|

|

市場調査レポート

商品コード

1336826

mRNAがんワクチンの世界市場の機会と臨床パイプラインの考察(2023年)Global mRNA Cancer Vaccines Market Opportunity & Clinical Pipeline Insight 2023 |

||||||

|

|

|||||||

|

|||||||

| mRNAがんワクチンの世界市場の機会と臨床パイプラインの考察(2023年) |

|

出版日: 2023年08月01日

発行: KuicK Research

ページ情報: 英文 100 Pages

納期: 即日から翌営業日

|

- 全表示

- 概要

- 図表

- 目次

世界のmRNAがんワクチン市場は、投資や戦略的提携の急増、がん治療における画期的な進歩への期待により、臨床的・商業的に大きな転換期を迎えています。製薬企業やバイオテクノロジー企業がmRNA技術の可能性を認識するにつれ、かつてない精度を持ったがんを標的とする革新的な治療法の開発の見通しに後押しされ、熾烈な競合が徐々に展開されつつあります。

製薬企業は、mRNAがんワクチンを実験段階から実現可能な治療選択肢へと押し上げるために多大な資源を投入しているため、研究開発投資によって市場は拡大しています。新興企業も既存の市場企業も、迅速な適応性や、特定の抗原を提示するがん細胞に対する強力な免疫反応を引き起こす可能性など、mRNAがんワクチンのさまざまな利点を追求しています。

さらに、世界の大手製薬企業とバイオテクノロジーイノベーターとの戦略的提携が、mRNAがんワクチンの商業の軌道を形成しつつあります。BioNTechとGenentech、ModernaとMerckの提携は、がんを適応症とする新規mRNAワクチンの開発を目的とした提携事業の成功例です。このような提携は、両者の専門知識を組み合わせることで、これらの新規治療法の開発、製造、流通を加速させることを目的としています。さらに、多様化するがん領域のパイプラインにmRNAワクチンが組み込まれることで、急速に進化するがん治療薬市場において、各社の競争力が高まっています。

mRNAがんワクチンの魅力により、強力な足場を築こうとする市場参入企業が相次いでいます。参入企業の増加により競合が激化し、イノベーションが促進されています。各社は独自のmRNAプラットフォームの開発に注力し、既存のがんだけでなく、より希少ながんへの応用も模索しています。例えば、BioNTechのFixVacプラットフォームは、同社のmRNAがんワクチン5種の開発に使用されています。同社にはiNeSTプラットフォームと呼ばれる別のプラットフォームもあります。どちらのプラットフォームも個別化がんワクチンの開発を可能にしています。さらに、競合によって生産プロセス、価格戦略、流通網の効率も向上しています。

しかし、mRNAがんワクチンの商業化には、慎重な検討を要する課題があります。価格戦略は、患者の利便性を確保することと、研究開発に必要な多額の投資に対する見返りを提供することの間で微妙なバランスをとらなければなりません。がん治療薬のコストにはいくつかの要因が影響します。研究開発費、製造の複雑さ、生産規模と生産、サプライチェーンのロジスティクス、知的財産、ライセンス供与などです。しかし、さまざまなmRNAがんワクチンの市場参入が増加することによる競合が、これらのワクチンを手頃な価格で販売するのに役立つことも予想されます。

さらに、mRNAがんワクチンの市場参入を成功させるためには、規制当局への対応、知的財産権の確保、潜在的な安全上の懸念への対処も重大な要素となります。最初のmRNAベースのCOVID-19ワクチンが承認されたことで、がんを含む後続のmRNA療法の規制プロセスがよりスムーズに進む道が開かれました。世界中の規制当局がmRNA技術に精通するにつれ、市場参入に必要な時間や資源が減少する可能性があり、商業化活動が促進されます。

最後に、市場は地理的な境界線にとらわれることはありません。市場拡大戦略には、多様な医療エコシステムへの参入や、地域のステークホルダーとの協働が含まれます。これらのワクチンが有効性と安全性の実証に寄与するにつれて、さまざまな市場で採用され、治療のパラダイムを変え、世界規模でがんとの闘いに貢献することが見込まれます。

