|

|

市場調査レポート

商品コード

1674553

アーバンエアモビリティの世界市場:ソリューション別、プラットフォームアーキテクチャ別、モビリティタイプ別、エンドユーザー別、操作モード別、航続距離別、地域別 - 2035年までの予測Urban Air Mobility Market by Mobility Type, Solution, Platform Architecture, Range & Region - Global Forecast to 2035 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| アーバンエアモビリティの世界市場:ソリューション別、プラットフォームアーキテクチャ別、モビリティタイプ別、エンドユーザー別、操作モード別、航続距離別、地域別 - 2035年までの予測 |

|

出版日: 2025年03月01日

発行: MarketsandMarkets

ページ情報: 英文 428 Pages

納期: 即納可能

|

全表示

- 概要

- 図表

- 目次

アーバンエアモビリティ(UAM)の市場規模は、2024年に46億米ドルとなりました。

同市場は、2024年から2030年に31.2%のCAGRで拡大し、2030年までに235億米ドルとなるとみられ、2030年から2035年に12.1%のCAGRで拡大し、2035年までに415億米ドルに達すると予測されています。プラットフォーム台数は、2024年の61,479台から、2030年には519,370台、2035年には875,438台へと成長すると予測されます。

| 調査範囲 | |

|---|---|

| 調査対象年 | 2020年~2035年 |

| 基準年 | 2023年 |

| 予測期間 | 2024年~2035年 |

| 検討単位 | 金額(10億米ドル) |

| セグメント別 | ソリューション別、プラットフォームアーキテクチャ別、モビリティタイプ別、エンドユーザー別、操作モード別、航続距離別、地域別 |

| 対象地域 | 北米、欧州、アジア太平洋、その他の地域 |

UAM市場の主な促進要因としては、混雑緩和のための効率的な都市モビリティソリューションに対する高い需要、電気エンジン、自律走行システム、改良型バッテリーによる技術的に高度な推進力、ベンチャーキャピタルや民間からの多額の投資などが挙げられます。規制枠組みの支援や、バーティポートや充電ステーションといった要件のインフラ開拓は、市場を後押しする不可欠な要素です。さらに、排出ガスに対する懸念の高まりと、新しいオンデマンド・モビリティ・オプションに対する消費者の関心の高まりにより、環境問題への懸念と消費者の好奇心が市場の成長を後押ししています。

したがって、プラットフォームセグメントの貢献は、2024年の市場で最大となるとみられています。実際、プラットフォームは航空モビリティ・ソリューションの展開と運用において重要な役割を果たすため、このセグメントはUAM市場を独占する可能性が高いです。プラットフォームは、eVTOL航空機と付随するソフトウェアで構成され、初期配備と販売、リース、サービスからの収益が含まれます。現在の交通インフラとの統合の可能性、技術進歩の急速なペース、競争力のある革新的な能力により、このセグメントの市場における主導的地位は確実なものとなっています。

エンドユーザー別では、ライドシェア企業セグメントは予測期間中に最も成長すると予想されます。UAMは、ライドシェアリング事業を展開する企業によって支配される可能性が高いです。なぜなら、このビジネスモデルは迅速なスケールアップに最適な能力を示しており、迅速かつ効率的に大幅な成長に対応することができ、巨大なフリートを扱ってきた長い歴史が、このような企業の経験に基づくマーケットプレースに確固たる地盤を与えているからです。その上、既存のブランド名と顧客ロイヤルティは、市場でのポジショニングを大幅に強化します。こうしたエアモビリティー・ソリューションが統合されるにつれ、ライドシェア企業は既存のインフラと運用経験を活用して、シームレスで斬新な輸送サービスの大規模な導入を実現し、それによってUAM分野が大きく成長する原動力となると思われます。

北米は、都市交通の新たなコンセプトにおける世界のその他の地域のイノベーションのペースをリードし、これらのイノベーションに必要なインフラを構築しているため、UAM市場で最大のシェアを維持しています。同地域ではテクノロジー・エコシステムが確立されており、起業家の存在感が強いため、UAMの開発は非常に速いです。

その上、北米は都市部や郊外の多様な環境から、様々な使用事例や用途に対応するUAMソリューションの理想的な地上試験まで、多様な地域を提供しています。さらに、航空宇宙や自動車の大手企業が拠点を置いており、UAM技術の開発と商業化を加速させるための協力的な環境が整っています。

当レポートでは、世界のアーバンエアモビリティ市場について調査し、ソリューション別、プラットフォームアーキテクチャ別、モビリティタイプ別、エンドユーザー別、操作モード別、航続距離別、地域別動向、および市場に参入する企業のプロファイルなどをまとめています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- バリューチェーン分析

- エコシステム分析

- 顧客ビジネスに影響を与える動向と混乱

- 貿易分析

- 規制状況

- 使用事例分析

- 主な利害関係者と購入基準

- 2025年の主な会議とイベント

- マクロ経済見通し

- 部品表

- 総所有コスト

- ビジネスモデル

- 投資と資金調達のシナリオ

- アーバンエアモビリティ市場のロードマップ

- 運用データ

- 指標価格分析

- 技術ロードマップ

- AI/生成AIがアーバンエアモビリティ市場に与える影響

- アーバンエアモビリティのためのEVTOLプラットフォームのシナリオ分析

第6章 業界の動向

- イントロダクション

- 技術動向

- 技術分析

- メガトレンドの影響

- 特許分析

第7章 アーバンエアモビリティ市場、ソリューション別

- イントロダクション

- プラットフォーム

- インフラストラクチャ

第8章 アーバンエアモビリティ市場、プラットフォームアーキテクチャ別

- イントロダクション

- ロータリーウィング

- 固定翼ハイブリッド

- 固定翼

第9章 アーバンエアモビリティ市場、モビリティタイプ別

- イントロダクション

- エアタクシー

- エアシャトルとエアメトロ

- 個人用航空機

- 貨物航空機

- 救急航空および医療緊急車両

第10章 アーバンエアモビリティ市場、エンドユーザー別

- イントロダクション

- ライドシェアリング会社

- 定期運行会社

- eコマース商取引企業

- 病院および医療機関

- 民間事業者

第11章 アーバンエアモビリティ市場、操作モード別

- イントロダクション

- パイロット型

- 自律型

第12章 アーバンエアモビリティ市場、航続距離別

- イントロダクション

- 都市間(>100 km)

- 都市内(<100 km)

第13章 アーバンエアモビリティ市場、地域別

- イントロダクション

- 北米

- イントロダクション

- PESTLE分析

- 米国

- カナダ

- 欧州

- イントロダクション

- PESTLE分析

- 英国

- フランス

- ドイツ

- イタリア

- スイス

- スペイン

- アイルランド

- ベルギー

- アジア太平洋

- イントロダクション

- PESTLE分析

- 中国

- インド

- 日本

- 韓国

- オーストラリア

- シンガポール

- インドネシア

- ラテンアメリカ

- イントロダクション

- PESTLE分析

- ブラジル

- メキシコ

- アルゼンチン

- コスタリカ

- その他の地域

- イントロダクション

- 中東

- アフリカ

第14章 競合情勢

- イントロダクション

- 主要参入企業の戦略/強み

- 収益分析

- 市場シェア分析

- 企業評価マトリックス:主要参入企業(プラットフォーム別)、2023年

- 企業評価マトリックス:主要参入企業(インフラストラクチャ別)、2023年

- 会社の足跡

- 企業評価マトリックス:スタートアップ/中小企業(ソリューション別)、2023年

- 企業価値評価と財務指標

- 競合シナリオ

- 市場評価フレームワーク

- ブランド比較

第15章 企業プロファイル

- 主要参入企業

- AIRBUS

- EVE HOLDING, INC.

- VERTICAL AEROSPACE

- EHANG

- ARCHER AVIATION INC.

- TEXTRON INC.

- JOBY AVIATION

- FERROVIAL

- SKYPORTS INFRASTRUCTURE LIMITED

- WISK AERO LLC

- JAUNT AIR MOBILITY LLC.

- LILIUM GMBH

- WINGCOPTER

- BETA TECHNOLOGIES

- VOLOCOPTER GMBH

- その他の企業

- ARC AERO SYSTEMS

- SKYDRIVE INC.

- ELECTRA.AERO

- AUTOFLIGHT

- OVERAIR, INC.

- MANTA AIRCRAFT

- AIR VEV LTD

- URBAN AERONAUTICS LTD.

- SKYRYSE, INC.

- ASCENDANCE FLIGHT TECHNOLOGIES S.A.S.

