|

|

市場調査レポート

商品コード

1297940

腐食防止コーティングの世界市場:樹脂の種類別 (エポキシ、PU、アクリル、亜鉛、塩素化ゴム)・技術別 (水性、溶剤系、粉末)・最終用途別 (石油・ガス、船舶、インフラ、発電、水処理)・地域別の将来予測 (2028年まで)Corrosion Protection Coatings Market by Resin Type (Epoxy, PU, Acrylic, Zinc, Chlorinated Rubber), Technology (Water, Solvent, Powder), End-use (Oil & Gas, Marine, Infrastructure, Power Generation, Water Treatment), & Region - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 腐食防止コーティングの世界市場:樹脂の種類別 (エポキシ、PU、アクリル、亜鉛、塩素化ゴム)・技術別 (水性、溶剤系、粉末)・最終用途別 (石油・ガス、船舶、インフラ、発電、水処理)・地域別の将来予測 (2028年まで) |

|

出版日: 2023年06月21日

発行: MarketsandMarkets

ページ情報: 英文 289 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界の腐食防止コーティングの市場規模は、2023年の104億米ドルから2028年には124億米ドルに達し、2023年から2028年の間に3.5%のCAGRで成長すると予測されています。

腐食防止コーティング市場に関連する課題は、各国の国内系企業との競合の激化です。国内系企業は、研究開発 (R&D) イニシアチブを強化し、限られた地域に集中することで、徐々に優位に立とうとしています。彼らは地域市場のニーズと需要を見極め、用途に特化した製品でそれを満たしています。

"アクリル樹脂:樹脂の種類別で最も急成長するセグメント"

アクリル樹脂は、その優れた皮膜形成特性、耐久性、環境要因への耐性により、腐食防止コーティングに広く使用されています。これらの樹脂は、プライマー・トップコート・クリアシーラントなど様々な種類の塗料に配合することができ、金属表面を腐食から保護します。アクリル樹脂は水性塗料に配合することができ、VOC (揮発性有機化合物) の排出量が少なく、塗布が容易で、乾燥時間が早いなどの利点があります。水性アクリル塗料は環境にやさしく、大気質や安全性に関する厳しい規制に適合しています。

"最終用途産業別では、石油・ガスのセグメントが予測期間中に最大の市場シェアを獲得する"

石油・ガス産業では、腐食による設備やインフラの劣化を防ぐため、腐食防止コーティングが重要な役割を果たしています。湿気・腐食性の化学物質・高温にさらされるなど、過酷な使用条件下では腐食が大きな問題となります。腐食防止コーティングの選択は、使用環境、基材、要求される寿命、塗布方法など様々な要因によって決まります。特定の石油・ガス用途に適切なコーティングシステムを決定する際に、業界標準や規制も重要な役割を果たします。

"アジア太平洋:地域別で最大かつ最も急成長しているセグメント"

世界の腐食防止コーティング市場を地域別に見ると、アジア太平洋が最も速い速度で拡大しています。経済成長に続いて、石油化学、石油・ガス、インフラ、発電、工業などさまざまな分野への大規模な投資が主な原因となっています。また国際企業は、安価な労働力を利用し、現地市場の需要に応えるため、生産工場をアジア太平洋に移転しています。

アジア太平洋の中でも、中国・インド・日本・韓国は特に重要な国々です。中でも中国とインドは、世界的に最も急速に経済成長している国々です。さらに、この地域で急成長が見込まれる最終用途産業は、原子力発電、石油・ガス、自動車産業であり、そのため腐食防止コーティングの需要が高まっています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 腐食防止コーティング市場の概要

- 腐食防止コーティングを選択する際に考慮される要素

- バリューチェーンの概要

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- ポーターのファイブフォース分析

- 主要な利害関係者と購入基準

- マクロ経済指標

- 技術概要

- ケーススタディ

- 価格分析

- 輸出入 (EXIM) 貿易統計

- 市場の成長に影響を与える世界経済シナリオ

- エコシステムマップ

- 顧客のビジネスに影響を与える動向と混乱

- 規制状況と基準

- 関税と規制

- 規制機関、政府機関、その他の組織

- 特許分析

- 主な会議とイベント (2023年~2024年)

第6章 腐食防止コーティング市場:樹脂の種類別

- イントロダクション

- エポキシ

- ポリウレタン (PU)

- アクリル

- アルキド

- 亜鉛

- 塩素化ゴム

- その他の樹脂タイプ

第7章 腐食防止コーティング市場:技術別

- イントロダクション

- 溶剤系腐食防止コーティング

- 水性腐食防止コーティング

- 粉末ベース腐食防止コーティング

- その他の技術

第8章 腐食防止コーティング市場:最終用途産業別

- イントロダクション

- 船舶

- 石油・ガス

- 石油化学

- インフラ

- 発電

- 水処理

- その他の最終用途産業

第9章 腐食防止コーティング市場:地域別

- イントロダクション

- アジア太平洋

- 中国

- インド

- 日本

- 韓国

- インドネシア

- タイ

- その他のアジア太平洋

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- ドイツ

- 英国

- イタリア

- フランス

- トルコ

- その他の欧州

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- その他の中東・アフリカ

- 南米

- ブラジル

- アルゼンチン

- チリ

- その他の南米

第10章 競合情勢

- 概要

- 企業評価クアドラントマトリックス (2022年)

- 製品ポートフォリオの強み

- 中小企業評価クアドラントマトリックス (2022年)

- 市場シェア分析

- 収益分析

- 市場ランキング分析

- 競合シナリオ

- 競合ベンチマーキング

- 戦略的開発

第11章 企業プロファイル

- 主要企業

- THE SHERWIN-WILLIAMS COMPANY

- PPG INDUSTRIES INC.

- AKZONOBEL N.V.

- JOTUN A/S

- KANSAI PAINT CO., LTD.

- AXALTA COATING SYSTEMS LLC

- HEMPEL A/S

- CHUGOKU MARINE PAINTS LTD.

- NIPPON PAINT HOLDINGS CO., LTD.

- TEKNOS

- その他の企業

- NOROO PAINT & COATINGS

- DIAMOND VOGEL

- GREENKOTE PLC

- RENNER HERRMANN S.A.

- NYCOTE LABORATORIES CORPORATION

- O3 GROUP

- THE MAGNI GROUP, INC.

