|

|

市場調査レポート

商品コード

1405062

米国の産業ガスの市場規模、シェア、動向分析レポート:製品別、用途別、セグメント別予測、2024~2030年U.S. Industrial Gases Market Size, Share & Trends Analysis Report By Product (Nitrogen, Hydrogen, Carbon Dioxide), By Application (Healthcare, Manufacturing), And Segment Forecasts, 2024 - 2030 |

||||||

|

|

|||||||

カスタマイズ可能

|

|||||||

| 米国の産業ガスの市場規模、シェア、動向分析レポート:製品別、用途別、セグメント別予測、2024~2030年 |

|

出版日: 2023年11月30日

発行: Grand View Research

ページ情報: 英文 70 Pages

納期: 2~10営業日

|

- 全表示

- 概要

- 図表

- 目次

米国の産業ガス市場の成長と動向:

Grand View Research, Incの最新レポートによると、米国の産業ガス市場は2030年までに393億8,000万米ドルに達すると推定され、2024年から2030年までのCAGRは6.7%で成長すると予測されています。

この成長は、製造業、ヘルスケア、飲食品、冶金などの様々な産業におけるこれらのガスのアプリケーションの増加に起因しており、今後数年間の米国産業ガス市場の成長に影響を与えると予想されています。

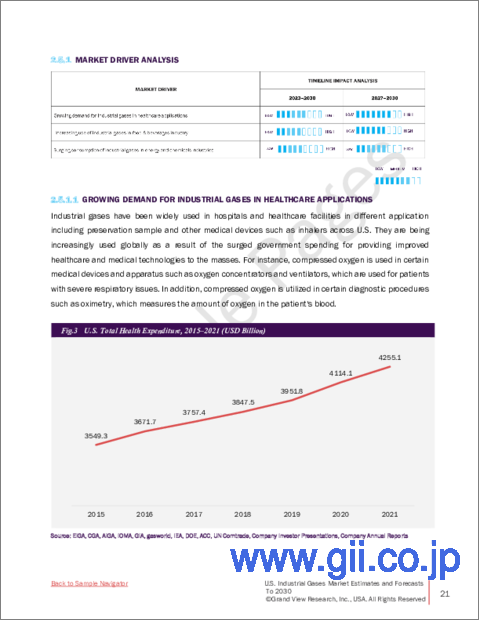

米国市場では、酸素は鉄鋼や銅の生産、医療用途、燃費改善プログラムなどで広く使用されています。炉で酸素化プロセスを実行することで、鉄鋼、セメント、銅の生産で必要とされる効率的なエネルギー生成が可能になります。酸素はまた、有害物質の洗浄や汚染水の処理にも利用できます。石炭ガス化システムにも使用されています。さらに、パルプ・製紙業界では塩素の代替として使用し、汚染を減らすこともできます。

米国のエレクトロニクス産業では、プリンテッドエレクトロニクス、半導体、フラットパネル・ディスプレイに使用されるため、工業用ガスの需要が急増しています。この業界では、六フッ化硫黄(SF6)、三フッ化窒素(NF3)、シラン(SiH4)などの工業用ガスを使用して、シリコンウエハーや集積回路、フラットパネル・ディスプレイ、化合物半導体などの最先端部品を開発しています。エレクトロニクス産業では、技術革新や新製品開発のために工業用ガスが必要とされています。

プラズマスクリーンの製造には窒素とアルゴンガスが使われ、ハードディスクドライブの開発にはヘリウムが使われています。さらに、工業用ガスは、製造工程中の電子システムの冷却、特に高性能マイクロプロセッサの製造に使用されます。このように、産業ガスの利用可能性と有効利用は、効率、品質、生産高を向上させることにより、エレクトロニクス産業に大きな影響を与えています。

炭素回収・利用・貯蔵(CCUS)技術の開拓は、産業ガス市場の成長機会を生み出しています。これらの技術は、増進回収法(EOR)に使用する二酸化炭素を必要とするからです。また、地層から二酸化炭素を隔離するためにも使われます。

米国の産業ガス市場は競合が激しいだけでなく、統合も進んでいます。市場をリードするのは、エア・リキード、メッサー北米、リンデ&エアープロダクツ&ケミカルズです。これらの企業は米国の産業ガス市場で大きなシェアを占めており、世界的に大きな顧客基盤を持っています。さらに、これらの大手メーカーは、幅広い製品ポートフォリオにより、ほぼすべての最終用途産業の産業ガス要件に対応しています。