市場には有望な未来がありますが、同時に対処すべきさまざまな側面もあります。mRNAがんワクチンが臨床に大きな影響を与える可能性があることは明らかですが、その商業化は、規制当局の認可、市場の受け入れ、償還政策、複雑なサプライチェーンネットワークを管理する能力などの要因に左右されます。したがって、市場は戦術的計画、共同研究、発見の寄せ集めです。世界市場で大きなシェアを獲得するためには、世界展開戦略、競合力学、価格戦略、投資動向の複雑な相互作用を理解することが重要です。

当レポートでは、世界のmRNAがんワクチン市場について調査分析し、臨床パイプライン、各企業の独自技術、提携と投資などの考察を提供しています。

目次

第1章 次世代がん免疫療法としてのmRNAワクチン

- mRNAワクチンの概要

- mRNAワクチンとその他のがん治療アプローチの比較

- mRNAワクチンとその他のワクチンの比較

第2章 世界のmRNAがんワクチン市場の概要

- 現在の市場情勢

- 将来の臨床と商品化の機会

第3章 世界のmRNAがんワクチン市場の動向:国別

- 米国

- 中国

- オーストラリア

- 欧州

- カナダ

第4章 世界のmRNAがんワクチン市場の提携、取引、投資

第5章 世界のmRNAがんワクチン市場の臨床情勢:適応症別

- 乳がん

- 脳腫瘍

- メラノーマ

- 大腸がん

- 頭頸部がん

第6章 世界のmRNAがんワクチンの臨床パイプラインの概要

- 企業別

- 国別

- 患者セグメント別

- フェーズ別

- 優先順位別

第7章 世界のmRNAがんワクチンの臨床パイプライン:企業別、適応症別、フェーズ別

- 調査

- 前臨床

- フェーズI

- フェーズI/II

- フェーズII

- フェーズII/III

- フェーズIII

第8章 RNAがんワクチンの開発に向けた独自の技術と手法

- FixVac - BioNTech

- iNeST - BioNTech

- NanoReady - Samyang Holdings

- CureVac Method - CureVac

- mRNA platform - Moderna

- NeoCura Ag - NeoCura

第9章 競合情勢

- Avstera Therapeutics

- BioNTech

- Combined Therapeutics

- CureVac

- EpiVax

- Immorna

- Immune Design

- MDimune

- Moderna Therapeutics

- NeoCura

- Orna Therapeutics

- pHion Therapeutics

- Regen BioPharma

- RNAimmune

- TransCode Therapeutics

List of Figures

- Figure 5-1: KEYNOTE-603 Phase I Study - Initiation & Completion Years

- Figure 5-2: GO39733 Phase I Study - Initiation & Completion Years

- Figure 5-3: ATTAC-II Phase II Study - Initiation & Completion Years

- Figure 5-4: CV-GBLM-001 Phase I Study - Initiation & Completion Years

- Figure 5-5: GO39733 Phase II Study - Initiation & Completion Years

- Figure 5-6: BNT111-01 Phase II Study - Initiation & Completion Years

- Figure 5-7: BNT122-01 Phase II Study - Initiation & Completion Years

- Figure 5-8: AHEAD-MERIT Phase II Study - Initiation & Completion Years

- Figure 5-9: KEYNOTE-603 Phase II Study - Initiation & Completion Years

- Figure 6-1: Global - mRNA Cancer Vaccines Clinical Pipeline by Company (Numbers), 2023

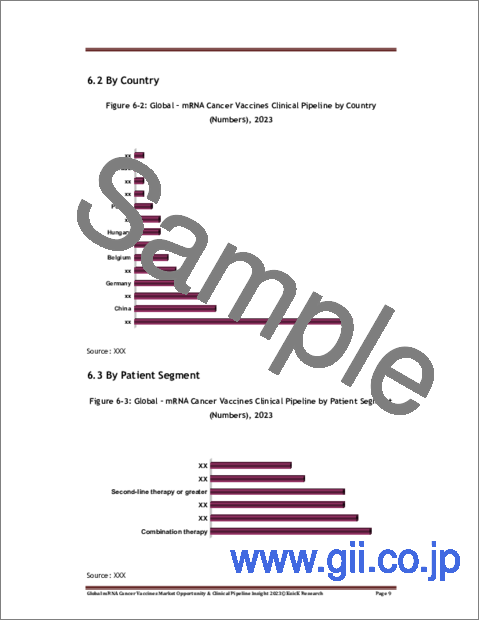

- Figure 6-2: Global - mRNA Cancer Vaccines Clinical Pipeline by Country (Numbers), 2023

