 74 CONVENTIONAL LEAD-ACID BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- 7.2.2 VALVE-REGULATED LEAD-ACID BATTERIES

- 7.2.2.1 High reliability and low cost of ownership to drive market

- TABLE 75 VALVE-REGULATED LEAD-ACID BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 76 VALVE-REGULATED LEAD-ACID BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- 7.2.3 GEL TUBULAR LEAD-ACID BATTERIES

- 7.2.3.1 High current applications to increase demand

- TABLE 77 GEL TUBULAR LEAD-ACID BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 78 GEL TUBULAR LEAD-ACID BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- 7.3 NICKEL-CADMIUM BATTERIES

- TABLE 79 NICKEL-CADMIUM BATTERY MARKET, BY BATTERY TECHNOLOGY, 2018-2022 (UNITS)

- TABLE 80 NICKEL-CADMIUM BATTERY MARKET, BY BATTERY TECHNOLOGY, 2023-2030 (UNITS)

- 7.3.1 SINTER/PNE NICKEL-CADMIUM BATTERIES

- 7.3.1.1 Good chargeability and longer life cycle to drive demand

- TABLE 81 SINTER/PNE NICKEL-CADMIUM BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 82 SINTER/PNE NICKEL-CADMIUM BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- 7.3.2 POCKET PLATE NICKEL-CADMIUM BATTERIES

- 7.3.2.1 Lower energy density capacity and short lifetime to impact demand

- TABLE 83 POCKET PLATE NICKEL-CADMIUM BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 84 POCKET PLATE NICKEL-CADMIUM BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- 7.3.3 FIBER/PNE NICKEL-CADMIUM BATTERIES

- 7.3.3.1 Reduction in shortcomings of second-generation nickel-cadmium battery technology to drive demand

- TABLE 85 FIBER/PNE NICKEL-CADMIUM BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 86 FIBER/PNE NICKEL-CADMIUM BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- 7.4 LITHIUM-ION BATTERIES

- TABLE 87 LITHIUM-ION BATTERY MARKET, BY BATTERY TECHNOLOGY, 2018-2022 (UNITS)

- TABLE 88 LITHIUM-ION BATTERY MARKET, BY BATTERY TECHNOLOGY, 2023-2030 (UNITS)

- 7.4.1 LITHIUM IRON PHOSPHATE BATTERIES

- 7.4.1.1 Good chargeability and longer life cycle to drive demand

- TABLE 89 LITHIUM IRON PHOSPHATE BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 90 LITHIUM IRON PHOSPHATE BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- 7.4.2 LITHIUM TITANATE OXIDE BATTERIES

- 7.4.2.1 Fast charging capability to drive demand

- TABLE 91 LITHIUM TITANATE OXIDE BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 92 LITHIUM TITANATE OXIDE BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- 7.4.3 OTHERS

- TABLE 93 OTHER LITHIUM-ION BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 94 OTHER LITHIUM-ION BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

8 TRAIN BATTERY MARKET, BY ENGINE/HEAD

- 8.1 INTRODUCTION

- 8.1.1 INDUSTRY INSIGHTS

- FIGURE 36 TRAIN BATTERY MARKET, BY ENGINE/HEAD, 2023 VS. 2030 (USD MILLION)

- TABLE 95 TRAIN BATTERY MARKET, BY ENGINE/HEAD, 2018-2022 (UNITS)

- TABLE 96 TRAIN BATTERY MARKET, BY ENGINE/HEAD, 2023-2030 (UNITS)

- TABLE 97 TRAIN BATTERY MARKET, BY ENGINE/HEAD, 2018-2022 (USD MILLION)

- TABLE 98 TRAIN BATTERY MARKET, BY ENGINE/HEAD, 2023-2030 (USD MILLION)

- 8.2 DIESEL LOCOMOTIVES

- 8.2.1 DEVELOPMENT OF FREIGHT TRAINS AND RAIL NETWORKS IN EMERGING ECONOMIES TO DRIVE MARKET

- TABLE 99 DIESEL LOCOMOTIVES: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 100 DIESEL LOCOMOTIVES: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 101 DIESEL LOCOMOTIVES: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 102 DIESEL LOCOMOTIVES: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 8.3 DIESEL MULTIPLE UNITS