第16章 付録

List of Tables

- TABLE 1 URBAN AIR MOBILITY MARKET: INCLUSIONS AND EXCLUSIONS

- TABLE 2 USD EXCHANGE RATES

- TABLE 3 URBAN AIR MOBILITY MARKET: ROLE OF COMPANIES IN ECOSYSTEM

- TABLE 4 NORTH AMERICA: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 5 EUROPE: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 6 ASIA PACIFIC: REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER AGENCIES

- TABLE 7 REGION- AND COUNTRY-WISE REGULATIONS SUPPORTING URBAN AIR MOBILITY ECOSYSTEM DEVELOPMENT

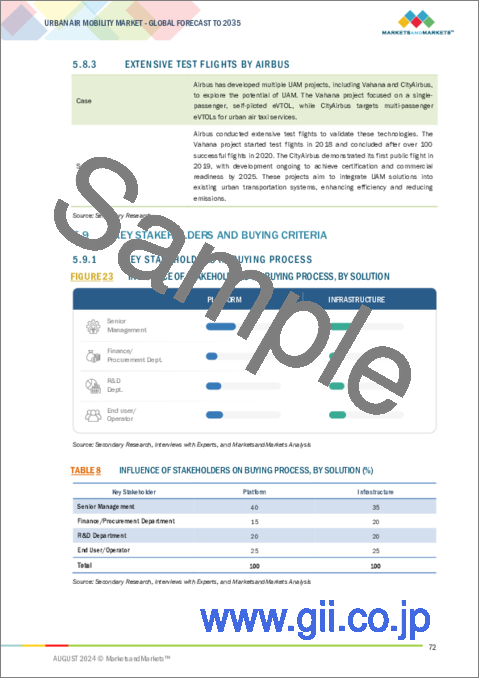

- TABLE 8 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY SOLUTION (%)

- TABLE 9 KEY BUYING CRITERIA FOR URBAN AIR MOBILITY, BY SOLUTION

- TABLE 10 URBAN AIR MOBILITY MARKET: KEY CONFERENCES AND EVENTS, 2025

- TABLE 11 TOTAL COST OF OWNERSHIP COMPARISON, BY SOLUTION

- TABLE 12 URBAN AIR MOBILITY PLATFORM OPERATIONS: BUSINESS MODEL COMPARISON

- TABLE 13 URBAN AIR MOBILITY INFRASTRUCTURE OPERATIONS: BUSINESS MODEL COMPARISON

- TABLE 14 KEY URBAN AIR MOBILITY PLATFORM ORDER BOOKS

- TABLE 15 TENTATIVE KEY ACTIVITIES ASSOCIATED WITH UNMANNED TRAFFIC MANAGEMENT SYSTEMS

- TABLE 16 PRICE RANGE OF AIRCRAFT MODELS BY KEY PLAYERS

- TABLE 17 VERTIPORT CONSTRUCTION EXPENDITURES BY SYSTEM SIZE: INCREMENTAL AND TOTAL EXPENDITURE (USD MILLION)

- TABLE 18 MAJOR PATENTS IN URBAN AIR MOBILITY MARKET, 2023-2024

- TABLE 19 URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 20 URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 21 URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 22 URBAN AIR MOBILITY MARKET, BY PLATFORM, 2020-2023 (USD MILLION)

- TABLE 23 URBAN AIR MOBILITY MARKET, BY PLATFORM, 2024-2030 (USD MILLION)

- TABLE 24 URBAN AIR MOBILITY MARKET, BY PLATFORM, 2031-2035 (USD MILLION)

- TABLE 25 URBAN AIR MOBILITY MARKET, BY AVIONICS, 2020-2023 (USD MILLION)

- TABLE 26 URBAN AIR MOBILITY MARKET, BY AVIONICS, 2024-2030 (USD MILLION)

- TABLE 27 URBAN AIR MOBILITY MARKET, BY AVIONICS, 2031-2035 (USD MILLION)

- TABLE 28 URBAN AIR MOBILITY MARKET, BY SENSORS, 2020-2023 (USD MILLION)

- TABLE 29 URBAN AIR MOBILITY MARKET, BY SENSORS, 2024-2030 (USD MILLION)

- TABLE 30 URBAN AIR MOBILITY MARKET, BY SENSORS, 2031-2035 (USD MILLION)

- TABLE 31 URBAN AIR MOBILITY MARKET, BY PROPULSION SYSTEMS, 2020-2023 (USD MILLION)

- TABLE 32 URBAN AIR MOBILITY MARKET, BY PROPULSION SYSTEMS, 2024-2030 (USD MILLION)

- TABLE 33 URBAN AIR MOBILITY MARKET, BY PROPULSION SYSTEMS, 2031-2035 (USD MILLION)

- TABLE 34 URBAN AIR MOBILITY MARKET, BY ELECTRICAL SYSTEMS, 2020-2023 (USD MILLION)

- TABLE 35 URBAN AIR MOBILITY MARKET, BY ELECTRICAL SYSTEMS, 2024-2030 (USD MILLION)

- TABLE 36 URBAN AIR MOBILITY MARKET, BY ELECTRICAL SYSTEMS, 2031-2035 (USD MILLION)

- TABLE 37 URBAN AIR MOBILITY MARKET, BY INFRASTRUCTURE, 2020-2023 (USD MILLION)

- TABLE 38 URBAN AIR MOBILITY MARKET, BY INFRASTRUCTURE, 2024-2030 (USD MILLION)

- TABLE 39 URBAN AIR MOBILITY MARKET, BY INFRASTRUCTURE, 2031-2035 (USD MILLION)

- TABLE 40 URBAN AIR MOBILITY MARKET, BY PLATFORM ARCHITECTURE, 2020-2023 (USD MILLION)

- TABLE 41 URBAN AIR MOBILITY MARKET, BY PLATFORM ARCHITECTURE, 2024-2030 (USD MILLION)

- TABLE 42 URBAN AIR MOBILITY MARKET, BY PLATFORM ARCHITECTURE, 2031-2035 (USD MILLION)

- TABLE 43 URBAN AIR MOBILITY MARKET, BY PLATFORM ARCHITECTURE, 2020-2023 (UNITS)

- TABLE 44 URBAN AIR MOBILITY MARKET, BY PLATFORM ARCHITECTURE, 2024-2030 (UNITS)

- TABLE 45 URBAN AIR MOBILITY MARKET, BY PLATFORM ARCHITECTURE, 2031-2035 (UNITS)

- TABLE 46 JAUNT AIR MOBILITY: SPECIFICATIONS

- TABLE 47 BELL 407: SPECIFICATIONS

- TABLE 48 VOLOCOPTER VOLOCITY: SPECIFICATIONS

- TABLE 49 EHANG 216: SPECIFICATIONS

- TABLE 50 EVE: SPECIFICATIONS

- TABLE 51 BETA TECHNOLOGIES ALIA VTOL: SPECIFICATIONS

- TABLE 52 LILIUM JET: SPECIFICATIONS

- TABLE 53 JOBY S4: SPECIFICATIONS

- TABLE 54 ARCHER MIDNIGHT: SPECIFICATIONS

- TABLE 55 BETA TECHNOLOGIES ALIA CTOL: SPECIFICATIONS

- TABLE 56 ELECTRA.AERO: SPECIFICATIONS

- TABLE 57 URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2020-2023 (USD MILLION)

- TABLE 58 URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2024-2030 (USD MILLION)

- TABLE 59 URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2031-2035 (USD MILLION)

- TABLE 60 URBAN AIR MOBILITY MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 61 URBAN AIR MOBILITY MARKET, BY END USER, 2024-2030 (USD MILLION)

- TABLE 62 URBAN AIR MOBILITY MARKET, BY END USER, 2031-2035 (USD MILLION)

- TABLE 63 URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 64 URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 65 URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 66 URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 67 URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 68 URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 69 URBAN AIR MOBILITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 70 URBAN AIR MOBILITY MARKET, BY REGION, 2024-2030 (USD MILLION)

- TABLE 71 URBAN AIR MOBILITY MARKET, BY REGION, 2031-2035 (USD MILLION)

- TABLE 72 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 73 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 74 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2031-2035 (USD MILLION)

- TABLE 75 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 76 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 77 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 78 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2020-2023 (USD MILLION)

- TABLE 79 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2024-2030 (USD MILLION)

- TABLE 80 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2031-2035 (USD MILLION)

- TABLE 81 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 82 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 83 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 84 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 85 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 86 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 87 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 88 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY END USER, 2024-2030 (USD MILLION)

- TABLE 89 NORTH AMERICA: URBAN AIR MOBILITY MARKET, BY END USER, 2031-2035 (USD MILLION)

- TABLE 90 US: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 91 US: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 92 US: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 93 US: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 94 US: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 95 US: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 96 US: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 97 US: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 98 US: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 99 CANADA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 100 CANADA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 101 CANADA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 102 CANADA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 103 CANADA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 104 CANADA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 105 CANADA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 106 CANADA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 107 CANADA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 108 EUROPE: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 109 EUROPE: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 110 EUROPE: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2031-2035 (USD MILLION)

