|

|

市場調査レポート

商品コード

1297938

デジタル糖尿病管理の世界市場:製品別 (デバイス、糖尿病アプリ、サービス、ソフトウェア・プラットフォーム)・デバイスの種類別 (ハンドヘルド、ウェアラブル)・エンドユーザー別 (病院、自己治療/在宅医療) の将来予測 (2028年まで)Digital Diabetes Management Market by Product (Device (CGM, Smart Glucometer, Insulin Patch Pump), Diabetes Apps, Service, Software & Platforms), Device Type (Handheld & Wearables), End User (Hospitals & Self/Home Healthcare) - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| デジタル糖尿病管理の世界市場:製品別 (デバイス、糖尿病アプリ、サービス、ソフトウェア・プラットフォーム)・デバイスの種類別 (ハンドヘルド、ウェアラブル)・エンドユーザー別 (病院、自己治療/在宅医療) の将来予測 (2028年まで) |

|

出版日: 2023年06月20日

発行: MarketsandMarkets

ページ情報: 英文 237 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

世界のデジタル糖尿病管理の市場規模は、2023年の168億米ドルから、2028年には313億米ドルに達し、予測期間中に13.3%のCAGRで成長すると予測されています。

糖尿病の有病率の上昇により、より優れた糖尿病治療ソリューションを開発・導入する意義が高まっています。また技術開発により、適応性の高いソリューションの導入が可能になっています。その他の主な成長促進要因としては、企業向けクラウドベースソリューションの普及や、接続デバイスやアプリの利用が増加していることが挙げられます。しかし予測期間中には、装置の価格の高さ、新興国市場での償還不足、従来の標準型の糖尿病管理装置の受け入れ拡大といった要因が、市場成長の妨げになると予測されます。

"製品別では、スマート血糖値計のセグメントが最大シェアを占める"

デジタル糖尿病管理デバイス市場では2022年に、スマート血糖値計のセグメントが25.2%の市場シェアを占めました。スマート血糖値計を使用する際の利便性と、低血糖・高血糖糖尿病の早期発見における利点が、この市場の成長の主な原因となっています。その他、Bluetooth対応血糖値計、分析機能付きオールインワン型血糖値計、携帯可能なポケットサイズの血糖値計などの技術進歩も、この市場セグメントの人気拡大を後押ししています。

"ウェアラブルデバイスのセグメントが、予測期間中に最も高いCAGRで成長する"

デジタル糖尿病管理市場をデバイスの種類別に見ると、2022年にはウェアラブル技術が市場の60.3%を占めました。予測期間中、このセグメントは13.2%と最も高いCAGRで成長すると予測されています。ウェアラブル市場は、技術進歩、スマートインスリンポンプやインスリンパッチの採用増加、ウェアラブルに関する規制承認の増加などの結果、拡大しています。

"2022年には、自己治療/在宅医療のセグメントが最大シェアを占める"

エンドユーザー別では、2022年には自己治療/在宅医療のセグメントが最大の市場シェアを占めました。これは主に、糖尿病管理のためのデジタルプラットフォームに対する認識が高まった結果、在宅医療を受け入れる患者が増加したことに起因します。継続的なインスリン療法を必要とする患者にとって、自己投与は最も有益です。長期的な治療が必要な患者にとって入院治療は非常に高額であり、日常生活に戻れないという問題もあります。

"北米が2021年のデジタル糖尿病管理市場で最大シェアを占める"

地域別に見ると、2022年には北米が41.4%で最大の市場シェアを占め、次いで欧州が29.0%でした。コネクテッド糖尿病管理装置の成長、糖尿病・肥満管理アプリの人気上昇、技術的に高度なソリューションに対する需要の高まり、支払者によるデジタル糖尿病ソリューションの受け入れ拡大、デジタルヘルスを推進する政府の取り組み、同地域における自己糖尿病管理に対する意識の高まりなどが、北米がデジタル糖尿病管理市場を独占する主な要因となっています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

- 促進要因

- 抑制要因

- 機会

- 課題

- 業界の動向

- 規制分析

- エコシステム分析

- バリューチェーン分析

- ポーターのファイブフォース分析

- 特許分析

- 価格分析

- サプライチェーン分析

- 主な会議とイベント (2023年~2024年)

- 主要な利害関係者と購入基準

- 技術分析

- 償還シナリオ

- 貿易分析

第6章 デジタル糖尿病管理市場:製品・サービス別

- イントロダクション

- デバイス

- スマート血糖値計

- 連続血糖モニタリング装置 (CGM)

- スマートインスリンペン

- スマートインスリンポンプ/閉ループシステムおよびスマートインスリンパッチ

- デジタル糖尿病管理アプリ

- 糖尿病・血糖値追跡アプリ

- 体重・食事管理アプリ

- データ管理ソフトウェア・プラットフォーム

- サービス

第7章 デジタル糖尿病管理市場:種類別

- イントロダクション

- ウェアラブルデバイス

- ハンドヘルドデバイス

第8章 デジタル糖尿病管理市場:エンドユーザー別

- イントロダクション

- 自己治療/在宅医療

- 病院・糖尿病専門クリニック

- 学術研究機関

第9章 デジタル糖尿病管理市場:地域別

- イントロダクション

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- その他の欧州

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- その他のアジア太平洋

- ラテンアメリカ

- ブラジル

- メキシコ

- その他のラテンアメリカ

- 中東・アフリカ

第10章 競合情勢

- 概要

- 主要企業の戦略/有力企業

- デジタル糖尿病管理市場:主要企業の収益シェア分析

- 市場シェア分析

- 企業評価マトリックス

- スタートアップ/中小企業の評価マトリックス (2022年)

- 競合ベンチマーキング

- 競合シナリオ

第11章 企業プロファイル

- 主要企業

- MEDTRONIC

- F. HOFFMANN-LA ROCHE

- DEXCOM, INC.

