|

|

市場調査レポート

商品コード

1456955

ギアポンプ市場-2024年から2029年までの予測Gear Pumps Market - Forecasts from 2024 to 2029 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| ギアポンプ市場-2024年から2029年までの予測 |

|

出版日: 2024年02月08日

発行: Knowledge Sourcing Intelligence

ページ情報: 英文 132 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

ギアポンプ市場はCAGR 4.88%で成長し、2022年の市場規模11億1,877万1,000米ドルから2029年には15億6,129万米ドルに達すると予測されています。

ギアポンプは、歯車の噛み合いを利用して流体を圧送する容積式ポンプの一種であり、ケーシング内で噛み合って回転する2つ以上の歯車で構成されています。ギアポンプは、そのシンプルさ、信頼性、効率性で知られており、ギアが回転することにより、流体はポンプの吸込口に吸い込まれ、吐出口から押し出されます。ギアポンプは、石油・ガス、自動車、パルプ・製紙、飲食品などの産業・商業用途で一般的に使用されています。世界のギアポンプ市場は、様々な最終用途産業からのギアポンプに対する需要の増加と、ポンプ設計における継続的な技術進歩によって牽引されると予想されます。

高効率

産業界がより高い生産性と費用対効果を目指す中、効果的なポンプソリューションの必要性が高まっています。ギアポンプは、その使いやすさ、信頼性、スムーズな操作性により、多くの用途で標準的な選択肢となっています。ギアポンプポンプは、幅広い粘度範囲に対応し、安定した流量を供給できるため、様々な工業プロセスに適応できます。

これらのポンプは、エネルギー損失を低減し、安定した信頼性の高い流体の流れを提供することにより、システム全体の効率を向上させます。ギアポンプは、製造、石油化学、自動車、化学処理などの業界で、潤滑や流体移送の手順を改善するために頻繁に使用されています。また、ギアポンプは、小型でメンテナンスが簡単なため、スペースが重要視される用途にも適しています。

石油・ガス産業における需要の増加

石油・ガス業界の成長により、ギアポンプの需要が急増しています。これらの産業が世界的に急速に拡大するにつれ、信頼性が高く効果的な流体移送メカニズムへのニーズが高まり、ギアポンプの需要が大幅に増加しています。ギアポンプは、石油・ガス産業において、燃料移送、油圧システム、潤滑など、様々な用途で必要不可欠な製品であり、採掘、抽出、精製段階における機器の効率的な稼働を保証します。

ギアポンプは、化学産業が化学薬品を正確に取り扱い、移送するために不可欠であり、生産プロセスの生産性と安全性を向上させます。人口の増加や工業化により、世界中でエネルギーや化学薬品に対するニーズが高まっていることから、ギアポンプはこれらの重要な産業において流体移送を可能にする重要な役割を担っています。石油・ガスと化学産業が成長と変化を続ける中、ギアポンプ市場のメーカーは、独創的で信頼性の高いソリューションを提供することで、この需要の高まりから利益を得ることができます。

石油化学産業における高い需要

ギアポンプは、石油化学産業に不可欠な要素です。ピッチ、ビチューメン、潤滑油、ディーゼル油、原油などは、石油化学産業が生産する製品のひとつです。珪酸ソーダ、混合化学品、酸、ポリマー、イソシアネートなどの危険物も輸送されています。この市場のメーカーを世界の生産能力の拡大に駆り立てている主要理由のひとつは、自動車、包装、家庭用品、医療機器など、さまざまな用途で石油化学製品に対する需要が高まっていることです。例えば、Bharat Petroleum Corporation Limited(BPCL)は、急速に変化する業界において競合を維持し、将来に備えるため、2022年5月から今後5年間で石油化学プロジェクトに3,000億インドルピーを投資する予定です。

技術の進歩

技術の飛躍的進歩と環境への配慮により、ギヤ油圧ポンプ市場はより持続可能で効率的な市場へと大きくシフトしています。設計と材料科学の進歩が市場を変革し、コンパクトで環境への影響が少ない、信頼性の高い大容量ポンプへの動きを促進しています。操作機能を再定義するIoT統合とスマートポンプソリューションを重視する動きが強まっていることも、市場成長にとって注目すべき動向です。

インテリジェントポンプの採用

歯車油圧ポンプへのインテリジェント技術の統合も重要な市場動向です。これらの独創的なポンプは、リアルタイムの運転監視と制御を可能にする組み込みコントローラとセンサーを備えています。これにより、予知保全、システム効率の向上、性能の最適化が可能になります。インテリジェントポンプの使用は、製造、自動車、航空宇宙など、正確性と信頼性が重要な産業でより普及しています。