米国産業ガス市場レポート・ハイライト

- 酸素は2024年から2030年までのCAGRが7.0%で、最も急成長している製品セグメントに浮上しました。酸素の多用途性により、酸素はヘルスケア産業と化学産業に不可欠な要素となっています。病院や診療所では、医療用酸素は様々な手術や治療に不可欠です。

- 酸素はまた、溶接、金属切断、洗浄、溶融用途にも使用されます。さらに酸素は、食品業界では赤身肉の新鮮で自然な色を維持するために使用されます。

- ヘルスケアは2024年から2030年までのCAGRが7.3%で最も急成長している製品分野であり、これは人々の健康状態の高まりによるものです。

- 米国の様々な最終用途産業からの工業用ガスに対する需要の増加は、市場プレーヤーが地域的な足跡を増やし、製品範囲を広げることを後押ししています。この市場で活発に活動している主要企業には、リンデ・グループ、メッサー・グループ、エアープロダクツ&ケミカルズ社、エア・リキード社などがあります。

- 業界各社は、より多くの地域でサービスを提供し、業界における市場シェアをさらに拡大するために、数多くの製品開拓とイノベーションを行っています。例えば、2023年1月、エア・リキードは、金属、ガラス、二次電子機器、浄水などの拡大する市場において、水素、窒素、酸素を顧客に提供するための複数の長期契約を産業用商材ビジネスラインで締結しました。

- さらに、プレーヤーは市場での自社製品のリーチを広げるために拡大戦略も採用しています。この無機的成長戦略を採用している主な市場プレーヤーは、イノックス・エア・プロダクツ、エア・リキード、リンデplcなどです。例えば、リンデ社は2024年までにフリーポートに新しいヘリウム処理プラントを建設する計画で、回収ヘリウムを精製・液化して米国の最終用途産業で使用します。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 米国の産業ガス:市場変数、動向、範囲

- 市場系統の見通し

- 世界の産業ガス市場の見通し

- 業界のバリューチェーン分析

- 原材料の動向

- 製造・技術動向

- 販売チャネル分析

- 潜在的なエンドユーザーのリスト

- 価格に影響を与える要因

- 規制の枠組み

- 市場力学

- 市場促進要因分析

- 市場抑制要因分析

- 市場課題の分析

- 市場機会分析

- 業界分析ツール

- ポーターズ分析

- マクロ経済分析-PESTLE分析

第4章 米国の産業ガス:サプライヤーのポートフォリオ分析

- 主要な原材料サプライヤーのリスト

- ポートフォリオ分析/Kraljicマトリックス

- エンゲージメントモデル

- 交渉戦略

- 調達のベストプラクティス

第5章 ラスベガスの産業ガス市場展望

- 製品の推定・動向分析

- 用途の推定・動向分析

第6章 米国の産業ガス市場:製品推定・動向分析

- 製品の変動分析と市場シェア、2023年と2030年

- 窒素

- 水素

- 二酸化炭素

- 酸素

- アルゴン

- アセチレン

第7章 米国の産業ガス市場:用途の推定・動向分析

- 用途の変動分析と市場シェア、2023年と2030年

- ヘルスケア

- 製造業

- 冶金とガラス

- 食品・飲料

- 小売り

- 化学物質とエネルギー

- その他の用途

第8章 競合情勢

- 主要市場参入企業による最近の動向と影響分析

- 会社の分類

- ベンダー情勢

- 企業の市場ポジショニング分析、2023年

- 企業ヒートマップ分析

- 戦略マッピング

- 会社一覧(事業概要、財務実績、製品ベンチマーク)

- Messer North America, Inc.

- Air Products and Chemicals, Inc.

- Linde plc

- Air Liquide

- Matheson Tri-Gas, Inc

- BASF SE

- MESA Specialty Gases &Equipment

- Universal Industrial Gases, Inc.

List of Tables

- Table 1 List of Raw Material Suppliers

- Table 2 List of Potential End-Users

- Table 3 Recent Developments & Impact Analysis, By Key Market Participants

- Table 4 Company Heat Map Analysis

- Table 5 Financial Performance

- Table 6 Product Benchmarking

- Table 7 Key Companies launching new products.

