|

|

市場調査レポート

商品コード

1355383

防衛における5Gの世界市場:プラットフォーム別、ソリューション別、エンドユーザー別、ネットワークタイプ別、運用周波数別、設置別、地域別 - 2028年までの予測5G in Defense Market by Platform (Land, Naval, Airborne), Solution (Communication Network,Chipset, Core Network), End User, Network Type, Installation and Region (North America, Europe, Asia Pacific, LA, MEA) - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 防衛における5Gの世界市場:プラットフォーム別、ソリューション別、エンドユーザー別、ネットワークタイプ別、運用周波数別、設置別、地域別 - 2028年までの予測 |

|

出版日: 2023年09月22日

発行: MarketsandMarkets

ページ情報: 英文 250 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

防衛における5Gの市場規模は、2023年に9億米ドル、2028年には23億米ドルになると予測されており、2023年から2028年までのCAGRは19.9%と見込まれています。

多くの要因により、世界の防衛における5G市場は大きく拡大しています。

5Gとして知られる第5世代の携帯電話ネットワークは、通信技術の大幅な進歩を意味します。その前身である4Gの最大100倍の速度を提供し、個人にも企業にも前例のない可能性を開く。5Gが提供する強化された接続速度、驚くほど低い待ち時間、拡大された帯域幅は、社会の進歩を促進し、様々な産業を再構築しています。この変革は、人々の日常体験を大きく向上させています。

市場の成長は、コマンド、制御、通信、コンピュータ、インテリジェンス、監視、偵察(C4ISR)システム、無人機(UAV)、無人地上車両(UGV)、自律型艦艇を含む無人システムとのより信頼性の高い迅速な通信を改善することができる低遅延ネットワークに対する需要の高まりによって牽引されています。より速いデータ速度とより低いレイテンシは、訓練シミュレーションや戦場でのデータ可視化のためのARやVRをサポートすることができます。

「プラットフォーム別では、2023年の市場規模において陸上が最大となります。5Gスペクトラムのミリ波は、高周波で波長が短いことが特徴で、軍事基地や司令部など高度なセキュリティが必要なエリアでのリアルタイム通信を容易にすることができます。逆に、低周波で波長の長いスペクトラムは、長距離通信のニーズに活用できます。防衛分野における陸上5G市場の成長を促進する要因には、安全で信頼性の高い通信に対する需要の増加、無人化の進展、世界的網羅の必要性、新技術の開発などがあります。

通信ネットワークの成長によるスモールセル分野は、さまざまな経済圏で可処分所得が増加し、高データレートの消費が増加していることに起因しています。また、スモールセルは高帯域にわたって信号放送を強化し、信号性能を高める。例えば、屋外アンテナからの5Gミッドバンド信号は、屋内では一貫した信頼性を提供できない可能性があります。戦略的に配置されたスモールセルを使用することで、信号の信頼性と性能を大幅に向上させることができます。

当レポートでは、世界の防衛における5G市場について調査し、プラットフォーム別、ソリューション別、エンドユーザー別、ネットワークタイプ別、運用周波数別、設置別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 顧客のビジネスに影響を与える動向と混乱

- 景気後退の影響分析

- エコシステム分析

- 技術分析

- 価格分析

- バリューチェーン分析

- ケーススタディ分析

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- 関税と規制状況

- 2023年~2024年の主要な会議とイベント

第6章 業界の動向

- イントロダクション

- 防衛における5G市場の主要な技術動向

- メガトレンドの影響

- イノベーションと特許登録

第7章 防衛における5G市場、ソリューション別

- イントロダクション

- 通信ネットワーク

- チップセット

- コアネットワーク

第8章 防衛における5G市場、プラットフォーム別

- イントロダクション

- 陸

- 海

- 空中

第9章 防衛における5G市場、エンドユーザー別

- イントロダクション

- 軍隊

- 国土安全保障

第10章 防衛における5G市場、ネットワークタイプ別

- イントロダクション

- 強化モバイルブロードバンド

- 超信頼性の低遅延通信

- 大規模マシンタイプの通信

第11章 防衛における5G市場、運用周波数別

- イントロダクション

- 低

- 中

- 高

第12章 防衛における5G市場、設置別

- イントロダクション

- アップグレード

- 新たな実装

第13章 防衛における5G市場、地域別

- イントロダクション

- 地域不況の影響分析

- 北米

- 欧州

- アジア太平洋

- 中東・アフリカ

- ラテンアメリカ

第14章 競合情勢

- イントロダクション

- 会社概要

- 市場ランキング分析、2022年

- 主要な市場参入企業の収益分析、2020年~2022年

- 市場シェア分析、2022年

- 企業評価マトリックス

- 新興企業/中小企業の評価マトリックス

- 競合ベンチマーキング

- 競合シナリオ

第15章 企業プロファイル

- イントロダクション

- 主要参入企業

- ERICSSON

- NOKIA

- NEC CORPORATION

- SAMSUNG ELECTRONICS CO., LTD.

- HUAWEI

- THALES GROUP

- RAYTHEON TECHNOLOGIES CORPORATION

- INTELSAT

- QUALCOMM, INC.

- CISCO SYSTEMS, INC.

- VERIZON COMMUNICATIONS, INC.

- DEUTSCHE TELEKOM AG

- ORANGE S.A.

- GOGO, INC.

- LIGADO NETWORKS

- WIND RIVER SYSTEMS, INC.

- ANALOG DEVICES, INC.

- INTEL CORPORATION

- L3HARRIS TECHNOLOGIES, INC.

- その他の企業

- COMBA TELECOM

- STERLITE TECHNOLOGIES LTD.

- T-MOBILE US, INC.

- TELECOM ITALIA

- MARVELL

- MEDIATEK INC.

第16章 付録

The 5G in Defense market is estimated to be USD 0.9 Billion in 2023 to USD 2.3 billion by 2028, at a CAGR of 19.9% from 2023 to 2028. Due to a number of factors, the global market for 5G in defense are expanding significantly.

The fifth generation of cellular networks, known as 5G, represents a significant advancement in telecommunications technology. It offers speeds up to 100 times faster than its predecessor, 4G, opening up unprecedented possibilities for individuals and enterprises alike. The enhanced connectivity speeds, remarkably low latency, and expanded bandwidth that 5G provides are driving progress in societies and reshaping various industries. This transformation is greatly improving everyday experiences for people.

