|

|

市場調査レポート

商品コード

1571635

注射ドラッグデリバリーデバイスの市場規模、シェア、動向分析レポート:製品別、治療用途別、最終用途別、地域別、セグメント別予測、2024年~2030年Injectable Drug Delivery Devices Market Size, Share & Trends Analysis Report By Product, By Therapeutic Use, By End-use, By Region, And Segment Forecasts, 2024 - 2030 |

||||||

|

|||||||

カスタマイズ可能

|

|||||||

| 注射ドラッグデリバリーデバイスの市場規模、シェア、動向分析レポート:製品別、治療用途別、最終用途別、地域別、セグメント別予測、2024年~2030年 |

|

出版日: 2024年09月17日

発行: Grand View Research

ページ情報: 英文 100 Pages

納期: 2~10営業日

|

全表示

- 概要

- 目次

注射ドラッグデリバリーデバイス市場の成長と動向:

Grand View Research, Inc.の最新レポートによると、世界の注射ドラッグデリバリーデバイス市場規模は2030年までに8,232億9,000万米ドルに達すると予測されています。

同市場は2024年から2030年にかけてCAGR 8.7%で成長すると予測されています。糖尿病やがんなどの慢性疾患の増加により、注射によるドラッグデリバリーの必要性が高まっています。他の伝統的なドラッグデリバリー形態とは異なり、注射剤は初回通過代謝をバイパスするため、医薬品のバイオアベイラビリティを最大限に高めることができます。技術の進歩に伴い、製造・販売されているデバイスは、患者の特定のニーズに応えるように作られています。

自己注射装置の出現により、医療補助を必要とせずに注射薬を自己投与できるようになった。生物製剤市場では、多くの技術指向の開拓が行われ、課題となっている疾患領域におけるこれらの注射器具の適用性をさらに高めています。自己注射器によって、糖尿病患者は自動注射器、ペン型注射器、針を使わない注射器を使ってインスリン濃度を管理できるようになった。

この市場の主な抑制要因は、注射針による怪我や感染症、規制償還に関する曖昧さ、注射薬の無菌性、毒性が低く投与が容易な他のドラッグデリバリーシステムが好まれることです。このような市場抑制要因があるにもかかわらず、主要プレイヤーの大半が他のデリバリー形態よりも注射剤を選択しており、注射剤デリバリー製品の市場ポテンシャルは非常に大きいです。注射ドラッグデリバリー業界は、製品タイプによって自己注射デバイスと従来型注射デバイスの2つのサブタイプに区分されます。さらに、治療用途に基づき、注射剤デリバリー業界は自己免疫疾患、ホルモン疾患、腫瘍学、その他に区分されます。

エンドユーザー用途別では、注射ドラッグデリバリー産業は、病院、在宅介護環境、研究施設、診断、臨床研究所を含むその他に分類されます。

注射ドラッグデリバリーデバイス市場レポートハイライト:

- 予測期間中、腫瘍学分野のCAGRは9.3%と最速と予測されます。これは、世界のがん罹患率の増加と標的療法の進化によるものです。

- 2023年の市場シェアは53.2%で病院が圧倒的。病院では、迅速な治療効果を提供できることから、先進的な注射デバイスの採用が増加しており、これは救急医療や危機的状況において極めて重要です。

- 北米のドラッグデリバリーデバイス市場は、2023年に40.5%のシェアを占めました。北米は、糖尿病、がん、自己免疫疾患などの慢性疾患を持つ人口が多いです。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 注射ドラッグデリバリーデバイス市場の変数、動向、範囲