- SECOA METAL FINISHING

- EONCOAT, LLC

- DAI NIPPON TORYO CO., LTD.

- ADVANCED NANOTECH LAB

- HUISINS NEW MATERIAL TECHNOLOGY CO.

- BLUCHEM

- SK FORMULATIONS INDIA PVT. LTD.

- ANCATT INC.

第12章 付録

The Corrosion protection coatings market is projected to grow from USD 10.4 Billion in 2023 to USD 12.4 Billion by 2028, at a CAGR of 3.5% between 2023-2028. The challenges related to the Corrosion protection coatings market are increasing competition from local players. Local players are gradually gaining an edge through increased R&D initiatives and focus on limited geographic regions. They identify the needs and demands in the local market and fulfill them with application-specific products.

"Acrylic resin is estimated to be the fastest growing segment in the Corrosion Protection Coatings market."

Acrylic resins are commonly used in corrosion protection coatings due to their excellent film-forming properties, durability, and resistance to environmental factors. These resins can be formulated into various types of coatings, such as primers, topcoats, and clear sealants, to provide protection for metal surfaces against corrosion. Acrylic resins can be formulated into water-based coatings, which offer advantages such as low VOC (volatile organic compound) emissions, ease of application, and fast drying times. Waterborne acrylic coatings are environmentally friendly and comply with strict regulations regarding air quality and safety.

"Oil & Gas end-use industry to gain the maximum market share during the forecast period."

Corrosion protection coatings play a crucial role in the oil and gas industry to prevent the degradation of equipment and infrastructure caused by corrosion. The harsh operating conditions, including exposure to moisture, aggressive chemicals, and high temperatures, make corrosion a significant concern. The selection of corrosion protection coatings depends on various factors, including the operating environment, substrate material, required lifespan, and application method. Industry standards and regulations also play a significant role in determining the appropriate coating systems for specific oil and gas applications.

"Asia Pacific is estimated to be the largest and fastest-growing segment of the Corrosion protection coatings market."

The global market for corrosion protection coatings is expanding at the quickest rate in Asia Pacific. Economic growth, followed by significant investment in a variety of sectors, including petrochemical, oil & gas, infrastructure, power generation, and industrial, are primarily responsible for this. The most potential market is in Asia Pacific, and it is likely to be the case in the foreseeable future. Additionally, to take advantage of the cheap labour and meet local market demand, international businesses are moving their production plants to Asia Pacific.

China, India, Japan, and South Korea are important nations in the Asia Pacific market. based on the IMF (International Monetary Fund). The economies of China and India are among the ones expanding the quickest globally. Additionally end-use industries that are anticipated to have rapid growth in the region are the nuclear power, oil & gas, and automotive industries, subsequently rising demand for Corrosion Protection Coatings.

Extensive primary interviews have been conducted, and information has been gathered from secondary research to determine and verify the market size of several segments and sub-segments.

Breakdown of Primary Interviews:

- By Company Type: Tier 1 - 46%, Tier 2 - 43%, and Tier 3 - 27%

- By Designation: D Level - 23%, C Level - 21%, and Others - 56%

- By Region: North America - 37%, Asia Pacific - 26%, Europe - 23%, Middle East & Africa - 10%, and South America - 4%, and

The key companies profiled in this report are Akzo Nobel NV (Netherlands), PPG Industries, Inc. (US), Jotun A/S (Norway), The Sherwin-Williams Company (US), and Kansai Paint Co., Ltd. (Japan).

Research Coverage:

Corrosion protection coatings Market by Resin Type (Epoxy, PU, Acrylic, Zinc, Chlorinated Rubber), by Technology (Water-based, Solvent-based, Powder), by End-use (Oil & Gas, Marine, Petrochemical, Infrastructure, Power Generation, Water Treatment), and Region (North America, Europe, Asia Pacific, South America, and Middle East & Africa).

Reasons to Buy the Report

From an insight perspective, this research report focuses on various levels of analyses - industry analysis (industry trends), market share analysis of top players, and company profiles, which together comprise and discuss the basic views on the competitive landscape, emerging and high-growth segments of the market; high growth regions; and market drivers, restraints, opportunities, and challenges.

The report provides insights on the following pointers:

- Analysis of Market Drivers (Increasing losses and damage due to corrosion, Increasing need for efficient processes and longer life of equipment, Innovations in modern structures, Growth in end-use industries), Restraints (Stringent environmental regulations, High prices of raw materials and energy), Opportunities (Demand for high-efficiency high performance corrosion protection coatings, Emerging countries offer significant growth opportunities), Challenges (Challenges from local players, Rise in use of substitutes)

- Market Penetration: Comprehensive information on Corrosion protection coatings offered by top players in the market

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product launches in the market

- Market Development: Comprehensive information about lucrative emerging markets - the report analyzes the market for Corrosion protection coatings across regions

- Market Diversification: Exhaustive information about new products, untapped geographies, recent developments, and investments in the market

- Competitive Assessment: In-depth assessment of market shares, strategies, products, and manufacturing capabilities of leading players in the market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 STUDY SCOPE

- 1.3.1 MARKETS COVERED

- FIGURE 1 CORROSION PROTECTION COATINGS MARKET SEGMENTATION

- 1.3.2 REGIONS COVERED

- FIGURE 2 CORROSION PROTECTION COATINGS MARKET: GEOGRAPHIC SCOPE

- 1.3.3 INCLUSIONS AND EXCLUSIONS

- 1.3.4 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- 1.5 UNIT CONSIDERED

- 1.6 LIMITATIONS

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 3 CORROSION PROTECTION COATINGS MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Critical secondary inputs

- 2.1.1.2 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key primary data sources