The growth of the market is being driven by the increasing demand for low latency networks which can improve command, control, communications, computers, intelligence, surveillance, and reconnaissance (C4ISR) systems, more reliable and quicker communication with unmanned systems, including drones (UAVs), unmanned ground vehicles (UGVs), and autonomous naval vessels. Faster data speeds and lower latency can support AR and VR applications for training simulations and on-the-battlefield data visualization.

"Land Segment: The largest share of the 5G in Defense Market by platform in 2023." Based on Platform, the 5G in Defense Market has been segmented into Land, Naval, and Airborne. Land shares the largest market value in 2023. The 5G spectrum's millimeter-wave, characterized by its high frequency and short wavelength, can facilitate real-time communication in areas requiring heightened security, such as military bases and command posts. Conversely, the low-frequency, long-wavelength spectrum can be harnessed for long-range communication needs. There are a number of factors driving the growth of the land 5G in Defense Market, including: The increasing demand for secure and reliable communications, growing use of unmanned, need for global coverage, development of new technologies etc. The land 5G in Defense Market's growth is a reflection of the evolving strategic, operational, and technological landscapes of modern ground warfare. As the nature of conflicts and technological paradigms shift, so too will the requirements and solutions in the land 5G technology sector.

" Communication Infrastructure: The largest segment of the 5G in Defense Market by solution in 2023"

Small cell segment from communication network growth is attributed to the rise in disposable income across different economies, coupled with increased consumption of high data rates.Also, small cells enhance signal broadcasting across the high band, boosting signal performance. For instance, 5G mid-band signals from an outdoor antenna may not offer consistent reliability indoors. By using small cells positioned strategically, the signal's reliability and performance can be significantly improved.

" Ultra-reliable and low-latency communications (URLLC): The Second largest share of the 5G in Defense Market by network type segment in 2023."

Ultra-reliable and low-latency communications (URLLC) is a service category supported by 5G in defense, which offers significant advantages for various industries and applications. By leveraging satellite-based networks, URLLC can provide ultra-reliable connectivity, free from terrestrial interference, ensuring critical applications remain consistently available. 5G in defense enables low-latency connectivity, crucial for applications where even minimal delays can have a substantial impact. For instance, industrial automation can benefit from this technology by enhancing efficiency and productivity through real-time communication among sensors and actuators. Similarly, autonomous vehicles can operate safely and efficiently by leveraging 5G in defense to enable seamless and instantaneous communication between vehicles and surrounding infrastructure. These examples highlight the transformative potential of 5G in defense in enabling a wide range of innovative URLLC applications.

The largest segment of the 5G in Defense Market by end user in 2023: Military

The Military segment of the 5G in defense market has a lot of applications such as: The low latency of 5G is crucial for the operation of drones (UAVs), unmanned ground vehicles (UGVs), and other robotic systems. These systems can be used for surveillance, bomb disposal, and even combat. 5G can support the streaming of high-definition video feeds from reconnaissance platforms, providing timely intelligence and a comprehensive view of the battlefield. Real-time data flow powered by 5G can significantly improve situational awareness and decision-making, allowing commanders to react swiftly to changing battle conditions. With 5G, soldiers can be equipped with wearable devices that monitor vital signs, location, or environmental conditions, transmitting data in real-time to medical or command centers.

" Medium Operational Frequency: The largest share of the 5G in Defense Market by operational frequency segment in 2023." Based on operational frequency segment, the 5G in Defense Market has been segmented into low, medium and high. Based on the numbers, medium operational frequency secured the largest market share in their usage. Mid-band 5G operates in the frequency range of 1.7GHz to 2.5GHz. It provides an optimal combination of both speed and coverage, delivering connectivity over extensive areas with speeds between 100 to 900 Mbps. The mid-band 5G is particularly beneficial for applications such as enhanced mobile broadband (eMBB) and Ultra Reliable Low Latency Communications, as well as for autonomous vehicles. Additionally, it supports sectors like media and entertainment, healthcare, smart urban planning, and intelligent agriculture.

" New Implementation Segment: The segment to grow by fastest CAGR in the forecasted period of the 5G in Defense Market by Installation "

The new implementation market refers to an independent 5G network market. The new implementation of 5G includes both New Radio and Core. This network provides an end-to-end 5G experience to users. The network can interoperate with the existing 4G or LTE network to provide service continuity between the two network generations. 5G Core uses a cloud-aligned service-based architecture (SBA) that supports control plane function interaction, reusability, flexible connections, and service discovery that spans all functions.

The deployment of the new implementation architecture network can be capital intensive. It includes all use cases, including eMBB and those dependent on URLLC and mMTC. With the operating data rate of 20 Gbps or 10Gbps, it has a latency of 1 ms (comparatively lower than NSA) and a network density of 1 million devices/km2.

"Japan to account for the largest CAGR in the 5G in Defense Market in forecasted year."

The Japanese government has been proactive in formulating policies and strategies to ensure the rapid deployment of 5G networks. The Ministry of Internal Affairs and Communications (MIC) has played a significant role in setting guidelines and spectrum allocations for 5G. In April 2022, the Japanese government established an ambitious 5G target aiming to provide 5G network coverage to 99% of its populace by the fiscal year ending 2030. This initiative is primarily overseen by the Ministry of Internal Affairs and Communications (MIC). Back in 2019, MIC granted 5G spectrum access to leading telecommunication entities, namely NTT Docomo, KDDI au, SoftBank, and the newer entrant, Rakuten Mobile, paving the way for them to develop 5G infrastructures. By March 2021, all these carriers had commenced commercial 5G services across every prefecture in Japan. As of 2022, over 20,000 mmWave gNodeBs have been deployed by these four primary service providers. Furthermore, there's a commitment to install additional nodes as per the obligations set by the MIC, with a targeted completion by early 2024. This pact emphasizes collaboration in 5G technology, artificial intelligence, and a spectrum of other vital domains. Both strategic allies have resolved to expand their partnership, placing emphasis on advancing the supply chain initiative within the Indo-Pacific zone.