- Figure 6-3: Global - mRNA Cancer Vaccines Clinical Pipeline by Patient Segment (Numbers), 2023

- Figure 6-4: Global - mRNA Cancer Vaccines Clinical Pipeline by Phase (Numbers), 2023

- Figure 6-5: Global - mRNA Cancer Vaccines Clinical Pipeline by Priority Status (Numbers), 2023

- Figure 8-1: BioNTech - uRNA products

- Figure 8-2: BioNTech - iNeST technology

- Figure 8-3: CureVac - CureVac Method for Generation of mRNA Therapeutics

- Figure 8-4: Moderna - mRNA Technology

- Figure 8-5: NeoCura - NeoCura Ag Platform

List of Tables

- Table 1-1: mRNA Vaccines v/s Other Cancer Therapeutic Approaches

- Table 1-2: mRNA-Based Cancer Vaccines vs. Other Cancer Vaccines

- Table 2-1: Recent Designations Granted to Investigational mRNA Cancer Vaccines

- Table 5-1: Breast Cancer mRNA Vaccines in Clinical Trials

- Table 5-2: Brain Cancer mRNA Vaccines in Clinical Trials

- Table 5-3: Melanoma mRNA Vaccines in Clinical Trials

- Table 5-4: Colorectal Cancer mRNA Vaccines in Clinical Trials

- Table 5-5: Head & Neck Cancer mRNA Vaccines in Clinical Trials

“Global mRNA Cancer Vaccines Market Opportunity & Clinical Pipeline Insight 2023” Report Highlights:

- mRNA Cancer Vaccines Clinical Pipeline Insight: > 40 Vaccines In Trials

- Highest Phase Of Clinical Development: Phase 3 (August 2023)

- Till Now (August 2023) No Vaccines Is Commercially Approved In Market

- mRNA Cancer Vaccines Clinical Pipeline Insight By Indication, Company, Country & Phase

- RNA Cancer Vaccines Proprietary Technologies By Companies

- Market Collaborations & Investments Insight

The clinical and commercial landscape of the global mRNA cancer vaccines market is undergoing a transformative shift marked by a surge in investment, strategic collaborations, and the anticipation of groundbreaking advancements in cancer treatment. As pharmaceutical and biotechnology companies recognize the potential of mRNA technology, a fierce competition is slowly unfolding, fuelled by the prospect of developing innovative therapies that target cancer with unprecedented precision.

Pharmaceutical companies are devoting significant resources into pushing mRNA cancer vaccines from the experimental stage to feasible therapeutic options, therefore the market is expanding as a result of research and development investments. Both start-ups and established market players are pursuing the various advantages of mRNA cancer vaccines, such as their fast adaptability and potential to trigger strong immune responses against cancer cells presenting a particular antigen.

Moreover, strategic partnerships between global pharmaceutical giants and biotechnology innovators are shaping the commercial trajectory of mRNA cancer vaccines. The collaborations between BioNTech and Genentech, and Moderna and Merck are prime examples of successful collaboration ventures aimed at the development of novel mRNA vaccines for cancer indications. Such collaborations aim to combine the expertise of both parties, accelerating the development, manufacturing and distribution of these novel therapies. Moreover, the inclusion of mRNA vaccines in diversified oncology pipelines is enhancing companies' overall competitiveness in the rapidly evolving cancer therapeutics market.

The allure of mRNA cancer vaccines has driven a wave of market entrants seeking to establish a strong foothold. The influx of players has led to heightened competition, fostering innovation. Companies are focusing on developing proprietary mRNA platforms, targeting not only established cancers but also exploring applications in rarer cancer indications. For instance, BioNTech's FixVac platform has been used to develop 5 of the company's mRNA cancer vaccines. The company has another platform, called the iNeST platform. Both platforms allow the developed of individualized cancer vaccines. In addition, the competition has also increased the efficiency in production processes, pricing strategies and distribution networks.