- 市場イントロダクション/系統展望

- 市場規模と成長見通し

- 市場力学

- 市場促進要因分析

- 市場抑制要因分析

- 注射ドラッグデリバリーデバイス市場分析ツール

- ポーターの分析

- PESTEL分析

第4章 注射ドラッグデリバリーデバイス市場:製品の推定・動向分析

- セグメントダッシュボード

- 注射ドラッグデリバリーデバイス市場:製品変動分析、2023年および2030年

- デバイス

- 製剤

第5章 注射ドラッグデリバリーデバイス市場:治療用途の推定・動向分析

- セグメントダッシュボード

- 注射ドラッグデリバリーデバイス市場:治療用途変動分析、2023年および2030年

- 自己免疫疾患

- ホルモン障害

- 腫瘍学

- その他

第6章 注射ドラッグデリバリーデバイス市場:最終用途の推定・動向分析

- セグメントダッシュボード

- 注射ドラッグデリバリーデバイス市場:最終用途変動分析、2023年および2030年

- 病院

- 在宅ケア環境

- その他

第7章 注射ドラッグデリバリーデバイス市場:地域の推定・動向分析

- 注射ドラッグデリバリーデバイスの市場シェア、地域別、2023年および2030年

- 北米

- 米国

- カナダ

- メキシコ

- 欧州

- 英国

- ドイツ

- フランス

- イタリア

- スペイン

- デンマーク

- スウェーデン

- ノルウェー

- アジア太平洋

- 中国

- 日本

- インド

- 韓国

- オーストラリア

- タイ

- ラテンアメリカ

- ブラジル

- アルゼンチン

- 中東およびアフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

- クウェート

第8章 競合情勢

- 主要市場参入企業による最近の動向と影響分析

- 企業分類

- 企業ヒートマップ分析

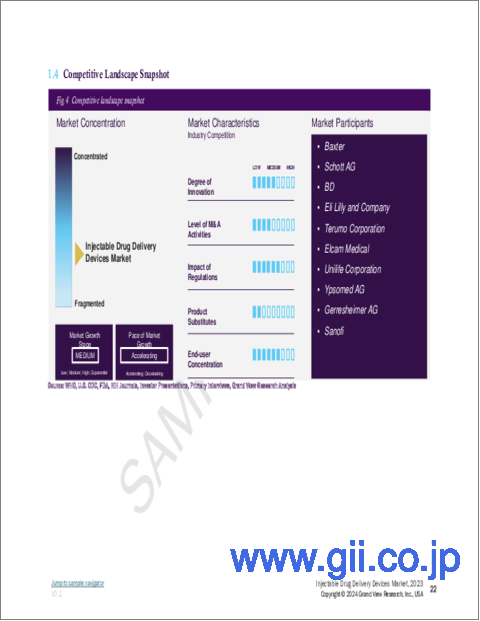

- 企業プロファイル

- Baxter

- Schott AG

- BD

- Eli Lilly and Company

- Terumo Corporation

- Elcam Medical

- Unilife Corporation

- Ypsomed AG

- Gerresheimer AG

- Sanofi

Injectable Drug Delivery Devices Market Growth & Trends:

The global injectable drug delivery devices market size is anticipated to reach USD 823.29 billion by 2030, according to a new report by Grand View Research, Inc. The market is projected to grow at a CAGR of 8.7% from 2024 to 2030. The increase in the number of chronic diseases like diabetes and cancer has fueled the need for injectable drug delivery. Unlike other traditional forms of drug delivery, injectables allow maximum bioavailability of the pharmaceutical drug as it bypasses the first-pass metabolism. With substantial growth in technological advancements, the devices being manufactured and marketed are built so as to cater to the specific needs of the patients.

With the advent of self-injection devices, injectable drugs can be self-administered without the need for medical assistance. A large number of technology-oriented developments have taken place in the biologics market, which further increases the applicability of these injectable devices in the challenging disease areas. Self-injection devices have allowed patients suffering from diabetes to manage insulin levels with auto-injectors, pen-injectors, and needle-free injectors; thus, the homecare segment has been a large grosser in the end-user application.

The major restraints in this market are injuries and infections caused by needles, ambiguities related to regulatory reimbursements, sterility of the injectable drugs, and the preference of other drug delivery systems that possess less toxicity and are easy to administer. Despite these restraints, the market potential for injectable drug delivery products is tremendous with the majority of the key players opting to injectables over other forms of delivery. The injectable drug delivery industry, based on product type is segmented into two sub-types namely self-injection devices and conventional injection devices. Further, on the basis of therapeutic use, the injectable drug delivery industry is segmented into autoimmune disorders, hormonal disorders, oncology, and others.

The injectable drug delivery industry by end-user application is categorized into hospitals, home care settings, and others including research establishments, diagnostics, and clinical laboratories.

Injectable Drug Delivery Devices Market Report Highlights:

- Oncology is anticipated to witness the fastest CAGR of 9.3% over the forecast period. This is due to the growing incidence of cancer globally and the evolution of targeted therapies.

- Hospitals dominated the market with 53.2% share in 2023. Hospitals are increasingly adopting advanced injectable devices due to their ability to provide rapid therapeutic effects, which is crucial in emergency care and critical situations.

- North America injectable drug delivery devices market dominated with 40.5% market share in 2023. North America has a significant population with chronic diseases such as diabetes, cancer, and autoimmune disorders.