Break-up of profiles of primary participants in the 5G in Defense Market: * By Company Type: Tier 1-55%; Tier 2-20%; and Tier 3-25%

- By Designation: C Level-75%; Manager Level-25%;

- By Region: North America-20%; Europe-25%; Asia Pacific-30%; Latin America-15%, MEA-10% Prominent companies in the 5G in defense Market are Ericsson (Sweden), Huawei (China), Nokia Networks (Finland), Samsung Electronics Co Ltd. (South Korea), NEC (Japan), Thales Group (France), L3Harris Technologies, Inc. (US), Raytheon Technologies (US), Ligado Networks (US), and Wind River Systems, Inc. (US). Research Coverage: The market study covers the 5G in Defense market across segments. It aims at estimating the market size and the growth potential of this market across different segments, such as platform, solution, end user, installation, operational frequency, network type and region. The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to product and business offerings, recent developments, and key market strategies. Key benefits of buying this report: This report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall 5G in defense market and its subsegments. The report covers the entire ecosystem of the 5G in defense industry and will help stakeholders understand the competitive landscape and gain more insights to better position their businesses and plan suitable go-to-market strategies. The report will also help stakeholders understand the pulse of the market and provide them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

- Analysis of key drivers (Use of 5G in situational awareness operations, rise in technological innovations in 5G, growing use ofth of autonomous and connected devices, transitioning from legacy systems to cloud-based solutions, increasing demand for high-speed and, low-latency connectivity), restraints (High investments in early phases and Lack of established protocols and standards) , opportunities(Rise in virtual networking architecture), challenges(Security concerns on collaboration with 5G suppliers) and there are several factors that could influence the growth of the 5G in Defense Market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the 5G in Defense Market.

- Market Development: Comprehensive information about lucrative markets - the report analyses of the 5G in Defense Market across varied regions

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the 5G in Defense Market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies and service offerings of leading players like Ericsson (Sweden), Huawei (China), Nokia Networks (Finland), Samsung Electronics Co Ltd. (South Korea), NEC (Japan), Thales Group (France), L3Harris Technologies, Inc. (US), Raytheon Technologies (US), Ligado Networks (US), and Wind River Systems, Inc. (US)..

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 5G IN DEFENSE MARKET SEGMENTATION

- 1.3.2 REGIONAL SCOPE

- 1.3.3 YEARS CONSIDERED

- 1.4 INCLUSIONS AND EXCLUSIONS

- TABLE 1 INCLUSIONS AND EXCLUSIONS IN 5G IN DEFENSE MARKET

- 1.5 CURRENCY CONSIDERED

- TABLE 2 USD EXCHANGE RATES

- 1.6 STUDY LIMITATIONS

- 1.7 MARKET STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.9 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 RESEARCH FLOW

- FIGURE 3 RESEARCH DESIGN

- 2.2 SECONDARY DATA

- 2.2.1 SECONDARY SOURCES

- 2.3 PRIMARY DATA

- 2.3.1 PRIMARY SOURCES

- 2.3.1.1 Insights from industry experts

- 2.3.1.2 Breakdown of primary interviews: by company type, designation, and region

- TABLE 3 DETAILS OF PRIMARY INTERVIEWEES

- 2.3.1 PRIMARY SOURCES

- 2.4 FACTOR ANALYSIS

- 2.4.1 INTRODUCTION

- 2.4.2 DEMAND-SIDE INDICATORS

- 2.4.3 SUPPLY-SIDE INDICATORS

- 2.4.3.1 Financial trends of major US defense contractors

- 2.5 MARKET SIZE ESTIMATION

- 2.5.1 BOTTOM-UP APPROACH

- FIGURE 4 MARKET SIZE ESTIMATION: BOTTOM-UP APPROACH

- 2.5.2 TOP-DOWN APPROACH

- FIGURE 5 MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- 2.6 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 6 DATA TRIANGULATION METHODOLOGY

- 2.7 RESEARCH ASSUMPTIONS

- FIGURE 7 ASSUMPTIONS FOR RESEARCH STUDY

- 2.8 RISK ANALYSIS

3 EXECUTIVE SUMMARY

- FIGURE 8 AIRBORNE SEGMENT TO EXHIBIT HIGHEST CAGR DURING FORECAST MARKET

- FIGURE 9 COMMUNICATION NETWORK SEGMENT TO DOMINATE MARKET FROM 2023 TO 2028

- FIGURE 10 EMBB SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 11 MILITARY SEGMENT TO REGISTER HIGHER CAGR THAN HOMELAND SECURITY SEGMENT DURING FORECAST PERIOD

- FIGURE 12 MEDIUM SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- FIGURE 13 NEW IMPLEMENTATION SEGMENT TO REGISTER HIGHER CAGR THAN UPGRADE SEGMENT DURING FORECAST PERIOD

- FIGURE 14 ASIA PACIFIC MARKET TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN 5G IN DEFENSE MARKET

- FIGURE 15 INCREASING USE OF 5G FOR IOT, ENHANCED AR & VR, ADVANCED AUTONOMOUS SYSTEMS, AND CYBERSECURITY TO DRIVE MARKET

- 4.2 5G IN DEFENSE MARKET, BY PLATFORM

- FIGURE 16 LAND SEGMENT TO LEAD MARKET FROM 2023 TO 2028

- 4.3 5G IN DEFENSE MARKET, BY SOLUTION

- FIGURE 17 COMMUNICATION NETWORK SEGMENT TO COMMAND LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.4 5G IN DEFENSE MARKET, BY END USER

- FIGURE 18 MILITARY SEGMENT TO ACCOUNT FOR LARGEST MARKET SHARE DURING FORECAST PERIOD

- 4.5 5G IN DEFENSE MARKET, BY NETWORK TYPE

- FIGURE 19 EMBB SEGMENT TO LEAD MARKET DURING FORECAST PERIOD

- 4.6 5G IN DEFENSE MARKET, BY INSTALLATION

- FIGURE 20 NEW IMPLEMENTATION SEGMENT TO COMMAND LARGER MARKET SHARE THAN UPGRADE SEGMENT DURING FORECAST PERIOD

- 4.7 5G IN DEFENSE MARKET, BY OPERATIONAL FREQUENCY

- FIGURE 21 LOW SEGMENT TO HAVE LARGEST MARKET SHARE DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 22 5G IN DEFENSE MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Use of 5G in situational awareness operations

- 5.2.1.2 Technological innovations in 5G network

- 5.2.1.3 Growing use of autonomous and connected devices integrated with 5G

- 5.2.1.4 Transition from legacy systems to cloud-based solutions

- 5.2.1.5 Increasing demand for high-speed and low-latency connectivity

- 5.2.2 RESTRAINTS

- 5.2.2.1 High investments in early phases

- 5.2.2.2 Lack of established protocols and standards

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing defense budgets for R&D and technological advancements in unmanned systems