- 8.3.1 EXPANSION OF INTERCITY RAIL NETWORKS TO DRIVE MARKET

- TABLE 103 DIESEL MULTIPLE UNITS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 104 DIESEL MULTIPLE UNITS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 105 DIESEL MULTIPLE UNITS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 106 DIESEL MULTIPLE UNITS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 8.4 ELECTRIC LOCOMOTIVES

- 8.4.1 LOW MAINTENANCE COST AND HIGHER OPERATIONAL EFFICIENCY TO DRIVE MARKET

- TABLE 107 ELECTRIC LOCOMOTIVES: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 108 ELECTRIC LOCOMOTIVES: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 109 ELECTRIC LOCOMOTIVES: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 110 ELECTRIC LOCOMOTIVES: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 8.5 ELECTRIC MULTIPLE UNITS

- 8.5.1 ADVANCEMENTS IN LIGHTING SOLUTIONS, SAFETY DOORS, AND HVACS TO DRIVE MARKET

- TABLE 111 ELECTRIC MULTIPLE UNITS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 112 ELECTRIC MULTIPLE UNIT: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 113 ELECTRIC MULTIPLE UNITS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 114 ELECTRIC MULTIPLE UNITS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

9 TRAIN BATTERY MARKET, BY RAILWAY APPLICATION

- 9.1 INTRODUCTION

- 9.1.1 INDUSTRY INSIGHTS

- FIGURE 37 TRAIN BATTERY MARKET, BY RAILWAY APPLICATION, 2023 VS. 2030 (USD MILLION)

- TABLE 115 TRAIN BATTERY MARKET, BY RAILWAY APPLICATION, 2018-2022 (UNITS)

- TABLE 116 TRAIN BATTERY MARKET, BY RAILWAY APPLICATION, 2023-2030 (UNITS)

- TABLE 117 TRAIN BATTERY MARKET, BY RAILWAY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 118 TRAIN BATTERY MARKET, BY RAILWAY APPLICATION, 2023-2030 (USD MILLION)

- 9.2 METROS

- 9.2.1 EXPANSION OF URBAN RAIL NETWORK TO DRIVE DEMAND

- TABLE 119 METROS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 120 METROS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 121 METROS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 122 METROS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.3 HIGH-SPEED TRAINS

- 9.3.1 INFRASTRUCTURE DEVELOPMENT AND NEED FOR CHEAPER AND FASTER TRANSPORTATION MODES TO DRIVE DEMAND

- TABLE 123 HIGH-SPEED TRAINS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 124 HIGH-SPEED TRAINS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 125 HIGH-SPEED TRAINS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 126 HIGH-SPEED TRAINS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.4 LIGHT RAILS/TRAMS/MONORAILS

- 9.4.1 RAPID URBANIZATION AND AESTHETIC VALUE TO DRIVE DEMAND

- TABLE 127 LIGHT RAILS/TRAMS/MONORAILS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 128 LIGHT RAILS/TRAMS/MONORAILS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 129 LIGHT RAILS/TRAMS/MONORAILS: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 130 LIGHT RAILS/TRAMS/MONORAILS: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 9.5 PASSENGER COACHES

- 9.5.1 RAIL EXPANSION PROJECTS AND INCREASING NUMBER OF PASSENGERS TO DRIVE DEMAND

- TABLE 131 PASSENGER COACHES: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 132 PASSENGER COACHES: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 133 PASSENGER COACHES: TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 134 PASSENGER COACHES: TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

10 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE

- 10.1 INTRODUCTION

- 10.1.1 INDUSTRY INSIGHTS

- FIGURE 38 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE, 2023 VS. 2030 (USD MILLION)

- TABLE 135 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE, 2018-2022 (UNITS)

- TABLE 136 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE, 2023-2030 (UNITS)

- TABLE 137 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE, 2018-2022 (USD MILLION)

- TABLE 138 TRAIN BATTERY MARKET, BY ADVANCED TRAIN TYPE, 2023-2030 (USD MILLION)