- TABLE 111 EUROPE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 112 EUROPE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 113 EUROPE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 114 EUROPE: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2020-2023 (USD MILLION)

- TABLE 115 EUROPE: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2024-2030 (USD MILLION)

- TABLE 116 EUROPE: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2031-2035 (USD MILLION)

- TABLE 117 EUROPE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 118 EUROPE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 119 EUROPE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 120 EUROPE: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 121 EUROPE: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 122 EUROPE: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 123 EUROPE: URBAN AIR MOBILITY MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 124 EUROPE: URBAN AIR MOBILITY MARKET, BY END USER, 2024-2030 (USD MILLION)

- TABLE 125 EUROPE: URBAN AIR MOBILITY MARKET, BY END USER, 2031-2035 (USD MILLION)

- TABLE 126 UK: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 127 UK: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 128 UK: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 129 UK: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 130 UK: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 131 UK: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 132 UK: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 133 UK: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 134 UK: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 135 FRANCE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 136 FRANCE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 137 FRANCE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 138 FRANCE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 139 FRANCE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 140 FRANCE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 141 FRANCE: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 142 FRANCE: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 143 FRANCE: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 144 GERMANY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 145 GERMANY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 146 GERMANY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 147 GERMANY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 148 GERMANY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 149 GERMANY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 150 GERMANY: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 151 GERMANY: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 152 GERMANY: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 153 ITALY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 154 ITALY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 155 ITALY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 156 ITALY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 157 ITALY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 158 ITALY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 159 ITALY: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 160 ITALY: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 161 ITALY: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 162 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 163 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 164 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 165 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 166 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 167 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 168 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 169 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 170 SWITZERLAND: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 171 SPAIN: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 172 SPAIN: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 173 SPAIN: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 174 SPAIN: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 175 SPAIN: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 176 SPAIN: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 177 SPAIN: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 178 SPAIN: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 179 SPAIN: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 180 IRELAND: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 181 IRELAND: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 182 IRELAND: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 183 IRELAND: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 184 IRELAND: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 185 IRELAND: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 186 IRELAND: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 187 IRELAND: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 188 IRELAND: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 189 BELGIUM: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 190 BELGIUM: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 191 BELGIUM: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 192 BELGIUM: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 193 BELGIUM: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 194 BELGIUM: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 195 BELGIUM: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 196 BELGIUM: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 197 BELGIUM: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 198 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 199 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 200 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2031-2035 (USD MILLION)

- TABLE 201 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 202 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 203 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 204 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2020-2023 (USD MILLION)

- TABLE 205 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2024-2030 (USD MILLION)

- TABLE 206 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2031-2035 (USD MILLION)

- TABLE 207 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 208 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 209 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 210 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 211 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 212 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 213 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 214 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY END USER, 2024-2030 (USD MILLION)

- TABLE 215 ASIA PACIFIC: URBAN AIR MOBILITY MARKET, BY END USER, 2031-2035 (USD MILLION)

- TABLE 216 CHINA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 217 CHINA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 218 CHINA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 219 CHINA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 220 CHINA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 221 CHINA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 222 CHINA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 223 CHINA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 224 CHINA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 225 INDIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 226 INDIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 227 INDIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 228 INDIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 229 INDIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 230 INDIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 231 INDIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 232 INDIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 233 INDIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 234 JAPAN: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 235 JAPAN: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 236 JAPAN: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 237 JAPAN: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 238 JAPAN: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 239 JAPAN: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 240 JAPAN: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 241 JAPAN: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 242 JAPAN: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 243 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 244 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 245 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 246 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 247 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 248 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 249 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 250 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 251 SOUTH KOREA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 252 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 253 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 254 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 255 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 256 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 257 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 258 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 259 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 260 AUSTRALIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 261 SINGAPORE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 262 SINGAPORE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 263 SINGAPORE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 264 SINGAPORE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 265 SINGAPORE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 266 SINGAPORE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 267 SINGAPORE: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 268 SINGAPORE: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 269 SINGAPORE: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 270 INDONESIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 271 INDONESIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 272 INDONESIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 273 INDONESIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 274 INDONESIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 275 INDONESIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 276 INDONESIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 277 INDONESIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 278 INDONESIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 279 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 280 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 281 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2031-2035 (USD MILLION)

- TABLE 282 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 283 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 284 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 285 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2020-2023 (USD MILLION)

- TABLE 286 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2024-2030 (USD MILLION)

- TABLE 287 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2031-2035 (USD MILLION)

- TABLE 288 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 289 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 290 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 291 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 292 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 293 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 294 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 295 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY END USER, 2024-2030 (USD MILLION)

- TABLE 296 LATIN AMERICA: URBAN AIR MOBILITY MARKET, BY END USER, 2031-2035 (USD MILLION)

- TABLE 297 BRAZIL: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 298 BRAZIL: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 299 BRAZIL: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 300 BRAZIL: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 301 BRAZIL: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 302 BRAZIL: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 303 BRAZIL: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 304 BRAZIL: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 305 BRAZIL: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 306 MEXICO: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 307 MEXICO: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 308 MEXICO: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 309 MEXICO: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 310 MEXICO: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 311 MEXICO: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 312 MEXICO: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 313 MEXICO: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 314 MEXICO: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 315 ARGENTINA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 316 ARGENTINA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 317 ARGENTINA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 318 ARGENTINA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 319 ARGENTINA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 320 ARGENTINA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 321 ARGENTINA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 322 ARGENTINA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 323 ARGENTINA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 324 COSTA RICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 325 COSTA RICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 326 COSTA RICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 327 COSTA RICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 328 COSTA RICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 329 COSTA RICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 330 COSTA RICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 331 COSTA RICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 332 COSTA RICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 333 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY REGION, 2020-2023 (USD MILLION)

- TABLE 334 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY REGION, 2024-2030 (USD MILLION)

- TABLE 335 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY REGION, 2031-2035 (USD MILLION)

- TABLE 336 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 337 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 338 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 339 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2020-2023 (USD MILLION)

- TABLE 340 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2024-2030 (USD MILLION)

- TABLE 341 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2031-2035 (USD MILLION)

- TABLE 342 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 343 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 344 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 345 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 346 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 347 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 348 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY END USER, 2020-2023 (USD MILLION)

- TABLE 349 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY END USER, 2024-2030 (USD MILLION)

- TABLE 350 REST OF THE WORLD: URBAN AIR MOBILITY MARKET, BY END USER, 2031-2035 (USD MILLION)

- TABLE 351 MIDDLE EAST: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2020-2023 (USD MILLION)

- TABLE 352 MIDDLE EAST: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2024-2030 (USD MILLION)

- TABLE 353 MIDDLE EAST: URBAN AIR MOBILITY MARKET, BY COUNTRY, 2031-2035 (USD MILLION)

- TABLE 354 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 355 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 356 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 357 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 358 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 359 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 360 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 361 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 362 SAUDI ARABIA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 363 UAE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 364 UAE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 365 UAE: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 366 UAE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 367 UAE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 368 UAE: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 369 UAE: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 370 UAE: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 371 UAE: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 372 TURKEY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 373 TURKEY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 374 TURKEY: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 375 TURKEY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 376 TURKEY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 377 TURKEY: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 378 TURKEY: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 379 TURKEY: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 380 TURKEY: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 381 AFRICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2020-2023 (USD MILLION)

- TABLE 382 AFRICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2030 (USD MILLION)

- TABLE 383 AFRICA: URBAN AIR MOBILITY MARKET, BY SOLUTION, 2031-2035 (USD MILLION)

- TABLE 384 AFRICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2020-2023 (USD MILLION)

- TABLE 385 AFRICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2030 (USD MILLION)

- TABLE 386 AFRICA: URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2031-2035 (USD MILLION)

- TABLE 387 AFRICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2020-2023 (USD MILLION)

- TABLE 388 AFRICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2030 (USD MILLION)

- TABLE 389 AFRICA: URBAN AIR MOBILITY MARKET, BY RANGE, 2031-2035 (USD MILLION)

- TABLE 390 KEY STRATEGIES ADOPTED BY KEY PLAYERS, 2023

- TABLE 391 URBAN AIR MOBILITY MARKET: DEGREE OF COMPETITION

- TABLE 392 URBAN AIR MOBILITY MARKET: COMPANY SOLUTION FOOTPRINT

- TABLE 393 URBAN AIR MOBILITY MARKET: COMPANY RANGE FOOTPRINT

- TABLE 394 URBAN AIR MOBILITY MARKET: COMPANY MODE OF OPERATION FOOTPRINT

- TABLE 395 URBAN AIR MOBILITY MARKET: COMPANY REGION FOOTPRINT

- TABLE 396 URBAN AIR MOBILITY MARKET: LIST OF STARTUPS/SMES

- TABLE 397 URBAN AIR MOBILITY MARKET: COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 398 URBAN AIR MOBILITY MARKET: PRODUCT LAUNCHES AND DEVELOPMENTS, JANUARY 2021-JULY 2024