- 2.1.2.2 Critical primary inputs

- 2.1.2.3 Key data from primary sources

- 2.1.2.4 Key industry insights

- 2.1.2.5 Breakdown of primary interviews

- 2.2 MARKET SIZE ESTIMATION APPROACH

- 2.2.1 TOP-DOWN APPROACH

- FIGURE 4 CORROSION PROTECTION COATINGS MARKET SIZE ESTIMATION: TOP-DOWN APPROACH

- FIGURE 5 CORROSION PROTECTION COATINGS MARKET SIZE ESTIMATION: BY VALUE

- FIGURE 6 CORROSION PROTECTION COATINGS MARKET SIZE ESTIMATION, BY REGION

- FIGURE 7 CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE

- FIGURE 8 CORROSION PROTECTION COATINGS MARKET SIZE ESTIMATION, BY TECHNOLOGY

- FIGURE 9 CORROSION PROTECTION COATINGS MARKET SIZE ESTIMATION, BOTTOM-UP APPROACH: BY END-USE INDUSTRY

- FIGURE 10 CORROSION PROTECTION COATINGS MARKET SIZE ESTIMATION, BY END-USE INDUSTRY

- 2.3 MARKET FORECAST APPROACH

- 2.3.1 SUPPLY-SIDE FORECAST

- FIGURE 11 CORROSION PROTECTION COATINGS MARKET: SUPPLY SIDE FORECAST

- FIGURE 12 METHODOLOGY FOR SUPPLY SIDE SIZING OF CORROSION PROTECTION COATINGS MARKET

- 2.3.2 DEMAND-SIDE FORECAST

- FIGURE 13 CORROSION PROTECTION COATINGS MARKET: DEMAND SIDE FORECAST

- 2.4 FACTOR ANALYSIS

- FIGURE 14 FACTOR ANALYSIS OF CORROSION PROTECTION COATINGS MARKET

- 2.5 DATA TRIANGULATION

- FIGURE 15 CORROSION PROTECTION COATINGS MARKET: DATA TRIANGULATION

- 2.6 RESEARCH ASSUMPTIONS

- 2.7 RESEARCH LIMITATIONS

- 2.8 GROWTH RATE ASSUMPTIONS/GROWTH FORECAST

- 2.9 IMPACT OF RECESSION

3 EXECUTIVE SUMMARY

- TABLE 1 CORROSION PROTECTION COATINGS MARKET SNAPSHOT, 2023 VS. 2028

- FIGURE 16 EPOXY SEGMENT TO DOMINATE CORROSION PROTECTION COATINGS MARKET BETWEEN 2023 AND 2028

- FIGURE 17 SOLVENT-BASED SEGMENT TO LEAD CORROSION PROTECTION COATINGS MARKET BETWEEN 2023 AND 2028

- FIGURE 18 OIL & GAS TO BE LARGEST END-USE INDUSTRY OF CORROSION PROTECTION COATINGS BETWEEN 2023 AND 2028

- FIGURE 19 ASIA PACIFIC TO BE FASTEST-GROWING CORROSION PROTECTION COATINGS MARKET BETWEEN 2023 AND 2028

4 PREMIUM INSIGHTS

- 4.1 SIGNIFICANT OPPORTUNITIES FOR PLAYERS IN CORROSION PROTECTION COATINGS MARKET

- FIGURE 20 CORROSION PROTECTION COATINGS MARKET TO WITNESS HIGH GROWTH IN INFRASTRUCTURE SEGMENT BETWEEN 2023 AND 2028

- 4.2 CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE

- FIGURE 21 EPOXY TO BE LARGEST SEGMENT BETWEEN 2023 AND 2028

- 4.3 CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY

- FIGURE 22 MARINE END-USE INDUSTRY SEGMENT TO LEAD CORROSION PROTECTION COATINGS MARKET DURING FORECAST PERIOD

- 4.4 CORROSION PROTECTION COATINGS MARKET, DEVELOPED VS. EMERGING ECONOMIES

- FIGURE 23 CHINA TO DOMINATE GLOBAL MARKET DURING FORECAST PERIOD

- 4.5 CORROSION PROTECTION COATINGS MARKET, BY KEY COUNTRY

- FIGURE 24 INDIA TO BE FASTEST-GROWING CORROSION PROTECTION COATINGS MARKET BETWEEN 2023 AND 2028

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- FIGURE 25 ROLE OF CORROSION PROTECTION COATINGS

- 5.2 OVERVIEW OF CORROSION PROTECTION COATINGS MARKET

- FIGURE 26 CORROSION PREVENTION METHODS

- 5.2.1 TYPES OF CORROSION

- 5.2.1.1 Galvanic corrosion

- 5.2.1.2 Stress corrosion

- 5.2.1.3 General corrosion

- 5.2.1.4 Localized corrosion

- 5.2.1.5 Caustic agent corrosion

- 5.3 FACTORS CONSIDERED WHILE SELECTING CORROSION PROTECTION COATINGS

- 5.3.1 TYPE OF SURFACE OR SUBSTRATE TO BE COATED

- 5.3.2 LIFE EXPECTANCY

- TABLE 2 CRITERIA FOR SELECTION OF CORROSION PROTECTION COATINGS BASED ON LIFE EXPECTANCY

- 5.3.3 EASE OF ACCESS

- 5.3.4 COMPLIANCE WITH LEGISLATIVE AND ENVIRONMENTAL REGULATIONS

- 5.4 VALUE CHAIN OVERVIEW

- 5.4.1 VALUE CHAIN ANALYSIS

- FIGURE 27 VALUE CHAIN ANALYSIS

- TABLE 3 SUPPLY CHAIN ECOSYSTEM

- 5.5 MARKET DYNAMICS

- FIGURE 28 DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES IN CORROSION PROTECTION COATINGS MARKET

- 5.5.1 DRIVERS

- 5.5.1.1 Increasing losses and damage due to corrosion

- 5.5.1.2 Increasing need for efficient processes and longer life of equipment

- 5.5.1.3 Innovation in modern structures

- 5.5.1.4 Growth in end-use industries

- 5.5.2 RESTRAINTS

- 5.5.2.1 Stringent environmental regulations

- 5.5.2.2 High price of raw materials and energy

- TABLE 4 RESIN PRICES

- 5.5.3 OPPORTUNITIES

- 5.5.3.1 Demand for high-efficiency high-performance corrosion protection coatings

- 5.5.3.2 Significant growth opportunities in emerging economies

- 5.5.4 CHALLENGES

- 5.5.4.1 Increasing competition from local players

- 5.5.4.2 Rise in use of substitutes

- 5.6 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 29 PORTER'S FIVE FORCES ANALYSIS

- TABLE 5 PORTER'S FIVE FORCES ANALYSIS

- 5.6.1 THREAT OF NEW ENTRANTS

- 5.6.2 THREAT OF SUBSTITUTES

- 5.6.3 BARGAINING POWER OF SUPPLIERS

- 5.6.4 BARGAINING POWER OF BUYERS

- 5.6.5 INTENSITY OF COMPETITIVE RIVALRY

- 5.7 KEY STAKEHOLDERS & BUYING CRITERIA

- 5.7.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 30 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS

- TABLE 6 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP INDUSTRIES (%)

- 5.7.2 BUYING CRITERIA

- FIGURE 31 KEY BUYING CRITERIA FOR CORROSION PROTECTION COATINGS

- TABLE 7 KEY BUYING CRITERIA FOR CORROSION PROTECTION COATINGS

- 5.8 MACROECONOMIC INDICATORS

- 5.8.1 INTRODUCTION

- 5.8.2 GDP TRENDS AND FORECAST

- TABLE 8 GDP TRENDS AND FORECAST, PERCENTAGE CHANGE

- 5.8.3 TRENDS AND FORECAST OF GLOBAL CONSTRUCTION INDUSTRY

- FIGURE 32 GLOBAL SPENDING IN CONSTRUCTION INDUSTRY, 2014-2035

- 5.8.4 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- FIGURE 33 TRENDS IN GLOBAL AUTOMOTIVE INDUSTRY

- 5.9 TECHNOLOGY OVERVIEW

- FIGURE 34 CORROSION PROTECTION COATING TECHNOLOGY

- 5.10 CASE STUDY

- 5.10.1 CORROSION PROTECTION COATINGS USED FOR PIPELINE IN NUCLEAR POWER PLANT

- 5.11 PRICING ANALYSIS

- 5.11.1 AVERAGE SELLING PRICE, BY REGION

- FIGURE 35 PRICING ANALYSIS, BY REGION, 2022

- 5.11.2 AVERAGE SELLING PRICE, BY END-USE INDUSTRY

- FIGURE 36 PRICING ANALYSIS, BY END-USE INDUSTRY, 2022

- 5.11.3 AVERAGE SELLING PRICE, BY TYPE

- FIGURE 37 PRICING ANALYSIS, BY TYPE, 2022

- 5.11.4 AVERAGE SELLING PRICE, BY KEY PLAYER

- FIGURE 38 PRICING ANALYSIS OF KEY PLAYERS, BY END-USE INDUSTRY, 2022

- 5.12 EXPORT AND IMPORT (EXIM) TRADE STATISTICS

- 5.12.1 KEY COUNTRIES

- TABLE 9 INTENSITY OF TRADE, BY KEY COUNTRY

- 5.12.2 EXPORT TRADE DATA

- TABLE 10 EXPORT DATA IN USD THOUSAND (2018-2022)

- 5.12.3 IMPORT TRADE DATA

- TABLE 11 IMPORT DATA IN USD THOUSAND (2018-2022)

- 5.13 GLOBAL ECONOMIC SCENARIO AFFECTING MARKET GROWTH

- 5.13.1 GLOBAL IMPACT OF RECESSION

- 5.13.1.1 North America

- 5.13.1.2 Europe

- 5.13.1.3 Asia Pacific

- 5.13.1 GLOBAL IMPACT OF RECESSION

- 5.14 ECOSYSTEM MAP

- FIGURE 39 PAINTS & COATINGS ECOSYSTEM

- 5.15 TRENDS AND DISRUPTIONS IMPACTING CUSTOMER BUSINESS

- FIGURE 40 TRENDS IN END-USE INDUSTRIES IMPACTING STRATEGIES OF COATINGS MANUFACTURERS

- 5.16 REGULATORY LANDSCAPE AND STANDARDS

- TABLE 12 CS-1, CS-3, CS-4, SS-1, SS-2, AND SS-3 CLASSIFICATIONS FOR CORROSION PROTECTION COATINGS MARKET

- TABLE 13 STANDARDS FOR CORROSION INSPECTION PRACTICES

- 5.17 TARIFFS & REGULATIONS

- 5.17.1 COATING STANDARD

- TABLE 14 BASIC COATING SYSTEM REQUIREMENTS FOR DEDICATED SEAWATER BALLAST TANKS OF ALL TYPES OF SHIPS AND DOUBLE-SIDE SKIN SPACES OF BULK CARRIERS OF 150 M AND UPWARDS:

- 5.18 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 15 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 REST OF THE WORLD: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 5.19 PATENT ANALYSIS

- 5.19.1 METHODOLOGY

- 5.19.2 PUBLICATION TRENDS

- FIGURE 41 PUBLICATION TRENDS, 2018-2023

- 5.19.3 INSIGHTS

- 5.19.4 JURISDICTION ANALYSIS

- FIGURE 42 JURISDICTION ANALYSIS OF REGISTERED PATENTS, 2018-2023

- 5.19.5 TOP APPLICANTS

- FIGURE 43 NUMBER OF PATENTS, BY COMPANY, 2018-2023

- 5.20 KEY CONFERENCES & EVENTS IN 2023-2024

- TABLE 19 DETAILED LIST OF CONFERENCES & EVENTS

6 CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE

- 6.1 INTRODUCTION

- FIGURE 44 EPOXY-BASED CORROSION PROTECTION COATINGS TO LEAD MARKET BETWEEN 2023 AND 2028

- TABLE 20 CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (USD MILLION)

- TABLE 21 CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- TABLE 22 CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (KILOTON)

- TABLE 23 CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (KILOTON)

- 6.2 EPOXY

- 6.2.1 SUPERIOR PROTECTIVE CHARACTERISTICS AND MODIFIABLE NATURE OF EPOXY

- TABLE 24 CHARACTERISTICS OF EPOXY CORROSION PROTECTION COATINGS

- TABLE 25 EPOXY CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 26 EPOXY CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 27 EPOXY CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 28 EPOXY CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