- 10.2 HYBRID TRAINS

- 10.2.1 REDUCTION IN ENERGY CONSUMPTION AND REDUCED LIFECYCLE COST TO DRIVE DEMAND

- 10.2.2 OPERATIONAL DATA

- TABLE 139 HYBRID TRAINS WITH PROPULSION TYPE

- TABLE 140 HYBRID TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 141 HYBRID TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 142 HYBRID TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 143 HYBRID TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 10.3 FULLY BATTERY-OPERATED TRAINS

- 10.3.1 EXPANSION OF RAIL NETWORK AND HIGHER COST OF ELECTRIFICATION TO DRIVE DEMAND

- TABLE 144 FULLY BATTERY-OPERATED TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 145 FULLY BATTERY-OPERATED TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 146 FULLY BATTERY-OPERATED TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 147 FULLY BATTERY-OPERATED TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 10.4 AUTONOMOUS TRAINS

- 10.4.1 CONTINUOUS DEVELOPMENTS, LOW COST OF OPERATION, AND LOW ENERGY CONSUMPTION TO DRIVE DEMAND

11 TRAIN BATTERY MARKET, BY REGION

- 11.1 INTRODUCTION

- 11.1.1 INDUSTRY INSIGHTS

- FIGURE 39 TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- TABLE 148 TRAIN BATTERY MARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 149 TRAIN BATTERY MARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 150 TRAIN BATTERY MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 151 TRAIN BATTERY MARKET, BY REGION, 2023-2030 (USD MILLION)

- 11.2 ASIA PACIFIC

- 11.2.1 RECESSION IMPACT

- FIGURE 40 ASIA PACIFIC: TRAIN BATTERY MARKET SNAPSHOT

- TABLE 152 ASIA PACIFIC: TRAIN BATTERY MARKET, BY COUNTRY, 2018-2022 (UNITS)

- TABLE 153 ASIA PACIFIC: TRAIN BATTERY MARKET, BY COUNTRY, 2023-2030 (UNITS)

- TABLE 154 ASIA PACIFIC: TRAIN BATTERY MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 155 ASIA PACIFIC: TRAIN BATTERY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- 11.2.2 CHINA

- 11.2.2.1 Rail expansion projects to drive market

- TABLE 156 CHINA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 157 CHINA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 158 CHINA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 159 CHINA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.2.3 INDIA

- 11.2.3.1 Electrification of rail routes to drive market

- TABLE 160 LIST OF APPROVED UPCOMING HIGH-SPEED RAILWAY PROJECTS IN INDIA

- TABLE 161 INDIA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 162 INDIA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 163 INDIA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 164 INDIA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.2.4 JAPAN

- 11.2.4.1 Development of high-speed EMUs to drive market

- TABLE 165 JAPAN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 166 JAPAN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 167 JAPAN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 168 JAPAN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.2.5 SOUTH KOREA

- 11.2.5.1 Strong urban rail network and development of high-speed rail service to drive market

- TABLE 169 SOUTH KOREA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 170 SOUTH KOREA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 171 SOUTH KOREA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 172 SOUTH KOREA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.3 EUROPE

- 11.3.1 RECESSION IMPACT

- FIGURE 41 EUROPE: TRAIN BATTERY MARKET SNAPSHOT

- TABLE 173 EUROPE: TRAIN BATTERY MARKET, BY COUNTRY, 2018-2022 (UNITS)

- TABLE 174 EUROPE: TRAIN BATTERY MARKET, BY COUNTRY, 2023-2030 (UNITS)

- TABLE 175 EUROPE: TRAIN BATTERY MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 176 EUROPE: TRAIN BATTERY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- 11.3.2 GERMANY

- 11.3.2.1 Replacement of diesel locomotives with battery-operated trains to drive market

- TABLE 177 GERMANY: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 178 GERMANY: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 179 GERMANY: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 180 GERMANY: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.3.3 FRANCE

- 11.3.3.1 Stringent emission norms for locomotives to boost demand for train batteries

- TABLE 181 FRANCE: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 182 FRANCE: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 183 FRANCE: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 184 FRANCE: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.3.4 ITALY

- 11.3.4.1 Increasing demand for batteries for EMUs and light rails to drive market

- TABLE 185 ITALY: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 186 ITALY: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 187 ITALY: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 188 ITALY: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.3.5 UK