- TABLE 399 URBAN AIR MOBILITY MARKET: DEALS, JANUARY 2021-JULY 2024

- TABLE 400 URBAN AIR MOBILITY MARKET: OTHER DEVELOPMENTS, JANUARY 2021-JULY 2024

- TABLE 401 AIRBUS: COMPANY OVERVIEW

- TABLE 402 AIRBUS: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 403 AIRBUS: PRODUCT LAUNCHES

- TABLE 404 AIRBUS: DEALS

- TABLE 405 EVE HOLDING, INC.: COMPANY OVERVIEW

- TABLE 406 EVE HOLDING, INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 407 EVE HOLDING, INC.: DEALS

- TABLE 408 VERTICAL AEROSPACE: COMPANY OVERVIEW

- TABLE 409 VERTICAL AEROSPACE: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 410 VERTICAL AEROSPACE: DEALS

- TABLE 411 VERTICAL AEROSPACE: OTHER DEVELOPMENTS

- TABLE 412 EHANG: COMPANY OVERVIEW

- TABLE 413 EHANG: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 414 EHANG: DEALS

- TABLE 415 EHANG: OTHERS

- TABLE 416 ARCHER AVIATION INC.: COMPANY OVERVIEW

- TABLE 417 ARCHER AVIATION INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 418 ARCHER AVIATION INC.: DEALS

- TABLE 419 ARCHER AVIATION INC.: OTHER DEVELOPMENTS

- TABLE 420 TEXTRON INC.: COMPANY OVERVIEW

- TABLE 421 TEXTRON INC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 422 TEXTRON INC.: DEALS

- TABLE 423 TEXTRON INC.: OTHER DEVELOPMENTS

- TABLE 424 JOBY AVIATION: COMPANY OVERVIEW

- TABLE 425 JOBY AVIATION: SERVICES/SOLUTIONS OFFERED

- TABLE 426 JOBY AVIATION: DEALS

- TABLE 427 JOBY AVIATION: OTHER DEVELOPMENTS

- TABLE 428 FERROVIAL: COMPANY OVERVIEW

- TABLE 429 FERROVIAL: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 430 FERROVIAL: DEALS

- TABLE 431 FERROVIAL: OTHER DEVELOPMENTS

- TABLE 432 SKYPORTS INFRASTRUCTURE LIMITED: COMPANY OVERVIEW

- TABLE 433 SKYPORTS INFRASTRUCTURE LIMITED: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 434 SKYPORTS INFRASTRUCTURE LIMITED: DEALS

- TABLE 435 SKYPORTS INFRASTRUCTURE LIMITED: OTHERS

- TABLE 436 WISK AERO LLC: COMPANY OVERVIEW

- TABLE 437 WISK AERO LLC: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 438 WISK AERO LLC: DEALS

- TABLE 439 WISK AERO LLC: OTHER DEVELOPMENTS

- TABLE 440 JAUNT AIR MOBILITY LLC.: COMPANY OVERVIEW

- TABLE 441 JAUNT AIR MOBILITY LLC.: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 442 JAUNT AIR MOBILITY LLC.: DEALS

- TABLE 443 LILIUM GMBH: COMPANY OVERVIEW

- TABLE 444 LILIUM GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 445 LILIUM GMBH: DEALS

- TABLE 446 LILIUM GMBH: OTHER DEVELOPMENTS

- TABLE 447 WINGCOPTER: COMPANY OVERVIEW

- TABLE 448 WINGCOPTER: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 449 WINGCOPTER: DEALS

- TABLE 450 WINGCOPTER: OTHER DEVELOPMENTS

- TABLE 451 BETA TECHNOLOGIES: COMPANY OVERVIEW

- TABLE 452 BETA TECHNOLOGIES: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 453 BETA TECHNOLOGIES: DEALS

- TABLE 454 BETA TECHNOLOGIES: OTHER DEVELOPMENTS

- TABLE 455 VOLOCOPTER GMBH: COMPANY OVERVIEW

- TABLE 456 VOLOCOPTER GMBH: PRODUCTS/SOLUTIONS/SERVICES OFFERED

- TABLE 457 VOLOCOPTER GMBH: DEALS

- TABLE 458 VOLOCOPTER GMBH: OTHER DEVELOPMENTS

- TABLE 459 ARC AERO SYSTEMS: COMPANY OVERVIEW

- TABLE 460 SKYDRIVE INC.: COMPANY OVERVIEW

- TABLE 461 ELECTRA.AERO: COMPANY OVERVIEW

- TABLE 462 AUTOFLIGHT: COMPANY OVERVIEW

- TABLE 463 OVERAIR, INC.: COMPANY OVERVIEW

- TABLE 464 MANTA AIRCRAFT: COMPANY OVERVIEW

- TABLE 465 AIR VEV LTD: COMPANY OVERVIEW

- TABLE 466 URBAN AERONAUTICS LTD.: COMPANY OVERVIEW

- TABLE 467 SKYRYSE, INC.: COMPANY OVERVIEW

- TABLE 468 ASCENDANCE FLIGHT TECHNOLOGIES S.A.S.: COMPANY OVERVIEW

List of Figures

- FIGURE 1 URBAN AIR MOBILITY MARKET SEGMENTATION

- FIGURE 2 RESEARCH PROCESS FLOW

- FIGURE 3 RESEARCH DESIGN

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS

- FIGURE 5 BOTTOM-UP APPROACH

- FIGURE 6 TOP-DOWN APPROACH

- FIGURE 7 DATA TRIANGULATION

- FIGURE 8 INTERCITY (>100 KM) SEGMENT TO HOLD LEADING MARKET SHARE IN 2024

- FIGURE 9 AIR TAXIS TO SURPASS OTHER SEGMENTS DURING FORECAST PERIOD

- FIGURE 10 PLATFORM TO HOLD LARGER MARKET SHARE THAN INFRASTRUCTURE BETWEEN 2024 AND 2035

- FIGURE 11 NORTH AMERICA TO REGISTER HIGHEST CAGR DURING FORECAST PERIOD

- FIGURE 12 NEED FOR ALTERNATIVE MODES OF TRANSPORTATION IN URBAN AREAS TO DRIVE MARKET

- FIGURE 13 RIDESHARING COMPANIES TO SECURE MAXIMUM MARKET SHARE DURING FORECAST PERIOD

- FIGURE 14 PILOTED SEGMENT TO RECORD LARGER MARKET SHARE THAN AUTONOMOUS SEGMENT BY 2035

- FIGURE 15 UK TO BE FASTEST-GROWING COUNTRY-LEVEL MARKET DURING FORECAST PERIOD

- FIGURE 16 URBAN AIR MOBILITY MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- FIGURE 17 VALUE CHAIN ANALYSIS

- FIGURE 18 URBAN AIR MOBILITY MARKET ECOSYSTEM

- FIGURE 19 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 20 TOP 10 IMPORTING COUNTRIES, 2019-2023 (USD THOUSAND)

- FIGURE 21 TOP 10 EXPORTING COUNTRIES, 2019-2023 (USD THOUSAND)

- FIGURE 22 CERTIFICATION PROCESS FOR URBAN AIR MOBILITY VEHICLES

- FIGURE 23 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS, BY SOLUTION

- FIGURE 24 KEY BUYING CRITERIA FOR URBAN AIR MOBILITY, BY SOLUTION

- FIGURE 25 MACROECONOMIC OUTLOOK FOR NORTH AMERICA, EUROPE, ASIA PACIFIC, AND MIDDLE EAST

- FIGURE 26 MACROECONOMIC OUTLOOK FOR LATIN AMERICA AND AFRICA

- FIGURE 27 BILL OF MATERIALS, BY PLATFORM

- FIGURE 28 BILL OF MATERIALS, BY URBAN AIR MOBILITY INFRASTRUCTURE

- FIGURE 29 TOTAL COST OF OWNERSHIP FOR URBAN AIR MOBILITY PLATFORM THROUGHOUT LIFE CYCLE

- FIGURE 30 TOTAL COST OF OWNERSHIP FOR URBAN AIR MOBILITY INFRASTRUCTURE THROUGHOUT LIFE CYCLE

- FIGURE 31 BUSINESS MODELS FOR URBAN AIR MOBILITY PLATFORM OPERATIONS

- FIGURE 32 BUSINESS MODELS FOR URBAN AIR MOBILITY INFRASTRUCTURE OPERATIONS

- FIGURE 33 INVESTMENT AND FUNDING SCENARIO, 2020-2024

- FIGURE 34 DEVELOPMENT POTENTIAL OF URBAN AIR MOBILITY FROM 2010 ONWARDS

- FIGURE 35 KEY URBAN AIR MOBILITY PLATFORM NOISE LEVELS

- FIGURE 36 KEY URBAN AIR MOBILITY PLATFORM TECHNOLOGY READINESS LEVEL

- FIGURE 37 KEY URBAN AIR MOBILITY PLATFORM SYSTEM SUPPLIER LANDSCAPE

- FIGURE 38 URBAN TRAFFIC MANAGEMENT DEVELOPMENT BY NASA

- FIGURE 39 FAA URBAN TRAFFIC MANAGEMENT DEVELOPMENT AND IMPLEMENTATION

- FIGURE 40 INDICATIVE PRICING ANALYSIS FOR URBAN AIR MOBILITY PLATFORM, BY KEY PLAYERS (USD MILLION)