- ASCENSIA DIABETES CARE HOLDINGS AG

- ABBOTT LABORATORIES

- B. BRAUN MELSUNGEN AG

- TIDEPOOL

- GLOOKO, INC.

- LIFESCAN, INC.

- AGAMATRIX

- TANDEM DIABETES CARE, INC.

- INSULET CORPORATION

- DARIOHEALTH CORPORATION

- ONE DROP

- YPSOMED HOLDING AG

- その他の企業

- ARKRAY

- DOTTLI

- ACON LABORATORIES, INC.

- CARE INNOVATIONS, LLC

- HEALTH2SYNC

- EMPERRA GMBH E-HEALTH TECHNOLOGIES

- AZUMIO

- DECIDE CLINICAL SOFTWARE GMBH

- PENDIQ GMBH

- BEATO

第12章 付録

The global digital diabetes management market is projected to reach USD 31.3 Billion by 2028 from an estimated USD 16.8 Billion in 2023, at a CAGR of 13.3% during the forecast period. The significance of developing and implementing better diabetes care solutions has increased due to the rising prevalence of diabetes. Additionally, technological development has made it feasible for the market to introduce highly adaptable solutions. Among the other key drivers of market growth are the rising adoption of cloud-based enterprise solutions and the rising use of connected devices and apps. But during the forecast period, factors like high device costs, a lack of reimbursement in developing countries, and a higher acceptance of standard and traditional diabetes management devices are anticipated to hinder the market growth.

"Smart glucose meters segment accounted for the largest share in the Digital Diabetes Management market."

The devices segment is sub-segmented into smart insulin pens, smart insulin pumps/closed-loop systems, smart insulin patches, smart insulin pens, and CGM systems. In 2022, the market for digital diabetes management devices was dominated by the smart glucose meter segment, which held a 25.2% market share. The convenience for using smart glucose meters and their advantages in the early detection of hypo- and hyperglycemic diabetes are primarily responsible for the growth of this market. Other factors driving the growing popularity of this market segment include technological advancements like Bluetooth-enabled glucometers, all-in-one glucometers with analysis capabilities, and portable, pocket-size glucometers.

"Wearable devices segment to grow at the highest CAGR during the forecast period."

Both handheld and wearable devices are the sub-segment of the device types that are taken into account in the digital diabetes management device market. In 2022, wearable technology accounted for 60.3% of the market for digital diabetes management devices. During the forecast period, this segment is anticipated to grow at the highest CAGR of 13.2%. The market for wearables is growing as a result of technological advancements, an increase in the adoption of smart insulin pumps and insulin patches, and an increase in the number of regulatory approvals for wearables.

"The Self/home healthcare segment accounted for the largest share of Digital Diabetes Management market in 2022"

In 2022, the self-/home healthcare segment held the largest market share for digital diabetes management. This is primarily attributed to the rising patient acceptance of home care as a result of growing awareness of digital platforms for managing diabetes. Patients who require continuous insulin therapy benefit most from self-administration. Inpatient treatment is very expensive for patients who require long-term therapy, and it also keeps them from going back to their daily routines.

"North America accounted for the largest share of the Digital Diabetes Management market in 2021"

North America held the largest market share in 2022 with a share of 41.4%, followed by Europe with a share of 29.0%. The growth of connected diabetes management devices, the rising popularity of diabetes and obesity management apps, the rising demand for technologically advanced solutions, the growing acceptance of digital diabetes solutions by payers, government initiatives to promote digital health, and increasing awareness of self-diabetes management in the region are the main factors driving North America to dominate the digital diabetes management market.

A breakdown of the primary participants (supply-side) for the Digital Diabetes Management market referred to for this report is provided below:

- By Company Type: Tier 1-46%, Tier 2-33%, and Tier 3-21%

- By Designation: C-level-43%, Director Level-35%, and Others-22%

- By Region: North America-34%, Europe-26%, Asia Pacific-19%, Latin America- 11%, and Middle East and Africa- 10%

The prominent players operating in the global digital diabetes management market are Medtronic (Ireland), B. Braun Melsungen AG (Germany), Dexcom, Inc. (US), Abbott Laboratories (US), F. Hoffmann-La Roche (Switzerland), Insulet Corporation (US), Tandem Diabetes Care (US), Dottli (Finland), Ypsomed Holding AG (Switzerland), ARKRAY (Japan), Ascensia Diabetes Care Holdings AG (Switzerland), Health2Sync (Taiwan), Emperra GmbH E-Health Technologies (Germany), ACON Laboratories, Inc. (US), Care Innovations, LLC (US), Azumio (US), LifeScan, Inc. (US), Tidepool (US), AgaMatrix (US), Glooko, Inc. (US), DarioHealth Corporation (Israel), One Drop (US), Decide Clinical Software GmbH (Austria), Pendiq GmbH (Germany), and BeatO (India).

Research Coverage:

The market study covers the digital diabetes management market across various segments. It aims at estimating the market size and the growth potential of this market across different segments by product & service, by device type, end user, and region. The study also includes an in-depth competitive analysis of the key players in the market, along with their company profiles, key observations related to their product and business offerings, recent developments, and key market strategies.