- 11.3.5.1 Urban rail developments to drive market

- TABLE 189 UK: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 190 UK: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 191 UK: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 192 UK: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.3.6 SPAIN

- 11.3.6.1 Investment in high-speed rail networks to drive market

- TABLE 193 SPAIN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 194 SPAIN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 195 SPAIN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 196 SPAIN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.3.7 SWITZERLAND

- 11.3.7.1 Growing development of passenger trains to drive demand for batteries

- TABLE 197 SWITZERLAND: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 198 SWITZERLAND: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 199 SWITZERLAND: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 200 SWITZERLAND: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.3.8 POLAND

- 11.3.8.1 Development of intercity trains to drive demand for batteries

- TABLE 201 POLAND: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 202 POLAND: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 203 POLAND: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 204 POLAND: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.3.9 SWEDEN

- 11.3.9.1 Rising demand for regional trains to drive market

- TABLE 205 SWEDEN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 206 SWEDEN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 207 SWEDEN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 208 SWEDEN: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.4 NORTH AMERICA

- 11.4.1 RECESSION IMPACT

- FIGURE 42 NORTH AMERICA: TRAIN BATTERY MARKET SNAPSHOT

- TABLE 209 NORTH AMERICA: TRAIN BATTERY MARKET, BY COUNTRY, 2018-2022 (UNITS)

- TABLE 210 NORTH AMERICA: TRAIN BATTERY MARKET, BY COUNTRY, 2023-2030 (UNITS)

- TABLE 211 NORTH AMERICA: TRAIN BATTERY MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 212 NORTH AMERICA: TRAIN BATTERY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- 11.4.2 US

- 11.4.2.1 Rising diesel prices to drive market

- TABLE 213 US: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 214 US: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 215 US: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 216 US: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.4.3 CANADA

- 11.4.3.1 Development of commuter trains like metros and passenger rails to drive demand for batteries

- TABLE 217 CANADA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 218 CANADA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 219 CANADA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 220 CANADA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.4.4 MEXICO

- 11.4.4.1 Growing development of catenary-free rail tracks to drive market

- TABLE 221 MEXICO: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 222 MEXICO: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 223 MEXICO: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 224 MEXICO: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.5 REST OF THE WORLD

- 11.5.1 RECESSION IMPACT

- FIGURE 43 REST OF THE WORLD: TRAIN BATTERY MARKET, 2023 VS. 2030 (USD MILLION)

- TABLE 225 REST OF THE WORLD: TRAIN BATTERY MARKET, BY COUNTRY, 2018-2022 (UNITS)

- TABLE 226 REST OF THE WORLD: TRAIN BATTERY MARKET, BY COUNTRY, 2023-2030 (UNITS)

- TABLE 227 REST OF THE WORLD: TRAIN BATTERY MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 228 REST OF THE WORLD: TRAIN BATTERY MARKET, BY COUNTRY, 2023-2030 (USD MILLION)

- 11.5.2 BRAZIL

- 11.5.2.1 Growing demand for auxiliary function batteries to drive market

- TABLE 229 BRAZIL: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 230 BRAZIL: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 231 BRAZIL: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 232 BRAZIL: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 11.5.3 RUSSIA

- 11.5.3.1 Increasing demand for wide temperature-range rail batteries to drive market

- TABLE 233 RUSSIA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 234 RUSSIA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 235 RUSSIA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 236 RUSSIA: TRAIN BATTERY MARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

12 TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK

- 12.1 INTRODUCTION

- 12.1.1 INDUSTRY INSIGHTS

- FIGURE 44 TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK, 2023 VS. 2030 (USD MILLION)

- TABLE 237 TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK, 2018-2022 (UNITS)

- TABLE 238 TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK, 2023-2030 (UNITS)

- TABLE 239 TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK, 2018-2022 (USD MILLION)

- TABLE 240 TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK, 2023-2030 (USD MILLION)

- 12.2 LOCOMOTIVES

- 12.2.1 IMPROVED LIFE CYCLE OF LOCOMOTIVES TO DRIVE DEMAND FOR TRAIN BATTERIES

- TABLE 241 LOCOMOTIVES: TRAIN BATTERY AFTERMARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 242 LOCOMOTIVES: TRAIN BATTERY AFTERMARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 243 LOCOMOTIVES: TRAIN BATTERY AFTERMARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 244 LOCOMOTIVES: TRAIN BATTERY AFTERMARKET, BY REGION, 2023-2030 (USD MILLION)