アジア太平洋が予測期間中に急成長

中国、インド、日本などの工業化が、りわけ化学薬品と原油の需要を押し上げています。中国の石油消費量は、自動車保有台数の拡大により大幅に増加しています。さらに中国天然資源省は、石油・ガス産業への外国直接投資の開放を発表しました。その目的は、国際企業に国内での石油・ガスの探査と採掘を許可することです。アジア太平洋の建設業界は、急激な勢いで拡大しています。中国は、主に住宅と商業の両方の建築業界における複数の進歩によって推進されており、経済の拡大に後押しされています。

主要市場参入

- 2022年10月、Hydrecoはアルミニウム製の破砕・篩い分けプラントモーターとギアポンプの初期製品ラインを発表しました。英国ドーセットに本社を置く同社は、HYラインの立ち上げに伴い、初のアルミニウム製ポンプを生産します。アルミ製ポンプのみ、2021年に開所予定のハイドレコの新設施設(イタリア・パルマ)で生産されます。グループ1と2のポンプは現在、鋳鉄製とアルミニウム製のボディを持つバージョンが提供されており、鋳鉄製ボディのグループ3ポンプは、最新のグループ3アルミニウムバージョンの直後にリリースされる予定です。鋳鉄ポンプは現在英国で製造されているが、Hydreco Hydraulics Italiaの社長であるMichele Guiati氏によると、長期的な目標はすべての鋳鉄ポンプの生産をパルマの工場に移すことです。

- 2022年6月、高性能ギアポンプとモーターの製造・製造・販売の大手企業であるMarzocchi Pompe S.p.A.は、ヘリカルロータポンプの新ライン「FTP-Fluid Transmission Pump」の導入に必要な研究開発段階を終了したと発表しました。新しいFTPシリーズは、主に低粘度流体の使用を必要とする低圧用途向けです。工作機械の潤滑回路、冷却システム、リフトシステム、風力タービンのブレード速度制御システムなどがその例です。これらは、現在の枠組みに比べ、同社にとって新たな対象市場となります。

目次

第1章 イントロダクション

- 市場概要

- 市場の定義

- 調査範囲

- 市場セグメンテーション

- 通貨

- 前提条件

- 基準年と予測年のタイムライン

- 関係者にとっての主要メリット

第2章 調査手法

- 調査デザイン

- 調査プロセス

第3章 エグゼクティブサマリー

- 主要調査結果

- アナリストビュー

第4章 市場力学

- 市場促進要因

- 市場抑制要因

- ポーターのファイブフォース分析

- 業界バリューチェーン分析

- アナリストビュー

第5章 ギアポンプ市場:タイプ別

- イントロダクション

- 内接歯車ポンプ

- 市場動向と機会

- 成長の展望

- 地理的収益性

- 外接歯車ポンプ

- 市場動向と機会

- 成長の展望

- 地理的収益性

第6章 ギアポンプ市場:用途別

- イントロダクション

- オイルと燃料

- 市場動向と機会

- 成長の展望

- 地理的収益性

- 絵の具とインク

- 市場動向と機会

- 成長の展望

- 地理的収益

- 化学薬品

- 市場動向と機会

- 成長の展望

- 地理的収益性

- 溶剤・接着剤

- 市場動向と機会

- 成長の展望

- 地理的収益性

- その他

- 市場動向と機会

- 成長の展望

- 地理的収益性

第7章 ギアポンプ市場:地域別

- イントロダクション

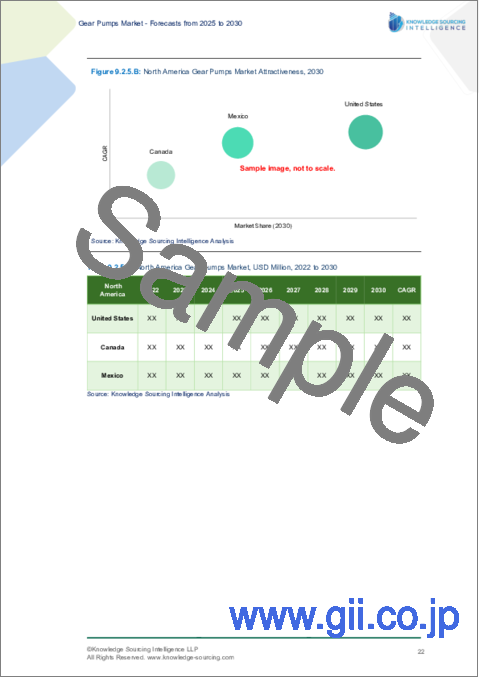

- 北米

- タイプ別

- 用途別

- 国別

- 南米

- タイプ別

- 用途別

- 国別

- 欧州

- タイプ別

- 用途別

- 国別

- 中東・アフリカ

- タイプ別

- 用途別

- 国別

- アジア太平洋

- タイプ別

- 用途別

- 国別

第8章 競合環境と分析

- 主要企業と戦略分析

- 市場シェア分析

- 合併、買収、合意とコラボレーション

- 競合ダッシュボード

第9章 企業プロファイル

- Del Pd Pumps & Gears Pvt.