- FIGURE 41 PRICING ANALYSIS: COMPARATIVE STUDY BETWEEN RANGE (KM) AND PRICE (USD MILLION)

- FIGURE 42 PRICING ANALYSIS: COMPARATIVE STUDY BETWEEN PRICE AND MTOW

- FIGURE 43 PRICING ANALYSIS: COMPARATIVE STUDY BETWEEN PRICE AND PASSENGER CAPACITY

- FIGURE 44 URBAN AIR MOBILITY MARKET: TECHNOLOGY ROADMAP

- FIGURE 45 URBAN AIR MOBILITY MARKET: EVOLUTION OF KEY TECHNOLOGIES

- FIGURE 46 AI/GENERATIVE AI LANDSCAPE

- FIGURE 47 AI/GENERATIVE AI ADOPTION IN TOP COUNTRIES FOR COMMERCIAL AVIATION

- FIGURE 48 SCENARIO ANALYSIS FOR EVTOL PLATFORMS FOR URBAN AIR MOBILITY

- FIGURE 49 LIST OF MAJOR PATENTS RELATED TO URBAN AIR MOBILITY MARKET

- FIGURE 50 URBAN AIR MOBILITY MARKET, BY SOLUTION, 2024-2035 (USD MILLION)

- FIGURE 51 URBAN AIR MOBILITY MARKET, BY PLATFORM ARCHITECTURE, 2024-2035 (USD MILLION)

- FIGURE 52 URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE, 2024-2035 (USD MILLION)

- FIGURE 53 URBAN AIR MOBILITY MARKET, BY END USER, 2024-2035 (USD MILLION)

- FIGURE 54 URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION, 2024-2035 (USD MILLION)

- FIGURE 55 URBAN AIR MOBILITY MARKET, BY RANGE, 2024-2035 (USD MILLION)

- FIGURE 56 NORTH AMERICA TO ACCOUNT FOR LARGEST SHARE OF URBAN AIR MOBILITY MARKET IN 2024

- FIGURE 57 NORTH AMERICA: URBAN AIR MOBILITY MARKET SNAPSHOT

- FIGURE 58 EUROPE: URBAN AIR MOBILITY MARKET SNAPSHOT

- FIGURE 59 ASIA PACIFIC: URBAN AIR MOBILITY MARKET SNAPSHOT

- FIGURE 60 LATIN AMERICA: URBAN AIR MOBILITY MARKET SNAPSHOT

- FIGURE 61 REST OF THE WORLD: URBAN AIR MOBILITY MARKET SNAPSHOT

- FIGURE 62 REVENUE ANALYSIS OF TOP 5 PLAYERS, 2021-2023

- FIGURE 63 MARKET SHARE ANALYSIS, 2023

- FIGURE 64 URBAN AIR MOBILITY MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS) BY PLATFORM, 2023

- FIGURE 65 URBAN AIR MOBILITY MARKET: COMPANY EVALUATION MATRIX (KEY PLAYERS), BY INFRASTRUCTURE, 2023

- FIGURE 66 URBAN AIR MOBILITY MARKET: COMPANY FOOTPRINT

- FIGURE 67 URBAN AIR MOBILITY MARKET: COMPANY EVALUATION MATRIX (STARTUPS/SMES), BY SOLUTION, 2023

- FIGURE 68 COMPANY VALUATION OF KEY PLAYERS, 2023

- FIGURE 69 EV/EBIDTA OF KEY PLAYERS, 2023

- FIGURE 70 AIRBUS: COMPANY SNAPSHOT

- FIGURE 71 WISK AERO LLC: COMPANY SNAPSHOT

The urban air mobility market is estimated to be USD 4.6 billion in 2024 and is projected to reach USD 23.5 billion by 2030, at a CAGR of 31.2% between 2024 and 2030, and USD 41.5 billion by 2035, at a CAGR of 12.1% from 2030 to 2035. The Platform Volumes are expected to grow from 61,479 units in 2024 to 519,370 in 2030 to 875,438 units in 2035.

| Scope of the Report | |

|---|---|

| Years Considered for the Study | 2020-2035 |

| Base Year | 2023 |

| Forecast Period | 2024-2035 |

| Units Considered | Value (USD Billion) |

| Segments | By solution, mobility type, platform architecture, range, mode of operation, end user |

| Regions covered | North America, Europe, APAC, RoW |

The key drivers of the UAM market include high demand for efficient urban mobility solutions to reduce congestion, technologically advanced propulsion through electric engines, autonomous systems, improved batteries, and significant venture capital and private investment. Supporting regulatory frameworks and infrastructural development of requirements such as vertiports and charging stations are the essential elements boosting the market. Further, with growing concerns about emissions and consumer interest in new, on-demand mobility options, environmental concerns and consumers' curiosity are fueling market growth.

"Platform segment is set to dominate the UAM market."

The contribution of the platform segment would, therefore, be the largest in the market in 2024. Actually, this segment is likely to dominate the UAM market since platforms play a critical role in deploying and operating air mobility solutions. Platforms consist of eVTOL aircraft with accompanying software; initial deployment and revenue from sales, leasing, and service are included. Their potential for integration with the current transportation infrastructure, the rapid pace of technological advance, and competitive, innovative capabilities secure the leading position of this segment in the market.

"Ride-sharing company by end user is estimated to grow at highest CAGR in forecast period."

Based on the end user, the ride-sharing company segment is expected to grow the most during the forecast period. UAM will likely be dominated by companies operating on ride sharing because this business model has shown the best capability of scaling up quickly; matching significant growth quickly and efficiently, their long history of dealing with huge fleets gives such corporations firm grounding in the marketplace based on these merits of experience. Besides, the existing brand name and customer loyalty significantly enhance market positioning. As these air mobility solutions become integrated, ride-sharing companies will utilize their existing infrastructure and operational experience to create larger implementations of seamless and novel transportation offerings, thereby propelling the UAM sector to significant growth.

"North America is expected to hold the highest market share in 2024."

Having the region lead the pace in innovation for the rest of the world in new concepts in urban transport and building the necessary infrastructure required for these innovations, North America maintains the largest share in the UAM market. The technology ecosystem is well-established in the region and with a strong entrepreneurial presence, development of UAM is very rapid.

Besides that, North America offers diversified geography, from varied urban and suburban environments to an ideal ground test of the UAM solution for various use cases and applications. Further, major companies in aerospace and automotive are based here; it remains a collaborative environment for the accelerated development and commercialization of UAM technologies.

The break-up of the profile of primary participants in the Urban Air Mobility market:

- By Company Type: Tier 1 - 35%, Tier 2 - 45%, and Tier 3 - 20%

- By Designation: C Level - 35%, Director Level - 25%, Others - 40%

- By Region: North America - 21%, Europe - 18%, Asia Pacific - 42%, Rest of the World - 19%,

include Lilium Aviation Gmbh (Germany), Archer Aviation Inc. (US), Eve Holdings, Inc. (Brazil), Airbus (France), and Ehang (China). These key players offer solutions applicable to various sectors and have well-equipped and strong distribution networks across North America, Europe, Asia Pacific, the Middle East, Africa, and Latin America.

Research Coverage:

The UAM market is segmented by solution platform and infrastructure. The platform is segmented into aerostructure, avionics, propulsion systems, electrical systems, and software. Infrastructure solution is segmented into vertiports, charging stations, traffic management, and maintenance facilities.

By Mobility type, the UAM market is segmented into Air Taxi, Air shuttle and Air Metro, Personal Aerial Vehicle, Air Ambulance & Medical Emergency Vehicle, and Cargo Air Vehicle (CAV),

By mode of operation, UAM arke is segmented into Piloted and Autonomous.

By Range, UAM market is segments into Intercity and Intracity

By End User, UAM market is segmented into Ride Sharing Companies, Scheduled Operators, E-Commerce Companies, Hospitals & Medical Agencies, and Private/Personal Operators.

By Platform architecture, UAM market is segmented into rotary wing, that includes helicopters and multicopters, Hybrid Wing, that includes Vectored thrust and Lift + Curise, and Fixed wing aircraft.