- 12.3 MULTIPLE UNITS

- 12.3.1 ADVANCED FEATURES IN URBAN TRANSIT SYSTEMS TO INCREASE TRAIN BATTERY ADOPTION IN MULTIPLE UNITS

- TABLE 245 MULTIPLE UNITS: TRAIN BATTERY AFTERMARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 246 MULTIPLE UNITS: TRAIN BATTERY AFTERMARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 247 MULTIPLE UNITS: TRAIN BATTERY AFTERMARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 248 MULTIPLE UNITS: TRAIN BATTERY AFTERMARKET, BY REGION, 2023-2030 (USD MILLION)

- 12.4 PASSENGER COACHES

- 12.4.1 REFURBISHMENT PROJECTS TO EXTEND OPERATIONAL LIFE OF PASSENGER COACHES TO BOOST DEMAND

- TABLE 249 PASSENGER COACHES: TRAIN BATTERY AFTERMARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 250 PASSENGER COACHES: TRAIN BATTERY AFTERMARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 251 PASSENGER COACHES: TRAIN BATTERY AFTERMARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 252 PASSENGER COACHES: TRAIN BATTERY AFTERMARKET, BY REGION, 2023-2030 (USD MILLION)

13 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE

- 13.1 INTRODUCTION

- 13.1.1 INDUSTRY INSIGHTS

- FIGURE 45 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE, 2023 VS. 2030 (USD MILLION)

- TABLE 253 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE, 2018-2022 (UNITS)

- TABLE 254 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE, 2023-2030 (UNITS)

- TABLE 255 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE, 2018-2022 (USD MILLION)

- TABLE 256 TRAIN BATTERY AFTERMARKET, BY BATTERY TYPE, 2023-2030 (USD MILLION)

- 13.2 LEAD-ACID BATTERIES

- 13.2.1 FREQUENT REPLACEMENT RATE AND LOW CYCLE LIFE TO DRIVE DEMAND

- TABLE 257 LEAD-ACID BATTERY AFTERMARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 258 LEAD-ACID BATTERY AFTERMARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 259 LEAD-ACID BATTERY AFTERMARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 260 LEAD-ACID BATTERY AFTERMARKET, BY REGION, 2023-2030 (USD MILLION)

- 13.3 NICKEL-CADMIUM BATTERIES

- 13.3.1 LONGER LIFE AND EASY MAINTENANCE TO BOOST MARKET SHARE

- TABLE 261 NICKEL-CADMIUM BATTERY AFTERMARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 262 NICKEL-CADMIUM BATTERY AFTERMARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 263 NICKEL-CADMIUM BATTERY AFTERMARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 264 NICKEL-CADMIUM BATTERY AFTERMARKET, BY REGION, 2023-2030 (USD MILLION)

14 TRAIN BATTERY AFTERMARKET, BY APPLICATION

- 14.1 INTRODUCTION

- 14.1.1 INDUSTRY INSIGHTS

- FIGURE 46 TRAIN BATTERY AFTERMARKET, BY APPLICATION, 2023 VS. 2030 (USD MILLION)

- TABLE 265 TRAIN BATTERY AFTERMARKET, BY APPLICATION, 2018-2022 (UNITS)

- TABLE 266 TRAIN BATTERY AFTERMARKET, BY APPLICATION, 2023-2030 (UNITS)

- TABLE 267 TRAIN BATTERY AFTERMARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 268 TRAIN BATTERY AFTERMARKET, BY APPLICATION, 2023-2030 (USD MILLION)

- 14.2 STARTER BATTERIES

- 14.2.1 REQUIREMENT FOR REPLACEMENT BATTERIES IN DMUS AND DIESEL LOCOMOTIVES TO DRIVE DEMAND

- TABLE 269 STARTER BATTERY AFTERMARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 270 STARTER BATTERY AFTERMARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 271 STARTER BATTERY AFTERMARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 272 STARTER BATTERY AFTERMARKET, BY REGION, 2023-2030 (USD MILLION)