- Gear Pump Manufacturing LLC

- Atlas Copco(KRACHT GmbH)

- Dover Corporation(MAAG Group)

- McNally Industries(Northern Pump)

- Rickmeier GmbH

- Teral Inc.

- Ingersoll Rand Inc(Tuthill Pumps)

- Verder Group

- Viking Pump(IDEX Corporation)

The gear pumps market is expected to grow at a CAGR of 4.88% reaching a market size of US$1,561.29 million in 2029 from US$1,118.771 million in 2022.

Gear pumps are a type of positive displacement pump that uses the meshing of gears to pump fluids and consist of two or more gears that mesh together and rotate within a casing. Gear pumps are known for their simplicity, reliability, and efficiency, and as gears rotate, fluid is drawn into the pump's inlet and forced out of the discharge port. Gear pumps are commonly used in industrial and commercial applications like oil & gas, automotive, pulp & paper, and food & beverage. The global gear pump market is expected to be driven by the increasing demand for gear pumps from various end-use industries and the ongoing technological advancements in pump design.

High efficiency

The need for effective pumping solutions has grown as industries aim for higher productivity and cost-effectiveness. Gear pumps have become the standard option for many applications due to their ease of use, dependability, and smooth operation. They are adaptable to a variety of industrial processes due to their capacity to manage a broad range of viscosities and provide steady flow rates.

These pumps increase the overall efficiency of the system by reducing energy losses and providing a steady and dependable fluid flow. Gear pumps are being used more often in industries like manufacturing, petrochemical, automotive, and chemical processing to improve their lubrication and fluid transfer procedures. In addition, gear pumps are appealing for applications where space is a crucial consideration due to their small size and simplicity of maintenance.

Increasing demand in the oil & gas industry

The growing oil and gas sectors are driving a surge in demand for gear pumps in the market. The need for dependable and effective fluid transfer mechanisms has increased as these industries see rapid global expansion, which has greatly increased demand for gear pumps. Gear pumps are essential to the oil and gas sector for several uses, including fuel transfer, hydraulic systems, and lubrication, which guarantees the efficient running of equipment during the extraction, extraction, and refining phases.

Gear pumps are essential to the chemical industry's ability to handle and transfer chemicals precisely, which improves the productivity and security of production processes. The growing need for energy and chemicals worldwide due to population expansion and industrialization highlights the vital role gear pumps play in enabling fluid transfer in these vital industries. As the oil and gas and chemical industries continue to grow and change, manufacturers in the gear pump market are well-positioned to benefit from this growing demand by offering creative and dependable solutions.

High demand in the petrochemical industry

Gear pumps are vital parts of the petrochemical industry. Pitch, bitumen, lubricating oil, diesel oil, and crude oil are among the products they produce. Hazardous materials including sodium silicate, mixed chemicals, acids, polymers, isocyanates, and others are also transported by them. One of the main reasons driving the manufacturers in this market to expand their global production capacity is the growing demand for petrochemicals in a variety of applications, including automotive, packaging, home goods, and medical equipment. For instance, to stay competitive in the rapidly changing industry and be prepared for the future, Bharat Petroleum Corporation Limited (BPCL) is planning to invest a substantial INR 30,000 crores in petrochemical projects over the next five years, starting in May 2022.

Technological advancements

Technology breakthroughs and environmental concerns have caused a major shift in the gear hydraulic pump market toward greater sustainability and efficiency. Advancements in design and materials science are transforming the market and fostering a movement toward reliable, high-capacity pumps that are compact and have less of an impact on the environment. The growing emphasis on IoT integration and smart pump solutions, which are poised to redefine operational functionalities, is another noteworthy trend for the market's growth.

Adoption of intelligent pumps

The integration of intelligent technologies into gear hydraulic pumps is another significant market trend. These ingenious pumps are equipped with embedded controllers and sensors that enable real-time operation monitoring and control. This allows for predictive maintenance, increased system efficiency, and optimized performance. The use of intelligent pumps is more prevalent in industries where accuracy and dependability are crucial, such as manufacturing, automotive, and aerospace.