Table of Contents

Chapter 1. Methodology and Scope

- 1.1. Market Segmentation and Scope

- 1.2. Market Definitions

- 1.3. Research Methodology

- 1.3.1. Information Procurement

- 1.3.2. Information or Data Analysis

- 1.3.3. Market Formulation & Data Visualization

- 1.3.4. Data Validation & Publishing

- 1.4. Research Scope and Assumptions

- 1.4.1. List of Data Sources

Chapter 2. Executive Summary

- 2.1. Market Outlook

- 2.2. Segment Outlook

- 2.3. Competitive Insights

Chapter 3. Injectable Drug Delivery Devices Market Variables, Trends, & Scope

- 3.1. Market Introduction/Lineage Outlook

- 3.2. Market Size and Growth Prospects (USD Million)

- 3.3. Market Dynamics

- 3.3.1. Market Drivers Analysis

- 3.3.2. Market Restraints Analysis

- 3.4. Injectable Drug Delivery Devices Market Analysis Tools

- 3.4.1. Porter's Analysis

- 3.4.1.1. Bargaining power of the suppliers

- 3.4.1.2. Bargaining power of the buyers

- 3.4.1.3. Threats of substitution

- 3.4.1.4. Threats from new entrants

- 3.4.1.5. Competitive rivalry

- 3.4.2. PESTEL Analysis

- 3.4.2.1. Political landscape

- 3.4.2.2. Economic and Social landscape

- 3.4.2.3. Technological landscape

- 3.4.2.4. Environmental landscape

- 3.4.2.5. Legal landscape

- 3.4.1. Porter's Analysis

Chapter 4. Injectable Drug Delivery Devices Market: Product Estimates & Trend Analysis

- 4.1. Segment Dashboard

- 4.2. Injectable Drug Delivery Devices Market: Product Movement Analysis, 2023 & 2030 (USD Million)

- 4.3. Devices

- 4.3.1. Devices Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

- 4.3.2. Self-injection Devices

- 4.3.2.1. Self-injection Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 4.3.3. Conventional Devices

- 4.3.3.1. Conventional Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 4.4. Formulations

- 4.4.1. Formulations Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

- 4.4.2. Conventional Drug Delivery

- 4.4.2.1. Conventional Drug Delivery Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 4.4.3. Novel Drug Delivery

- 4.4.3.1. Novel Drug Delivery Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 4.4.4. Others

- 4.4.4.1. Others Market Estimates and Forecasts, 2018 - 2030 (USD Million)

Chapter 5. Injectable Drug Delivery Devices Market: Therapeutic Use Estimates & Trend Analysis

- 5.1. Segment Dashboard

- 5.2. Injectable Drug Delivery Devices Market: Therapeutic Use Movement Analysis, 2023 & 2030 (USD Million)

- 5.3. Autoimmune Disorders

- 5.3.1. Autoimmune Disorders Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

- 5.4. Hormonal Disorders

- 5.4.1. Hormonal Disorders Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

- 5.5. Oncology

- 5.5.1. Oncology Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

- 5.6. Others

- 5.6.1. Others Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

Chapter 6. Injectable Drug Delivery Devices Market: End Use Estimates & Trend Analysis

- 6.1. Segment Dashboard

- 6.2. Injectable Drug Delivery Devices Market: End Use Movement Analysis, 2023 & 2030 (USD Million)

- 6.3. Hospitals

- 6.3.1. Hospitals Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

- 6.4. Homecare Settings

- 6.4.1. Homecare Settings Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

- 6.5. Others

- 6.5.1. Others Market Revenue Estimates and Forecasts, 2018 - 2030 (USD Million)

Chapter 7. Injectable Drug Delivery Devices Market: Regional Estimates & Trend Analysis

- 7.1. Injectable Drug Delivery Devices Market Share, By Region, 2023 & 2030 (USD Million)

- 7.2. North America

- 7.2.1. North America Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.2.2. U.S.

- 7.2.2.1. U.S. Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.2.3. Canada

- 7.2.3.1. Canada Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.2.4. Mexico

- 7.2.4.1. Mexico Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3. Europe

- 7.3.1. Europe Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3.2. UK

- 7.3.2.1. UK Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3.3. Germany

- 7.3.3.1. Germany Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3.4. France

- 7.3.4.1. France Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3.5. Italy

- 7.3.5.1. Italy Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3.6. Spain

- 7.3.6.1. Spain Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3.7. Denmark

- 7.3.7.1. Denmark Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3.8. Sweden

- 7.3.8.1. Sweden Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.3.9. Norway

- 7.3.9.1. Norway Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.4. Asia Pacific

- 7.4.1. Asia Pacific Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.4.2. China

- 7.4.2.1. China Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.4.3. Japan

- 7.4.3.1. Japan Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.4.4. India

- 7.4.4.1. India Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.4.5. South Korea

- 7.4.5.1. South Korea Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.4.6. Australia

- 7.4.6.1. Australia Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.4.7. Thailand

- 7.4.7.1. Thailand Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.5. Latin America

- 7.5.1. Latin America Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.5.2. Brazil

- 7.5.2.1. Brazil Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.5.3. Argentina

- 7.5.3.1. Argentina Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.6. Middle East and Africa

- 7.6.1. Middle East and Africa Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.6.2. South Africa

- 7.6.2.1. South Africa Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.6.3. Saudi Arabia

- 7.6.3.1. Saudi Arabia Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.6.4. UAE

- 7.6.4.1. UAE Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

- 7.6.5. Kuwait

- 7.6.5.1. Kuwait Injectable Drug Delivery Devices Market Estimates and Forecasts, 2018 - 2030 (USD Million)

Chapter 8. Competitive Landscape

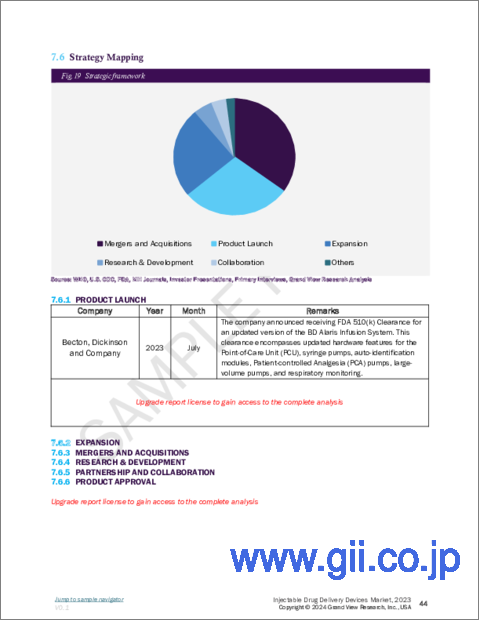

- 8.1. Recent Developments & Impact Analysis by Key Market Participants

- 8.2. Company Categorization

- 8.3. Company Heat Map Analysis

- 8.4. Company Profiles

- 8.4.1. Baxter

- 8.4.1.1. Participant's Overview

- 8.4.1.2. Financial Performance

- 8.4.1.3. Product Benchmarking

- 8.4.1.4. Recent Developments/ Strategic Initiatives

- 8.4.2. Schott AG

- 8.4.2.1. Participant's Overview

- 8.4.2.2. Financial Performance

- 8.4.2.3. Product Benchmarking

- 8.4.2.4. Recent Developments/ Strategic Initiatives

- 8.4.3. BD

- 8.4.3.1. Participant's Overview

- 8.4.3.2. Financial Performance

- 8.4.3.3. Product Benchmarking

- 8.4.3.4. Recent Developments/ Strategic Initiatives

- 8.4.4. Eli Lilly and Company

- 8.4.4.1. Participant's Overview

- 8.4.4.2. Financial Performance

- 8.4.4.3. Product Benchmarking

- 8.4.4.4. Recent Developments/ Strategic Initiatives

- 8.4.5. Terumo Corporation

- 8.4.5.1. Participant's Overview

- 8.4.5.2. Financial Performance

- 8.4.5.3. Product Benchmarking

- 8.4.5.4. Recent Developments/ Strategic Initiatives

- 8.4.6. Elcam Medical

- 8.4.6.1. Participant's Overview

- 8.4.6.2. Financial Performance

- 8.4.6.3. Product Benchmarking

- 8.4.6.4. Recent Developments/ Strategic Initiatives

- 8.4.7. Unilife Corporation

- 8.4.7.1. Participant's Overview

- 8.4.7.2. Financial Performance

- 8.4.7.3. Product Benchmarking

- 8.4.7.4. Recent Developments/ Strategic Initiatives

- 8.4.8. Ypsomed AG

- 8.4.8.1. Participant's Overview

- 8.4.8.2. Financial Performance

- 8.4.8.3. Product Benchmarking

- 8.4.8.4. Recent Developments/ Strategic Initiatives

- 8.4.9. Gerresheimer AG

- 8.4.9.1. Participant's Overview

- 8.4.9.2. Financial Performance

- 8.4.9.3. Product Benchmarking

- 8.4.9.4. Recent Developments/ Strategic Initiatives

- 8.4.10. Sanofi

- 8.4.10.1. Participant's Overview

- 8.4.10.2. Financial Performance

- 8.4.10.3. Product Benchmarking

- 8.4.10.4. Recent Developments/ Strategic Initiatives

- 8.4.1. Baxter