- 5.2.3.2 Rise in virtual networking architecture

- 5.2.4 CHALLENGES

- 5.2.4.1 Complexities in spectrum management

- 5.3 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.3.1 REVENUE SHIFT AND NEW REVENUE POCKETS FOR 5G IN DEFENSE MANUFACTURERS

- FIGURE 23 REVENUE SHIFT IN 5G IN DEFENSE MARKET

- 5.4 RECESSION IMPACT ANALYSIS

- FIGURE 24 RECESSION IMPACT ANALYSIS: OPTIMISTIC, PESSIMISTIC, AND NEUTRAL SCENARIOS

- 5.5 ECOSYSTEM ANALYSIS

- 5.5.1 PROMINENT COMPANIES

- 5.5.2 PRIVATE AND SMALL ENTERPRISES

- 5.5.3 END USERS

- FIGURE 25 ECOSYSTEM ANALYSIS

- TABLE 4 ROLE OF COMPANIES IN MARKET ECOSYSTEM

- 5.6 TECHNOLOGY ANALYSIS

- 5.6.1 MASSIVE MIMO

- 5.6.2 NON-STANDALONE 5G NETWORKS

- 5.7 PRICING ANALYSIS

- 5.7.1 AVERAGE SELLING PRICE TRENDS OF 5G IN DEFENSE, BY COMMUNICATION NETWORK

- TABLE 5 AVERAGE SELLING PRICE TRENDS OF 5G IN DEFENSE, BY COMMUNICATION NETWORK, 2022 (USD/UNIT)

- 5.8 VALUE CHAIN ANALYSIS

- FIGURE 26 VALUE CHAIN ANALYSIS

- 5.9 CASE STUDY ANALYSIS

- 5.9.1 CRITICAL COMMUNICATIONS (CC) AND ULTRA-RELIABLE AND LOW-LATENCY COMMUNICATIONS (URLLC)

- TABLE 6 ULTRA-RELIABLE AND LOW-LATENCY COMMUNICATIONS (URLLC)

- 5.9.2 SUCCESSFUL DEMONSTRATION UNDER US DOD'S 5G-TO-NEXT G INITIATIVE

- 5.9.3 5G EMERGENCY RESCUE PLATFORM

- 5.10 PORTER'S FIVE FORCES ANALYSIS

- TABLE 7 5G IN DEFENSE MARKET: IMPACT OF PORTER'S FIVE FORCES

- FIGURE 27 PORTER'S FIVE FORCES ANALYSIS

- 5.10.1 THREAT OF NEW ENTRANTS

- 5.10.2 THREAT OF SUBSTITUTES

- 5.10.3 BARGAINING POWER OF SUPPLIERS

- 5.10.4 BARGAINING POWER OF BUYERS

- 5.10.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.11 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.11.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 28 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE PLATFORMS

- TABLE 8 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP THREE PLATFORMS (%)

- 5.11.2 BUYING CRITERIA

- FIGURE 29 KEY BUYING CRITERIA FOR TOP THREE PLATFORMS

- TABLE 9 KEY BUYING CRITERIA FOR TOP THREE PLATFORMS

- 5.12 TARIFF AND REGULATORY LANDSCAPE

- TABLE 10 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 11 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 12 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 13 MIDDLE EAST & AFRICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 14 LATIN AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- 5.13 KEY CONFERENCES AND EVENTS, 2023-2024

- TABLE 15 5G IN DEFENSE MARKET: KEY CONFERENCES AND EVENTS, 2023-2024

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 KEY TECHNOLOGICAL TRENDS IN 5G IN DEFENSE MARKET

- 6.2.1 AUGMENTED REALITY (AR) AND VIRTUAL REALITY (VR)

- 6.2.2 EDGE COMPUTING

- 6.2.3 CLOUD COMPUTING

- 6.2.4 SMALL CELL NETWORK

- 6.3 IMPACT OF MEGATRENDS

- 6.3.1 REAL-TIME DATA COLLECTION USING INTERNET OF THINGS

- 6.3.2 INTEGRATION OF ARTIFICIAL INTELLIGENCE IN DEFENSE SOLUTIONS

- 6.4 INNOVATIONS AND PATENT REGISTRATIONS

- TABLE 16 INNOVATIONS AND PATENT REGISTRATIONS, 2020-2023

- FIGURE 30 EVOLUTION OF 5G IN DEFENSE: ROADMAP FROM 2017 TO 2030

7 5G IN DEFENSE MARKET, BY SOLUTION

- 7.1 INTRODUCTION

- FIGURE 31 5G IN DEFENSE MARKET, BY SOLUTION, 2023 VS. 2028 (USD MILLION)

- TABLE 17 5G IN DEFENSE MARKET, BY SOLUTION, 2020-2022 (USD MILLION)

- TABLE 18 5G IN DEFENSE MARKET, BY SOLUTION, 2023-2028 (USD MILLION)

- 7.2 COMMUNICATION NETWORK

- FIGURE 32 5G IN DEFENSE MARKET, BY COMMUNICATION NETWORK, 2023 & 2028 (USD MILLION)

- TABLE 19 5G IN DEFENSE MARKET, BY COMMUNICATION NETWORK, 2020-2022 (USD MILLION)

- TABLE 20 5G IN DEFENSE MARKET, BY COMMUNICATION NETWORK, 2023-2028 (USD MILLION)

- 7.2.1 SMALL CELLS

- 7.2.1.1 Provide better quality cellular coverage and capacity, especially in urban areas

- 7.2.2 MACRO CELLS

- 7.2.2.1 Offer extensive coverage crucial for defense operations in remote or less dense areas

- 7.3 CHIPSET

- FIGURE 33 5G IN DEFENSE MARKET, BY CHIPSET, 2023 VS. 2028 (USD MILLION)

- TABLE 21 5G IN DEFENSE MARKET, BY CHIPSET, 2020-2022 (USD MILLION)

- TABLE 22 5G IN DEFENSE MARKET, BY CHIPSET, 2023-2028 (USD MILLION)