Asia Pacific is witnessing exponential growth during the forecast period

The industrialization of nations like China, India, and Japan is driving up demand for chemicals and crude oil, among other things. China's oil consumption has increased significantly as a result of the nation's expanding automobile fleet. Furthermore, China's Ministry of Natural Resources announced the opening of foreign direct investments in the oil and gas industry to meet the country's demand for these resources and increase domestic energy supplies. Its goal is to give international businesses permission to search for and extract gas and oil in the nation. Asia Pacific's construction industry is expanding at an exponential rate. China has been primarily propelled by multiple advancements in the building industry, both residential and commercial, bolstered by the expanding economy.

Market key launches

- In October 2022, Hydreco introduced its initial line of crushing and screening plant motors and gear pumps made of aluminium. The company based in Dorset, UK, is producing its first aluminium pumps with the launch of the HY line. Only the aluminium pumps will be produced at Hydreco's newly constructed Parma, Italy facility, which is scheduled to open in 2021. Groups 1 and 2 pumps are currently offered in versions with cast iron and aluminium bodies, and a group 3 pump with a cast iron body will be released shortly after the most recent group 3 aluminium version. Although the cast iron pumps are currently manufactured in the UK, the long-term goal is to move all cast iron pump production to the Parma facility, according to Michele Guiati, managing director of Hydreco Hydraulics Italia.

- In June 2022, the leading manufacturer, manufacturer, and marketer of high-performance gear pumps and motors, Marzocchi Pompe S.p.A., said it finished the R&D stages needed to introduce the new "FTP - Fluid Transmission Pump" line of helical rotor pumps. The new FTP family is primarily intended for low-pressure applications, which also call for the use of low-viscosity fluids. A few instances are machine tool lubrication circuits, cooling systems, lift systems, and wind turbine blade speed control systems. These are new target markets for the company in comparison to the current framework.

Segmentation:

By Type

- Internal Gear Pump

- External Gear Pump

By Application

- Oil & Fuel

- Paints & Ink

- Chemical

- Solvents & Adhesives

- Others

By Geography

- North America

- USA

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Others

- Europe

- UK

- Germany

- France

- Spain

- Others

- Middle East and Africa

- Saudi Arabia

- UAE

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Other

TABLE OF CONTENTS

1. INTRODUCTION

- 1.1. Market Overview

- 1.2. Market Definition

- 1.3. Scope of the Study

- 1.4. Market Segmentation

- 1.5. Currency

- 1.6. Assumptions

- 1.7. Base, and Forecast Years Timeline

- 1.8. Key Benefits to the Stakeholder

2. RESEARCH METHODOLOGY

- 2.1. Research Design

- 2.2. Research Processes

3. EXECUTIVE SUMMARY

- 3.1. Key Findings

- 3.2. Analyst View

4. MARKET DYNAMICS

- 4.1. Market Drivers

- 4.2. Market Restraints

- 4.3. Porter's Five Forces Analysis

- 4.3.1. Bargaining Power of Suppliers

- 4.3.2. Bargaining Power of Buyers

- 4.3.3. Threat of New Entrants

- 4.3.4. Threat of Substitutes

- 4.3.5. Competitive Rivalry in the Industry

- 4.4. Industry Value Chain Analysis

- 4.5. Analyst View

5. GEAR PUMPS MARKET, BY TYPE

- 5.1. Introduction

- 5.2. Internal Gear Pump

- 5.2.1. Market Trends and Opportunities

- 5.2.2. Growth Prospects

- 5.2.3. Geographic Lucrativeness

- 5.3. External Gear Pump

- 5.3.1. Market Trends and Opportunities

- 5.3.2. Growth Prospects

- 5.3.3. Geographic Lucrativeness

6. GEAR PUMPS MARKET, BY APPLICATION

- 6.1. Introduction

- 6.2. Oil & Fuel

- 6.2.1. Market Trends and Opportunities

- 6.2.2. Growth Prospects

- 6.2.3. Geographic Lucrativeness

- 6.3. Paints & Ink

- 6.3.1. Market Trends and Opportunities

- 6.3.2. Growth Prospects

- 6.3.3. Geographic Lucrativeness

- 6.4. Chemical

- 6.4.1. Market Trends and Opportunities

- 6.4.2. Growth Prospects

- 6.4.3. Geographic Lucrativeness

- 6.5. Solvents & Adhesives

- 6.5.1. Market Trends and Opportunities

- 6.5.2. Growth Prospects

- 6.5.3. Geographic Lucrativeness

- 6.6. Others

- 6.6.1. Market Trends and Opportunities

- 6.6.2. Growth Prospects

- 6.6.3. Geographic Lucrativeness

7. GEAR PUMPS MARKET, BY GEOGRAPHY

- 7.1. Introduction

- 7.2. North America

- 7.2.1. By Type

- 7.2.2. By Application

- 7.2.3. By Country

- 7.2.3.1. USA

- 7.2.3.1.1. Market Trends and Opportunities

- 7.2.3.1.2. Growth Prospects

- 7.2.3.2. Canada

- 7.2.3.2.1. Market Trends and Opportunities

- 7.2.3.2.2. Growth Prospects

- 7.2.3.3. Mexico

- 7.2.3.3.1. Market Trends and Opportunities

- 7.2.3.3.2. Growth Prospects

- 7.2.3.1. USA

- 7.3. South America

- 7.3.1. By Type

- 7.3.2. By Application

- 7.3.3. By Country

- 7.3.3.1. Brazil

- 7.3.3.1.1. Market Trends and Opportunities

- 7.3.3.1.2. Growth Prospects

- 7.3.3.2. Argentina

- 7.3.3.2.1. Market Trends and Opportunities

- 7.3.3.2.2. Growth Prospects

- 7.3.3.3. Others

- 7.3.3.3.1. Market Trends and Opportunities

- 7.3.3.3.2. Growth Prospects

- 7.3.3.1. Brazil

- 7.4. Europe

- 7.4.1. By Type

- 7.4.2. By Application

- 7.4.3. By Country

- 7.4.3.1. UK

- 7.4.3.1.1. Market Trends and Opportunities

- 7.4.3.1.2. Growth Prospects

- 7.4.3.2. Germany

- 7.4.3.2.1. Market Trends and Opportunities

- 7.4.3.2.2. Growth Prospects

- 7.4.3.3. France

- 7.4.3.3.1. Market Trends and Opportunities

- 7.4.3.3.2. Growth Prospects

- 7.4.3.4. Spain

- 7.4.3.4.1. Market Trends and Opportunities

- 7.4.3.4.2. Growth Prospects

- 7.4.3.5. Others

- 7.4.3.5.1. Market Trends and Opportunities

- 7.4.3.5.2. Growth Prospects

- 7.4.3.1. UK

- 7.5. Middle East and Africa

- 7.5.1. By Type

- 7.5.2. By Application

- 7.5.3. By Country

- 7.5.3.1. Saudi Arabia

- 7.5.3.1.1. Market Trends and Opportunities

- 7.5.3.1.2. Growth Prospects

- 7.5.3.2. UAE

- 7.5.3.2.1. Market Trends and Opportunities

- 7.5.3.2.2. Growth Prospects

- 7.5.3.3. Others

- 7.5.3.3.1. Market Trends and Opportunities

- 7.5.3.3.2. Growth Prospects

- 7.5.3.1. Saudi Arabia

- 7.6. Asia Pacific

- 7.6.1. By Type

- 7.6.2. By Application

- 7.6.3. By Country

- 7.6.3.1. China

- 7.6.3.1.1. Market Trends and Opportunities

- 7.6.3.1.2. Growth Prospects

- 7.6.3.2. Japan

- 7.6.3.2.1. Market Trends and Opportunities

- 7.6.3.2.2. Growth Prospects

- 7.6.3.3. South Korea

- 7.6.3.3.1. Market Trends and Opportunities

- 7.6.3.3.2. Growth Prospects

- 7.6.3.4. Australia

- 7.6.3.4.1. Market Trends and Opportunities

- 7.6.3.4.2. Growth Prospects

- 7.6.3.5. Others

- 7.6.3.5.1. Market Trends and Opportunities

- 7.6.3.5.2. Growth Prospects

- 7.6.3.1. China

8. COMPETITIVE ENVIRONMENT AND ANALYSIS

- 8.1. Major Players and Strategy Analysis

- 8.2. Market Share Analysis

- 8.3. Mergers, Acquisitions, Agreements, and Collaborations

- 8.4. Competitive Dashboard

9. COMPANY PROFILES

- 9.1. Del Pd Pumps & Gears Pvt.

- 9.2. Gear Pump Manufacturing LLC

- 9.3. Atlas Copco (KRACHT GmbH)

- 9.4. Dover Corporation (MAAG Group)

- 9.5. McNally Industries (Northern Pump)

- 9.6. Rickmeier GmbH

- 9.7. Teral Inc.

- 9.8. Ingersoll Rand Inc (Tuthill Pumps)

- 9.9. Verder Group

- 9.10. Viking Pump (IDEX Corporation)