However, commercialization of mRNA cancer vaccines presents challenges that necessitate careful consideration. Pricing strategies must strike a delicate balance between ensuring patient accessibility and providing a return on the substantial investments required for research and development. Several factors influence the cost of a cancer therapeutic. These include research and development costs, manufacturing complexities, production scale and volume, supply chain logistics, intellectual property and licensing. However, it is also expected the competition resulting from increasing market entry of different mRNA cancer vaccines will help these vaccines be sold at affordable prices.

In addition, navigating regulatory pathways, securing intellectual property rights and addressing potential safety concerns are also critical components in successfully bringing mRNA cancer vaccines to the market. The approval of the first mRNA-based COVID-19 vaccines has paved the way for a smoother regulatory process for subsequent mRNA therapies, including those for cancer. As regulatory agencies around the world become more familiar with mRNA technology, the time and resources required for market entry may potentially decrease, expediting commercialization efforts.

Lastly, the global mRNA cancer vaccines market is not confined by geographical boundaries. Market expansion strategies involve penetrating diverse healthcare ecosystems and collaborating with regional stakeholders. As these vaccines contribute to demonstrate their efficacy and safety, their adoption across different markets holds the promise of changing treatment paradigms and contributing to the fight against cancer on a global scale.

The global market for mRNA cancer vaccines has a promising future but it also has different aspects that need to be addressed. Even while the potential for a substantial clinical impact of mRNA cancer vaccines is obvious, their commercialization will be dependent on factors such as regulatory clearance, market acceptance, reimbursement policies, and the ability to manage complex supply chain networks. Therefore, the global market for mRNA cancer vaccines is a mosaic of tactical planning, collaborations, and discoveries. Understanding the complex interactions between global expansion strategies, competitive dynamics, pricing strategies and investment trends in critical to be able to grab a sizeable market share in the global market.

Table of Contents

1. mRNA Vaccines as Next Generation Cancer Immunotherapy

- 1.1 mRNA Vaccines Overview

- 1.2 mRNA Vaccines v/s Other Cancer Therapeutic Approaches

- 1.3 mRNA Vaccines v/s Other Vaccines

2. Global mRNA Cancer Vaccines Market Overview

- 2.1 Current Market Landscape

- 2.2 Future Clinical & Commercialization Opportunities

3. Global mRNA Cancer Vaccines Market Trends by Country

- 3.1 US

- 3.2 China

- 3.3 Australia

- 3.4 Europe

- 3.5 Canada

4. Global mRNA Cancer Vaccines Market Collaborations, Deals & Investments

5. Global mRNA Cancer Vaccines Market Clinical Landscape by Indication

- 5.1 Breast Cancer

- 5.2 Brain Cancer

- 5.3 Melanoma

- 5.4 Colorectal Cancer

- 5.5 Head & Neck Cancers

6. Global mRNA Cancer Vaccines Clinical Pipeline Overview

- 6.1 By Company

- 6.2 By Country

- 6.3 By Patient Segment

- 6.4 By Phase

- 6.5 By Priority Status

7. Global mRNA Cancer Vaccines Clinical Pipeline By Company, Indication & Phase

- 7.1 Research

- 7.2 Preclinical

- 7.3 Phase-I

- 7.4 Phase-I/II

- 7.5 Phase-II

- 7.6 Phase-II/III

- 7.7 Phase-III

8. Proprietary Technologies & Methodologies for RNA Cancer Vaccines Development

- 8.1 FixVac - BioNTech

- 8.2 iNeST - BioNTech

- 8.3 NanoReady - Samyang Holdings

- 8.4 CureVac Method - CureVac

- 8.5 mRNA platform - Moderna

- 8.6 NeoCura Ag - NeoCura

9. Competitive Landscape

- 9.1 Avstera Therapeutics

- 9.2 BioNTech

- 9.3 Combined Therapeutics

- 9.4 CureVac

- 9.5 EpiVax

- 9.6 Immorna

- 9.7 Immune Design

- 9.8 MDimune

- 9.9 Moderna Therapeutics

- 9.10 NeoCura

- 9.11 Orna Therapeutics

- 9.12 pHion Therapeutics

- 9.13 Regen BioPharma

- 9.14 RNAimmune

- 9.15 TransCode Therapeutics