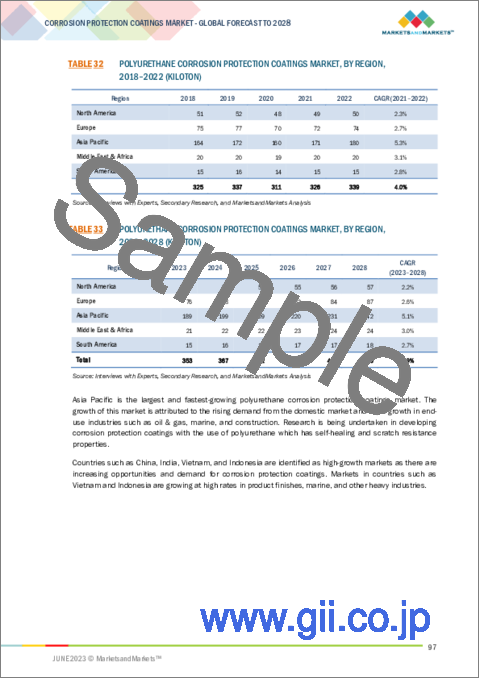

- 6.3 POLYURETHANE

- 6.3.1 GROWING DEMAND FOR POLYURETHANE RESINS IN HIGH-PERFORMANCE APPLICATIONS

- TABLE 29 PROPERTIES OF POLYURETHANE CORROSION PROTECTION COATINGS

- TABLE 30 POLYURETHANE CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 31 POLYURETHANE CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 32 POLYURETHANE CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 33 POLYURETHANE CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 6.4 ACRYLIC

- 6.4.1 SUPERIOR WEATHERING AND OXIDATION RESISTANCE PROPERTIES

- TABLE 34 CHARACTERISTICS OF ACRYLIC CORROSION PROTECTION COATINGS

- TABLE 35 ACRYLIC CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 36 ACRYLIC CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 37 ACRYLIC CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 38 ACRYLIC CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 6.5 ALKYD

- 6.5.1 LENIENT ENVIRONMENTAL REGULATIONS AND GROWTH OF END-USE INDUSTRIES IN ASIA PACIFIC

- TABLE 39 CHARACTERISTICS OF ALKYD CORROSION PROTECTION COATINGS

- TABLE 40 ALKYD CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 41 ALKYD CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 42 ALKYD CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 43 ALKYD CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 6.6 ZINC

- 6.6.1 STRINGENT REGULATIONS TO LIMIT USE OF ZINC-BASED COATINGS

- TABLE 44 CHARACTERISTICS OF ZINC CORROSION PROTECTION COATINGS

- TABLE 45 ZINC CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 46 ZINC CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 47 ZINC CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 48 ZINC CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 6.7 CHLORINATED RUBBER

- 6.7.1 SLOW GROWTH DUE TO VOC REGULATIONS IN NORTH AMERICA AND EUROPE

- TABLE 49 CHARACTERISTICS OF CHLORINATED RUBBER CORROSION PROTECTION COATINGS

- TABLE 50 CHLORINATED RUBBER CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 51 CHLORINATED RUBBER CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 52 CHLORINATED RUBBER CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 53 CHLORINATED RUBBER CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 6.8 OTHER RESIN TYPES

- TABLE 54 OTHER CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 55 OTHER CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 56 OTHER CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 57 OTHER CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

7 CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY

- 7.1 INTRODUCTION

- FIGURE 45 SOLVENT-BASED CORROSION PROTECTION COATINGS SEGMENT TO DOMINATE BETWEEN 2023 AND 2028

- TABLE 58 CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 59 CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 60 CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (KILOTON)

- TABLE 61 CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (KILOTON)

- 7.2 SOLVENT-BASED CORROSION PROTECTION COATINGS

- 7.2.1 EXCELLENT PROPERTIES TO DRIVE DEMAND

- TABLE 62 SOLVENT-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 63 SOLVENT-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 64 SOLVENT-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 65 SOLVENT-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.3 WATER-BASED CORROSION PROTECTION COATINGS

- 7.3.1 LOW TOXICITY DUE TO LOW-VOC LEVELS TO INCREASE DEMAND

- TABLE 66 WATER-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 67 WATER-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 68 WATER-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 69 WATER-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.4 POWDER-BASED CORROSION PROTECTION COATINGS

- 7.4.1 SUPERIOR PERFORMANCE AND EXCELLENT PROPERTIES TO DRIVE DEMAND

- TABLE 70 POWDER-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 71 POWDER-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 72 POWDER-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 73 POWDER-BASED CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 7.5 OTHER TECHNOLOGIES

- TABLE 74 OTHER TECHNOLOGIES IN CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 75 OTHER TECHNOLOGIES IN CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 76 OTHER TECHNOLOGIES IN CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 77 OTHER TECHNOLOGIES IN CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

8 CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY

- 8.1 INTRODUCTION

- FIGURE 46 OIL & GAS INDUSTRY TO LEAD CORROSION PROTECTION COATINGS MARKET DURING FORECAST PERIOD

- TABLE 78 CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 79 CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 80 CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 81 CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- 8.2 MARINE

- 8.2.1 DEMAND FOR LARGE VOLUMES OF COATINGS

- TABLE 82 CORROSION PROTECTION COATINGS MARKET SIZE IN MARINE INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 83 CORROSION PROTECTION COATINGS MARKET SIZE IN MARINE INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 84 CORROSION PROTECTION COATINGS MARKET SIZE IN MARINE INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 85 CORROSION PROTECTION COATINGS MARKET SIZE IN MARINE INDUSTRY, BY REGION, 2023-2028 (KILOTON)

- 8.3 OIL & GAS

- 8.3.1 RAPIDLY GROWING BIO-FUEL INDUSTRY

- TABLE 86 CORROSION PROTECTION COATINGS MARKET SIZE IN OIL & GAS INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 87 CORROSION PROTECTION COATINGS MARKET SIZE IN OIL & GAS INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 88 CORROSION PROTECTION COATINGS MARKET SIZE IN OIL & GAS INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 89 CORROSION PROTECTION COATINGS MARKET SIZE IN OIL & GAS INDUSTRY, BY REGION, 2023-2028 (KILOTON)

- 8.4 PETROCHEMICAL

- 8.4.1 INDIA AND CHINA DRIVING FORCES FOR MARKET

- TABLE 90 CORROSION PROTECTION COATINGS MARKET SIZE IN PETROCHEMICAL INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 91 CORROSION PROTECTION COATINGS MARKET SIZE IN PETROCHEMICAL INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 92 CORROSION PROTECTION COATINGS MARKET SIZE IN PETROCHEMICAL INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 93 CORROSION PROTECTION COATINGS MARKET SIZE IN PETROCHEMICAL INDUSTRY, BY REGION, 2023-2028 (KILOTON)