- 7.3.1 APPLICATION-SPECIFIC INTEGRATED CIRCUIT (ASIC) CHIPSETS

- 7.3.1.1 Custom-designed and tailored for specific tasks

- 7.3.2 RADIO FREQUENCY INTEGRATED CIRCUIT (RFIC) CHIPSETS

- 7.3.2.1 Process and produce high-frequency signals

- 7.3.3 MILLIMETER WAVE (MMWAVE) CHIPSETS

- 7.3.3.1 Deal with frequency bands from 30 to 300 GHz

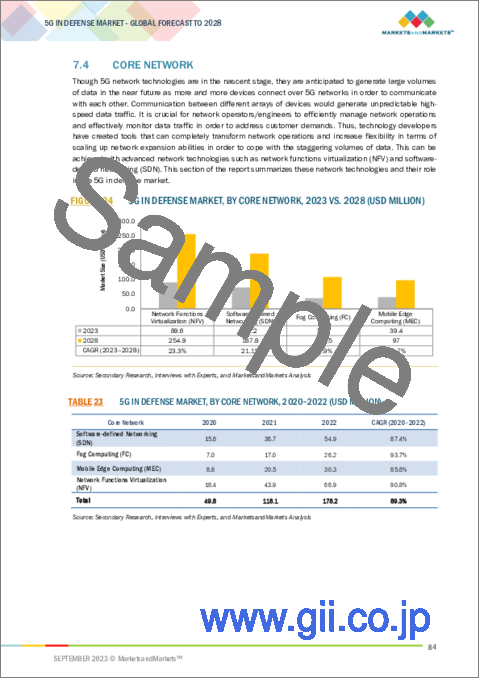

- 7.4 CORE NETWORK

- FIGURE 34 5G IN DEFENSE MARKET, BY CORE NETWORK, 2023 VS. 2028 (USD MILLION)

- TABLE 23 5G IN DEFENSE MARKET, BY CORE NETWORK, 2020-2022 (USD MILLION)

- TABLE 24 5G IN DEFENSE MARKET, BY CORE NETWORK, 2023-2028 (USD MILLION)

- 7.4.1 SOFTWARE-DEFINED NETWORKING (SDN)

- 7.4.1.1 Allows for dynamic, programmatically efficient network configuration

- 7.4.2 FOG COMPUTING (FC)

- 7.4.2.1 Offers high-speed data transfer protocol used in storage area networks

- 7.4.3 MOBILE EDGE COMPUTING (MEC)

- 7.4.3.1 Enables cloud computing capabilities and IT service environment at cellular network edge

- 7.4.4 NETWORK FUNCTIONS VIRTUALIZATION (NFV)

- 7.4.4.1 Enables network operators to easily implement different network functions

8 5G IN DEFENSE MARKET, BY PLATFORM

- 8.1 INTRODUCTION

- FIGURE 35 5G IN DEFENSE MARKET, BY PLATFORM, 2023 VS. 2028 (USD MILLION)

- TABLE 25 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 26 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- 8.2 LAND

- 8.2.1 ADVANCEMENTS IN LAND-BASED MILITARY AND WEAPON SYSTEMS TO DRIVE MARKET

- 8.2.1.1 Armored fighting vehicles

- 8.2.1.2 Unmanned ground vehicles

- 8.2.1.3 Command centers

- 8.2.1.4 Dismounted soldier systems

- 8.2.1 ADVANCEMENTS IN LAND-BASED MILITARY AND WEAPON SYSTEMS TO DRIVE MARKET

- 8.3 NAVAL

- 8.3.1 INCREASING NUMBER OF SENSORS ON SHIPS AND ADVANCEMENTS IN RADAR TECHNOLOGY TO DRIVE MARKET

- 8.3.1.1 Aircraft carriers

- 8.3.1.2 Amphibious ships

- 8.3.1.3 Destroyers

- 8.3.1.4 Frigates

- 8.3.1.5 Submarines

- 8.3.1.6 Unmanned maritime vehicles

- 8.3.1 INCREASING NUMBER OF SENSORS ON SHIPS AND ADVANCEMENTS IN RADAR TECHNOLOGY TO DRIVE MARKET

- 8.4 AIRBORNE

- 8.4.1 INCREASING SPENDING BY COUNTRIES ON 5G DEPLOYMENT ON AIRBORNE PLATFORMS TO DRIVE MARKET

- 8.4.1.1 Military aircraft

- 8.4.1.2 Unmanned aerial vehicles

- 8.4.1.3 Military helicopters

- 8.4.1 INCREASING SPENDING BY COUNTRIES ON 5G DEPLOYMENT ON AIRBORNE PLATFORMS TO DRIVE MARKET

9 5G IN DEFENSE MARKET, BY END USER

- 9.1 INTRODUCTION

- FIGURE 36 5G IN DEFENSE MARKET, BY END USER, 2023 VS. 2028 (USD MILLION)

- TABLE 27 5G IN DEFENSE MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 28 5G IN DEFENSE MARKET, BY END USER, 2023-2028 (USD MILLION)

- 9.2 MILITARY

- 9.2.1 5G TO ENHANCE MILITARY CAPABILITIES AND HELP MAINTAIN TECHNOLOGICAL ADVANTAGE ON BATTLEFIELD

- 9.3 HOMELAND SECURITY

- 9.3.1 5G TO ENHANCE SURVEILLANCE AND TRAINING CAPABILITIES

10 5G IN DEFENSE MARKET, BY NETWORK TYPE

- 10.1 INTRODUCTION

- FIGURE 37 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023 VS. 2028 (USD MILLION)

- TABLE 29 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 30 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 10.2 ENHANCED MOBILE BROADBAND

- 10.2.1 OFFERS HIGH SPEED AND HIGH BANDWIDTH FOR RELIABLE CONNECTIVITY ON THE MOVE

- 10.3 ULTRA-RELIABLE AND LOW-LATENCY COMMUNICATIONS

- 10.3.1 USED IN INDUSTRIAL AUTOMATION TO INCREASE PRODUCTIVITY

- 10.4 MASSIVE MACHINE-TYPE COMMUNICATIONS

- 10.4.1 5G IN DEFENSE EMPOWERS MASSIVE MACHINE-TYPE COMMUNICATIONS TO SUPPORT SENSOR DEPLOYMENTS

11 5G IN DEFENSE MARKET, BY OPERATIONAL FREQUENCY

- 11.1 INTRODUCTION

- FIGURE 38 5G IN DEFENSE MARKET, BY OPERATIONAL FREQUENCY, 2023 VS. 2028 (USD MILLION)

- TABLE 31 5G IN DEFENSE MARKET, BY OPERATIONAL FREQUENCY, 2020-2022 (USD MILLION)

- TABLE 32 5G IN DEFENSE MARKET, BY OPERATIONAL FREQUENCY, 2023-2028 (USD MILLION)