- 14.3 AUXILIARY BATTERIES

- 14.3.1 GROWING POWER REQUIREMENT FOR ONBOARD ELECTRIC SYSTEMS TO RAISE DEMAND

- TABLE 273 AUXILIARY BATTERY AFTERMARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 274 AUXILIARY BATTERY AFTERMARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 275 AUXILIARY BATTERY AFTERMARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 276 AUXILIARY BATTERY AFTERMARKET, BY REGION, 2023-2030 (USD MILLION)

15 TRAIN BATTERY AFTERMARKET, BY REGION

- 15.1 INTRODUCTION

- 15.1.1 INDUSTRY INSIGHTS

- FIGURE 47 TRAIN BATTERY AFTERMARKET, BY REGION, 2023 VS. 2030 (USD MILLION)

- TABLE 277 TRAIN BATTERY AFTERMARKET, BY REGION, 2018-2022 (UNITS)

- TABLE 278 TRAIN BATTERY AFTERMARKET, BY REGION, 2023-2030 (UNITS)

- TABLE 279 TRAIN BATTERY AFTERMARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 280 TRAIN BATTERY AFTERMARKET, BY REGION, 2023-2030 (USD MILLION)

- 15.2 ASIA PACIFIC

- 15.2.1 HIGH NUMBER OF ROLLING STOCKS TO DRIVE REPLACEMENT DEMAND

- 15.3 EUROPE

- 15.3.1 EXPANSION OF INTERCITY RAIL NETWORKS TO DRIVE DEMAND

- 15.4 NORTH AMERICA

- 15.4.1 GROWING DIESEL LOCOMOTIVE RETROFITTING AND REFURBISHMENT TO DRIVE DEMAND

16 COMPETITIVE LANDSCAPE

- 16.1 OVERVIEW

- 16.2 MARKET SHARE ANALYSIS, 2022

- TABLE 281 TRAIN BATTERY MARKET SHARE ANALYSIS, 2022

- 16.3 TRAIN BATTERY MARKET SHARE ANALYSIS, 2022

- FIGURE 48 TRAIN BATTERY MARKET SHARE ANALYSIS, 2022

- 16.4 REVENUE ANALYSIS OF TOP LISTED/PUBLIC PLAYERS

- FIGURE 49 REVENUE ANALYSIS OF TOP 5 MARKET PLAYERS, 2020-2022

- 16.5 COMPANY EVALUATION MATRIX

- 16.5.1 STARS

- 16.5.2 EMERGING LEADERS

- 16.5.3 PERVASIVE PLAYERS

- 16.5.4 PARTICIPANTS

- FIGURE 50 COMPANY EVALUATION MATRIX: TRAIN BATTERY MANUFACTURERS, 2022

- 16.5.5 COMPANY FOOTPRINT

- TABLE 282 TRAIN BATTERY MARKET: COMPANY PRODUCT FOOTPRINT, 2022

- TABLE 283 TRAIN BATTERY MARKET: COMPANY APPLICATION FOOTPRINT, 2022

- TABLE 284 TRAIN BATTERY MARKET: COMPANY REGION FOOTPRINT, 2022

- 16.6 COMPANY EVALUATION MATRIX - BATTERY MANUFACTURERS FOR FULLY BATTERY-OPERATED TRAINS

- 16.6.1 STARS

- 16.6.2 EMERGING LEADERS

- 16.6.3 PERVASIVE PLAYERS

- 16.6.4 PARTICIPANTS

- FIGURE 51 COMPANY EVALUATION MATRIX: BATTERY MANUFACTURERS FOR FULLY BATTERY-OPERATED TRAINS, 2022

- 16.6.5 COMPANY FOOTPRINT

- TABLE 285 COMPANY PRODUCT FOOTPRINT, 2022

- TABLE 286 COMPANY APPLICATION FOOTPRINT, 2022

- TABLE 287 COMPANY REGION FOOTPRINT, 2022

- 16.7 COMPETITIVE SCENARIO

- 16.7.1 PRODUCT LAUNCHES

- TABLE 288 PRODUCT LAUNCHES, 2018-2023

- 16.7.2 DEALS

- TABLE 289 DEALS, 2018-2023

- 16.7.3 OTHERS