This report segments the Urban Air Mobility market across five key regions: North America, Europe, Asia Pacific, Latin America, and the rest of the world, along with their respective key countries. The report's scope includes in-depth information on significant factors, such as drivers, restraints, challenges, and opportunities that influence the growth of the Urban Air Mobility market.

A comprehensive analysis of major industry players has been conducted to provide insights into their business profiles, solutions, and services. This analysis also covers key aspects like agreements, collaborations, new product launches, contracts, expansions, acquisitions, and partnerships in the Urban Air Mobility market.

Reasons to buy this report:

This report is a valuable resource for market leaders and newcomers in the Urban Air Mobility market. It offers data that closely approximates revenue figures for the overall market and its subsegments. It equips stakeholders with a comprehensive understanding of the competitive landscape, facilitating informed decisions to enhance their market positioning and formulating effective go-to-market strategies. The report imparts valuable insights into the market dynamics, offering information on crucial factors such as drivers, restraints, challenges, and opportunities, enabling stakeholders to gauge the market's pulse.

The report provides insights on the following pointers:

- Analysis of the key driver (Rise in urban congestion), restraint (High Initial Investment), opportunities (Growing demand for shorter travel time and efficient transportation), and challenges (Cybersecurity concerns), several factors could contribute to an increase in the Urban Air Mobility market.

- Market Penetration: Comprehensive information on Urban Air Mobility solutions offered by the top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the Urban Air Mobility market

- Market Development: Comprehensive information about lucrative markets - the report analyses the Urban Air Mobility market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the Urban Air Mobility market

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players in the Urban Air Mobility market

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 YEARS CONSIDERED

- 1.4 INCLUSIONS AND EXCLUSIONS

- 1.5 CURRENCY CONSIDERED

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary sources

- 2.1.2.2 Key data from primary sources

- 2.1.1 SECONDARY DATA

- 2.2 FACTOR ANALYSIS

- 2.2.1 INTRODUCTION

- 2.2.2 DEMAND-SIDE INDICATORS

- 2.2.3 SUPPLY-SIDE INDICATORS

- 2.3 MARKET SIZE ESTIMATION

- 2.3.1 BOTTOM-UP APPROACH

- 2.3.1.1 Market size estimation and methodology

- 2.3.2 TOP-DOWN APPROACH

- 2.3.1 BOTTOM-UP APPROACH

- 2.4 DATA TRIANGULATION

- 2.5 RISK ASSESSMENT

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS

3 EXECUTIVE SUMMARY

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR PLAYERS IN URBAN AIR MOBILITY MARKET

- 4.2 URBAN AIR MOBILITY MARKET, BY END USER

- 4.3 URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION

- 4.4 URBAN AIR MOBILITY MARKET, BY COUNTRY

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Rise in urban congestion

- 5.2.1.2 Shift of rural population to urban areas

- 5.2.1.3 Technological advancements in battery technology and electric propulsion systems

- 5.2.1.4 Smart city initiatives

- 5.2.2 RESTRAINTS

- 5.2.2.1 High initial investment

- 5.2.2.2 Increase in urban airspace congestion

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Growing demand for shorter travel time and efficient transportation

- 5.2.3.2 Need for sustainable transportation solutions

- 5.2.4 CHALLENGES

- 5.2.4.1 Cybersecurity concerns

- 5.2.4.2 Lack of skilled labor

- 5.2.1 DRIVERS

- 5.3 VALUE CHAIN ANALYSIS

- 5.4 ECOSYSTEM ANALYSIS

- 5.4.1 PROMINENT COMPANIES

- 5.4.2 PRIVATE AND SMALL ENTERPRISES

- 5.4.3 END USERS

- 5.5 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- 5.6 TRADE ANALYSIS

- 5.6.1 IMPORT DATA STATISTICS

- 5.6.2 EXPORT DATA STATISTICS

- 5.7 REGULATORY LANDSCAPE

- 5.7.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.8 USE CASE ANALYSIS

- 5.8.1 UBER'S PARTNERSHIP WITH INDUSTRY LEADERS

- 5.8.2 AMU-LED PERFORMING REAL-LIFE UAM DEMONSTRATIONS AND FLIGHTS USING U-SPACE

- 5.8.3 EXTENSIVE TEST FLIGHTS BY AIRBUS

- 5.9 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.9.1 KEY STAKEHOLDERS IN BUYING PROCESS

- 5.9.2 BUYING CRITERIA

- 5.10 KEY CONFERENCES AND EVENTS, 2025

- 5.11 MACROECONOMIC OUTLOOK

- 5.11.1 INTRODUCTION

- 5.11.2 NORTH AMERICA

- 5.11.3 EUROPE

- 5.11.4 ASIA PACIFIC

- 5.11.5 MIDDLE EAST

- 5.11.6 LATIN AMERICA

- 5.11.7 AFRICA

- 5.12 BILL OF MATERIALS

- 5.12.1 BILL OF MATERIALS, BY PLATFORM

- 5.12.2 BILL OF MATERIALS, BY URBAN AIR MOBILITY INFRASTRUCTURE

- 5.13 TOTAL COST OF OWNERSHIP

- 5.13.1 TOTAL COST OF OWNERSHIP FOR URBAN AIR MOBILITY PLATFORM

- 5.13.2 TOTAL COST OF OWNERSHIP FOR URBAN AIR MOBILITY INFRASTRUCTURE

- 5.13.3 TOTAL COST OF OWNERSHIP COMPARISON, BY SOLUTION

- 5.13.3.1 For urban air mobility platform

- 5.13.3.2 For urban air mobility infrastructure

- 5.14 BUSINESS MODELS

- 5.14.1 BUSINESS MODELS FOR URBAN AIR MOBILITY PLATFORM OPERATIONS

- 5.14.2 BUSINESS MODELS FOR URBAN AIR MOBILITY INFRASTRUCTURE OPERATIONS

- 5.15 INVESTMENT AND FUNDING SCENARIO

- 5.16 ROADMAP FOR URBAN AIR MOBILITY MARKET

- 5.17 OPERATIONAL DATA

- 5.17.1 PLATFORM DATA

- 5.17.1.1 Key urban air mobility platform order books

- 5.17.1.2 Key urban air mobility platform noise levels

- 5.17.1.3 Key urban air mobility platform technology readiness level

- 5.17.1.4 Key urban air mobility platform system supplier landscape

- 5.17.2 INFRASTRUCTURE DATA

- 5.17.2.1 Stages of unmanned traffic management and unmanned aircraft system research, development, testing, and implementation

- 5.17.1 PLATFORM DATA

- 5.18 INDICATIVE PRICING ANALYSIS

- 5.18.1 INDICATIVE PRICING ANALYSIS FOR URBAN AIR MOBILITY PLATFORM, BY KEY PLAYERS

- 5.18.1.1 Pricing analysis: Comparative study of similar price range models (technology and feature)

- 5.18.2 PRICING ANALYSIS OF INFRASTRUCTURE AND PLATFORM

- 5.18.1 INDICATIVE PRICING ANALYSIS FOR URBAN AIR MOBILITY PLATFORM, BY KEY PLAYERS

- 5.19 TECHNOLOGY ROADMAP

- 5.20 IMPACT OF AI/GENERATIVE AI ON URBAN AIR MOBILITY MARKET

- 5.20.1 INTRODUCTION

- 5.20.2 ADOPTION OF AI/GENERATIVE AI IN TOP COUNTRIES FOR COMMERCIAL AVIATION

- 5.21 SCENARIO ANALYSIS FOR EVTOL PLATFORMS FOR URBAN AIR MOBILITY

- 5.21.1 OPTIMISTIC SCENARIO

- 5.21.2 OPTIMISTIC TO REALISTIC SCENARIO

- 5.21.3 PESSIMISTIC SCENARIO

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TECHNOLOGY TRENDS

- 6.2.1 PLATFORM

- 6.2.1.1 Hydrogen propulsion

- 6.2.1.2 Flight management systems (FMS)

- 6.2.1.3 Advanced materials and manufacturing techniques

- 6.2.2 INFRASTRUCTURE

- 6.2.2.1 Internet of Things (IoT)