- 11.2 LOW

- 11.2.1 LOW OPERATING FREQUENCY OFFERS COVERAGE AND CAPACITY BENEFITS

- 11.3 MEDIUM

- 11.3.1 MID-BAND SPECTRUM OFFERS MIDDLE GROUND BETWEEN PERFORMANCE AND COVERAGE

- 11.4 HIGH

- 11.4.1 HIGH OPERATIONAL FREQUENCY REQUIRED TO MEET ULTRA-HIGH BROADBAND SPEEDS PROJECTED FOR 5G

12 5G IN DEFENSE MARKET, BY INSTALLATION

- 12.1 INTRODUCTION

- FIGURE 39 5G IN DEFENSE MARKET, BY INSTALLATION, 2023 VS. 2028 (USD MILLION)

- TABLE 33 5G IN DEFENSE MARKET, BY INSTALLATION, 2020-2022 (USD MILLION)

- TABLE 34 5G IN DEFENSE MARKET, BY INSTALLATION, 2023-2028 (USD MILLION)

- 12.2 UPGRADE

- 12.2.1 5G ARCHITECTURE UPGRADE OPERATES IN MASTER-SLAVE CONFIGURATION

- 12.3 NEW IMPLEMENTATION

- 12.3.1 NEW IMPLEMENTATION NETWORK PROVIDES END-TO-END 5G EXPERIENCE TO USERS

13 5G IN DEFENSE MARKET, BY REGION

- 13.1 INTRODUCTION

- FIGURE 40 ASIA PACIFIC MARKET TO REGISTER HIGHEST CAGR FROM 2023 TO 2028

- 13.2 REGIONAL RECESSION IMPACT ANALYSIS

- TABLE 35 REGIONAL RECESSION IMPACT ANALYSIS

- TABLE 36 5G IN DEFENSE MARKET, BY REGION, 2020-2022 (USD MILLION)

- TABLE 37 5G IN DEFENSE MARKET, BY REGION, 2023-2028 (USD MILLION)

- 13.3 NORTH AMERICA

- 13.3.1 PESTLE ANALYSIS: NORTH AMERICA

- 13.3.1.1 Political

- 13.3.1.2 Economic

- 13.3.1.3 Social

- 13.3.1.4 Technological

- 13.3.1.5 Legal

- 13.3.1.6 Environmental

- FIGURE 41 NORTH AMERICA: 5G IN DEFENSE MARKET SNAPSHOT

- TABLE 38 NORTH AMERICA: 5G IN DEFENSE MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 39 NORTH AMERICA: 5G IN DEFENSE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 40 NORTH AMERICA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 41 NORTH AMERICA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 42 NORTH AMERICA: 5G IN DEFENSE MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 43 NORTH AMERICA: 5G IN DEFENSE MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 44 NORTH AMERICA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 45 NORTH AMERICA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.3.2 US

- 13.3.2.1 Increased spending by US DOD and private players to drive market

- TABLE 46 US: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 47 US: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 48 US: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 49 US: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.3.3 CANADA

- 13.3.3.1 Increased R&D in 5G technology to drive market

- TABLE 50 CANADA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 51 CANADA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 52 CANADA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 53 CANADA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.3.1 PESTLE ANALYSIS: NORTH AMERICA

- 13.4 EUROPE

- 13.4.1 PESTLE ANALYSIS: EUROPE

- 13.4.1.1 Political

- 13.4.1.2 Economic

- 13.4.1.3 Social

- 13.4.1.4 Technological

- 13.4.1.5 Legal

- 13.4.1.6 Environmental

- FIGURE 42 EUROPE: 5G IN DEFENSE MARKET SNAPSHOT

- TABLE 54 EUROPE: 5G IN DEFENSE MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 55 EUROPE: 5G IN DEFENSE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 56 EUROPE: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 57 EUROPE: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 58 EUROPE: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 59 EUROPE: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.4.2 UK

- 13.4.2.1 New developments and investment in military equipment to drive market

- TABLE 60 UK: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 61 UK: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 62 UK: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 63 UK: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.4.3 FRANCE

- 13.4.3.1 Increased R&D investment in 5G for defense to drive market

- TABLE 64 FRANCE: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 65 FRANCE: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 66 FRANCE: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 67 FRANCE: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.4.4 GERMANY

- 13.4.4.1 Continuous focus on upgrading battle management and communications systems to drive market

- TABLE 68 GERMANY: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 69 GERMANY: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 70 GERMANY: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 71 GERMANY: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.4.5 ITALY

- 13.4.5.1 Increasing development of secure communications systems to drive market

- TABLE 72 ITALY: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 73 ITALY: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 74 ITALY: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 75 ITALY: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.4.6 RUSSIA

- 13.4.6.1 Increasing deployment of AI in command & control to modernize military forces to drive market

- TABLE 76 RUSSIA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 77 RUSSIA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 78 RUSSIA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 79 RUSSIA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.4.1 PESTLE ANALYSIS: EUROPE

- 13.5 ASIA PACIFIC

- 13.5.1 PESTLE ANALYSIS: ASIA PACIFIC

- 13.5.1.1 Political

- 13.5.1.2 Economic

- 13.5.1.3 Social

- 13.5.1.4 Technological

- 13.5.1.5 Legal

- 13.5.1.6 Environmental

- FIGURE 43 ASIA PACIFIC: 5G IN DEFENSE MARKET SNAPSHOT

- TABLE 80 ASIA PACIFIC: 5G IN DEFENSE MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 81 ASIA PACIFIC: 5G IN DEFENSE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 82 ASIA PACIFIC: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 83 ASIA PACIFIC: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 84 ASIA PACIFIC: 5G IN DEFENSE MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 85 ASIA PACIFIC: 5G IN DEFENSE MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 86 ASIA PACIFIC: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 87 ASIA PACIFIC: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.2 CHINA

- 13.5.2.1 Military technology modernization and increase in defense budget to drive market

- TABLE 88 CHINA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 89 CHINA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 90 CHINA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 91 CHINA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.3 JAPAN

- 13.5.3.1 Enhancement of defense and surveillance capabilities to drive market

- TABLE 92 JAPAN: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 93 JAPAN: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 94 JAPAN: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 95 JAPAN: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.4 INDIA

- 13.5.4.1 Increasing demand for ISR, real-time information, and telecommunication to drive market

- TABLE 96 INDIA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 97 INDIA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 98 INDIA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 99 INDIA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.5 SOUTH KOREA

- 13.5.5.1 Development of new technologies and increased government investment to drive market

- TABLE 100 SOUTH KOREA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 101 SOUTH KOREA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 102 SOUTH KOREA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 103 SOUTH KOREA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.6 AUSTRALIA