- 8.5 INFRASTRUCTURE

- 8.5.1 ASIA PACIFIC TO BE STRATEGIC INFRASTRUCTURE MARKET

- TABLE 94 CORROSION PROTECTION COATINGS MARKET SIZE IN INFRASTRUCTURE INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 95 CORROSION PROTECTION COATINGS MARKET SIZE IN INFRASTRUCTURE INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 96 CORROSION PROTECTION COATINGS MARKET SIZE IN INFRASTRUCTURE INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 97 CORROSION PROTECTION COATINGS MARKET SIZE IN INFRASTRUCTURE INDUSTRY, BY REGION, 2023-2028 (KILOTON)

- 8.6 POWER GENERATION

- 8.6.1 POWER GENERATION AMONG FASTEST-GROWING INDUSTRIES IN ASIA PACIFIC

- TABLE 98 CORROSION PROTECTION COATINGS MARKET SIZE IN POWER GENERATION INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 99 CORROSION PROTECTION COATINGS MARKET SIZE IN POWER GENERATION INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 100 CORROSION PROTECTION COATINGS MARKET SIZE IN POWER GENERATION INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 101 CORROSION PROTECTION COATINGS MARKET SIZE IN POWER GENERATION INDUSTRY, BY REGION, 2023-2028 (KILOTON)

- 8.7 WATER TREATMENT

- 8.7.1 INCREASING CONCERNS IN WATER DISPOSAL AND WATER CONSERVATION

- TABLE 102 CORROSION PROTECTION COATINGS MARKET SIZE IN WATER TREATMENT INDUSTRY, BY REGION, 2018-2022 (USD MILLION)

- TABLE 103 CORROSION PROTECTION COATINGS MARKET SIZE IN WATER TREATMENT INDUSTRY, BY REGION, 2023-2028 (USD MILLION)

- TABLE 104 CORROSION PROTECTION COATINGS MARKET SIZE IN WATER TREATMENT INDUSTRY, BY REGION, 2018-2022 (KILOTON)

- TABLE 105 CORROSION PROTECTION COATINGS MARKET SIZE IN WATER TREATMENT INDUSTRY, BY REGION, 2023-2028 (KILOTON)

- 8.8 OTHER END-USE INDUSTRIES

- TABLE 106 CORROSION PROTECTION COATINGS MARKET SIZE IN OTHER END-USE INDUSTRIES, BY REGION, 2018-2022 (USD MILLION)

- TABLE 107 CORROSION PROTECTION COATINGS MARKET SIZE IN OTHER END-USE INDUSTRIES, BY REGION, 2023-2028 (USD MILLION)

- TABLE 108 CORROSION PROTECTION COATINGS MARKET SIZE IN OTHER END-USE INDUSTRIES, BY REGION, 2018-2022 (KILOTON)

- TABLE 109 CORROSION PROTECTION COATINGS MARKET SIZE IN OTHER END-USE INDUSTRIES, BY REGION, 2023-2028 (KILOTON)

9 CORROSION PROTECTION COATINGS MARKET, BY REGION

- 9.1 INTRODUCTION

- 9.1.1 GLOBAL RECESSION OVERVIEW

- FIGURE 47 ASIA PACIFIC COUNTRIES EMERGING AS STRATEGIC LOCATIONS FOR CORROSION PROTECTION COATINGS MARKET

- TABLE 110 CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 111 CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 112 CORROSION PROTECTION COATINGS MARKET, BY REGION, 2018-2022 (KILOTON)

- TABLE 113 CORROSION PROTECTION COATINGS MARKET, BY REGION, 2023-2028 (KILOTON)

- 9.2 ASIA PACIFIC

- 9.2.1 IMPACT OF RECESSION ON ASIA PACIFIC

- FIGURE 48 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET SNAPSHOT

- TABLE 114 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (USD MILLION)

- TABLE 115 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- TABLE 116 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (KILOTON)

- TABLE 117 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (KILOTON)

- TABLE 118 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 119 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 120 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (KILOTON)

- TABLE 121 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (KILOTON)

- TABLE 122 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 123 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 124 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 125 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- TABLE 126 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 127 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 128 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 129 ASIA PACIFIC: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 9.2.2 CHINA

- 9.2.2.1 Strong manufacturing industries

- TABLE 130 UPCOMING MEGA PROJECTS IN CHINA

- 9.2.3 INDIA

- 9.2.3.1 Government's focus on manufacturing sector

- TABLE 131 UPCOMING MEGA PROJECTS IN INDIA

- 9.2.4 JAPAN

- 9.2.4.1 Presence of well-established industries

- TABLE 132 UPCOMING MEGA PROJECTS IN JAPAN

- 9.2.5 SOUTH KOREA

- 9.2.5.1 Marine industry among leading global industries

- 9.2.6 INDONESIA

- 9.2.6.1 Increasing investments to drive market

- 9.2.7 THAILAND

- 9.2.7.1 Manufacturing industry to contribute significantly to market growth

- 9.2.8 REST OF ASIA PACIFIC

- 9.3 NORTH AMERICA

- 9.3.1 IMPACT OF RECESSION ON NORTH AMERICA

- FIGURE 49 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET SNAPSHOT

- TABLE 133 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (USD MILLION)

- TABLE 134 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- TABLE 135 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (KILOTON)

- TABLE 136 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (KILOTON)

- TABLE 137 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 138 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 139 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (KILOTON)

- TABLE 140 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (KILOTON)

- TABLE 141 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 142 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 143 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 144 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- TABLE 145 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 146 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 147 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 148 NORTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- TABLE 149 UPCOMING MEGA PROJECTS IN NORTH AMERICA

- 9.3.2 US

- 9.3.2.1 Presence of major manufacturers

- 9.3.3 CANADA

- 9.3.3.1 Environmental regulations to play major role

- 9.3.4 MEXICO

- 9.3.4.1 Private investments, particularly in infrastructure, oil & gas, and energy sectors, to enhance economic growth

- 9.4 EUROPE

- 9.4.1 IMPACT OF RECESSION ON EUROPE

- FIGURE 50 EUROPE: CORROSION PROTECTION COATINGS MARKET SNAPSHOT

- TABLE 150 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (USD MILLION)

- TABLE 151 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- TABLE 152 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (KILOTON)

- TABLE 153 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (KILOTON)

- TABLE 154 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 155 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 156 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (KILOTON)