Reasons to Buy the Report

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall digital diabetes management market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and to plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

This report provides insights on the following pointers:

- Analysis of key drivers (Increasing Prevalence Of Diabetes, Technological Advancements and Growing Adoption Of Cloud-Based Enterprise Solutions For Diabetes Management), restraints (High Cost Of Devices And Lack Of Reimbursement In Developing Countries and Higher Acceptance Of Traditional Diabetes Management Devices), opportunities (Increasing Diabetes-Related Health Expenditure In Emerging Economies), and challenges (Low Penetration In Developing Economies and Lack Of Data Security) influencing the growth of the digital diabetes management market

- Market Penetration: Comprehensive information on the product portfolios offered by the top players in the global digital diabetes management market

- Product Development/Innovation: Detailed insights on the upcoming trends, R&D activities, and product or service launches in the global digital diabetes management market

- Market Development: Comprehensive information on the lucrative emerging regions by product & services, device types, end users, and region

- Market Diversification: Exhaustive information about new products, growing geographies, and recent developments in the global digital diabetes management market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, revenue analysis, and products of leading players in the global digital diabetes management market.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.2.1 PRODUCT AND SERVICES

- 1.2.2 DEVICE TYPE

- 1.2.3 END USER

- 1.2.4 INCLUSIONS AND EXCLUSIONS

- 1.3 MARKET SCOPE

- 1.3.1 MARKETS COVERED

- 1.3.2 YEARS CONSIDERED

- 1.4 CURRENCY CONSIDERED

- TABLE 1 STANDARD CURRENCY CONVERSION RATES

- 1.5 LIMITATIONS

- 1.6 STAKEHOLDERS

- 1.7 SUMMARY OF CHANGES

- 1.7.1 REFINEMENTS IN SEGMENTATION OF GLOBAL DIGITAL DIABETES MANAGEMENT MARKET

- 1.7.2 UPDATED FINANCIAL INFORMATION/PRODUCT PORTFOLIOS OF PLAYERS

- 1.7.3 UPDATED MARKET DEVELOPMENTS OF PROFILED PLAYERS

- 1.7.4 ADDITION OF RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 1 RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- FIGURE 2 PRIMARY SOURCES

- 2.1.2.1 Key data from primary sources

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS (SUPPLY SIDE): BY COMPANY TYPE, DESIGNATION, AND REGION

- FIGURE 4 BREAKDOWN OF PRIMARY INTERVIEWS (DEMAND SIDE): BY END USER AND REGION

- 2.2 MARKET SIZE ESTIMATION

- FIGURE 5 MARKET SIZE ESTIMATION: REVENUE SHARE ANALYSIS (2022)

- FIGURE 6 MARKET SIZE ESTIMATION: COMPANY-WISE REVENUE SHARE ANALYSIS (2022)

- FIGURE 7 SUPPLY-SIDE ANALYSIS: DIGITAL DIABETES MANAGEMENT MARKET (2022)

- FIGURE 8 SUPPLY-SIDE ANALYSIS: SMART GLUCOSE METERS MARKET (2022)

- FIGURE 9 SUPPLY-SIDE ANALYSIS: CONTINUOUS GLUCOSE MONITORING SYSTEMS MARKET (2022)

- FIGURE 10 SUPPLY-SIDE ANALYSIS: SMART INSULIN PENS MARKET (2022)

- FIGURE 11 SUPPLY-SIDE ANALYSIS: SMART INSULIN PUMPS/CLOSED-LOOP SYSTEMS AND SMART INSULIN PATCHES MARKET (2022)

- FIGURE 12 SUPPLY-SIDE ANALYSIS: DIGITAL DIABETES MANAGEMENT APPS MARKET (2022)

- FIGURE 13 CAGR PROJECTIONS FROM ANALYSIS OF DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES FOR DIGITAL DIABETES MANAGEMENT MARKET (2023-2028)

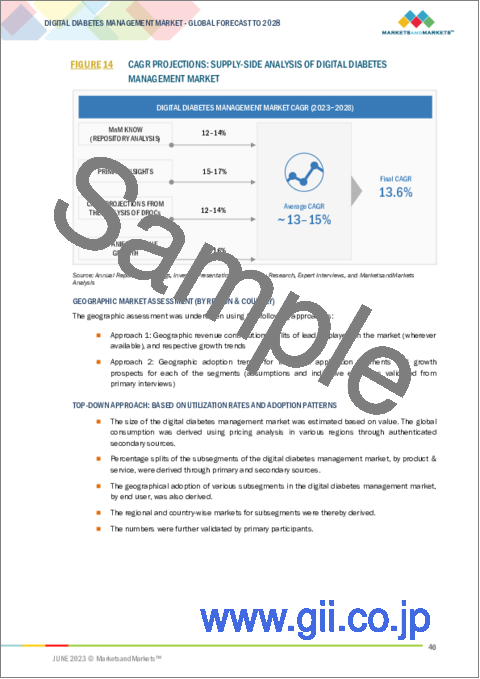

- FIGURE 14 CAGR PROJECTIONS: SUPPLY-SIDE ANALYSIS OF DIGITAL DIABETES MANAGEMENT MARKET

- FIGURE 15 TOP-DOWN APPROACH: GLOBAL DIGITAL DIABETES MANAGEMENT MARKET

- FIGURE 16 BOTTOM-UP APPROACH: GLOBAL DIGITAL DIABETES MANAGEMENT MARKET

- FIGURE 17 GLOBAL DIGITAL DIABETES MANAGEMENT MARKET SIZING, BY DEVICE TYPE

- 2.3 MARKET BREAKDOWN AND DATA TRIANGULATION

- FIGURE 18 DATA TRIANGULATION METHODOLOGY

- 2.4 MARKET SHARE ESTIMATION

- 2.5 STUDY ASSUMPTIONS

- 2.6 IMPACT OF RECESSION

3 EXECUTIVE SUMMARY

- FIGURE 19 DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2023 VS. 2028 (USD MILLION)

- FIGURE 20 DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 21 DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 22 DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 23 DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2023 VS. 2028 (USD MILLION)

- FIGURE 24 DIGITAL DIABETES MANAGEMENT MARKET: GEOGRAPHICAL SNAPSHOT

4 PREMIUM INSIGHTS

- 4.1 DIGITAL DIABETES MANAGEMENT MARKET OVERVIEW

- FIGURE 25 INCREASING PREVALENCE OF DIABETES AND GROWING DEMAND FOR DIGITAL SOLUTIONS TO DRIVE MARKET GROWTH

- 4.2 ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE AND COUNTRY (2022)