- 13.5.6.1 Growing demand for advanced network technology to drive market

- TABLE 104 AUSTRALIA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 105 AUSTRALIA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 106 AUSTRALIA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 107 AUSTRALIA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.7 MIDDLE EAST & AFRICA

- 13.5.8 PESTLE ANALYSIS: MIDDLE EAST & AFRICA

- 13.5.8.1 Political

- 13.5.8.2 Economic

- 13.5.8.3 Social

- 13.5.8.4 Technological

- 13.5.8.5 Legal

- 13.5.8.6 Environmental

- FIGURE 44 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET SNAPSHOT

- TABLE 108 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 109 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 110 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 111 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 112 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 113 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 114 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 115 MIDDLE EAST & AFRICA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.9 SAUDI ARABIA

- 13.5.9.1 Increasing military expenditure to drive market

- TABLE 116 SAUDI ARABIA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 117 SAUDI ARABIA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 118 SAUDI ARABIA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 119 SAUDI ARABIA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.10 ISRAEL

- 13.5.10.1 Heavy investment in 5G-related telecommunications to drive market

- TABLE 120 ISRAEL: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 121 ISRAEL: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 122 ISRAEL: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 123 ISRAEL: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.11 TURKEY

- 13.5.11.1 Rising demand for modern and advanced military networking to drive market

- TABLE 124 TURKEY: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 125 TURKEY: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 126 TURKEY: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 127 TURKEY: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.12 SOUTH AFRICA

- 13.5.12.1 Rising demand for modern digital technologies in military equipment to drive market

- TABLE 128 SOUTH AFRICA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 129 SOUTH AFRICA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 130 SOUTH AFRICA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 131 SOUTH AFRICA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.13 LATIN AMERICA

- 13.5.14 PESTLE ANALYSIS: LATIN AMERICA

- 13.5.14.1 Political

- 13.5.14.2 Economic

- 13.5.14.3 Social

- 13.5.14.4 Technological

- 13.5.14.5 Legal

- 13.5.14.6 Environmental

- FIGURE 45 LATIN AMERICA: 5G IN DEFENSE MARKET SNAPSHOT

- TABLE 132 LATIN AMERICA: 5G IN DEFENSE MARKET, BY COUNTRY, 2020-2022 (USD MILLION)

- TABLE 133 LATIN AMERICA: 5G IN DEFENSE MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 134 LATIN AMERICA: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 135 LATIN AMERICA: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 136 LATIN AMERICA: 5G IN DEFENSE MARKET, BY END USER, 2020-2022 (USD MILLION)

- TABLE 137 LATIN AMERICA: 5G IN DEFENSE MARKET, BY END USER, 2023-2028 (USD MILLION)

- TABLE 138 LATIN AMERICA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 139 LATIN AMERICA: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.15 BRAZIL

- 13.5.15.1 Expansion of telecommunication services to drive market

- TABLE 140 BRAZIL: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 141 BRAZIL: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 142 BRAZIL: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 143 BRAZIL: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.16 MEXICO

- 13.5.16.1 Growing demand for high network speeds and low latency communications systems to drive market

- TABLE 144 MEXICO: 5G IN DEFENSE MARKET, BY PLATFORM, 2020-2022 (USD MILLION)

- TABLE 145 MEXICO: 5G IN DEFENSE MARKET, BY PLATFORM, 2023-2028 (USD MILLION)

- TABLE 146 MEXICO: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2020-2022 (USD MILLION)

- TABLE 147 MEXICO: 5G IN DEFENSE MARKET, BY NETWORK TYPE, 2023-2028 (USD MILLION)

- 13.5.1 PESTLE ANALYSIS: ASIA PACIFIC

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 COMPANY OVERVIEW

- TABLE 148 KEY DEVELOPMENTS OF LEADING PLAYERS IN 5G IN DEFENSE MARKET, 2020-2023

- 14.3 MARKET RANKING ANALYSIS, 2022

- FIGURE 46 RANKING OF KEY PLAYERS IN 5G IN DEFENSE MARKET, 2022

- 14.4 REVENUE ANALYSIS OF KEY MARKET PLAYERS, 2020-2022

- FIGURE 47 REVENUE ANALYSIS OF KEY MARKET, 2020-2022

- 14.5 MARKET SHARE ANALYSIS, 2022

- FIGURE 48 MARKET SHARE ANALYSIS, 2022

- 14.6 COMPANY EVALUATION MATRIX

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- FIGURE 49 5G IN DEFENSE MARKET: COMPANY EVALUATION MATRIX, 2022

- 14.7 START-UP/SME EVALUATION MATRIX

- 14.7.1 PROGRESSIVE COMPANIES

- 14.7.2 RESPONSIVE COMPANIES

- 14.7.3 STARTING BLOCKS

- 14.7.4 DYNAMIC COMPANIES

- FIGURE 50 5G IN DEFENSE MARKET: START-UP/SME EVALUATION MATRIX, 2022

- 14.8 COMPETITIVE BENCHMARKING

- TABLE 149 COMPANY PRODUCT FOOTPRINT

- TABLE 150 COMPANY PLATFORM FOOTPRINT

- TABLE 151 COMPANY SOLUTION FOOTPRINT

- TABLE 152 COMPANY REGION FOOTPRINT

- 14.9 COMPETITIVE SCENARIO

- 14.9.1 MARKET EVALUATION FRAMEWORK

- 14.9.2 PRODUCT LAUNCHES

- TABLE 153 PRODUCT LAUNCHES, 2020-MAY 2023

- 14.9.3 DEALS

- TABLE 154 DEALS, 2020-SEPTEMBER 2023

15 COMPANY PROFILES

- (Business Overview, Products Offered, Recent Developments, MnM View Right to win, Strategic choices made, Weaknesses and competitive threats) **

- 15.1 INTRODUCTION

- 15.2 KEY PLAYERS

- 15.2.1 ERICSSON

- TABLE 155 ERICSSON: COMPANY OVERVIEW

- FIGURE 51 ERICSSON: COMPANY SNAPSHOT

- TABLE 156 ERICSSON: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 157 ERICSSON: DEALS

- 15.2.2 NOKIA

- TABLE 158 NOKIA: COMPANY OVERVIEW

- FIGURE 52 NOKIA: COMPANY SNAPSHOT

- TABLE 159 NOKIA: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 160 NOKIA: DEALS

- 15.2.3 NEC CORPORATION

- TABLE 161 NEC CORPORATION: COMPANY OVERVIEW

- FIGURE 53 NEC CORPORATION: COMPANY SNAPSHOT

- TABLE 162 NEC CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 163 NEC CORPORATION: DEALS

- 15.2.4 SAMSUNG ELECTRONICS CO., LTD.