- 6.2.2.2 Vertically integrated facilities

- 6.2.1 PLATFORM

- 6.3 TECHNOLOGY ANALYSIS

- 6.3.1 KEY TECHNOLOGIES

- 6.3.1.1 Electric propulsion and battery technology

- 6.3.1.2 Lift + cruise configuration

- 6.3.1.3 Urban air traffic management

- 6.3.2 COMPLEMENTARY TECHNOLOGIES

- 6.3.2.1 Robotics

- 6.3.2.2 Charging infrastructure

- 6.3.3 ADJACENT TECHNOLOGIES

- 6.3.3.1 Application development for urban air mobility

- 6.3.1 KEY TECHNOLOGIES

- 6.4 IMPACT OF MEGATRENDS

- 6.4.1 ARTIFICIAL INTELLIGENCE

- 6.4.2 SUSTAINABLE AVIATION FUEL

- 6.5 PATENT ANALYSIS

7 URBAN AIR MOBILITY MARKET, BY SOLUTION

- 7.1 INTRODUCTION

- 7.2 PLATFORM

- 7.2.1 PROPULSION SYSTEMS TO DRIVE SEGMENTAL GROWTH

- 7.2.2 AEROSTRUCTURES

- 7.2.3 AVIONICS

- 7.2.3.1 Flight control systems

- 7.2.3.2 Navigation systems

- 7.2.3.3 Communications systems

- 7.2.3.4 Sensors

- 7.2.3.4.1 Speed sensors

- 7.2.3.4.2 Light sensors

- 7.2.3.4.3 Proximity sensors

- 7.2.3.4.4 Position sensors

- 7.2.3.4.5 Temperature sensors

- 7.2.4 PROPULSION SYSTEMS

- 7.2.4.1 Electric Batteries

- 7.2.4.2 Solar cells

- 7.2.4.3 Fuel cells

- 7.2.4.4 Hybrid electric

- 7.2.4.5 Fuel-powered

- 7.2.5 ELECTRICAL SYSTEMS

- 7.2.5.1 Generators

- 7.2.5.2 Motors

- 7.2.5.3 Electric actuators

- 7.2.5.4 Electric pumps

- 7.2.5.5 Distribution devices

- 7.2.6 SOFTWARE

- 7.3 INFRASTRUCTURE

- 7.3.1 VERTIPORTS TO LEAD SEGMENTAL GROWTH

- 7.3.2 CHARGING STATIONS

- 7.3.3 VERTIPORTS

- 7.3.4 AIR TRAFFIC MANAGEMENT FACILITIES

- 7.3.5 MAINTENANCE FACILITIES

8 URBAN AIR MOBILITY MARKET, BY PLATFORM ARCHITECTURE

- 8.1 INTRODUCTION

- 8.2 ROTARY WING

- 8.2.1 ABILITY TO OFFER DIRECT ACCESS TO CONGESTED AREAS TO DRIVE MARKET

- 8.2.2 HELICOPTERS

- 8.2.2.1 Jaunt Air Mobility Journey

- 8.2.2.2 Bell 407

- 8.2.3 MULTICOPTERS

- 8.2.3.1 Volocopter VoloCity

- 8.2.3.2 EHang 216

- 8.3 FIXED-WING HYBRID

- 8.3.1 ABILITY TO LEVERAGE EXISTING AIRPORT INFRASTRUCTURE TO DRIVE MARKET

- 8.3.2 LIFT + CRUISE

- 8.3.2.1 Eve

- 8.3.2.2 BETA Technologies Alia VTOL

- 8.3.3 VECTOR THRUST

- 8.3.3.1 Lilium Jet

- 8.3.3.2 Joby S4

- 8.3.3.3 Archer Midnight

- 8.4 FIXED WING

- 8.4.1 DEMAND FOR EFFICIENT AND LONG-RANGE TRANSPORTATION TO DRIVE MARKET

- 8.4.2 BETA TECHNOLOGIES ALIA CTOL

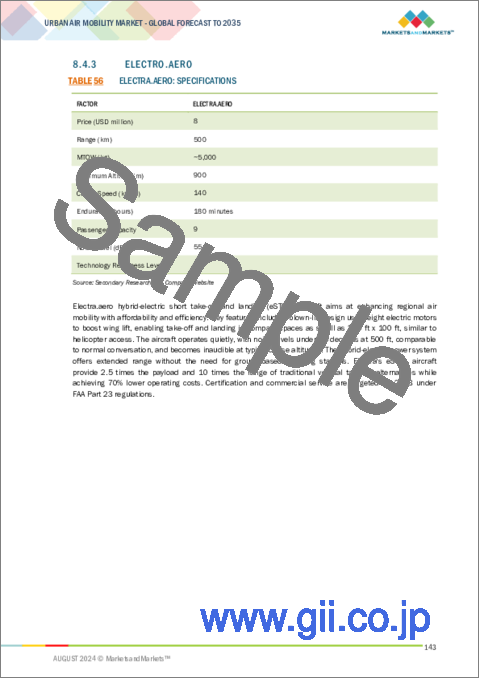

- 8.4.3 ELECTRO.AERO

9 URBAN AIR MOBILITY MARKET, BY MOBILITY TYPE

- 9.1 INTRODUCTION

- 9.2 AIR TAXIS

- 9.2.1 NEED FOR CONGESTION-FREE TRANSPORTATION IN URBAN ENVIRONMENTS TO DRIVE MARKET

- 9.2.2 MANNED TAXIS

- 9.2.3 DRONE TAXIS

- 9.3 AIR SHUTTLES & AIR METRO

- 9.3.1 GROWING URBAN POPULATION TO GENERATE DEMAND FOR AIR METRO

- 9.4 PERSONAL AIR VEHICLES

- 9.4.1 RISING DEMAND FOR ENHANCED PERSONAL MOBILITY TO DRIVE MARKET

- 9.5 CARGO AIR VEHICLES

- 9.5.1 GROWING FOCUS ON LIGHT AND HEAVY CARGO FOR INTERCITY AND INTRACITY DELIVERIES TO DRIVE MARKET

- 9.5.2 FIRST-MILE DELIVERY

- 9.5.3 MIDDLE-MILE DELIVERY

- 9.5.4 LAST-MILE DELIVERY

- 9.6 AIR AMBULANCES & MEDICAL EMERGENCY VEHICLES

- 9.6.1 NEED FOR RAPID MEDICAL RESPONSE TO DRIVE MARKET

10 URBAN AIR MOBILITY MARKET, BY END USER

- 10.1 INTRODUCTION

- 10.2 RIDESHARING COMPANIES

- 10.2.1 NEED FOR INNOVATIVE SOLUTIONS TO URBAN CONGESTION TO DRIVE MARKET

- 10.3 SCHEDULED OPERATORS

- 10.3.1 NEED FOR OFFER EFFICIENT, RELIABLE, AND SCALABLE TRANSPORTATION TO DRIVE MARKET

- 10.4 E-COMMERCE COMPANIES

- 10.4.1 NEED FOR SPEED AND EFFICIENCY IN DELIVERY SERVICES TO DRIVE MARKET

- 10.5 HOSPITALS & MEDICAL AGENCIES

- 10.5.1 EMERGENCE OF AIR AMBULANCES TO DRIVE MARKET

- 10.6 PRIVATE OPERATORS

- 10.6.1 DEMAND FOR TIME-EFFICIENT TRAVEL TO DRIVE MARKET

11 URBAN AIR MOBILITY MARKET, BY MODE OF OPERATION

- 11.1 INTRODUCTION

- 11.2 PILOTED

- 11.2.1 TRADITIONAL AVIATION WITH MODERN ELECTRIC PROPULSION AND VERTICAL TAKE-OFF CAPABILITIES

- 11.3 AUTONOMOUS

- 11.3.1 CONTINUOUS IMPROVEMENTS IN ARTIFICIAL INTELLIGENCE AND SENSOR TECHNOLOGIES

- 11.3.2 REMOTELY/OPTIONALLY PILOTED

- 11.3.3 FULLY AUTONOMOUS

12 URBAN AIR MOBILITY MARKET, BY RANGE

- 12.1 INTRODUCTION

- 12.2 INTERCITY (>100 KM)

- 12.2.1 ADVANCEMENT IN BATTERY TECHNOLOGY AND HYBRID PROPULSION SYSTEMS TO DRIVE MARKET

- 12.3 INTRACITY (<100 KM)

- 12.3.1 DEVELOPMENT OF VERTIPORTS TO SPUR DEMAND FOR INTRACITY TRANSPORTATION

13 URBAN AIR MOBILITY MARKET, BY REGION

- 13.1 INTRODUCTION

- 13.2 NORTH AMERICA

- 13.2.1 INTRODUCTION

- 13.2.2 PESTLE ANALYSIS

- 13.2.3 US

- 13.2.3.1 Development of eVTOL aircraft to drive market

- 13.2.4 CANADA

- 13.2.4.1 Government initiatives to reduce greenhouse gas emissions to drive market

- 13.3 EUROPE

- 13.3.1 INTRODUCTION

- 13.3.2 PESTLE ANALYSIS

- 13.3.3 UK

- 13.3.3.1 Substantial funding and strategic partnerships to drive market

- 13.3.4 FRANCE

- 13.3.4.1 Establishment of multiple vertiports across Paris to drive market

- 13.3.5 GERMANY

- 13.3.5.1 Well-established aerospace and automotive industries to drive market

- 13.3.6 ITALY

- 13.3.6.1 Strong tourism sector to drive market

- 13.3.7 SWITZERLAND

- 13.3.7.1 Emphasis on R&D of new technologies to drive market

- 13.3.8 SPAIN

- 13.3.8.1 Expertise in aerospace engineering to drive market

- 13.3.9 IRELAND

- 13.3.9.1 Supportive regulatory environment to advance UAM technologies to drive market