- TABLE 290 OTHERS, 2018-2023

- 16.8 KEY PLAYER STRATEGIES/RIGHT TO WIN, 2018-2022

- TABLE 291 COMPANIES ADOPTED PRODUCT DEVELOPMENTS AND EXPANSIONS AS KEY GROWTH STRATEGIES, 2018-2022

- 16.9 MAJOR BATTERY SUPPLIERS - CURRENT PRODUCT OFFERINGS AND FUTURE PRODUCT PLANS

- TABLE 292 CURRENT VS. FUTURE PRODUCT PLANS

17 COMPANY PROFILES

- 17.1 KEY PLAYERS

- (Business Overview, Products/Services/Solutions Offered, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats, Recent Developments)**

- 17.1.1 ENERSYS

- TABLE 293 ENERSYS: COMPANY OVERVIEW

- FIGURE 52 ENERSYS: COMPANY SNAPSHOT

- TABLE 294 ENERSYS: PRODUCT LAUNCHES

- TABLE 295 ENERSYS: DEALS

- 17.1.2 SAFT

- TABLE 296 SAFT: COMPANY OVERVIEW

- TABLE 297 SAFT: DEALS

- TABLE 298 SAFT: OTHERS

- 17.1.3 GS YUASA INTERNATIONAL LTD.

- TABLE 299 GS YUASA INTERNATIONAL LTD.: COMPANY OVERVIEW

- FIGURE 53 GS YUASA INTERNATIONAL LTD.: COMPANY SNAPSHOT

- TABLE 300 GS YUASA INTERNATIONAL LTD.: PRODUCT LAUNCHES

- TABLE 301 GS YUASA INTERNATIONAL LTD.: OTHERS

- 17.1.4 EXIDE INDUSTRIES LTD.

- TABLE 302 EXIDE INDUSTRIES LTD.: COMPANY OVERVIEW

- FIGURE 54 EXIDE INDUSTRIES LTD.: COMPANY SNAPSHOT

- TABLE 303 EXIDE INDUSTRIES LTD.: DEALS

- TABLE 304 EXIDE INDUSTRIES LTD.: OTHERS

- 17.1.5 AMARA RAJA BATTERIES LIMITED

- TABLE 305 AMARA RAJA BATTERIES LIMITED: COMPANY OVERVIEW

- FIGURE 55 AMARA RAJA BATTERIES LIMITED: COMPANY SNAPSHOT

- TABLE 306 AMARA RAJA BATTERIES LIMITED: DEALS

- TABLE 307 AMARA RAJA BATTERIES LIMITED: OTHERS

- 17.1.6 HOPPECKE BATTERIEN GMBH & CO. KG

- TABLE 308 HOPPECKE BATTERIEN GMBH & CO. KG: COMPANY OVERVIEW

- TABLE 309 HOPPECKE BATTERIEN GMBH & CO. KG: DEALS

- TABLE 310 HOPPECKE BATTERIEN GMBH & CO. KG: OTHERS

- 17.1.7 SEC BATTERY

- TABLE 311 SEC BATTERY: COMPANY OVERVIEW

- 17.1.8 FIRST NATIONAL BATTERY

- TABLE 312 FIRST NATIONAL BATTERY: COMPANY OVERVIEW

- 17.1.9 POWER & INDUSTRIAL BATTERY SYSTEMS GMBH

- TABLE 313 POWER & INDUSTRIAL BATTERY SYSTEMS GMBH: COMPANY OVERVIEW

- 17.1.10 EXIDE TECHNOLOGIES

- TABLE 314 EXIDE TECHNOLOGIES: COMPANY OVERVIEW

- 17.1.11 TOSHIBA CORPORATION

- TABLE 315 TOSHIBA CORPORATION: COMPANY OVERVIEW

- FIGURE 56 TOSHIBA CORPORATION: COMPANY SNAPSHOT

- TABLE 316 TOSHIBA CORPORATION: PRODUCT LAUNCHES

- TABLE 317 TOSHIBA CORPORATION: DEALS

- TABLE 318 TOSHIBA CORPORATION: OTHERS

- *Business Overview, Products/Services/Solutions Offered, MnM View, Key Strengths and Right to Win, Strategic Choices Made, Weaknesses and Competitive Threats, Recent Developments might not be captured in case of unlisted companies.