- TABLE 164 SAMSUNG ELECTRONICS CO., LTD.: COMPANY OVERVIEW

- FIGURE 54 SAMSUNG ELECTRONICS CO., LTD.: COMPANY SNAPSHOT

- TABLE 165 SAMSUNG ELECTRONICS CO., LTD.: PRODUCT/SOLUTIONS/SERVICES OFFERED

- TABLE 166 SAMSUNG ELECTRONICS CO., LTD.: DEALS

- 15.2.5 HUAWEI

- TABLE 167 HUAWEI: COMPANY OVERVIEW

- FIGURE 55 HUAWEI: COMPANY SNAPSHOT

- TABLE 168 HUAWEI: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 169 HUAWEI: DEALS

- 15.2.6 THALES GROUP

- TABLE 170 THALES GROUP: COMPANY OVERVIEW

- FIGURE 56 THALES GROUP: COMPANY SNAPSHOT

- TABLE 171 THALES GROUP: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 172 THALES GROUP: DEALS

- 15.2.7 RAYTHEON TECHNOLOGIES CORPORATION

- TABLE 173 RAYTHEON TECHNOLOGIES CORPORATION: COMPANY OVERVIEW

- FIGURE 57 RAYTHEON TECHNOLOGIES CORPORATION: COMPANY SNAPSHOT

- TABLE 174 RAYTHEON TECHNOLOGIES CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 175 RAYTHEON TECHNOLOGIES CORPORATION: DEALS

- 15.2.8 INTELSAT

- TABLE 176 INTELSAT: COMPANY OVERVIEW

- TABLE 177 INTELSAT: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 178 INTELSAT: DEALS

- 15.2.9 QUALCOMM, INC.

- TABLE 179 QUALCOMM, INC.: COMPANY OVERVIEW

- FIGURE 58 QUALCOMM, INC.: COMPANY SNAPSHOT

- TABLE 180 QUALCOMM, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 181 QUALCOMM, INC.: DEALS

- 15.2.10 CISCO SYSTEMS, INC.

- TABLE 182 CISCO SYSTEMS, INC.: COMPANY OVERVIEW

- FIGURE 59 CISCO SYSTEMS, INC.: COMPANY SNAPSHOT

- TABLE 183 CISCO SYSTEMS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 15.2.11 VERIZON COMMUNICATIONS, INC.

- TABLE 184 VERIZON COMMUNICATIONS, INC.: COMPANY OVERVIEW

- FIGURE 60 VERIZON COMMUNICATIONS, INC.: COMPANY SNAPSHOT

- TABLE 185 VERIZON COMMUNICATIONS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 186 VERIZON COMMUNICATIONS, INC.: DEALS

- 15.2.12 DEUTSCHE TELEKOM AG

- TABLE 187 DEUTSCHE TELEKOM AG: COMPANY OVERVIEW

- TABLE 188 DEUTSCHE TELEKOM AG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 189 DEUTSCHE TELEKOM AG: DEALS

- 15.2.13 ORANGE S.A.

- TABLE 190 ORANGE S.A.: COMPANY OVERVIEW

- FIGURE 61 ORANGE S.A.: COMPANY SNAPSHOT

- TABLE 191 ORANGE S.A.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 192 ORANGE S.A.: PRODUCT LAUNCHES

- TABLE 193 ORANGE S.A.: DEALS

- 15.2.14 GOGO, INC.

- TABLE 194 GOGO, INC.: COMPANY OVERVIEW

- FIGURE 62 GOGO, INC.: COMPANY SNAPSHOT

- TABLE 195 GOGO, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 15.2.15 LIGADO NETWORKS

- TABLE 196 LIGADO NETWORKS: COMPANY OVERVIEW

- TABLE 197 LIGADO NETWORKS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 198 LIGADO NETWORKS: DEALS

- 15.2.16 WIND RIVER SYSTEMS, INC.

- TABLE 199 WIND RIVER SYSTEMS, INC.: COMPANY OVERVIEW

- TABLE 200 WIND RIVER SYSTEMS, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 15.2.17 ANALOG DEVICES, INC.

- TABLE 201 ANALOG DEVICES, INC.: COMPANY OVERVIEW

- FIGURE 63 ANALOG DEVICES, INC.: COMPANY SNAPSHOT

- TABLE 202 ANALOG DEVICES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 203 ANALOG DEVICES, INC.: DEALS

- 15.2.18 INTEL CORPORATION

- TABLE 204 INTEL CORPORATION: COMPANY OVERVIEW

- FIGURE 64 INTEL CORPORATION: COMPANY SNAPSHOT

- TABLE 205 INTEL CORPORATION: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 206 INTEL CORPORATION: DEALS

- 15.2.19 L3HARRIS TECHNOLOGIES, INC.

- TABLE 207 L3HARRIS TECHNOLOGIES, INC.: COMPANY OVERVIEW

- FIGURE 65 L3HARRIS TECHNOLOGIES, INC.: COMPANY SNAPSHOT

- TABLE 208 L3HARRIS TECHNOLOGIES, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- 15.3 OTHER PLAYERS

- 15.3.1 COMBA TELECOM

- TABLE 209 COMBA TELECOM: COMPANY OVERVIEW

- 15.3.2 STERLITE TECHNOLOGIES LTD.

- TABLE 210 STERLITE TECHNOLOGIES LTD.: COMPANY OVERVIEW

- 15.3.3 T-MOBILE US, INC.

- TABLE 211 T-MOBILE US, INC.: COMPANY OVERVIEW

- 15.3.4 TELECOM ITALIA

- TABLE 212 TELECOM ITALIA: COMPANY OVERVIEW

- 15.3.5 MARVELL

- TABLE 213 MARVELL: COMPANY OVERVIEW

- 15.3.6 MEDIATEK INC.

- TABLE 214 MEDIATEK INC.: COMPANY OVERVIEW

- *Details on Business Overview, Products Offered, Recent Developments, MnM View, Right to win, Strategic choices made, Weaknesses and competitive threats might not be captured in case of unlisted companies.

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.3 CUSTOMIZATION OPTIONS

- 16.4 RELATED REPORTS

- 16.5 AUTHOR DETAILS