- TABLE 157 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (KILOTON)

- TABLE 158 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 159 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 160 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 161 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- TABLE 162 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 163 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 164 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 165 EUROPE: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 9.4.2 GERMANY

- 9.4.2.1 Leading manufacturer of machinery and chemicals

- 9.4.3 UK

- 9.4.3.1 Sustainable and quality products to increase demand

- 9.4.4 ITALY

- 9.4.4.1 New project finance rules and investment policies

- 9.4.5 FRANCE

- 9.4.5.1 Adoption of innovative technologies

- 9.4.6 TURKEY

- 9.4.6.1 Booming and highly attractive market

- 9.4.7 REST OF EUROPE

- 9.5 MIDDLE EAST & AFRICA

- 9.5.1 IMPACT OF RECESSION ON MIDDLE EAST & AFRICA

- FIGURE 51 SAUDI ARABIA TO BE LARGEST CORROSION PROTECTION COATINGS MARKET

- TABLE 166 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (USD MILLION)

- TABLE 167 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- TABLE 168 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (KILOTON)

- TABLE 169 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (KILOTON)

- TABLE 170 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 171 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 172 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (KILOTON)

- TABLE 173 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (KILOTON)

- TABLE 174 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 175 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 176 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 177 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- TABLE 178 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 179 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 180 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 181 MIDDLE EAST & AFRICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 9.5.2 SAUDI ARABIA

- 9.5.2.1 Increasing population and urbanization

- 9.5.3 UAE

- 9.5.3.1 Increasing focus on developing regulatory mechanisms and R&D capabilities

- 9.5.4 SOUTH AFRICA

- 9.5.4.1 Surge in demand for coated products

- 9.5.5 REST OF MIDDLE EAST & AFRICA

- 9.6 SOUTH AMERICA

- FIGURE 52 BRAZIL TO BE LARGEST AND FASTEST-GROWING MARKET

- TABLE 182 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (USD MILLION)

- TABLE 183 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (USD MILLION)

- TABLE 184 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2018-2022 (KILOTON)

- TABLE 185 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY RESIN TYPE, 2023-2028 (KILOTON)

- TABLE 186 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (USD MILLION)

- TABLE 187 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (USD MILLION)

- TABLE 188 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2018-2022 (KILOTON)

- TABLE 189 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY TECHNOLOGY, 2023-2028 (KILOTON)

- TABLE 190 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (USD MILLION)

- TABLE 191 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (USD MILLION)

- TABLE 192 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2018-2022 (KILOTON)

- TABLE 193 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY END-USE INDUSTRY, 2023-2028 (KILOTON)

- TABLE 194 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 195 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- TABLE 196 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2018-2022 (KILOTON)

- TABLE 197 SOUTH AMERICA: CORROSION PROTECTION COATINGS MARKET, BY COUNTRY, 2023-2028 (KILOTON)

- 9.6.1 BRAZIL

- 9.6.1.1 Easy availability of raw materials

- 9.6.2 ARGENTINA

- 9.6.2.1 Increased projects in infrastructure & construction industry

- 9.6.3 CHILE

- 9.6.3.1 Various sectors driving market demand

- 9.6.4 REST OF SOUTH AMERICA

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- TABLE 198 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS

- 10.2 COMPANY EVALUATION QUADRANT MATRIX, 2022

- 10.2.1 STARS

- 10.2.2 EMERGING LEADERS

- 10.2.3 PERVASIVE

- 10.2.4 PARTICIPANTS

- FIGURE 53 COMPANY EVALUATION MATRIX, 2022

- 10.3 STRENGTH OF PRODUCT PORTFOLIO

- 10.4 SMALL AND MEDIUM-SIZED ENTERPRISES EVALUATION QUADRANT MATRIX, 2022

- 10.4.1 PROGRESSIVE COMPANIES

- 10.4.2 RESPONSIVE COMPANIES

- 10.4.3 STARTING BLOCKS

- 10.4.4 DYNAMIC COMPANIES

- FIGURE 54 SMALL AND MEDIUM-SIZED ENTERPRISES' EVALUATION MATRIX, 2022

- 10.5 MARKET SHARE ANALYSIS

- FIGURE 55 MARKET SHARE, BY KEY PLAYERS (2022)

- 10.6 REVENUE ANALYSIS

- FIGURE 56 REVENUE ANALYSIS OF TOP PLAYERS, 2018-2022

- 10.6.1 AKZONOBEL NV

- 10.6.2 PPG INDUSTRIES, INC.

- 10.6.3 THE SHERWIN-WILLIAMS COMPANY

- 10.6.4 JOTUN A/S

- 10.7 MARKET RANKING ANALYSIS

- TABLE 199 MARKET RANKING ANALYSIS, 2022

- 10.8 COMPETITIVE SCENARIO

- 10.8.1 MARKET EVALUATION FRAMEWORK

- TABLE 200 COMPANY END-USE INDUSTRY FOOTPRINT

- TABLE 201 COMPANY REGION FOOTPRINT

- TABLE 202 COMPANY OVERALL FOOTPRINT

- 10.8.2 MARKET EVALUATION MATRIX

- TABLE 203 STRATEGIC DEVELOPMENTS, BY COMPANY

- TABLE 204 MOST FOLLOWED STRATEGIES

- TABLE 205 GROWTH STRATEGIES ADOPTED BY KEY COMPANIES

- 10.9 COMPETITIVE BENCHMARKING

- TABLE 206 DETAILED LIST OF KEY MARKET PLAYERS

- TABLE 207 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- 10.10 STRATEGIC DEVELOPMENTS

- TABLE 208 PRODUCT LAUNCHES, 2019-2023

- TABLE 209 DEALS, 2019-2023

11 COMPANY PROFILES

- (Business overview, Products offered, Recent Developments, MNM view)**

- 11.1 KEY PLAYERS

- 11.1.1 THE SHERWIN-WILLIAMS COMPANY

- TABLE 210 THE SHERWIN-WILLIAMS COMPANY: COMPANY OVERVIEW

- FIGURE 57 THE SHERWIN-WILLIAMS COMPANY: COMPANY SNAPSHOT

- TABLE 211 THE SHERWIN-WILLIAMS COMPANY: PRODUCT LAUNCHES

- TABLE 212 THE SHERWIN-WILLIAMS COMPANY: DEALS

- 11.1.2 PPG INDUSTRIES INC.