- FIGURE 26 DEVICES TO ACCOUNT FOR LARGEST SHARE OF ASIA PACIFIC MARKET

- 4.3 DIGITAL DIABETES MANAGEMENT MARKET: GEOGRAPHICAL GROWTH OPPORTUNITIES

- FIGURE 27 US TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- 4.4 REGIONAL MIX: DIGITAL DIABETES MANAGEMENT MARKET

- FIGURE 28 NORTH AMERICAN MARKET TO GROW AT HIGHEST CAGR DURING FORECAST PERIOD

- 4.5 DIGITAL DIABETES MANAGEMENT MARKET: DEVELOPED VS. DEVELOPING ECONOMIES, 2023 VS. 2028 (USD MILLION)

- FIGURE 29 DEVELOPED ECONOMIES TO REGISTER HIGHER GROWTH DURING FORECAST PERIOD

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 30 DIGITAL DIABETES MANAGEMENT MARKET: DRIVERS, RESTRAINTS, OPPORTUNITIES, AND CHALLENGES

- 5.2.1 DRIVERS

- 5.2.1.1 Increasing prevalence of diabetes

- TABLE 2 TOP FIVE COUNTRIES WITH HIGHEST NUMBER OF DIABETICS (20-79 YEARS), 2021 VS. 2045

- 5.2.1.2 Technological advancements

- TABLE 3 PRODUCT LAUNCHES WITH NEW TECHNOLOGICAL ADVANCEMENTS

- 5.2.1.3 Growing adoption of cloud-based enterprise solutions for diabetes management

- 5.2.1.4 Advent of artificial intelligence in diabetes care devices

- 5.2.1.5 Increasing penetration of digital platforms and adoption of mobile apps for diabetes management

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost of devices and lack of reimbursement in developing countries

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Increasing diabetes-related health expenditure

- 5.2.4 CHALLENGES

- 5.2.4.1 Low adoption in developing economies

- 5.2.4.2 Data security

- 5.3 INDUSTRY TRENDS

- 5.3.1 GROWING DEMAND FOR HYBRID CLOSED-LOOP SYSTEMS/ARTIFICIAL PANCREAS DEVICE SYSTEMS

- TABLE 4 HYBRID CLOSED-LOOP SYSTEMS: LATEST EXAMPLES

- 5.3.2 GROWING NUMBER OF COLLABORATIONS BETWEEN STAKEHOLDERS

- TABLE 5 RECENT COLLABORATIONS IN DIGITAL DIABETES MANAGEMENT MARKET

- 5.3.3 INCREASING DEMAND FOR FLASH GLUCOSE MONITORING (FGM) SYSTEMS

- 5.4 REGULATORY ANALYSIS

- 5.4.1 REGULATORY LANDSCAPE

- 5.4.1.1 North America

- 5.4.1.1.1 US

- 5.4.1.1 North America

- TABLE 6 US: TIME, COST, AND COMPLEXITY OF REGISTRATION PROCESS

- FIGURE 31 FDA 510(K) APPROVAL PROCESS

- 5.4.1.1.2 Canada

- TABLE 7 CANADA: TIME, COST, AND COMPLEXITY OF REGISTRATION PROCESS

- 5.4.1.2 Europe

- FIGURE 32 CE APPROVAL PROCESS FOR DIGITAL DIABETES MANAGEMENT SOLUTIONS

- 5.4.1.3 Asia Pacific

- 5.4.1.3.1 Australia

- 5.4.1.3.2 Japan

- 5.4.1.3 Asia Pacific

- TABLE 8 CLASSIFICATION OF MEDICAL DEVICES AND REVIEWING BODY IN JAPAN

- 5.4.1.3.3 China

- TABLE 9 CHINA: TIME, COST, AND COMPLEXITY OF REGISTRATION PROCESS

- 5.4.1.3.4 India

- 5.4.1.4 Latin America

- 5.4.2 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 10 INDICATIVE LIST OF REGULATORY AUTHORITIES

- 5.4.1 REGULATORY LANDSCAPE

- 5.5 ECOSYSTEM ANALYSIS

- FIGURE 33 DIGITAL DIABETES MANAGEMENT MARKET: ECOSYSTEM ANALYSIS (2022)

- 5.6 VALUE CHAIN ANALYSIS

- FIGURE 34 DIGITAL DIABETES MANAGEMENT DEVICES MARKET: VALUE CHAIN ANALYSIS (2022)

- 5.7 PORTER'S FIVE FORCES ANALYSIS

- TABLE 11 DIGITAL DIABETES MANAGEMENT MARKET: PORTER'S FIVE FORCES ANALYSIS

- 5.7.1 THREAT OF NEW ENTRANTS

- 5.7.2 INTENSITY OF COMPETITIVE RIVALRY

- 5.7.3 BARGAINING POWER OF BUYERS

- 5.7.4 BARGAINING POWER OF SUPPLIERS

- 5.7.5 THREAT OF SUBSTITUTES

- 5.8 PATENT ANALYSIS

- 5.8.1 PATENT PUBLICATION TRENDS FOR DIGITAL DIABETES MANAGEMENT

- FIGURE 35 PATENT PUBLICATION TRENDS (JANUARY 2014-MAY 2023)

- 5.8.2 TOP APPLICANTS (COMPANIES) FOR DIGITAL DIABETES MANAGEMENT PATENTS

- FIGURE 36 TOP APPLICANT COMPANIES FOR DIGITAL DIABETES MANAGEMENT PATENTS, 2014-2023

- 5.8.3 JURISDICTION ANALYSIS: TOP APPLICANTS (COUNTRIES) FOR DIGITAL DIABETES MANAGEMENT PATENTS

- FIGURE 37 JURISDICTION ANALYSIS: TOP APPLICANT COUNTRIES FOR DIGITAL DIABETES MANAGEMENT PATENTS, 2014-2023

- 5.9 PRICING ANALYSIS

- 5.9.1 KEY PLAYERS: AVERAGE SELLING PRICE, BY DEVICE

- TABLE 12 AVERAGE SELLING PRICE, BY DEVICE, 2022

- 5.10 SUPPLY CHAIN ANALYSIS

- FIGURE 38 DIGITAL DIABETES MANAGEMENT MARKET: STAKEHOLDERS IN SUPPLY CHAIN

- 5.11 KEY CONFERENCES AND EVENTS IN 2023-2024

- TABLE 13 DIGITAL DIABETES MANAGEMENT MARKET: LIST OF CONFERENCES AND EVENTS

- 5.12 KEY STAKEHOLDERS AND BUYING CRITERIA

- 5.12.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 39 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS

- TABLE 14 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR TOP 3 APPLICATIONS (%)

- 5.12.2 BUYING CRITERIA

- FIGURE 40 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

- TABLE 15 KEY BUYING CRITERIA FOR TOP 3 APPLICATIONS

- 5.13 TECHNOLOGY ANALYSIS

- 5.14 REIMBURSEMENT SCENARIO

- TABLE 16 DIGITAL DIABETES MANAGEMENT PRODUCTS: GLOBAL COVERAGE AND REIMBURSEMENT

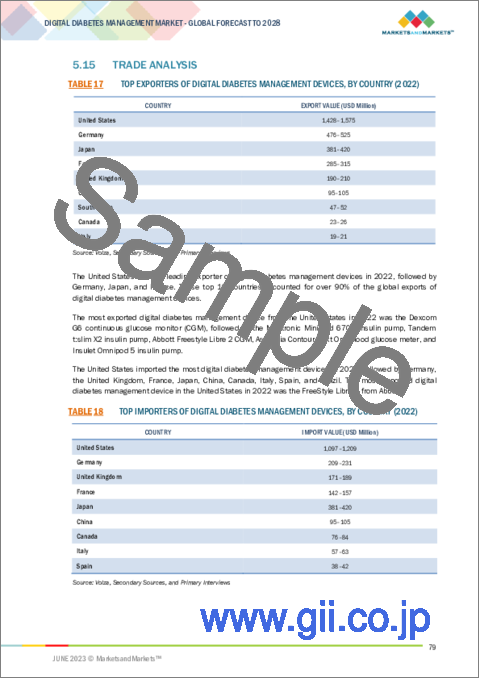

- 5.15 TRADE ANALYSIS

- TABLE 17 TOP EXPORTERS OF DIGITAL DIABETES MANAGEMENT DEVICES, BY COUNTRY (2022)

- TABLE 18 TOP IMPORTERS OF DIGITAL DIABETES MANAGEMENT DEVICES, BY COUNTRY (2022)

6 DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE

- 6.1 INTRODUCTION

- TABLE 19 DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- 6.2 DEVICES

- TABLE 20 DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 21 DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 22 DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (THOUSAND UNITS)

- 6.2.1 SMART GLUCOSE METERS

- 6.2.1.1 Reducing prices and technological innovations to drive growth

- TABLE 23 KEY SMART GLUCOSE METERS OFFERED BY MARKET PLAYERS

- TABLE 24 SMART GLUCOSE METERS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 25 SMART GLUCOSE METERS MARKET, BY REGION, 2021-2028 (THOUSAND UNITS)

- 6.2.2 CONTINUOUS GLUCOSE MONITORING SYSTEMS

- 6.2.2.1 CGM segment to grow at highest CAGR during forecast period

- TABLE 26 KEY CGM SYSTEMS OFFERED BY MARKET PLAYERS

- TABLE 27 CONTINUOUS GLUCOSE MONITORING SYSTEMS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 28 CONTINUOUS GLUCOSE MONITORING SYSTEMS MARKET, BY REGION, 2021-2028 (THOUSAND UNITS)

- 6.2.3 SMART INSULIN PENS

- 6.2.3.1 Increasing demand for personalized/patient-centric devices without risk of needle-stick injuries to drive growth

- TABLE 29 KEY SMART INSULIN PENS OFFERED BY MARKET PLAYERS

- TABLE 30 SMART INSULIN PENS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 31 SMART INSULIN PENS MARKET, BY REGION, 2021-2028 (THOUSAND UNITS)

- 6.2.4 SMART INSULIN PUMPS/CLOSED-LOOP SYSTEMS AND SMART INSULIN PATCHES

- 6.2.4.1 Benefits of smart insulin pumps and closed-loop systems to drive growth

- TABLE 32 KEY SMART INSULIN PUMPS/CLOSED-LOOP SYSTEMS AND SMART INSULIN PATCHES OFFERED BY MARKET PLAYERS

- TABLE 33 SMART INSULIN PUMPS/CLOSED-LOOP SYSTEMS AND SMART INSULIN PATCHES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 34 SMART INSULIN PUMPS/CLOSED-LOOP SYSTEMS AND SMART INSULIN PATCHES MARKET, BY REGION, 2021-2028 (THOUSAND UNITS)

- 6.3 DIGITAL DIABETES MANAGEMENT APPS

- TABLE 35 DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 36 DIGITAL DIABETES MANAGEMENT APPS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.3.1 DIABETES AND BLOOD GLUCOSE TRACKING APPS

- 6.3.1.1 Growing adoption of connected devices to drive growth

- TABLE 37 KEY DIABETES AND BLOOD GLUCOSE TRACKING APPS OFFERED BY MARKET PLAYERS

- TABLE 38 DIABETES AND BLOOD GLUCOSE TRACKING APPS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.3.2 WEIGHT AND DIET MANAGEMENT APPS

- 6.3.2.1 Growing obese population and increasing need to prevent diabetes to drive growth

- TABLE 39 KEY WEIGHT AND DIET MANAGEMENT APPS OFFERED BY MARKET PLAYERS

- TABLE 40 WEIGHT AND DIET MANAGEMENT APPS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.4 DATA MANAGEMENT SOFTWARE AND PLATFORMS

- 6.4.1 GROWING DEMAND FOR DIABETES DATA MANAGEMENT TO DRIVE GROWTH

- TABLE 41 KEY DATA MANAGEMENT SOFTWARE AND PLATFORMS OFFERED BY MARKET PLAYERS

- TABLE 42 DATA MANAGEMENT SOFTWARE AND PLATFORMS MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 6.5 SERVICES

- 6.5.1 INCREASING ADOPTION OF REMOTE ONLINE COACHING SERVICES AMONG DIABETES PATIENTS TO DRIVE GROWTH

- TABLE 43 KEY SERVICES OFFERED BY MARKET PLAYERS

- TABLE 44 DIGITAL DIABETES MANAGEMENT SERVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

7 DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE

- 7.1 INTRODUCTION

- TABLE 45 DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- 7.2 WEARABLE DEVICES

- 7.2.1 WEARABLE DEVICES TO DOMINATE DIGITAL DIABETES MANAGEMENT DEVICES MARKET DURING FORECAST PERIOD

- TABLE 46 WEARABLE DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- 7.3 HANDHELD DEVICES

- 7.3.1 INCREASING DEMAND FOR REMOTE MONITORING TO BOOST GROWTH

- TABLE 47 HANDHELD DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

8 DIGITAL DIABETES MANAGEMENT MARKET, BY END USER

- 8.1 INTRODUCTION

- TABLE 48 DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 8.2 SELF/HOME HEALTHCARE

- 8.2.1 HIGH COST OF INPATIENT CARE TO FUEL PREFERENCE FOR SELF/HOME CARE

- TABLE 49 DIGITAL DIABETES MANAGEMENT MARKET FOR SELF/HOME HEALTHCARE, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.3 HOSPITALS AND SPECIALTY DIABETES CLINICS

- 8.3.1 RISING DEMAND FOR POC TESTING IN HOSPITALS TO BOOST GROWTH

- TABLE 50 DIGITAL DIABETES MANAGEMENT MARKET FOR HOSPITALS AND SPECIALTY DIABETES CLINICS, BY COUNTRY, 2021-2028 (USD MILLION)

- 8.4 ACADEMIC AND RESEARCH INSTITUTES

- 8.4.1 PRODUCT INNOVATION FOR DIABETES MANAGEMENT TO DRIVE GROWTH

- TABLE 51 DIGITAL DIABETES MANAGEMENT MARKET FOR ACADEMIC AND RESEARCH INSTITUTES, BY COUNTRY, 2021-2028 (USD MILLION)

9 DIGITAL DIABETES MANAGEMENT MARKET, BY REGION

- 9.1 INTRODUCTION

- FIGURE 41 DIGITAL DIABETES MANAGEMENT MARKET: GEOGRAPHIC SNAPSHOT

- TABLE 52 DIGITAL DIABETES MANAGEMENT MARKET, BY REGION, 2021-2028 (USD MILLION)

- 9.2 NORTH AMERICA

- 9.2.1 NORTH AMERICA: RECESSION IMPACT

- FIGURE 42 NORTH AMERICA: DIGITAL DIABETES MANAGEMENT MARKET SNAPSHOT

- TABLE 53 NORTH AMERICA: DIGITAL DIABETES MANAGEMENT MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 54 NORTH AMERICA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 55 NORTH AMERICA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 56 NORTH AMERICA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 57 NORTH AMERICA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 58 NORTH AMERICA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.2.2 US

- 9.2.2.1 Increasing diabetes prevalence and high penetration of digital platforms to boost market

- TABLE 59 US: MACROECONOMIC INDICATORS

- TABLE 60 US: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 61 US: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 62 US: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 63 US: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 64 US: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.2.3 CANADA

- 9.2.3.1 Favorable reimbursement scenario to drive digital diabetes management adoption in Canada

- TABLE 65 CANADA: MACROECONOMIC INDICATORS

- TABLE 66 CANADA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 67 CANADA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 68 CANADA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 69 CANADA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 70 CANADA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3 EUROPE

- 9.3.1 EUROPE: RECESSION IMPACT

- FIGURE 43 EUROPE: DIGITAL DIABETES MANAGEMENT MARKET SNAPSHOT

- TABLE 71 EUROPE: DIGITAL DIABETES MANAGEMENT MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 72 EUROPE: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 73 EUROPE: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 74 EUROPE: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 75 EUROPE: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 76 EUROPE: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.2 GERMANY

- 9.3.2.1 Germany to dominate European market over forecast period

- TABLE 77 GERMANY: MACROECONOMIC INDICATORS

- TABLE 78 GERMANY: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 79 GERMANY: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 80 GERMANY: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 81 GERMANY: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 82 GERMANY: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.3 UK

- 9.3.3.1 Government initiatives to support market growth

- TABLE 83 UK: MACROECONOMIC INDICATORS

- TABLE 84 UK: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 85 UK: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 86 UK: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 87 UK: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 88 UK: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.4 FRANCE

- 9.3.4.1 Affordability of healthcare to propel adoption of digital solutions

- TABLE 89 FRANCE: MACROECONOMIC INDICATORS

- TABLE 90 FRANCE: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 91 FRANCE: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 92 FRANCE: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 93 FRANCE: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 94 FRANCE: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.5 ITALY

- 9.3.5.1 Rising diabetes prevalence to offer growth opportunities

- TABLE 95 ITALY: MACROECONOMIC INDICATORS

- TABLE 96 ITALY: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 97 ITALY: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 98 ITALY: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 99 ITALY: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 100 ITALY: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.6 SPAIN

- 9.3.6.1 Growing healthcare budget and efforts to boost local manufacturing of medical products

- TABLE 101 SPAIN: MACROECONOMIC INDICATORS

- TABLE 102 SPAIN: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 103 SPAIN: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 104 SPAIN: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 105 SPAIN: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 106 SPAIN: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.3.7 REST OF EUROPE

- TABLE 107 REST OF EUROPE: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 108 REST OF EUROPE: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 109 REST OF EUROPE: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 110 REST OF EUROPE: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 111 REST OF EUROPE: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4 ASIA PACIFIC

- 9.4.1 ASIA PACIFIC: RECESSION IMPACT

- FIGURE 44 ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT MARKET SNAPSHOT

- TABLE 112 ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 113 ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 114 ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 115 ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 116 ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 117 ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.2 CHINA

- 9.4.2.1 China to hold largest share of APAC market

- TABLE 118 CHINA: MACROECONOMIC INDICATORS

- TABLE 119 CHINA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 120 CHINA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 121 CHINA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 122 CHINA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 123 CHINA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.3 JAPAN

- 9.4.3.1 High acceptance of digital solutions for diabetes management to boost growth

- TABLE 124 JAPAN: MACROECONOMIC INDICATORS

- TABLE 125 JAPAN: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 126 JAPAN: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 127 JAPAN: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 128 JAPAN: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 129 JAPAN: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.4 INDIA

- 9.4.4.1 Rising diabetes prevalence and focus on cost curtailment to favor adoption

- TABLE 130 INDIA: MACROECONOMIC INDICATORS

- TABLE 131 INDIA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 132 INDIA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 133 INDIA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 134 INDIA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 135 INDIA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.5 AUSTRALIA

- 9.4.5.1 Initiatives to help treat or manage diabetes-related problems to drive market growth

- TABLE 136 AUSTRALIA: MACROECONOMIC INDICATORS

- TABLE 137 AUSTRALIA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 138 AUSTRALIA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 139 AUSTRALIA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 140 AUSTRALIA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 141 AUSTRALIA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.6 SOUTH KOREA

- 9.4.6.1 Government initiatives for diabetes management to drive growth

- TABLE 142 SOUTH KOREA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 143 SOUTH KOREA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 144 SOUTH KOREA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 145 SOUTH KOREA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 146 SOUTH KOREA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.4.7 REST OF ASIA PACIFIC

- TABLE 147 REST OF ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 148 REST OF ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 149 REST OF ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 150 REST OF ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 151 REST OF ASIA PACIFIC: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.5 LATIN AMERICA

- 9.5.1 LATIN AMERICA: RECESSION IMPACT

- TABLE 152 LATIN AMERICA: DIGITAL DIABETES MANAGEMENT MARKET, BY COUNTRY, 2021-2028 (USD MILLION)

- TABLE 153 LATIN AMERICA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 154 LATIN AMERICA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 155 LATIN AMERICA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 156 LATIN AMERICA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 157 LATIN AMERICA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.5.2 BRAZIL

- 9.5.2.1 High private healthcare expenditure and increasing geriatric population to drive market

- TABLE 158 BRAZIL: MACROECONOMIC INDICATORS

- TABLE 159 BRAZIL: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 160 BRAZIL: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 161 BRAZIL: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 162 BRAZIL: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 163 BRAZIL: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.5.3 MEXICO

- 9.5.3.1 Growing obesity rate in Mexico to drive market

- TABLE 164 MEXICO: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 165 MEXICO: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 166 MEXICO: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 167 MEXICO: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 168 MEXICO: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.5.4 REST OF LATIN AMERICA

- TABLE 169 REST OF LATIN AMERICA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 170 REST OF LATIN AMERICA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 171 REST OF LATIN AMERICA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 172 REST OF LATIN AMERICA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 173 REST OF LATIN AMERICA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

- 9.6 MIDDLE EAST & AFRICA

- 9.6.1 SLOW DIGITIZATION OF HEALTH SYSTEMS IN AFRICAN COUNTRIES TO AFFECT GROWTH

- 9.6.2 MIDDLE EAST & AFRICA: RECESSION IMPACT

- TABLE 174 AFRICA: MACROECONOMIC INDICATORS

- TABLE 175 MIDDLE EAST & AFRICA: DIGITAL DIABETES MANAGEMENT MARKET, BY PRODUCT & SERVICE, 2021-2028 (USD MILLION)

- TABLE 176 MIDDLE EAST & AFRICA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY PRODUCT TYPE, 2021-2028 (USD MILLION)

- TABLE 177 MIDDLE EAST & AFRICA: DIGITAL DIABETES MANAGEMENT APPS MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 178 MIDDLE EAST & AFRICA: DIGITAL DIABETES MANAGEMENT DEVICES MARKET, BY TYPE, 2021-2028 (USD MILLION)

- TABLE 179 MIDDLE EAST & AFRICA: DIGITAL DIABETES MANAGEMENT MARKET, BY END USER, 2021-2028 (USD MILLION)

10 COMPETITIVE LANDSCAPE

- 10.1 OVERVIEW

- 10.2 STRATEGIES OF KEY PLAYERS/RIGHT TO WIN

- FIGURE 45 OVERVIEW OF STRATEGIES ADOPTED BY KEY PLAYERS IN DIGITAL DIABETES MANAGEMENT MARKET

- 10.3 REVENUE SHARE ANALYSIS OF KEY PLAYERS IN DIGITAL DIABETES MANAGEMENT MARKET

- FIGURE 46 REVENUE SHARE ANALYSIS OF KEY PLAYERS OPERATING IN DIGITAL DIABETES MANAGEMENT MARKET (2018-2022)

- 10.4 MARKET SHARE ANALYSIS

- FIGURE 47 MARKET SHARE ANALYSIS: SMART GLUCOSE METERS MARKET (2022)

- FIGURE 48 MARKET SHARE ANALYSIS: CONTINUOUS GLUCOSE MONITORING DEVICES MARKET (2022)

- FIGURE 49 MARKET SHARE ANALYSIS: INSULIN PUMPS MARKET (2022)

- FIGURE 50 MARKET SHARE ANALYSIS: SMART INSULIN PENS MARKET (2022)

- FIGURE 51 MARKET SHARE ANALYSIS: DIABETES APPS MARKET (2022)

- 10.5 COMPANY EVALUATION MATRIX

- FIGURE 52 DIGITAL DIABETES MANAGEMENT MARKET: COMPANY EVALUATION MATRIX FOR KEY PLAYERS, 2022

- 10.5.1 STARS

- 10.5.2 EMERGING LEADERS

- 10.5.3 PERVASIVE PLAYERS

- 10.5.4 PARTICIPANTS

- 10.6 EVALUATION MATRIX FOR START-UP/SME PLAYERS (2022)

- FIGURE 53 DIGITAL DIABETES MANAGEMENT MARKET: COMPANY EVALUATION MATRIX FOR START-UP/SME PLAYERS, 2022

- 10.6.1 PROGRESSIVE COMPANIES

- 10.6.2 DYNAMIC COMPANIES

- 10.6.3 STARTING BLOCKS

- 10.6.4 RESPONSIVE COMPANIES

- 10.7 COMPETITIVE BENCHMARKING

- 10.7.1 OVERALL FOOTPRINT OF COMPANIES

- TABLE 180 OVERALL FOOTPRINT OF COMPANIES

- TABLE 181 COMPANY FOOTPRINT: BY PRODUCT & SERVICE

- TABLE 182 COMPANY FOOTPRINT: BY DEVICE TYPE

- TABLE 183 COMPANY FOOTPRINT: BY END USER

- TABLE 184 COMPANY FOOTPRINT: BY REGION

- 10.8 COMPETITIVE SCENARIO

- 10.8.1 PRODUCT LAUNCHES

- TABLE 185 PRODUCT LAUNCHES

- 10.8.2 DEALS

- TABLE 186 DEALS

11 COMPANY PROFILES

- 11.1 KEY PLAYERS

- (Business overview, Products & services offered, Recent developments, MnM view, Key strengths, Strategic choices, and Weaknesses and competitive threats)**

- 11.1.1 MEDTRONIC

- TABLE 187 MEDTRONIC: BUSINESS OVERVIEW

- FIGURE 54 MEDTRONIC: COMPANY SNAPSHOT (2022)

- 11.1.2 F. HOFFMANN-LA ROCHE

- TABLE 188 F. HOFFMANN-LA ROCHE: BUSINESS OVERVIEW

- FIGURE 55 F. HOFFMANN-LA ROCHE: COMPANY SNAPSHOT (2022)

- 11.1.3 DEXCOM, INC.

- TABLE 189 DEXCOM, INC.: BUSINESS OVERVIEW

- FIGURE 56 DEXCOM, INC.: COMPANY SNAPSHOT (2022)

- 11.1.4 ASCENSIA DIABETES CARE HOLDINGS AG

- TABLE 190 ASCENSIA DIABETES CARE HOLDINGS AG: BUSINESS OVERVIEW

- 11.1.5 ABBOTT LABORATORIES

- TABLE 191 ABBOTT LABORATORIES: BUSINESS OVERVIEW

- FIGURE 57 ABBOTT LABORATORIES: COMPANY SNAPSHOT (2022)

- 11.1.6 B. BRAUN MELSUNGEN AG

- TABLE 192 B. BRAUN MELSUNGEN AG: BUSINESS OVERVIEW

- FIGURE 58 B. BRAUN MELSUNGEN AG: COMPANY SNAPSHOT (2022)

- 11.1.7 TIDEPOOL

- TABLE 193 TIDEPOOL: BUSINESS OVERVIEW

- 11.1.8 GLOOKO, INC.

- TABLE 194 GLOOKO, INC.: BUSINESS OVERVIEW

- 11.1.9 LIFESCAN, INC.

- TABLE 195 LIFESCAN, INC.: BUSINESS OVERVIEW

- 11.1.10 AGAMATRIX

- TABLE 196 AGAMATRIX: BUSINESS OVERVIEW

- 11.1.11 TANDEM DIABETES CARE, INC.

- TABLE 197 TANDEM DIABETES CARE, INC.: BUSINESS OVERVIEW

- FIGURE 59 TANDEM DIABETES CARE, INC.: COMPANY SNAPSHOT (2022)

- 11.1.12 INSULET CORPORATION

- TABLE 198 INSULET CORPORATION: BUSINESS OVERVIEW

- FIGURE 60 INSULET CORPORATION: COMPANY SNAPSHOT (2022)

- 11.1.13 DARIOHEALTH CORPORATION

- TABLE 199 DARIOHEALTH CORPORATION: BUSINESS OVERVIEW

- FIGURE 61 DARIOHEALTH CORPORATION: COMPANY SNAPSHOT (2022)

- 11.1.14 ONE DROP

- TABLE 200 ONE DROP: BUSINESS OVERVIEW

- 11.1.15 YPSOMED HOLDING AG

- TABLE 201 YPSOMED HOLDING AG: BUSINESS OVERVIEW

- FIGURE 62 YPSOMED HOLDING AG: COMPANY SNAPSHOT (2022)

- 11.2 OTHER PLAYERS

- 11.2.1 ARKRAY

- 11.2.2 DOTTLI

- 11.2.3 ACON LABORATORIES, INC.

- 11.2.4 CARE INNOVATIONS, LLC

- 11.2.5 HEALTH2SYNC

- 11.2.6 EMPERRA GMBH E-HEALTH TECHNOLOGIES

- 11.2.7 AZUMIO

- 11.2.8 DECIDE CLINICAL SOFTWARE GMBH

- 11.2.9 PENDIQ GMBH

- 11.2.10 BEATO

- *Details on Business overview, Products & services offered, Recent developments, MnM view, Key strengths, Strategic choices, and Weaknesses and competitive threats might not be captured in case of unlisted companies.

12 APPENDIX

- 12.1 DISCUSSION GUIDE

- 12.2 KNOWLEDGESTORE: MARKETSANDMARKETS' SUBSCRIPTION PORTAL

- 12.3 CUSTOMIZATION OPTIONS

- 12.4 RELATED REPORTS

- 12.5 AUTHOR DETAILS