- 13.3.10 BELGIUM

- 13.3.10.1 Advancement in aerospace technologies to drive market

- 13.4 ASIA PACIFIC

- 13.4.1 INTRODUCTION

- 13.4.2 PESTLE ANALYSIS

- 13.4.3 CHINA

- 13.4.3.1 Strategic government support to drive market

- 13.4.4 INDIA

- 13.4.4.1 Rise in demand for efficient urban transportation solutions to drive market

- 13.4.5 JAPAN

- 13.4.5.1 Focus on advanced technological capabilities to drive market

- 13.4.6 SOUTH KOREA

- 13.4.6.1 Government-driven strategic roadmaps and substantial investments to drive market

- 13.4.7 AUSTRALIA

- 13.4.7.1 Enhancement of regional connectivity and improving access to remote areas to drive market

- 13.4.8 SINGAPORE

- 13.4.8.1 Investment in developing cutting-edge transportation solutions to drive market

- 13.4.9 INDONESIA

- 13.4.9.1 Innovative transportation solutions to improve connectivity to drive market

- 13.5 LATIN AMERICA

- 13.5.1 INTRODUCTION

- 13.5.2 PESTLE ANALYSIS

- 13.5.3 BRAZIL

- 13.5.3.1 Demand for innovative and efficient transportation solutions to drive market

- 13.5.4 MEXICO

- 13.5.4.1 Strength of public-private partnerships to drive market

- 13.5.5 ARGENTINA

- 13.5.5.1 Green transportation projects to drive market

- 13.5.6 COSTA RICA

- 13.5.6.1 Integration of innovative transportation solutions to drive market

- 13.6 REST OF THE WORLD

- 13.6.1 INTRODUCTION

- 13.6.2 MIDDLE EAST

- 13.6.2.1 Economic diversification and technological innovation to drive market.

- 13.6.2.2 Gulf Cooperation Council (GCC)

- 13.6.2.2.1 Saudi Arabia

- 13.6.2.2.2 UAE

- 13.6.2.3 Turkey

- 13.6.2.3.1 Strategic investment in aerospace industry to drive market

- 13.6.3 AFRICA

- 13.6.3.1 Growing middle-class population and increasing air travel demand to drive market

14 COMPETITIVE LANDSCAPE

- 14.1 INTRODUCTION

- 14.2 KEY PLAYER STRATEGIES/RIGHT TO WIN

- 14.3 REVENUE ANALYSIS

- 14.4 MARKET SHARE ANALYSIS

- 14.5 COMPANY EVALUATION MATRIX: KEY PLAYERS (BY PLATFORM), 2023

- 14.5.1 STARS

- 14.5.2 EMERGING LEADERS

- 14.5.3 PERVASIVE PLAYERS

- 14.5.4 PARTICIPANTS

- 14.6 COMPANY EVALUATION MATRIX: KEY PLAYERS (BY INFRASTRUCTURE), 2023

- 14.6.1 STARS

- 14.6.2 EMERGING LEADERS

- 14.6.3 PERVASIVE PLAYERS

- 14.6.4 PARTICIPANTS

- 14.7 COMPANY FOOTPRINT

- 14.8 COMPANY EVALUATION MATRIX: STARTUPS/SMES (BY SOLUTION), 2023

- 14.8.1 PROGRESSIVE COMPANIES

- 14.8.2 RESPONSIVE COMPANIES

- 14.8.3 DYNAMIC COMPANIES

- 14.8.4 STARTING BLOCKS

- 14.8.5 COMPETITIVE BENCHMARKING: STARTUPS/SMES, 2023

- 14.9 COMPANY VALUATION AND FINANCIAL METRICS

- 14.10 COMPETITIVE SCENARIO

- 14.11 MARKET EVALUATION FRAMEWORK

- 14.11.1 PRODUCT LAUNCHES AND DEVELOPMENTS

- 14.11.2 DEALS

- 14.11.3 OTHER DEVELOPMENTS

- 14.12 BRAND COMPARISON

15 COMPANY PROFILES

- 15.1 KEY PLAYERS

- 15.1.1 AIRBUS

- 15.1.1.1 Business overview

- 15.1.1.2 Products/Solutions/Services offered

- 15.1.1.3 Recent developments

- 15.1.1.4 MnM view

- 15.1.1.4.1 Key strengths

- 15.1.1.4.2 Strategic choices

- 15.1.1.4.3 Weaknesses and competitive threats

- 15.1.2 EVE HOLDING, INC.

- 15.1.2.1 Business overview

- 15.1.2.2 Products/Solutions/Services offered

- 15.1.2.3 Recent developments

- 15.1.2.4 MnM view

- 15.1.2.4.1 Key strengths

- 15.1.2.4.2 Strategic choices

- 15.1.2.4.3 Weaknesses and competitive threats

- 15.1.3 VERTICAL AEROSPACE

- 15.1.3.1 Business overview

- 15.1.3.2 Products/Solutions/Services offered

- 15.1.3.3 Recent developments

- 15.1.3.4 MnM view

- 15.1.3.4.1 Key strengths

- 15.1.3.4.2 Strategic choices

- 15.1.3.4.3 Weaknesses and competitive threats

- 15.1.4 EHANG

- 15.1.4.1 Business overview

- 15.1.4.2 Products/Solutions/Services offered

- 15.1.4.3 Recent developments

- 15.1.4.4 MnM view

- 15.1.4.4.1 Key strengths

- 15.1.4.4.2 Strategic choices

- 15.1.4.4.3 Weaknesses and competitive threats

- 15.1.5 ARCHER AVIATION INC.

- 15.1.5.1 Business overview

- 15.1.5.2 Products/Solutions/Services offered

- 15.1.5.3 Recent developments

- 15.1.5.4 MnM view

- 15.1.5.4.1 Key strengths

- 15.1.5.4.2 Strategic choices

- 15.1.5.4.3 Weaknesses and competitive threats

- 15.1.6 TEXTRON INC.

- 15.1.6.1 Business overview

- 15.1.6.2 Products/Solutions/Services offered

- 15.1.6.3 Recent developments

- 15.1.7 JOBY AVIATION

- 15.1.7.1 Business overview

- 15.1.7.2 Products/Solutions/Services offered

- 15.1.7.3 Recent developments

- 15.1.8 FERROVIAL

- 15.1.8.1 Business overview

- 15.1.8.2 Products/Solutions/Services offered

- 15.1.8.3 Recent developments

- 15.1.9 SKYPORTS INFRASTRUCTURE LIMITED

- 15.1.9.1 Business overview

- 15.1.9.2 Products/Solutions/Services offered

- 15.1.10 WISK AERO LLC

- 15.1.10.1 Business overview

- 15.1.10.2 Products/Services/Solutions offered

- 15.1.10.3 Recent developments

- 15.1.11 JAUNT AIR MOBILITY LLC.

- 15.1.11.1 Business overview

- 15.1.11.2 Products/Solutions/Services offered

- 15.1.11.3 Recent developments

- 15.1.12 LILIUM GMBH

- 15.1.12.1 Business overview

- 15.1.12.2 Products/Solutions/Services offered

- 15.1.12.3 Recent developments

- 15.1.13 WINGCOPTER

- 15.1.13.1 Business overview

- 15.1.13.2 Products/Solutions/Services offered

- 15.1.13.3 Recent developments

- 15.1.14 BETA TECHNOLOGIES

- 15.1.14.1 Business overview

- 15.1.14.2 Products/Solutions/Services offered

- 15.1.14.3 Recent developments

- 15.1.15 VOLOCOPTER GMBH

- 15.1.15.1 Business overview

- 15.1.15.2 Products/Solutions/Services offered

- 15.1.15.3 Recent developments

- 15.1.1 AIRBUS

- 15.2 OTHER PLAYERS

- 15.2.1 ARC AERO SYSTEMS

- 15.2.2 SKYDRIVE INC.

- 15.2.3 ELECTRA.AERO

- 15.2.4 AUTOFLIGHT

- 15.2.5 OVERAIR, INC.

- 15.2.6 MANTA AIRCRAFT

- 15.2.7 AIR VEV LTD

- 15.2.8 URBAN AERONAUTICS LTD.

- 15.2.9 SKYRYSE, INC.

- 15.2.10 ASCENDANCE FLIGHT TECHNOLOGIES S.A.S.

16 APPENDIX

- 16.1 DISCUSSION GUIDE

- 16.2 COMPANY LONG LIST

- 16.3 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 16.4 CUSTOMIZATION OPTIONS

- 16.5 RELATED REPORTS

- 16.6 AUTHOR DETAILS