- 17.2 OTHER PLAYERS

- 17.2.1 EAST PENN MANUFACTURING COMPANY

- TABLE 319 EAST PENN MANUFACTURING COMPANY: COMPANY OVERVIEW

- 17.2.2 MICROTEX ENERGY PRIVATE LIMITED

- TABLE 320 MICROTEX ENERGY PRIVATE LIMITED: COMPANY OVERVIEW

- 17.2.3 AEG POWER SOLUTIONS

- TABLE 321 AEG POWER SOLUTIONS: COMPANY OVERVIEW

- 17.2.4 FURUKAWA ELECTRIC CO., LTD.

- TABLE 322 FURUKAWA ELECTRIC CO., LTD.: COMPANY OVERVIEW

- 17.2.5 HUNAN FENGRI POWER & ELECTRIC CO., LTD.

- TABLE 323 HUNAN FENGRI POWER & ELECTRIC CO., LTD.: COMPANY OVERVIEW

- 17.2.6 SHUANGDENG GROUP CO., LTD.

- TABLE 324 SHUANGDENG GROUP CO., LTD.: COMPANY OVERVIEW

- 17.2.7 COSLIGHT INDIA

- TABLE 325 COSLIGHT INDIA: COMPANY OVERVIEW

- 17.2.8 SHIELD BATTERIES LIMITED

- TABLE 326 SHIELD BATTERIES LIMITED: COMPANY OVERVIEW

- 17.2.9 AKASOL AG

- TABLE 327 AKASOL AG: COMPANY OVERVIEW

- 17.2.10 DMS TECHNOLOGIES

- TABLE 328 DMS TECHNOLOGIES: COMPANY OVERVIEW

- 17.2.11 NATIONAL RAILWAY SUPPLY

- TABLE 329 NATIONAL RAILWAY SUPPLY: COMPANY OVERVIEW

- 17.2.12 LECLANCHE SA

- TABLE 330 LECLANCHE SA: COMPANY OVERVIEW

- 17.2.13 ECOBAT

- TABLE 331 ECOBAT: COMPANY OVERVIEW

- 17.2.14 HBL BATTERIES

- TABLE 332 HBL BATTERIES: COMPANY OVERVIEW

- 17.2.15 STAR BATTERY LTD.

- TABLE 333 STAR BATTERY LTD.: COMPANY OVERVIEW

- 17.2.16 HITACHI, LTD.

- TABLE 334 HITACHI, LTD.: COMPANY OVERVIEW

18 RECOMMENDATIONS FROM MARKETSANDMARKETS

- 18.1 ASIA PACIFIC: POTENTIAL MARKET FOR TRAIN BATTERY MANUFACTURERS TO FOCUS ON

- 18.2 COST-EFFECTIVE BATTERY TECHNOLOGIES WITH HIGH ENERGY DENSITY: NEED OF FUTURE

- 18.3 CONCLUSION

19 APPENDIX

- 19.1 INSIGHTS FROM INDUSTRY EXPERTS

- 19.2 DISCUSSION GUIDE

- 19.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 19.4 CUSTOMIZATION OPTIONS

- 19.4.1 TRAIN BATTERY MARKET, BY APPLICATION AND ROLLING STOCK

- 19.4.1.1 Engine Starters

- 19.4.1.2 Auxiliary Functions

- 19.4.2 TRAIN BATTERY MARKET, BY ROLLING STOCK AND BY BATTERY TYPE

- 19.4.2.1 Lead-acid

- 19.4.2.2 Nickel-Cadmium

- 19.4.2.3 Lithium-ion

- 19.4.3 US TRAIN BATTERY AFTERMARKET, BY ROLLING STOCK

- 19.4.3.1 Locomotives

- 19.4.3.2 Multiple Units

- 19.4.3.3 Passenger Coaches

- 19.4.1 TRAIN BATTERY MARKET, BY APPLICATION AND ROLLING STOCK

- 19.5 RELATED REPORTS

- 19.6 AUTHOR DETAILS