- TABLE 213 PPG INDUSTRIES INC.: COMPANY OVERVIEW

- FIGURE 58 PPG INDUSTRIES INC.: COMPANY SNAPSHOT

- TABLE 214 PPG INDUSTRIES INC.: PRODUCT LAUNCHES

- TABLE 215 PPG INDUSTRIES INC.: DEALS

- TABLE 216 PPG INDUSTRIES INC.: OTHERS

- 11.1.3 AKZONOBEL N.V.

- TABLE 217 AKZONOBEL N.V.: COMPANY OVERVIEW

- FIGURE 59 AKZONOBEL N.V.: COMPANY SNAPSHOT

- TABLE 218 AKZONOBEL N.V.: PRODUCT LAUNCHES

- TABLE 219 AKZONOBEL N.V.: DEALS

- TABLE 220 AKZONOBEL N.V.: OTHERS

- 11.1.4 JOTUN A/S

- TABLE 221 JOTUN A/S: COMPANY OVERVIEW

- FIGURE 60 JOTUN A/S: COMPANY SNAPSHOT

- TABLE 222 JOTUN A/S: DEALS

- TABLE 223 JOTUN A/S: OTHERS

- 11.1.5 KANSAI PAINT CO., LTD.

- TABLE 224 KANSAI PAINT CO. LTD.: COMPANY OVERVIEW

- FIGURE 61 KANSAI PAINT CO., LTD.: COMPANY SNAPSHOT

- TABLE 225 KANSAI PAINT CO., LTD.: DEALS

- 11.1.6 AXALTA COATING SYSTEMS LLC

- TABLE 226 AXALTA COATING SYSTEMS LLC: COMPANY OVERVIEW

- FIGURE 62 AXALTA COATING SYSTEMS LLC: COMPANY SNAPSHOT

- TABLE 227 AXALTA COATING SYSTEMS LLC: PRODUCT LAUNCHES

- TABLE 228 AXALTA COATING SYSTEMS LLC: DEALS

- 11.1.7 HEMPEL A/S

- TABLE 229 HEMPEL A/S: COMPANY OVERVIEW

- FIGURE 63 HEMPEL A/S: COMPANY SNAPSHOT

- TABLE 230 HEMPEL A/S: PRODUCT LAUNCHES

- TABLE 231 HEMPEL A/S: DEALS

- TABLE 232 HEMPEL A/S: OTHERS

- 11.1.8 CHUGOKU MARINE PAINTS LTD.

- TABLE 233 CHUGOKU MARINE PAINTS LTD.: COMPANY OVERVIEW

- FIGURE 64 CHUGOKU MARINE PAINTS LTD.: COMPANY SNAPSHOT

- TABLE 234 CHUGOKU MARINE PAINTS LTD.: PRODUCT LAUNCHES

- 11.1.9 NIPPON PAINT HOLDINGS CO., LTD.

- TABLE 235 NIPPON PAINT HOLDINGS CO. LTD.: COMPANY OVERVIEW

- FIGURE 65 NIPPON PAINT HOLDINGS CO., LTD.: COMPANY SNAPSHOT

- TABLE 236 NIPPON PAINT HOLDINGS CO., LTD.: PRODUCT LAUNCHES

- TABLE 237 NIPPON PAINT HOLDINGS CO., LTD.: DEALS

- 11.1.10 TEKNOS

- TABLE 238 TEKNOS: COMPANY OVERVIEW

- FIGURE 66 TEKNOS: COMPANY SNAPSHOT

- TABLE 239 TEKNOS: PRODUCT LAUNCHES

- 11.2 OTHER PLAYERS

- 11.2.1 NOROO PAINT & COATINGS

- TABLE 240 NOROO PAINT & COATINGS: COMPANY OVERVIEW

- 11.2.2 DIAMOND VOGEL

- TABLE 241 DIAMOND VOGEL: COMPANY OVERVIEW

- 11.2.3 GREENKOTE PLC

- TABLE 242 GREENKOTE PLC: COMPANY OVERVIEW

- TABLE 243 GREENKOTE PLC: PRODUCT LAUNCHES

- TABLE 244 GREENKOTE PLC: DEALS

- 11.2.4 RENNER HERRMANN S.A.

- TABLE 245 RENNER HERRMANN S.A.: COMPANY OVERVIEW

- 11.2.5 NYCOTE LABORATORIES CORPORATION

- TABLE 246 NYCOTE LABORATORIES: COMPANY OVERVIEW

- TABLE 247 NYCOTE LABORATORIES CORPORATION: PRODUCT LAUNCHES

- TABLE 248 NYCOTE LABORATORIES CORPORATION: DEALS

- 11.2.6 O3 GROUP

- TABLE 249 O3 GROUP: COMPANY OVERVIEW

- 11.2.7 THE MAGNI GROUP, INC.

- TABLE 250 THE MAGNI GROUP, INC.: COMPANY OVERVIEW

- 11.2.8 SECOA METAL FINISHING

- TABLE 251 SECOA METAL FINISHING: COMPANY OVERVIEW

- 11.2.9 EONCOAT, LLC

- TABLE 252 EONCOAT, LLC: COMPANY OVERVIEW

- 11.2.10 DAI NIPPON TORYO CO., LTD.

- TABLE 253 DAI NIPPON TORYO CO., LTD: COMPANY OVERVIEW

- 11.2.11 ADVANCED NANOTECH LAB

- TABLE 254 ADVANCED NANOTECH LAB: COMPANY OVERVIEW

- 11.2.12 HUISINS NEW MATERIAL TECHNOLOGY CO.

- TABLE 255 HUISINS NEW MATERIAL TECHNOLOGY CO.: COMPANY OVERVIEW

- 11.2.13 BLUCHEM

- TABLE 256 BLUCHEM: COMPANY OVERVIEW

- 11.2.14 SK FORMULATIONS INDIA PVT. LTD.

- TABLE 257 SK FORMULATIONS INDIA PVT. LTD.: COMPANY OVERVIEW

- 11.2.15 ANCATT INC.

- TABLE 258 ANCATT INC.: COMPANY OVERVIEW

- *Details on Business overview, Products offered, Recent Developments, MNM view might not be captured in case of unlisted companies.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS