|

|

市場調査レポート

商品コード

1323870

特殊食品原料の世界市場:タイプ別(酸味料、着色料、香料、酵素、乳化剤、F&Bスターターカルチャー、保存料、機能性食品原料、特殊澱粉、砂糖代替品)、流通チャネル別-2028年までの予測Specialty Food Ingredients Market by Type (Acidulant, Colors, Flavors, Enzymes, Emulsifiers, F&B Starter Culture, Preservatives, Functional Food Ingredients, Specialty Starches, Sugar Substitutes), Distribution Channel - Global Forecast to 2028 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 特殊食品原料の世界市場:タイプ別(酸味料、着色料、香料、酵素、乳化剤、F&Bスターターカルチャー、保存料、機能性食品原料、特殊澱粉、砂糖代替品)、流通チャネル別-2028年までの予測 |

|

出版日: 2023年07月27日

発行: MarketsandMarkets

ページ情報: 英文 473 Pages

納期: 即納可能

|

- 全表示

- 概要

- 目次

特殊食品原料の市場規模は、2023年の1,798億米ドルから2028年には2,409億米ドルに成長し、予測期間中のCAGRは6.0%と予測されています。

世界の人口増加と都市化の動向は、特殊食品原料市場に直接的な影響を与えています。より多くの人々が都市部に移り住むにつれて、レディトゥイート食品・飲料の需要が高まり、特殊食品成分の需要が高まっています。

消費者は、肥満、糖尿病、虫歯など、砂糖の過剰摂取が健康に及ぼす有害な影響をより意識するようになり、より健康的な代替品を求めるようになっています。この消費者行動は、栄養価が高く体に良い製品を求める健康志向の人々の嗜好に応えることが多い特殊食品原料に対する需要の高まりと一致しています。代替糖は味を損なうことなく、カロリーを削減し血糖値をコントロールする手段を提供します。アスパルテームやサッカリンのような人工甘味料、ステビアベースの天然甘味料を含む代替糖市場は、健康志向の広がりとともに拡大しています。

代替糖の製品タイプ拡大には、健康意識の高まり、糖尿病の流行、政府の後押し、技術の進歩、製品の多様性など、さまざまな要因が絡み合っています。人々が通常の砂糖に代わるより健康的な代替品を探しているため、砂糖代替品市場は今後数年間着実に拡大すると予想されます。

食品着色料は、飲食物の美的魅力を向上させるために不可欠です。明るく人目を引く色は、顧客を引き付け、より魅力的なものにすることができます。食品メーカーは、競争の激しい市場で商品を差別化するために、人工着色料と天然着色料の両方を幅広く使用しています。キャンディ、ベーカリー、飲料など、視覚的アピールが消費者の購買決定に大きな役割を果たす業界では、人目を引く色が特に重要です。

美観に優れ、自然で安全な食品を求める消費者の欲求が市場を牽引し続ける中、特殊食品原料の中の食品着色料カテゴリーは一貫した拡大が見込まれています。業界が技術革新を重視し、製品の差別化、消費者の認識、法令遵守のためのツールとして色を使用することが、この分野の拡大を後押ししています。

当レポートでは、世界の特殊食品原料市場について調査し、市場の概要とともに、タイプ別、流通チャネル別、地域別の動向、および市場に参入する企業のプロファイルなどを提供しています。

目次

第1章 イントロダクション

第2章 調査手法

第3章 エグゼクティブサマリー

第4章 重要考察

第5章 市場概要

- イントロダクション

- 市場力学

第6章 業界の動向

- イントロダクション

- 顧客のビジネスに影響を与える動向/混乱

- バリューチェーン分析

- 技術分析

- 貿易分析

- 特許分析

- ポーターのファイブフォース分析

- ケーススタディ分析

- 価格分析

- 規制の枠組み

- 主要な利害関係者と購入基準

- 主要な会議とイベント

第7章 不況の影響分析、地域別

- 北米:不況の影響分析

- 欧州:不況の影響分析

- アジア太平洋:不況の影響分析

- 南米:不況の影響分析

- その他の地域:不況の影響分析

第8章 酸味料市場

- イントロダクション

- 酸味料市場、用途別

- 酸味料市場、地域別

第9章 着色料市場

- イントロダクション

- 着色料市場、由来別

- 着色料市場、用途別

- 着色料市場、地域別

第10章 香料市場

- イントロダクション

- 香料市場、由来別

- 香料市場、形態別

- 香料市場、タイプ別

- 香料市場、用途別

- 香料市場、地域別

第11章 酵素市場

- イントロダクション

- 酵素市場、用途別

- 酵素市場、地域別

第12章 乳化剤市場

- イントロダクション

- 乳化剤市場、タイプ別

- 乳化剤市場、用途別

- 乳化剤市場、地域別

第13章 F&Bスターターカルチャー市場

- イントロダクション

- F&Bスターターカルチャー市場、用途別

- F&Bスターターカルチャー市場、地域別

第14章 保存料市場

- イントロダクション

- 保存料市場、タイプ別

- 保存料市場、用途別

- 保存料市場、地域別

第15章 機能性食品原料市場

- イントロダクション

- 機能性食品原料市場、タイプ別

- 機能性食品原料市場、用途別

- 機能性食品原料市場、地域別

第16章 特殊澱粉市場

- イントロダクション

- 特殊澱粉市場、タイプ別

- 特殊澱粉市場、用途別

- 特殊澱粉市場、地域別

第17章 砂糖代替品市場

- イントロダクション

- 砂糖代替品市場、タイプ別

- 砂糖代替品市場、用途別

- 砂糖代替品市場、地域別

第18章 特殊食品原料市場、流通チャネル別

- イントロダクション

- 販売代理店

- メーカー

第19章 競合情勢

第20章 企業プロファイル

- 主要参入企業

- ADM

- DSM

- INTERNATIONAL FLAVORS & FRAGRANCES INC.

- KERRY GROUP PLC

- GIVAUDAN

- CARGILL, INCORPORATED

- SENSIENT TECHNOLOGIES CORPORATION

- INGREDION

- CHR. HANSEN HOLDING A/S

- TATE & LYLE

- AMANO ENZYME INC.

- BIOCATALYSTS

- ENZYME SUPPLIES

- ROQUETTE FRERES

- ACE INGREDIENTS CO., LTD.

- スタートアップ/中小企業

- AXIOM FOOD, INC.

- AMCO PROTEINS

- FDL LTD

- CRESPEL & DEITERS GROUP

- AMINOLA

第21章 隣接市場および関連市場

第22章 付録

The specialty food ingredients market is projected to grow from USD 179.8 Billion in 2023 to USD 240.9 Billion by 2028, at a CAGR of 6.0% during the forecast period. The increasing global population, coupled with urbanization trends, has a direct impact on the specialty food ingredients market. As more people move to urban areas, the demand for ready-to-eat food and beverage products rises, creating a higher demand for specialty food ingredients.

The sugar substitutes segment in ingredient type is expected to be one of the dominant segments in the market.

Consumers are looking for healthier substitutes as they become more aware of the harmful health implications of excessive sugar consumption, such as obesity, diabetes, and tooth decay. According to the National Library of Medicine (US) survey on "Consumer willingness to pay for healthier food products", the majority of consumers, as observed in 88.5% of the 26 experiments, are willing to pay a price premium ranging from 5.6% to 91.5% (with a mean of 30.7%) for healthier food options. This consumer behavior aligns with the growing demand for specialty food ingredients, which often cater to the preferences of health-conscious individuals seeking nutritious and better-for-you products. With no taste loss, sugar alternatives provide a means to cut calories and control blood sugar levels. The market for sugar alternatives, including artificial sweeteners like aspartame, saccharin, and stevia-based natural sweeteners, is increasing as health consciousness spreads.

The expansion of the sugar replacements ingredient type category has been spurred by a mix of factors, including increased health consciousness, the prevalence of diabetes, governmental backing, technical advancements, and product diversity. The market for sugar substitutes is anticipated to increase steadily over the next few years as people look for healthier alternatives to regular sugar.

Food color is one of the segments that is projected to grow in the ingredient type segment during the forecast period.

Food colors are essential for improving the aesthetic appeal of food and drink items. Bright, eye-catching colors can draw customers and make things more alluring. Food manufacturers use a wide variety of both artificial and natural food colors to distinguish their goods in a competitive marketplace. In industries like candy, bakery, and drinks, where visual appeal plays a big role in consumer purchasing decisions, eye-catching colors are especially crucial.

The food color category within specialty food ingredients is expected to have consistent expansion as customer desires for aesthetically pleasing, natural, and secure food products continue to drive the market. The industry's emphasis on innovation, the use of colors as a tool for product distinction, consumer perception, and legal compliance are driving the expansion of this segment.

The break-up of the profile of primary participants in the specialty food ingredients market:

- By Company Type: Tier 1 - 40%, Tier 2 - 35%, and Tier 3 - 25%

- By Designation: C Level - 45%, Director Level - 30%, Others-25%

- By Region: Asia Pacific - 35%, Europe - 30%, North America - 25%, and Rest of the World - 10%

Prominent companies include ADM (US), DSM (Netherlands), International Flavors & Fragrances Inc. IFF (US), Kerry Group plc. (Ireland), Cargill, Incorporated (US) and among others.

Research Coverage:

This research report categorizes the specialty food ingredients market by Type (Acidulant, Colors, Flavors, Enzymes, Emulsifiers, F&B Starter Culture, Preservatives, Functional Food Ingredients, Specialty Starches, Sugar Substitutes), Distribution Channel (Distributors and Manufacturers) and Region (North America, Europe, Asia Pacific, South America, and Rest of the World). The scope of the report covers detailed information regarding the major factors, such as drivers, restraints, challenges, and opportunities, influencing the growth of the specialty food ingredients market. A detailed analysis of the key industry players has been done to provide insights into their business overview, solutions, and services; key strategies; contracts, partnerships, agreements, new product & service launches, mergers and acquisitions, and recent developments associated with the specialty food ingredients market. Competitive analysis of upcoming startups in the specialty food ingredients market ecosystem is covered in this report.

Reasons to buy this report:

The report will help the market leaders/new entrants in this market with information on the closest approximations of the revenue numbers for the overall specialty food ingredients market and the subsegments. This report will help stakeholders understand the competitive landscape and gain more insights to position their businesses better and plan suitable go-to-market strategies. The report also helps stakeholders understand the pulse of the market and provides them with information on key market drivers, restraints, challenges, and opportunities.

The report provides insights on the following pointers:

Analysis of key drivers (Growth in demand for fortified food owing to rising health awareness, Shift in consumer preferences for food & beverages), restraints (High cost and limited availability of raw materials, Increase in instances of allergies and intolerances related to few ingredients), opportunity (Rise in the number of end-use applications, Product-based and technological innovations in the ingredient industry), and challenges (Lack of consistency in regulations about various ingredients, Threat of substitutes) influencing the growth of the specialty food ingredients market.

- Product Development/Innovation: Detailed insights on upcoming technologies, research & development activities, and new product & service launches in the specialty food ingredients market.

- Market Development: Comprehensive information about lucrative markets - the report analyses the specialty food ingredients market across varied regions.

- Market Diversification: Exhaustive information about new products & services, untapped geographies, recent developments, and investments in the specialty food ingredients market.

- Competitive Assessment: In-depth assessment of market shares, growth strategies, and service offerings of leading players like ADM (US), DSM (Netherlands), International Flavors & Fragrances Inc. IFF (US), Kerry Group plc. (Ireland), Cargill, Incorporated (US) among others in the specialty food ingredients market strategies. The report also helps stakeholders understand the specialty food ingredients market and provides them with information on key market drivers, restraints, challenges, and opportunities.

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 STUDY OBJECTIVES

- 1.2 MARKET DEFINITION

- 1.3 MARKET SEGMENTATION

- FIGURE 1 SPECIALTY FOOD INGREDIENTS MARKET SEGMENTATION

- 1.3.1 INCLUSIONS & EXCLUSIONS

- TABLE 1 INCLUSIONS AND EXCLUSIONS

- 1.4 REGIONS COVERED

- 1.5 PERIODIZATION CONSIDERED

- 1.6 UNITS CONSIDERED

- 1.6.1 VALUE/CURRENCY UNIT

- TABLE 2 US DOLLAR EXCHANGE RATES CONSIDERED, 2020-2022

- 1.6.2 VOLUME UNIT

- 1.7 STAKEHOLDERS

- 1.8 SUMMARY OF CHANGES

- 1.8.1 RECESSION IMPACT

2 RESEARCH METHODOLOGY

- 2.1 RESEARCH DATA

- FIGURE 2 SPECIALTY FOOD INGREDIENTS MARKET: RESEARCH DESIGN

- 2.1.1 SECONDARY DATA

- 2.1.1.1 Key data from secondary sources

- 2.1.2 PRIMARY DATA

- 2.1.2.1 Key data from primary sources

- 2.1.2.2 Key industry insights

- 2.1.2.3 Breakdown of primary interviews

- FIGURE 3 BREAKDOWN OF PRIMARY INTERVIEWS: BY COMPANY TYPE, DESIGNATION, AND REGION

- 2.2 MARKET SIZE ESTIMATION

- 2.2.1 BOTTOM-UP APPROACH

- FIGURE 4 SPECIALTY FOOD INGREDIENTS MARKET: BOTTOM-UP APPROACH

- 2.2.2 TOP-DOWN APPROACH

- FIGURE 5 SPECIALTY FOOD INGREDIENTS MARKET: TOP-DOWN APPROACH

- 2.3 DATA TRIANGULATION

- FIGURE 6 DATA TRIANGULATION

- 2.4 RESEARCH ASSUMPTIONS

- 2.5 RESEARCH LIMITATIONS

- 2.6 RECESSION IMPACT ANALYSIS

- 2.6.1 MACRO INDICATORS OF RECESSION

- FIGURE 7 INDICATORS OF RECESSION

- FIGURE 8 GLOBAL INFLATION RATE, 2012-2022

- FIGURE 9 GLOBAL GROSS DOMESTIC PRODUCT, 2012-2022 (USD TRILLION)

- FIGURE 10 RECESSION INDICATORS AND THEIR IMPACT ON SPECIALTY FOOD INGREDIENTS MARKET

- FIGURE 11 SPECIALTY FOOD INGREDIENTS MARKET: CURRENT FORECAST VS. RECESSION FORECAST

3 EXECUTIVE SUMMARY

- TABLE 3 SPECIALTY FOOD INGREDIENTS MARKET SNAPSHOT, 2023 VS. 2028

- FIGURE 12 SPECIALTY FOOD INGREDIENTS MARKET, BY TYPE, 2023 VS. 2028 (USD MILLION)

- FIGURE 13 SPECIALTY FOOD INGREDIENTS MARKET, BY DISTRIBUTION CHANNEL, 2023 VS. 2028 (USD MILLION)

- FIGURE 14 SPECIALTY FOOD INGREDIENTS MARKET SHARE (VALUE), BY REGION, 2022

4 PREMIUM INSIGHTS

- 4.1 ATTRACTIVE OPPORTUNITIES FOR SPECIALTY FOOD INGREDIENTS MARKET PLAYERS

- FIGURE 15 RISE IN DEMAND FOR CLEAN-LABEL PRODUCTS TO DRIVE GROWTH OF SPECIALTY FOOD INGREDIENTS MARKET

- 4.2 SPECIALTY FOOD INGREDIENTS MARKET: MAJOR REGIONAL SUBMARKETS FOR DISTRIBUTORS

- FIGURE 16 ASIA PACIFIC WAS PROMINENT MARKET GLOBALLY FOR SPECIALTY FOOD INGREDIENT DISTRIBUTORS IN 2022

- 4.3 SPECIALTY FOOD INGREDIENTS MARKET, BY TYPE

- FIGURE 17 FUNCTIONAL FOOD INGREDIENTS TO DOMINATE MARKET BY 2028

- 4.4 FUNCTIONAL FOOD INGREDIENTS MARKET, BY TYPE

- FIGURE 18 PROBIOTICS TO ACCOUNT FOR LARGEST FUNCTIONAL FOOD INGREDIENTS MARKET SHARE BY 2028

- 4.5 SUGAR SUBSTITUTES MARKET, BY TYPE

- FIGURE 19 HIGH-INTENSITY SWEETENERS TO LEAD SUGAR SUBSTITUTES MARKET THROUGH 2028

5 MARKET OVERVIEW

- 5.1 INTRODUCTION

- 5.2 MARKET DYNAMICS

- FIGURE 20 SPECIALTY FOOD INGREDIENTS: MARKET DYNAMICS

- 5.2.1 DRIVERS

- 5.2.1.1 Growth in demand for fortified food owing to rising health awareness

- FIGURE 21 AUSTRALIA: RETAIL SALES OF FUNCTIONAL AND FORTIFIED FOOD PRODUCTS, 2018-2022 (USD MILLION)

- 5.2.1.1.1 Demand for functional food ingredients due to increase in instances and economic burden of chronic diseases

- FIGURE 22 CHRONIC DISEASES WERE AMONG TOP 10 CAUSES OF DEATH WORLDWIDE ACROSS ALL AGES, 2019

- 5.2.1.1.2 Consumer awareness of micronutrient deficiencies

- 5.2.1.1.3 Malnutrition across regions

- FIGURE 23 PREVALENCE OF MALNUTRITION IN CHILDREN ACROSS ALL MAJOR ECONOMIES, 2022

- 5.2.1.1.4 Partnerships between key players to address nutritional deficiencies

- 5.2.1.2 Shift in consumer preferences for food & beverages

- FIGURE 24 US: CONSUMER CHECKS FOR LABEL AND NUTRITIONAL INFORMATION PANEL (NIP) OF FOOD PRODUCTS, 2019

- 5.2.1.2.1 Shift toward plant-based ingredients and proteins

- FIGURE 25 US: PLANT-BASED FOODS AND SALES GROWTH, BY CATEGORY, 2022 (USD BILLION)

- 5.2.1.2.2 Demand for natural, organic, and clean-label products

- 5.2.1.2.3 Increase in inclination toward premium and branded products

- 5.2.1.3 Increase in government support in major economies

- 5.2.1.3.1 Mandates on food fortification by government organizations

- 5.2.1.4 Consumer demand for nutrition and taste convergence

- 5.2.1.5 Rise in demand for convenience, ready-to-eat, and packaged foods

- 5.2.2 RESTRAINTS

- 5.2.2.1 High cost and limited availability of raw materials

- 5.2.2.1.1 Limited raw material availability due to seasonal changes

- 5.2.2.2 Use of artificial/synthetic ingredients in various applications resulting in health hazards

- 5.2.2.3 Increase in instances of allergies and intolerances related to few ingredients

- 5.2.2.1 High cost and limited availability of raw materials

- 5.2.3 OPPORTUNITIES

- 5.2.3.1 Rise in number of end-use applications

- 5.2.3.1.1 Synergy between ingredients owing to multifunctional attributes

- 5.2.3.1.2 Increase in consumption of processed food

- 5.2.3.1 Rise in number of end-use applications

- FIGURE 26 CONTRIBUTION OF FOODS IN DIETS, 2019

- 5.2.3.1.3 Rapidly growing beverage and functional drinks sales

- FIGURE 27 CHINA: SALES OF VARIOUS TYPES OF BEVERAGES, 2021

- FIGURE 28 US: IMPORT OF BEVERAGE PRODUCTS, 2015-2022 (USD MILLION)

- 5.2.3.2 Product-based and technological innovations in ingredient industry

- TABLE 4 RECENT NEW PRODUCT LAUNCHES, BY KEY PLAYERS, 2020

- 5.2.3.2.1 Use of encapsulation technology

- 5.2.3.3 Emerging economies present high-growth opportunities due to rise in food processing investments

- FIGURE 29 ANNUAL GDP GROWTH OF EMERGING ECONOMIES, 2012-2022

- 5.2.4 CHALLENGES

- 5.2.4.1 Lack of consistency in regulations about various ingredients

- 5.2.4.2 Increase in competition due to presence of low-cost ingredients

- 5.2.4.3 Growth in pressure on global resources and need to tap new raw materials

6 INDUSTRY TRENDS

- 6.1 INTRODUCTION

- 6.2 TRENDS/DISRUPTIONS IMPACTING CUSTOMERS' BUSINESS

- FIGURE 30 REVENUE SHIFT FOR SPECIALTY FOOD INGREDIENTS MARKET

- 6.3 VALUE CHAIN ANALYSIS

- FIGURE 31 SPECIALTY FOOD INGREDIENTS MARKET: VALUE CHAIN ANALYSIS

- 6.3.1 RESEARCH & DEVELOPMENT

- 6.3.2 SOURCING OF RAW MATERIALS

- 6.3.3 PRODUCTION & PROCESSING

- 6.3.4 DISTRIBUTION, MARKETING, AND SALES

- 6.4 TECHNOLOGY ANALYSIS

- 6.4.1 PROTECTION OF SPECIALTY FOOD INGREDIENTS USING ENCAPSULATION

- 6.5 MARKET MAPPING

- FIGURE 32 ECOSYSTEM MAP

- FIGURE 33 SPECIALTY FOOD INGREDIENTS MARKET MAP

- TABLE 5 SPECIALTY FOOD INGREDIENTS MARKET: ECOSYSTEM

- 6.5.1 SUPPLY SIDE

- FIGURE 34 PRODUCT DEVELOPMENT AND MANUFACTURING PLAY VITAL ROLE IN SPECIALTY FOOD INGREDIENTS SUPPLY CHAIN

- 6.6 TRADE ANALYSIS

- TABLE 6 TOP 10 EXPORTERS AND IMPORTERS OF ENZYMES, 2022 (USD THOUSAND)

- TABLE 7 TOP 10 EXPORTERS AND IMPORTERS OF ENZYMES, 2022 (TON)

- TABLE 8 TOP 10 EXPORTERS AND IMPORTERS OF VITAMINS AND PROVITAMINS, 2022 (USD THOUSAND)

- TABLE 9 TOP 10 EXPORTERS AND IMPORTERS OF VITAMINS AND PROVITAMINS, 2022 (TON)

- TABLE 10 TOP 10 EXPORTERS AND IMPORTERS OF DEXTRINS AND MODIFIED STARCHES, 2022 (USD THOUSAND)

- TABLE 11 TOP 10 EXPORTERS AND IMPORTERS OF DEXTRINS AND MODIFIED STARCHES, 2022 (TON)

- 6.7 PATENT ANALYSIS

- FIGURE 35 PATENTS GRANTED FOR SPECIALTY FOOD INGREDIENTS MARKET, 2013-2022

- TABLE 12 KEY PATENTS ABOUT SPECIALTY FOOD INGREDIENTS MARKET, 2021-2023

- 6.8 PORTER'S FIVE FORCES ANALYSIS

- FIGURE 36 HIGH INTENSITY OF COMPETITIVE RIVALRY OWING TO STRONG FOCUS ON NEW PRODUCT INNOVATIONS BY KEY PLAYERS

- TABLE 13 SPECIALTY FOOD INGREDIENTS MARKET: PORTER'S FIVE FORCES ANALYSIS

- 6.8.1 INTENSITY OF COMPETITIVE RIVALRY

- 6.8.2 BARGAINING POWER OF SUPPLIERS

- 6.8.3 BARGAINING POWER OF BUYERS

- 6.8.4 THREAT FROM NEW ENTRANTS

- 6.8.5 THREAT FROM SUBSTITUTES

- 6.9 CASE STUDY ANALYSIS

- 6.9.1 MIND RIGHT'S PLANT-BASED BARS WAS FORMULAED TO FOCUS ON MENTAL HEALTH ISSUES

- 6.10 PRICING ANALYSIS

- 6.10.1 SPECIALTY FOOD INGREDIENTS MARKET, BY TYPE

- TABLE 14 SPECIALTY FOOD INGREDIENTS MARKET: AVERAGE SELLING PRICE, BY TYPE, 2018-2023 (USD/KG)

- TABLE 15 SPECIALTY FOOD INGREDIENTS MARKET: AVERAGE SELLING PRICE, BY REGION, 2018-2023 (USD/KG)

- 6.11 REGULATORY FRAMEWORK

- 6.11.1 REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 16 NORTH AMERICA: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 17 EUROPE: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- TABLE 18 ASIA PACIFIC: LIST OF REGULATORY BODIES, GOVERNMENT AGENCIES, AND OTHER ORGANIZATIONS

- 6.12 NORTH AMERICA: REGULATIONS

- 6.12.1 REGULATIONS FOR ENZYMES

- TABLE 19 ENZYME PREPARATION APPROVED-FOOD ADDITIVES LISTED IN 21 CFR 173

- TABLE 20 ENZYME PREPARATION SPECIFIED IN FOOD STANDARDS

- TABLE 21 ENZYME PREPARATIONS AFFIRMED AS GRAS LISTED IN 21 CFR 184

- 6.12.2 REGULATIONS FOR SUGAR SUBSTITUTES

- 6.12.2.1 US

- 6.12.2.2 Canada

- 6.12.3 REGULATIONS FOR MEAT SUBSTITUTES

- 6.12.3.1 US

- 6.12.3.1.1 Wheat protein

- 6.12.3.1.2 Soy protein

- 6.12.3.2 Canada

- 6.12.3.2.1 Soy protein

- 6.12.3.1 US

- 6.12.4 REGULATIONS FOR FOOD COLORS

- TABLE 22 COMMON COLOR ADDITIVES EXEMPTED FROM CERTIFICATION

- 6.12.5 REGULATIONS FOR FLAVORS

- 6.13 EUROPE: REGULATIONS

- 6.13.1 REGULATIONS FOR ENZYMES

- TABLE 23 EUROPE: LIST OF PERMITTED ENZYMES

- 6.13.1.1 EU legislation relevant to food enzymes

- 6.13.2 REGULATIONS FOR FOOD ADDITIVES

- 6.13.2.1 Hydrocolloids

- TABLE 24 LIST OF HYDROCOLLOIDS USED IN FOOD INDUSTRY

- 6.13.2.2 Carotenoids

- 6.13.2.3 UK

- 6.13.3 REGULATIONS FOR MEAT SUBSTITUTES

- 6.13.3.1 Wheat protein

- 6.13.3.2 Soy protein

- 6.13.4 REGULATIONS FOR FOOD FLAVORS

- 6.14 ASIA AND AUSTRALIA & NEW ZEALAND: REGULATIONS

- 6.14.1 REGULATIONS FOR ENZYMES

- 6.14.2 REGULATIONS FOR FOOD ADDITIVES

- 6.14.3 REGULATIONS FOR SUGAR SUBSTITUTES

- 6.14.3.1 Hong Kong

- 6.14.4 REGULATIONS FOR MEAT SUBSTITUTES

- 6.14.4.1 India

- 6.14.4.1.1 Wheat protein usage level recommendation of Food Safety and Standards Authority of India (FSSAI)

- 6.14.4.1 India

- 6.15 CODEX ALIMENTARIUS

- 6.15.1 REGULATIONS FOR FOOD ADDITIVES

- 6.15.2 REGULATIONS FOR SUGAR SUBSTITUTES

- TABLE 25 LIST OF NON-NUTRITIVE SWEETENERS: MAXIMUM USAGE LEVEL

- 6.15.3 REGULATIONS FOR DIETARY FIBERS

- 6.15.3.1 Prosky method

- 6.15.3.2 McCleary method

- 6.15.3.3 Rapid integrated total dietary fiber

- 6.16 KEY STAKEHOLDERS AND BUYING CRITERIA

- 6.16.1 KEY STAKEHOLDERS IN BUYING PROCESS

- FIGURE 37 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR FUNCTIONAL FOOD INGREDIENT TYPES

- TABLE 26 INFLUENCE OF STAKEHOLDERS ON BUYING PROCESS FOR FUNCTIONAL FOOD INGREDIENT TYPES

- 6.16.2 BUYING CRITERIA

- TABLE 27 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS OF FUNCTIONAL FOOD INGREDIENTS

- FIGURE 38 KEY CRITERIA FOR SELECTING SUPPLIERS/VENDORS

- 6.17 KEY CONFERENCES & EVENTS

- TABLE 28 SPECIALTY FOOD INGREDIENTS MARKET: DETAILED LIST OF CONFERENCES & EVENTS, 2023-2024

7 RECESSION IMPACT ANALYSIS, BY REGION

- 7.1 NORTH AMERICA: RECESSION IMPACT ANALYSIS

- FIGURE 39 NORTH AMERICA: SPECIALTY FOOD INGREDIENTS MARKET, RECESSION IMPACT ANALYSIS

- 7.2 EUROPE: RECESSION IMPACT ANALYSIS

- FIGURE 40 EUROPE: SPECIALTY FOOD INGREDIENTS MARKET, RECESSION IMPACT ANALYSIS

- 7.3 ASIA PACIFIC: RECESSION IMPACT ANALYSIS

- FIGURE 41 ASIA PACIFIC: SPECIALTY FOOD INGREDIENTS MARKET SNAPSHOT

- 7.4 SOUTH AMERICA: RECESSION IMPACT ANALYSIS

- FIGURE 42 SOUTH AMERICA: SPECIALTY FOOD INGREDIENTS MARKET, RECESSION IMPACT ANALYSIS

- 7.5 ROW: RECESSION IMPACT

- FIGURE 43 ROW: SPECIALTY FOOD INGREDIENTS MARKET, RECESSION IMPACT ANALYSIS

8 ACIDULANTS MARKET

- 8.1 INTRODUCTION

- 8.2 ACIDULANTS MARKET, BY APPLICATION

- 8.2.1 INCREASE IN DEMAND FOR CARBONATED BEVERAGES & SOFT DRINKS

- TABLE 29 APPLICATIONS OF ACIDULANTS

- TABLE 30 ACIDULANTS MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 31 ACIDULANTS MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 32 ACIDULANTS MARKET, BY FOOD APPLICATION, 2018-2022 (USD MILLION)

- TABLE 33 ACIDULANTS MARKET, BY FOOD APPLICATION, 2023-2028 (USD MILLION)

- 8.2.1.1 Beverages

- 8.2.1.1.1 Citric acid: Widely used food additive owing to acidifying and flavor-enhancing qualities

- 8.2.1.2 Food

- 8.2.1.2.1 Increase in demand for convenience foods

- 8.2.1.2.2 Sauces, dressings, and condiments

- 8.2.1.2.2.1 High demand for acidulants in Asian cuisines

- 8.2.1.2.3 Processed foods

- 8.2.1.2.3.1 Increase in investments in food ingredients

- 8.2.1.2.4 Meat, poultry, and seafood

- 8.2.1.2.4.1 Need to inhibit microbial growth on meat

- 8.2.1.2.5 Bakery & confectionery

- 8.2.1.2.5.1 Demand for extended shelf life of bakery products

- 8.2.1.2.6 Other food applications

- 8.2.1.1 Beverages

- 8.3 ACIDULANTS MARKET, BY REGION

- 8.3.1 INCREASE IN END-USER APPLICATIONS ACROSS REGIONS DUE TO MULTIFUNCTIONAL ATTRIBUTES OF ACIDULANTS

- FIGURE 44 CHINA AND GERMANY TO GROW AT HIGHEST RATES DURING FORECAST PERIOD IN ACIDULANTS MARKET

- TABLE 34 ACIDULANTS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 35 ACIDULANTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 36 ACIDULANTS MARKET, BY REGION, 2018-2022 (KT)

- TABLE 37 ACIDULANTS MARKET, BY REGION, 2023-2028 (KT)

- 8.3.1.1 North America

- TABLE 38 NORTH AMERICA: ACIDULANTS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 39 NORTH AMERICA: ACIDULANTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 8.3.1.2 Europe

- TABLE 40 EUROPE: ACIDULANTS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 41 EUROPE: ACIDULANTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 8.3.1.3 Asia Pacific

- TABLE 42 ASIA PACIFIC: ACIDULANTS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 43 ASIA PACIFIC: ACIDULANTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 8.3.1.4 South America

- TABLE 44 SOUTH AMERICA: ACIDULANTS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 45 SOUTH AMERICA: ACIDULANTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 8.3.1.5 RoW

- TABLE 46 ROW: ACIDULANTS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 47 ROW: ACIDULANTS MARKET, BY REGION, 2023-2028 (USD MILLION)

9 COLORS MARKET

- 9.1 INTRODUCTION

- 9.2 COLORS MARKET, BY ORIGIN

- 9.2.1 RISE IN DEMAND FOR CLEAN-LABEL NATURAL INGREDIENTS

- TABLE 48 COLORS MARKET, BY ORIGIN, 2018-2022 (USD MILLION)

- TABLE 49 COLORS MARKET, BY ORIGIN, 2023-2028 (USD MILLION)

- 9.2.2 NATURAL

- 9.2.2.1 Increase in demand for natural safe-to-use food colors

- 9.2.3 SYNTHETIC

- 9.2.3.1 Demand for visually appealing colors in food products

- 9.2.4 NATURE-IDENTICAL

- 9.2.4.1 Low costs of nature-identical colors

- 9.3 COLORS MARKET, BY APPLICATION

- 9.3.1 GROWTH IN DEMAND FOR JUICES & FUNCTIONAL BEVERAGES

- TABLE 50 COLORS MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 51 COLORS MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 52 COLORS MARKET, BY FOOD APPLICATION, 2018-2022 (USD MILLION)

- TABLE 53 COLORS MARKET, BY FOOD APPLICATION, 2023-2028 (USD MILLION)

- 9.3.2 BEVERAGES

- 9.3.2.1 Availability of new, refreshing, and healthier juices and beverages

- 9.3.3 FOOD

- 9.3.3.1 Growth in preference for healthy natural ingredients

- 9.3.3.2 Processed food

- 9.3.3.2.1 Increase in demand for clean-label ingredients in processed food products

- 9.3.3.3 Bakery & confectionery

- 9.3.3.3.1 Nature-identical food colors such as carmine and lycopene used in cakes and bread

- 9.3.3.4 Meat, poultry, and seafood

- 9.3.3.4.1 Natural food coloring such as curing to provide stable red muscle pigment

- 9.3.3.5 Oils & fats

- 9.3.3.5.1 Colors in cooking oil enhance visual appeal of product

- 9.3.3.6 Dairy products

- 9.3.3.6.1 Natural food colors work well in sugar-free applications

- 9.3.3.7 Other food applications

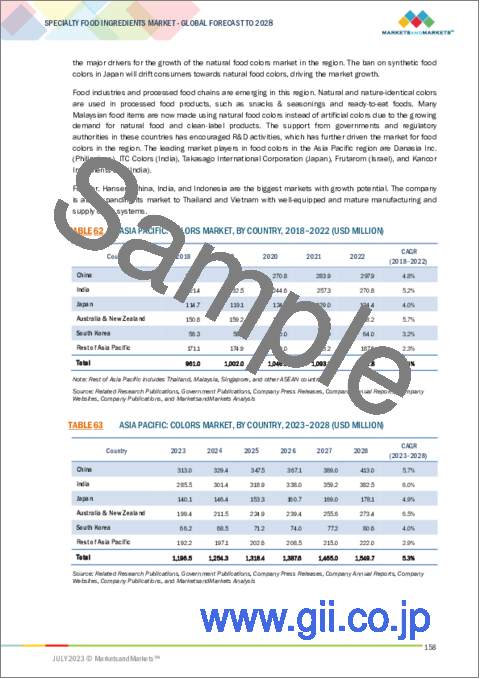

- 9.4 COLORS MARKET, BY REGION

- 9.4.1 RISE IN PROCESSED FOOD CONSUMPTION ACROSS REGIONS

- FIGURE 45 COLORS MARKET: REGIONAL AND COUNTRY-LEVEL GROWTH RATES, 2023-2028

- TABLE 54 COLORS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 55 COLORS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 56 COLORS MARKET, BY REGION, 2018-2022 (KT)

- TABLE 57 COLORS MARKET, BY REGION, 2023-2028 (KT)

- 9.4.2 NORTH AMERICA

- TABLE 58 NORTH AMERICA: COLORS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 59 NORTH AMERICA: COLORS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.4.3 EUROPE

- TABLE 60 EUROPE: COLORS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 61 EUROPE: COLORS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.4.4 ASIA PACIFIC

- TABLE 62 ASIA PACIFIC: COLORS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 63 ASIA PACIFIC: COLORS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.4.5 SOUTH AMERICA

- TABLE 64 SOUTH AMERICA: COLORS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 65 SOUTH AMERICA: COLORS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 9.4.6 ROW

- TABLE 66 ROW: COLORS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 67 ROW: COLORS MARKET, BY REGION, 2023-2028 (USD MILLION)

10 FOOD FLAVORS MARKET

- 10.1 INTRODUCTION

- 10.2 FOOD FLAVORS MARKET, BY ORIGIN

- 10.2.1 INCREASE IN POPULARITY OF ORGANIC FOODS TO DRIVE NATURAL FLAVORS MARKET

- TABLE 68 FOOD FLAVORS MARKET, BY ORIGIN, 2018-2022 (USD MILLION)

- TABLE 69 FOOD FLAVORS MARKET, BY ORIGIN, 2023-2028 (USD MILLION)

- 10.2.2 NATURAL

- 10.2.2.1 Fruit & nut flavors, chocolate flavors, and vanilla-popular natural flavors

- 10.2.3 SYNTHETIC

- 10.2.3.1 Increase in demand for synthetic food flavors due to their cost-effectiveness and affordability.

- 10.2.4 NATURE-IDENTICAL

- 10.2.4.1 Demand for nature-identical food flavors fueled by evolving consumer preferences

- 10.3 FOOD FLAVORS MARKET, BY FORM

- 10.3.1 SEVERAL CLASSES OF ORGANIC COMPOUNDS USED AS AROMAS

- TABLE 70 FOOD FLAVORS MARKET, BY FORM, 2018-2022 (USD MILLION)

- TABLE 71 FOOD FLAVORS MARKET, BY FORM, 2023-2028 (USD MILLION)

- 10.3.2 LIQUID & GEL

- 10.3.2.1 Increase in production of alcoholic and non-alcoholic beverages

- 10.3.3 DRY

- 10.3.3.1 Surge in popularity of baked and confectionery foods using dry flavors

- 10.4 FOOD FLAVORS MARKET, BY TYPE

- 10.4.1 GROWTH IN DEMAND FOR SPICES, HERBS, OR CONDIMENTS

- TABLE 72 FOOD FLAVORS MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 73 FOOD FLAVORS MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 10.4.2 CHOCOLATE & BROWN

- 10.4.2.1 Dark chocolate

- 10.4.2.2 Milk chocolate

- 10.4.2.3 White chocolate

- 10.4.2.4 Caramel

- 10.4.3 VANILLA

- 10.4.3.1 Bourbon-Madagascar vanilla

- 10.4.3.2 Mexican vanilla

- 10.4.3.3 Tahitian vanilla

- 10.4.4 FRUITS

- 10.4.4.1 Citrus

- 10.4.4.2 Tree fruits

- 10.4.4.3 Tropical & exotic fruits

- 10.4.4.4 Berries

- 10.4.4.5 Other fruits

- 10.4.5 DAIRY

- 10.4.5.1 Milk

- 10.4.5.2 Butter

- 10.4.5.3 Cream

- 10.4.5.4 Yogurt

- 10.4.5.5 Cheese

- 10.4.5.6 Other dairy flavors

- 10.4.6 SPICES & SAVORY

- 10.4.6.1 Essential oils & oleoresins

- 10.4.6.2 Vegetable flavors

- 10.4.6.3 Meat flavors

- 10.4.6.4 Other spices & savory

- 10.4.7 MINT

- 10.4.8 OTHER FLAVORS

- 10.5 FOOD FLAVORS MARKET, BY APPLICATION

- 10.5.1 INTRODUCTION OF VARIETY AND STABILITY OF FLAVOR ADDITIVES

- TABLE 74 FOOD FLAVORS MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 75 FOOD FLAVORS MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 76 FOOD FLAVORS MARKET, BY FOOD APPLICATION, 2018-2022 (USD MILLION)

- TABLE 77 FOOD FLAVORS MARKET, BY FOOD APPLICATION, 2023-2028 (USD MILLION)

- 10.5.2 FOOD

- 10.5.2.1 Increase in awareness among consumers about health benefits

- 10.5.2.2 Confectionery products

- 10.5.2.2.1 Shift toward healthier snacking

- 10.5.2.3 Bakery products

- 10.5.2.3.1 Increase in market potential for fusion flavors

- 10.5.2.4 Dairy products

- 10.5.2.4.1 Popularity of plant-based food culture to urge dairy industries to introduce experimental flavors

- 10.5.2.5 Meat & products

- 10.5.2.5.1 Proliferation in flavor and aroma of meat & seafood

- 10.5.2.6 Other food applications

- 10.5.3 BEVERAGES

- 10.5.3.1 High demand for variety in bottled water

- 10.6 FOOD FLAVORS MARKET, BY REGION

- 10.6.1 INCREASE IN R&D ACTIVITIES FOR DIFFERENT FUNCTIONAL FOODS IN DEVELOPED REGIONS

- FIGURE 46 BRAZIL TO GROW AT HIGHEST CAGR IN FOOD FLAVORS MARKET DURING FORECAST PERIOD

- TABLE 78 FOOD FLAVORS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 79 FOOD FLAVORS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 80 FOOD FLAVORS MARKET, BY REGION, 2018-2022 (KT)

- TABLE 81 FOOD FLAVORS MARKET, BY REGION, 2023-2028 (KT)

- 10.6.2 NORTH AMERICA

- TABLE 82 NORTH AMERICA: FOOD FLAVORS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 83 NORTH AMERICA: FOOD FLAVORS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.6.3 EUROPE

- TABLE 84 EUROPE: FOOD FLAVORS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 85 EUROPE: FOOD FLAVORS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.6.4 ASIA PACIFIC

- TABLE 86 ASIA PACIFIC: FOOD FLAVORS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 87 ASIA PACIFIC: FOOD FLAVORS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.6.5 SOUTH AMERICA

- TABLE 88 SOUTH AMERICA: FOOD FLAVORS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 89 SOUTH AMERICA: FOOD FLAVORS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 10.6.6 ROW

- TABLE 90 ROW: FOOD FLAVORS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 91 ROW: FOOD FLAVORS MARKET, BY REGION, 2023-2028 (USD MILLION)

11 ENZYMES MARKET

- 11.1 INTRODUCTION

- 11.2 ENZYMES MARKET, BY APPLICATION

- 11.2.1 INDUSTRIAL USAGE OF ENZYMES FOR FOOD & BEVERAGE APPLICATIONS

- TABLE 92 ENZYMES & THEIR APPLICATIONS

- TABLE 93 ENZYMES MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 94 ENZYMES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 11.2.2 FOOD

- 11.2.2.1 Growth of dairy and bakery products segments due to extensive range of enzymes and broader applications

- TABLE 95 ENZYMES MARKET, BY FOOD APPLICATION, 2018-2022 (USD MILLION)

- TABLE 96 ENZYMES MARKET, BY FOOD APPLICATION, 2023-2028 (USD MILLION)

- 11.2.2.1.1 Bakery & confectionery products

- 11.2.2.1.2 Dairy products

- 11.2.2.1.3 Meat processing products

- 11.2.2.1.4 Nutraceuticals

- 11.2.2.1.5 Other food applications

- 11.2.3 BEVERAGES

- 11.2.3.1 Use of pectin in beverages to help improve yield and quality

- TABLE 97 ENZYMES USED IN BEVERAGE APPLICATIONS

- 11.3 ENZYMES MARKET, BY REGION

- 11.3.1 ENZYMES AID IN INCREASING SHELF LIFE OF FOOD PRODUCTS, MITIGATING FOOD WASTAGE ACROSS REGIONS

- FIGURE 47 INDIA TO GROW AT HIGHEST RATE IN ENZYMES MARKET DURING FORECAST PERIOD

- TABLE 98 ENZYMES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 99 ENZYMES MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 100 ENZYMES MARKET, BY REGION, 2018-2022 (KT)

- TABLE 101 ENZYMES MARKET, BY REGION, 2023-2028 (KT)

- 11.3.1.1 North America

- TABLE 102 NORTH AMERICA: ENZYMES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 103 NORTH AMERICA: ENZYMES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.3.1.2 Europe

- TABLE 104 EUROPE: ENZYMES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 105 EUROPE: ENZYMES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.3.1.3 Asia Pacific

- TABLE 106 ASIA PACIFIC: ENZYMES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 107 ASIA PACIFIC: ENZYMES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.3.1.4 South America

- TABLE 108 SOUTH AMERICA: ENZYMES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 109 SOUTH AMERICA: ENZYMES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 11.3.1.5 RoW

- TABLE 110 ROW: ENZYMES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 111 ROW: ENZYMES MARKET, BY REGION, 2023-2028 (USD MILLION)

12 EMULSIFIERS MARKET

- 12.1 INTRODUCTION

- 12.2 EMULSIFIERS MARKET, BY TYPE

- 12.2.1 DIVERSE FUNCTIONALITIES OF EMULSIFIERS FIND APPLICATIONS IN FOOD AND OTHER SEGMENTS

- TABLE 112 EMULSIFIERS MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 113 EMULSIFIERS MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 12.2.1.1 Mono- & di-glycerides and their derivatives

- 12.2.1.1.1 Wide range of functionalities to boost applications

- 12.2.1.2 Lecithin (oiled & de-oiled)

- 12.2.1.2.1 Increase in demand for vegan products to drive growth for plant-sourced lecithin

- 12.2.1.3 Sorbitan esters

- 12.2.1.3.1 Aeration property of sorbitan esters to widen their scope of application

- 12.2.1.4 Stearoyl lactylates

- 12.2.1.4.1 Dough strengthening and foaming properties to widen usage of stearoyl lactylates

- 12.2.1.5 Polyglycerol esters

- 12.2.1.5.1 Cost-efficiency is associated with usage of polyglycerol esters

- 12.2.1.6 Other types

- 12.2.1.1 Mono- & di-glycerides and their derivatives

- 12.3 EMULSIFIERS MARKET, BY APPLICATION

- 12.3.1 EMULSIFIERS PROVIDE RICH TEXTURE AND SMOOTH FINISH TO FOOD PRODUCTS

- TABLE 114 EMULSIFIERS MARKET, BY FOOD & BEVERAGE APPLICATION, 2018-2022 (USD MILLION)

- TABLE 115 EMULSIFIERS MARKET, BY FOOD & BEVERAGE APPLICATION, 2023-2028 (USD MILLION)

- 12.3.2 BAKERY PRODUCTS

- 12.3.2.1 Popularity of yeast-raised bakery products

- 12.3.3 CONFECTIONERY PRODUCTS

- 12.3.3.1 Emulsifiers to aid in processing and storage

- 12.3.4 CONVENIENCE FOOD

- 12.3.4.1 Increase in demand for healthier convenience foods

- 12.3.5 DAIRY & FROZEN DESSERTS

- 12.3.5.1 Variety of products using emulsifiers

- 12.3.6 MEAT PRODUCTS

- 12.3.6.1 Cost-efficiency due to addition of emulsifiers

- 12.3.6.2 Hot processed meat emulsion

- 12.3.6.3 Cold processed meat emulsion

- 12.3.7 OTHER APPLICATIONS

- 12.4 EMULSIFIERS MARKET, BY REGION

- 12.4.1 INCREASE IN POPULARITY OF CLEAN-LABEL, INERT, AND BACTERIA-RESISTANT FOOD

- FIGURE 48 EMULSIFIERS MARKET: REGIONAL & COUNTRY-LEVEL GROWTH RATES, 2023-2028

- TABLE 116 EMULSIFIERS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 117 EMULSIFIERS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 118 EMULSIFIERS MARKET, BY REGION, 2018-2022 (KT)

- TABLE 119 EMULSIFIERS MARKET, BY REGION, 2023-2028 (KT)

- 12.4.1.1 North America

- TABLE 120 NORTH AMERICA: EMULSIFIERS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 121 NORTH AMERICA: EMULSIFIERS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 12.4.1.2 Europe

- TABLE 122 EUROPE: EMULSIFIERS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 123 EUROPE: EMULSIFIERS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 12.4.1.3 Asia Pacific

- TABLE 124 ASIA PACIFIC: EMULSIFIERS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 125 ASIA PACIFIC: EMULSIFIERS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 12.4.1.4 South America

- TABLE 126 SOUTH AMERICA: EMULSIFIERS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 127 SOUTH AMERICA: EMULSIFIERS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 12.4.1.5 RoW

- TABLE 128 ROW: EMULSIFIERS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 129 ROW: EMULSIFIERS MARKET, BY REGION, 2023-2028 (USD MILLION)

13 F&B STARTER CULTURES MARKET

- 13.1 INTRODUCTION

- 13.2 F&B STARTER CULTURES MARKET, BY APPLICATION

- 13.2.1 RISE IN POPULARITY OF PROBIOTICS

- TABLE 130 F&B STARTER CULTURES MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 131 F&B STARTER CULTURES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 13.2.2 DAIRY & DAIRY PRODUCTS

- 13.2.2.1 Cheese to be largest application of starter cultures

- TABLE 132 F&B STARTER CULTURES MARKET, BY DAIRY & DAIRY PRODUCTS, 2018-2022 (USD MILLION)

- TABLE 133 F&B STARTER CULTURES MARKET, BY DAIRY & DAIRY PRODUCTS, 2023-2028 (USD MILLION)

- 13.2.2.2 Cheese

- 13.2.2.3 Yogurt

- 13.2.2.4 Butter & creams

- 13.2.2.5 Other dairy products

- 13.2.3 MEAT & SEAFOOD

- 13.2.3.1 Starter cultures help in effective preservation of fermented meat

- 13.2.4 OTHER APPLICATIONS

- 13.3 F&B STARTER CULTURES MARKET, BY REGION

- 13.3.1 DAIRY INDUSTRY TO DRIVE GLOBAL F&B STARTER CULTURES MARKET

- FIGURE 49 F&B STARTER CULTURES MARKET: REGIONAL AND COUNTRY-LEVEL GROWTH RATES

- TABLE 134 F&B STARTER CULTURES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 135 F&B STARTER CULTURES MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 136 F&B STARTER CULTURES MARKET, BY REGION, 2018-2022 (KT)

- TABLE 137 F&B STARTER CULTURES MARKET, BY REGION, 2023-2028 (KT)

- 13.3.2 NORTH AMERICA

- TABLE 138 NORTH AMERICA: F&B STARTER CULTURES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 139 NORTH AMERICA: F&B STARTER CULTURES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 13.3.3 EUROPE

- TABLE 140 EUROPE: F&B STARTER CULTURES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 141 EUROPE: F&B STARTER CULTURES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 13.3.4 ASIA PACIFIC

- TABLE 142 ASIA PACIFIC: F&B STARTER CULTURES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 143 ASIA PACIFIC: F&B STARTER CULTURES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 13.3.5 SOUTH AMERICA

- TABLE 144 SOUTH AMERICA: F&B STARTER CULTURES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 145 SOUTH AMERICA: F&B STARTER CULTURES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 13.3.6 ROW

- TABLE 146 ROW: F&B STARTER CULTURES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 147 ROW: F&B STARTER CULTURES MARKET, BY REGION, 2023-2028 (USD MILLION)

14 PRESERVATIVES MARKET

- 14.1 INTRODUCTION

- TABLE 148 PRESERVATIVES MARKET: FUNCTIONS AND PERMISSIBLE LIMITS IN FOOD PRODUCTS

- 14.2 PRESERVATIVES MARKET, BY TYPE

- 14.2.1 NATURAL PRESERVATIVES TO BECOME POPULAR WITH AWARENESS REGARDING ORGANIC SOURCES

- TABLE 149 PRESERVATIVES MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 150 PRESERVATIVES MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 14.2.2 NATURAL PRESERVATIVES

- 14.2.2.1 High consumer awareness and preference for natural food ingredients

- 14.2.3 SYNTHETIC PRESERVATIVES

- 14.2.3.1 Cost-effectiveness and easy availability

- TABLE 151 SYNTHETIC FOOD PRESERVATIVE APPLICATIONS AND ASSOCIATED HEALTH RISKS

- TABLE 152 PRESERVATIVES MARKET, BY SYNTHETIC TYPE, 2018-2022 (USD MILLION)

- TABLE 153 PRESERVATIVES MARKET, BY SYNTHETIC TYPE, 2023-2028 (USD MILLION)

- 14.2.3.2 Sorbates

- 14.2.3.3 Benzoates

- 14.2.3.4 Propionates

- 14.2.3.5 Other synthetic preservatives

- 14.3 PRESERVATIVES MARKET, BY APPLICATION

- 14.3.1 BUSY LIFESTYLES FUEL DEMAND FOR PRESERVATIVE-INDUCED FOOD & BEVERAGES

- TABLE 154 PRESERVATIVES MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 155 PRESERVATIVES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 14.3.2 FOOD

- 14.3.2.1 Use of preservatives in food products to enhance shelf life and food safety

- TABLE 156 PRESERVATIVES MARKET, BY FOOD APPLICATION, 2018-2022 (USD MILLION)

- TABLE 157 PRESERVATIVES MARKET, BY FOOD APPLICATION, 2023-2028 (USD MILLION)

- 14.3.2.2 Oils & fats

- 14.3.2.2.1 High demand for natural antioxidants in vegetable oil preservation

- 14.3.2.3 Bakery products

- 14.3.2.3.1 Increase in adoption of calcium & sodium propionates in baking goods

- 14.3.2.4 Dairy & frozen products

- 14.3.2.4.1 Rise in consumption of dairy products

- 14.3.2.5 Snacks

- 14.3.2.5.1 Greater preference for convenient and ultra-processed food products

- 14.3.2.6 Meat, poultry, and seafood

- 14.3.2.6.1 Rise in consumption of meat and seafood worldwide

- 14.3.2.7 Confectionery products

- 14.3.2.7.1 Higher demand for preserving food aesthetics

- 14.3.2.8 Other food applications

- 14.3.2.2 Oils & fats

- 14.3.3 BEVERAGES

- 14.3.3.1 Rise in preference for naturally flavored health drinks to increase adoption of benzoates and sorbates

- 14.4 PRESERVATIVES MARKET, BY REGION

- 14.4.1 INCREASE IN CONSUMPTION OF CANNED FOODS

- FIGURE 50 PRESERVATIVES MARKET: REGIONAL & COUNTRY-LEVEL GROWTH RATES, 2023-2028

- TABLE 158 PRESERVATIVES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 159 PRESERVATIVES MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 160 PRESERVATIVES MARKET, BY REGION, 2018-2022 (KT)

- TABLE 161 PRESERVATIVES MARKET, BY REGION, 2023-2028 (KT)

- 14.4.2 NORTH AMERICA

- TABLE 162 NORTH AMERICA: PRESERVATIVES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 163 NORTH AMERICA: PRESERVATIVES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 14.4.3 EUROPE

- TABLE 164 EUROPE: PRESERVATIVES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 165 EUROPE: PRESERVATIVES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 14.4.4 ASIA PACIFIC

- TABLE 166 ASIA PACIFIC: PRESERVATIVES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 167 ASIA PACIFIC: PRESERVATIVES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 14.4.5 SOUTH AMERICA

- TABLE 168 SOUTH AMERICA: PRESERVATIVES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 169 SOUTH AMERICA: PRESERVATIVES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 14.4.6 ROW

- TABLE 170 ROW: PRESERVATIVES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 171 ROW: PRESERVATIVES MARKET, BY REGION, 2023-2028 (USD MILLION)

15 FUNCTIONAL FOOD INGREDIENTS MARKET

- 15.1 INTRODUCTION

- 15.2 FUNCTIONAL FOOD INGREDIENTS MARKET, BY TYPE

- 15.2.1 RISE IN CHRONIC DISEASES

- TABLE 172 FUNCTIONAL FOOD INGREDIENTS MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 173 FUNCTIONAL FOOD INGREDIENTS MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 15.2.2 PROBIOTICS

- 15.2.2.1 High consumer demand for scientifically proven health food and supplements, particularly in developed economies

- TABLE 174 PROBIOTIC COMPONENTS AND THEIR BENEFITS

- 15.2.3 PROTEINS & AMINO ACIDS

- 15.2.3.1 Rise in awareness about health benefits of amino acids

- 15.2.4 PHYTOCHEMICAL & PLANT EXTRACTS

- 15.2.4.1 Side effects of chemical ingredients in nutraceuticals

- 15.2.5 PREBIOTICS

- 15.2.5.1 Benefits in weight management and infant health improvement

- TABLE 175 PREBIOTIC COMPONENTS AND THEIR BENEFITS

- 15.2.6 FIBERS & SPECIALTY CARBOHYDRATES

- 15.2.6.1 Need to promote health and reduce risk of chronic diseases

- 15.2.7 OMEGA-3 FATTY ACIDS

- 15.2.7.1 Need to reduce consequences of several chronic mental and physical diseases

- 15.2.8 CAROTENOIDS

- 15.2.8.1 Potential of lutein and zeaxanthin in reducing risk of eye diseases

- 15.2.9 VITAMINS

- 15.2.9.1 Awareness, wide acceptance, and easy availability of different types of vitamins

- 15.2.10 MINERALS

- 15.2.10.1 Several health benefits of macro and microminerals

- 15.2.10.2 Macrominerals

- 15.2.10.3 Microminerals

- 15.3 FUNCTIONAL FOOD INGREDIENTS MARKET, BY APPLICATION

- 15.3.1 DEMAND FOR VERSATILE HEALTH BENEFITS AND ADDED SENSORY BENEFITS

- TABLE 176 FUNCTIONAL FOOD INGREDIENTS MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 177 FUNCTIONAL FOOD INGREDIENTS MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- TABLE 178 FUNCTIONAL FOOD INGREDIENTS MARKET, BY FOOD APPLICATION, 2018-2022 (USD MILLION)

- TABLE 179 FUNCTIONAL FOOD INGREDIENTS MARKET, BY FOOD APPLICATION, 2023-2028 (USD MILLION)

- 15.3.2 FOOD

- 15.3.2.1 Cost-effective food products with high nutritional benefits

- 15.3.2.2 Baby food

- 15.3.2.2.1 New product development with various value-added products

- 15.3.2.3 Dairy products

- 15.3.2.3.1 Rise in demand for new and improved functional dairy products

- 15.3.2.4 Bakery products

- 15.3.2.4.1 High consumption of bakery products to increase functional food ingredient use

- 15.3.2.5 Confectionery products

- 15.3.2.5.1 Increase in confectionery products offered with nutritional value

- 15.3.2.6 Snacks

- 15.3.2.6.1 Changing lifestyles of consumers

- 15.3.2.7 Meat & meat products

- 15.3.2.7.1 Enhancement of nutritional value by imparting functional food ingredients into meat products

- 15.3.2.8 Elderly nutrition & breakfast cereals

- 15.3.2.8.1 Rise in purchasing power of consumers

- 15.3.3 BEVERAGES

- 15.3.3.1 Rise in demand for health beverages

- 15.4 FUNCTIONAL FOOD INGREDIENTS MARKET, BY REGION

- 15.4.1 INCREASE IN POPULARITY OF CLEAN-LABEL AND FORTIFIED FOOD

- FIGURE 51 FUNCTIONAL FOOD INGREDIENTS MARKET: REGIONAL & COUNTRY-LEVEL GROWTH RATES, 2023-2028

- TABLE 180 FUNCTIONAL FOOD INGREDIENTS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 181 FUNCTIONAL FOOD INGREDIENTS MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 182 FUNCTIONAL FOOD INGREDIENTS MARKET, BY REGION, 2018-2022 (KT)

- TABLE 183 FUNCTIONAL FOOD INGREDIENTS MARKET, BY REGION, 2023-2028 (KT)

- 15.4.2 NORTH AMERICA

- TABLE 184 NORTH AMERICA: FUNCTIONAL FOOD INGREDIENTS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 185 NORTH AMERICA: FUNCTIONAL FOOD INGREDIENTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 15.4.3 EUROPE

- TABLE 186 EUROPE: FUNCTIONAL FOOD INGREDIENTS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 187 EUROPE: FUNCTIONAL FOOD INGREDIENTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 15.4.4 ASIA PACIFIC

- TABLE 188 ASIA PACIFIC: FUNCTIONAL FOOD INGREDIENTS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 189 ASIA PACIFIC: FUNCTIONAL FOOD INGREDIENTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 15.4.5 SOUTH AMERICA

- TABLE 190 SOUTH AMERICA: FUNCTIONAL FOOD INGREDIENTS MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 191 SOUTH AMERICA: FUNCTIONAL FOOD INGREDIENTS MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 15.4.6 ROW

- TABLE 192 ROW: FUNCTIONAL FOOD INGREDIENTS MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 193 ROW: FUNCTIONAL FOOD INGREDIENTS MARKET, BY REGION, 2023-2028 (USD MILLION)

16 SPECIALTY STARCH MARKET

- 16.1 INTRODUCTION

- 16.2 SPECIALTY STARCH MARKET, BY TYPE

- 16.2.1 VERSATILE NATURE OF STARCH TO ENABLE MODIFICATION OF VARIOUS CHEMICAL FORMS

- 16.2.2 ETHERIFIED STARCH

- 16.2.2.1 Preference for soft and creamy texture of dairy products

- TABLE 194 ETHERIFIED STARCH IN FOOD APPLICATIONS

- 16.2.3 ESTERIFIED STARCH

- 16.2.3.1 Increase in demand for frozen foods

- 16.2.4 RESISTANT STARCH

- 16.2.4.1 Nutritional benefits of resistant starch in humans

- TABLE 195 FUNCTIONS, BENEFITS, AND APPLICATIONS OF MODIFIED RESISTANT STARCH IN FOOD & BEVERAGE INDUSTRY

- 16.2.5 PREGELATINIZED

- 16.2.5.1 Pregelatinized starches to retain functional properties and viscosity of food & beverage products

- TABLE 196 FUNCTIONS OF PREGELATINIZED SPECIALTY STARCH IN FOOD & BEVERAGE APPLICATIONS

- 16.3 SPECIALTY STARCH MARKET, BY APPLICATION

- 16.3.1 INCREASE IN DEMAND FOR PLANT-BASED ALTERNATIVES FOR EMULSIFIERS AND STABILIZERS

- TABLE 197 SPECIALTY STARCHES MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 198 SPECIALTY STARCHES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 16.3.2 FOOD

- 16.3.2.1 Versatility and applications of specialty starches in food products

- TABLE 199 SPECIALTY STARCHES MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 200 SPECIALTY STARCHES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 16.3.2.2 Bakery & confectionery products

- 16.3.2.2.1 Demand for specialty starches to improve texture and quality of confectionery products

- 16.3.2.3 Processed foods

- 16.3.2.3.1 Preference for modified starch's freeze-thaw ability in processed foods

- 16.3.2.4 Meat, poultry, and seafood

- 16.3.2.4.1 Increase in use to enhance shelf life of meat products

- 16.3.2.5 Other food applications

- 16.3.2.2 Bakery & confectionery products

- 16.3.3 BEVERAGES

- 16.3.3.1 Variegated functional properties of specialty starches

- 16.4 SPECIALTY STARCH MARKET, BY REGION

- 16.4.1 RISE IN DEMAND FOR CLEAN-LABEL PRESERVATIVES AND STABILIZERS

- FIGURE 52 SPECIALTY STARCH INGREDIENTS MARKET: REGIONAL & COUNTRY-LEVEL GROWTH RATES, 2023-2028

- TABLE 201 SPECIALTY STARCHES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 202 SPECIALTY STARCHES MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 203 SPECIALTY STARCHES MARKET, BY REGION, 2018-2022 (KT)

- TABLE 204 SPECIALTY STARCHES MARKET, BY REGION, 2023-2028 (KT)

- 16.4.2 NORTH AMERICA

- TABLE 205 NORTH AMERICA: SPECIALTY STARCHES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 206 NORTH AMERICA: SPECIALTY STARCHES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 16.4.3 EUROPE

- TABLE 207 EUROPE: SPECIALTY STARCHES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 208 EUROPE: SPECIALTY STARCHES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 16.4.4 ASIA PACIFIC

- TABLE 209 ASIA PACIFIC: SPECIALTY STARCHES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 210 ASIA PACIFIC: SPECIALTY STARCHES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 16.4.5 SOUTH AMERICA

- TABLE 211 SOUTH AMERICA: SPECIALTY STARCHES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 212 SOUTH AMERICA: SPECIALTY STARCHES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 16.4.6 ROW

- TABLE 213 ROW: SPECIALTY STARCHES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 214 ROW: SPECIALTY STARCHES MARKET, BY REGION, 2023-2028 (USD MILLION)

17 SUGAR SUBSTITUTES MARKET

- 17.1 INTRODUCTION

- 17.2 SUGAR SUBSTITUTES MARKET, BY TYPE

- 17.2.1 HIGH-INTENSITY SWEETENERS (HIS) USED IN MOST COMPLEX PRODUCTS TO PRODUCE NATURAL FLAVORS

- 17.2.1.1 High-fructose syrup

- 17.2.1.1.1 Increase in demand for candies and soft drinks

- 17.2.1.2 High-intensity sweeteners

- 17.2.1.2.1 Rise in adoption of zero-calorie and sugar-free food & beverages

- 17.2.1.3 Low-intensity sweeteners

- 17.2.1.3.1 Increase in instances of metabolic diseases

- 17.2.1.1 High-fructose syrup

- TABLE 215 SUGAR SUBSTITUTES MARKET, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 216 SUGAR SUBSTITUTES MARKET, BY TYPE, 2023-2028 (USD MILLION)

- 17.2.1 HIGH-INTENSITY SWEETENERS (HIS) USED IN MOST COMPLEX PRODUCTS TO PRODUCE NATURAL FLAVORS

- 17.3 SUGAR SUBSTITUTES MARKET, BY APPLICATION

- 17.3.1 SHIFT TOWARD CONSUMPTION OF NO-SUGAR AND LOW-CALORIE FOODS

- TABLE 217 SUGAR SUBSTITUTES MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 218 SUGAR SUBSTITUTES MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 17.3.1.1 Food

- 17.3.1.1.1 Extensive use of sugar substitutes in food

- 17.3.1.2 Beverages

- 17.3.1.2.1 Growth in demand for low-calorie beverages

- 17.3.1.3 Health & wellness

- 17.3.1.3.1 Demand for natural sweeteners to make pharmaceutical products healthier

- 17.3.1.1 Food

- 17.4 SUGAR SUBSTITUTES MARKET, BY REGION

- 17.4.1 RISE IN DEMAND FOR PRODUCTS WITH LOW CALORIES

- FIGURE 53 SUGAR SUBSTITUTES MARKET: REGIONAL & COUNTRY-LEVEL GROWTH RATES, 2023-2028

- TABLE 219 SUGAR SUBSTITUTES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 220 SUGAR SUBSTITUTES MARKET, BY REGION, 2023-2028 (USD MILLION)

- TABLE 221 SUGAR SUBSTITUTES MARKET, BY REGION, 2018-2022 (KT)

- TABLE 222 SUGAR SUBSTITUTES MARKET, BY REGION, 2023-2028 (KT)

- 17.4.1.1 North America

- TABLE 223 NORTH AMERICA: SUGAR SUBSTITUTES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 224 NORTH AMERICA: SUGAR SUBSTITUTES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 17.4.1.2 Europe

- TABLE 225 EUROPE: SUGAR SUBSTITUTES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 226 EUROPE: SUGAR SUBSTITUTES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 17.4.1.3 Asia Pacific

- TABLE 227 ASIA PACIFIC: SUGAR SUBSTITUTES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 228 ASIA PACIFIC: SUGAR SUBSTITUTES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 17.4.1.4 South America

- TABLE 229 SOUTH AMERICA: SUGAR SUBSTITUTES MARKET, BY COUNTRY, 2018-2022 (USD MILLION)

- TABLE 230 SOUTH AMERICA: SUGAR SUBSTITUTES MARKET, BY COUNTRY, 2023-2028 (USD MILLION)

- 17.4.1.5 RoW

- TABLE 231 ROW: SUGAR SUBSTITUTES MARKET, BY REGION, 2018-2022 (USD MILLION)

- TABLE 232 ROW: SUGAR SUBSTITUTES MARKET, BY REGION, 2023-2028 (USD MILLION)

18 SPECIALTY FOOD INGREDIENTS MARKET, BY DISTRIBUTION CHANNEL

- 18.1 INTRODUCTION

- TABLE 233 SPECIALTY FOOD INGREDIENTS MARKET, BY DISTRIBUTION CHANNEL, 2018-2022 (USD MILLION)

- TABLE 234 SPECIALTY FOOD INGREDIENTS MARKET, BY DISTRIBUTION CHANNEL, 2023-2028 (USD MILLION)

- 18.2 DISTRIBUTORS

- 18.2.1 GROWTH IN GDP TO DRIVE DEMAND FOR DISTRIBUTION

- TABLE 235 SPECIALTY FOOD INGREDIENTS MARKET FOR DISTRIBUTORS, BY REGION, 2018-2022 (USD MILLION)

- TABLE 236 SPECIALTY FOOD INGREDIENTS MARKET FOR DISTRIBUTORS, BY REGION, 2023-2028 (USD MILLION)

- TABLE 237 SPECIALTY FOOD INGREDIENTS MARKET FOR DISTRIBUTORS, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 238 SPECIALTY FOOD INGREDIENTS MARKET FOR DISTRIBUTORS, BY TYPE, 2023-2028 (USD MILLION)

- 18.3 MANUFACTURERS

- 18.3.1 INCREASE IN RESEARCH & DEVELOPMENT ACTIVITIES

- TABLE 239 SPECIALTY FOOD INGREDIENTS MARKET FOR MANUFACTURERS, BY REGION, 2018-2022 (USD MILLION)

- TABLE 240 SPECIALTY FOOD INGREDIENTS MARKET FOR MANUFACTURERS, BY REGION, 2023-2028 (USD MILLION)

- TABLE 241 SPECIALTY FOOD INGREDIENTS MARKET FOR MANUFACTURERS, BY TYPE, 2018-2022 (USD MILLION)

- TABLE 242 SPECIALTY FOOD INGREDIENTS MARKET FOR MANUFACTURERS, BY TYPE, 2023-2028 (USD MILLION)

19 COMPETITIVE LANDSCAPE

- 19.1 OVERVIEW

- 19.2 MARKET SHARE ANALYSIS

- TABLE 243 DEGREE OF COMPETITION (CONSOLIDATED), 2022

- 19.3 SEGMENTAL REVENUE ANALYSIS OF KEY PLAYERS

- FIGURE 54 SEGMENTAL REVENUE ANALYSIS OF KEY MARKET PLAYERS, 2020-2022 (USD BILLION)

- 19.4 KEY PLAYERS' ANNUAL REVENUE VS GROWTH

- FIGURE 55 ANNUAL REVENUE, 2022 (USD BILLION) VS REVENUE GROWTH, 2020-2022

- 19.5 KEY PLAYERS' EBITDA

- FIGURE 56 EBITDA, 2022 (USD BILLION)

- 19.6 KEY PLAYER STRATEGIES

- TABLE 244 STRATEGIES ADOPTED BY KEY PLAYERS

- 19.7 GLOBAL SNAPSHOT OF KEY MARKET PARTICIPANTS

- FIGURE 57 SPECIALTY FOOD INGREDIENTS: GLOBAL SNAPSHOT OF KEY PARTICIPANTS, 2022

- 19.8 COMPANY EVALUATION QUADRANT (KEY PLAYERS)

- 19.8.1 STARS

- 19.8.2 EMERGING LEADERS

- 19.8.3 PERVASIVE PLAYERS

- 19.8.4 PARTICIPANTS

- FIGURE 58 SPECIALTY FOOD INGREDIENTS MARKET: COMPANY EVALUATION QUADRANT, 2022 (KEY PLAYERS)

- 19.9 COMPANY EVALUATION QUADRANT (STARTUPS/SMES)

- 19.9.1 PROGRESSIVE COMPANIES

- 19.9.2 STARTING BLOCKS

- 19.9.3 RESPONSIVE COMPANIES

- 19.9.4 DYNAMIC COMPANIES

- FIGURE 59 SPECIALTY FOOD INGREDIENTS MARKET: COMPANY EVALUATION QUADRANT, 2022 (STARTUPS/SMES)

- 19.9.5 COMPETITIVE BENCHMARKING OF KEY STARTUPS/SMES

- TABLE 245 SPECIALTY FOOD INGREDIENTS MARKET: DETAILED LIST OF KEY STARTUPS/SMES

- 19.10 COMPETITIVE SCENARIO

- 19.10.1 PRODUCT LAUNCHES

- TABLE 246 SPECIALTY FOOD INGREDIENTS MARKET: PRODUCT LAUNCHES, MARCH 2019-APRIL 2023

- 19.10.2 DEALS

- TABLE 247 SPECIALTY FOOD INGREDIENTS MARKET: DEALS, JANUARY 2019-JULY 2023

- 19.10.3 OTHERS

- TABLE 248 SPECIALTY FOOD INGREDIENTS MARKET: OTHERS, JUNE 2018-APRIL 2023

20 COMPANY PROFILES

- 20.1 KEY PLAYERS

- (Business overview, Products/Services/Solutions offered, Recent Developments, MNM view)**

- 20.1.1 ADM

- TABLE 249 ADM: BUSINESS OVERVIEW

- FIGURE 60 ADM: COMPANY SNAPSHOT

- TABLE 250 ADM: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 251 ADM: PRODUCT LAUNCHES

- TABLE 252 ADM: DEALS

- TABLE 253 ADM: OTHERS

- 20.1.2 DSM

- TABLE 254 DSM: BUSINESS OVERVIEW

- FIGURE 61 DSM: COMPANY SNAPSHOT

- TABLE 255 DSM: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 256 DSM: PRODUCT LAUNCHES

- TABLE 257 DSM: DEALS

- 20.1.3 INTERNATIONAL FLAVORS & FRAGRANCES INC.

- TABLE 258 INTERNATIONAL FLAVORS & FRAGRANCES INC.: BUSINESS OVERVIEW

- FIGURE 62 INTERNATIONAL FLAVORS & FRAGRANCES INC.: COMPANY SNAPSHOT

- TABLE 259 INTERNATIONAL FLAVORS & FRAGRANCES INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 260 INTERNATIONAL FLAVORS & FRAGRANCES INC.: PRODUCT LAUNCHES

- TABLE 261 INTERNATIONAL FLAVORS & FRAGRANCES INC.: DEALS

- TABLE 262 INTERNATIONAL FLAVORS & FRAGRANCES INC.: OTHERS

- 20.1.4 KERRY GROUP PLC

- TABLE 263 KERRY GROUP PLC: BUSINESS OVERVIEW

- FIGURE 63 KERRY GROUP PLC: COMPANY SNAPSHOT

- TABLE 264 KERRY GROUP PLC: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 265 KERRY GROUP PLC: PRODUCT LAUNCHES

- TABLE 266 KERRY GROUP PLC: DEALS

- TABLE 267 KERRY GROUP PLC: OTHERS

- 20.1.5 GIVAUDAN

- TABLE 268 GIVAUDAN: BUSINESS OVERVIEW

- FIGURE 64 GIVAUDAN: COMPANY SNAPSHOT

- TABLE 269 GIVAUDAN: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 270 GIVAUDAN: PRODUCT LAUNCHES

- TABLE 271 GIVAUDAN: DEALS

- TABLE 272 GIVAUDAN: OTHERS

- 20.1.6 CARGILL, INCORPORATED

- TABLE 273 CARGILL, INCORPORATED: BUSINESS OVERVIEW

- FIGURE 65 CARGILL, INCORPORATED: COMPANY SNAPSHOT

- TABLE 274 CARGILL, INCORPORATED: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 275 CARGILL, INCORPORATED: PRODUCT LAUNCHES

- TABLE 276 CARGILL, INCORPORATED: DEALS

- TABLE 277 CARGILL, INCORPORATED: OTHERS

- 20.1.7 SENSIENT TECHNOLOGIES CORPORATION

- TABLE 278 SENSIENT TECHNOLOGIES CORPORATION: BUSINESS OVERVIEW

- FIGURE 66 SENSIENT TECHNOLOGIES CORPORATION: COMPANY SNAPSHOT

- TABLE 279 SENSIENT TECHNOLOGIES CORPORATION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- 20.1.8 INGREDION

- TABLE 280 INGREDION: BUSINESS OVERVIEW

- FIGURE 67 INGREDION: COMPANY SNAPSHOT

- TABLE 281 INGREDION: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 282 INGREDION: PRODUCT LAUNCHES

- TABLE 283 INGREDION: DEALS

- TABLE 284 INGREDION: OTHERS

- 20.1.9 CHR. HANSEN HOLDING A/S

- TABLE 285 CHR. HANSEN HOLDING A/S: BUSINESS OVERVIEW

- FIGURE 68 CHR. HANSEN HOLDING A/S: COMPANY SNAPSHOT

- TABLE 286 CHR. HANSEN HOLDING A/S: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 287 CHR. HANSEN HOLDING A/S: DEALS

- TABLE 288 CHR. HANSEN HOLDING A/S: OTHERS

- 20.1.10 TATE & LYLE

- TABLE 289 TATE & LYLE: BUSINESS OVERVIEW

- FIGURE 69 TATE & LYLE: COMPANY SNAPSHOT

- TABLE 290 TATE & LYLE: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 291 TATE & LYLE: PRODUCT LAUNCHES

- TABLE 292 TATE & LYLE: DEALS

- 20.1.11 AMANO ENZYME INC.

- TABLE 293 AMANO ENZYME INC.: BUSINESS OVERVIEW

- TABLE 294 AMANO ENZYME INC.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 295 AMANO ENZYME INC.: PRODUCT LAUNCHES

- TABLE 296 AMANO ENZYME INC.: OTHERS

- 20.1.12 BIOCATALYSTS

- TABLE 297 BIOCATALYSTS: BUSINESS OVERVIEW

- TABLE 298 BIOCATALYSTS: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 299 BIOCATALYSTS: PRODUCT LAUNCHES

- TABLE 300 BIOCATALYSTS: OTHERS

- 20.1.13 ENZYME SUPPLIES

- TABLE 301 ENZYME SUPPLIES: BUSINESS OVERVIEW

- TABLE 302 ENZYME SUPPLIES: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- 20.1.14 ROQUETTE FRERES

- TABLE 303 ROQUETTE FRERES: BUSINESS OVERVIEW

- TABLE 304 ROQUETTE FRERES: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- TABLE 305 ROQUETTE FRERES: DEALS

- 20.1.15 ACE INGREDIENTS CO., LTD.

- TABLE 306 ACE INGREDIENTS CO., LTD.: BUSINESS OVERVIEW

- TABLE 307 ACE INGREDIENTS CO., LTD.: PRODUCTS/SERVICES/SOLUTIONS OFFERED

- *Details on Business overview, Products/Services/Solutions offered, Recent Developments, MNM view might not be captured in case of unlisted companies.

- 20.2 STARTUPS/SMES

- 20.2.1 AXIOM FOOD, INC.

- 20.2.2 AMCO PROTEINS

- 20.2.3 FDL LTD

- 20.2.4 CRESPEL & DEITERS GROUP

- 20.2.5 AMINOLA

21 ADJACENT & RELATED MARKETS

- 21.1 INTRODUCTION

- 21.2 LIMITATIONS

- 21.3 FOOD COLORS MARKET

- 21.3.1 MARKET DEFINITION

- 21.3.2 MARKET OVERVIEW

- TABLE 308 FOOD COLORS MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 309 FOOD COLORS MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 310 FOOD COLORS MARKET, BY TYPE, 2019-2022 (KT)

- TABLE 311 FOOD COLORS MARKET, BY TYPE, 2023-2028 (KT)

- 21.4 FOOD EMULSIFIERS MARKET

- 21.4.1 MARKET DEFINITION

- 21.4.2 MARKET OVERVIEW

- TABLE 312 FOOD EMULSIFIERS MARKET, BY APPLICATION, 2018-2022 (USD MILLION)

- TABLE 313 FOOD EMULSIFIERS MARKET, BY APPLICATION, 2023-2028 (USD MILLION)

- 21.5 FOOD PRESERVATIVES MARKET

- 21.5.1 MARKET DEFINITION

- 21.5.2 MARKET OVERVIEW

- TABLE 314 FOOD PRESERVATIVES MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 315 FOOD PRESERVATIVES MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 316 FOOD PRESERVATIVES MARKET, BY TYPE, 2019-2022 (KT)

- TABLE 317 FOOD PRESERVATIVES MARKET, BY TYPE, 2023-2028 (KT)

- 21.6 SUGAR SUBSTITUTES MARKET

- 21.6.1 MARKET DEFINITION

- 21.6.2 MARKET OVERVIEW

- TABLE 318 SUGAR SUBSTITUTES MARKET, BY TYPE, 2019-2022 (USD MILLION)

- TABLE 319 SUGAR SUBSTITUTES MARKET, BY TYPE, 2023-2028 (USD MILLION)

- TABLE 320 SUGAR SUBSTITUTES MARKET, BY TYPE, 2019-2022 (KT)

- TABLE 321 SUGAR SUBSTITUTES MARKET, BY TYPE, 2023-2028 (KT)

- 21.7 ENZYMES MARKET

- 21.7.1 MARKET DEFINITION

- 21.7.2 MARKET OVERVIEW

- TABLE 322 ENZYMES MARKET, BY TYPE, 2018-2021 (USD MILLION)

- TABLE 323 ENZYMES MARKET, BY TYPE, 2022-2027 (USD MILLION)

- 21.8 STARTER CULTURES MARKET

- 21.8.1 MARKET DEFINITION

- 21.8.2 MARKET OVERVIEW

- TABLE 324 STARTER CULTURES MARKET, BY MICROORGANISM, 2017-2021 (USD MILLION)

- TABLE 325 STARTER CULTURES MARKET, BY MICROORGANISM, 2022-2027 (USD MILLION)

- 21.9 FUNCTIONAL FOOD INGREDIENTS MARKET

- 21.9.1 MARKET DEFINITION

- 21.9.2 MARKET OVERVIEW

- TABLE 326 FUNCTIONAL FOOD INGREDIENTS MARKET, BY TYPE, 2016-2020 (USD MILLION)

- TABLE 327 FUNCTIONAL FOOD INGREDIENTS MARKET, BY TYPE, 2021-2026 (USD MILLION)

22 APPENDIX

- 22.1 DISCUSSION GUIDE

- 22.2 CUSTOMIZATION OPTIONS

- 22.3 RELATED REPORTS

- 22.4 AUTHOR DETAILS