List of Figures

- Fig. 1 U.S. Industrial Gases Market Segmentation & Scope

- Fig. 2 Information procurement

- Fig. 3 Data analysis models

- Fig. 4 Market formulation and validation

- Fig. 5 Data validation & publishing

- Fig. 6 U.S. Industrial Gases Market Snapshot

- Fig. 7 U.S. Industrial Gases Market Segment Snapshot

- Fig. 8 U.S. Industrial Gases Market Competitive Landscape Snapshot

- Fig. 9 Global Industrial Gases Market Value, 2023 (USD Billion)

- Fig. 10 U.S. Industrial Gases Market: Industry Value Chain Analysis

- Fig. 11 U.S. Industrial Gases Market Dynamics

- Fig. 12 U.S. Industrial Gases Market: Porter's Analysis

- Fig. 13 U.S. Industrial Gases Market: PESTLE Analysis

- Fig. 14 U.S. Industrial Gases Market Estimates & Forecasts, by Product: Key Takeaways

- Fig. 15 U.S. Industrial Gases Market Share, By Product, 2023 & 2030

- Fig. 16 Nitrogen Market Estimates & Forecasts, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 17 Hydrogen Market Estimates & Forecasts, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 18 Carbon Dioxide Market Estimates & Forecasts, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 19 Oxygen Market Estimates & Forecasts, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 20 Argon Market Estimates & Forecasts, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 21 Acetylene Market Estimates & Forecasts, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 22 U.S. Industrial Gases Market Estimates & Forecasts, by Application: Key Takeaways

- Fig. 23 U.S. Industrial Gases Market Share, By Application, 2023 & 2030

- Fig. 24 U.S. Industrial Gases Market Estimates & Forecasts, In Healthcare, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 25 U.S. Industrial Gases Market Estimates & Forecasts, in Manufacturing, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 26 U.S. Industrial Gases Market Estimates & Forecasts, in Metallurgy & Glass, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 27 U.S. Industrial Gases Market Estimates & Forecasts, in Food & Beverages, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 28 U.S. Industrial Gases Market Estimates & Forecasts, in Retail, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 29 U.S. Industrial Gases Market Estimates & Forecasts, in Chemicals & Energy, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 30 U.S. Industrial Gases Market Estimates & Forecasts, in Other Applications, 2018 - 2030 (Kilotons) (USD Million)

- Fig. 31 Key Company Categorization

- Fig. 32 U.S. Industrial Gases Market - Company Market Positioning Analysis - 2023

- Fig. 33 Strategic Mapping

U.S. Industrial Gases Market Growth & Trends:

The U.S. industrial gases market is estimated to reach USD 39.38 billion by 2030, according to a new report by Grand View Research, Inc, projected to grow at a CAGR of 6.7% from 2024 to 2030. This growth has been attributed to and increasing application of these gases in various industries such as manufacturing, healthcare, food & beverages, and metallurgy, are expected to influence the growth of the market for U.S. industries gases in the coming years.

In the U.S. market, oxygen is widely used in steel and copper production, medical applications, and fuel efficiency improvement programs. The execution of the oxygenation process in furnaces can result in efficient energy generation that is required in steel, cement, and copper production. Oxygen can also be used for cleaning hazardous materials and treating polluted water. It is used in coal gasification systems as well. Additionally, it can be employed as an alternative to chlorine in the pulp & paper industry to reduce pollution.

The demand for industrial gases is surging in the electronics industry in the U.S. owing to their use in printed electronics, semiconductors, and flat-panel displays. This industry uses industrial gases such as sulfur hexafluoride (SF6), nitrogen trifluoride (NF3), and silane (SiH4) to develop cutting-edge components such as silicon wafers and integrated circuits, flat-panel displays, and compound semiconductors. Industrial gases are required in the electronics industry to carry out innovations and new product developments.

Nitrogen and argon gases are used in the production of plasma screens, while helium is employed for the development of hard disk drives. Additionally, industrial gases are used to cool electronic systems during manufacturing processes, particularly the ones that are used for producing high-performance microprocessors. Thus, the availability and effective use of industrial gases have significantly impacted the electronics industry by improving efficiency, quality, and output.

The development of carbon capture, utilization, and storage (CCUS) technologies creates opportunities for the growth of the industrial gas market as these technologies require carbon dioxide for use in enhanced oil recovery (EOR) operations. They are also used for sequestering carbon dioxide from geological formations.

The industrial gas market in the U.S. is not only competitive but highly consolidated as well. The leading players operating in the market are Air Liquide, Messer North America, and Linde Plc & Air Products and Chemicals, Inc. These companies account for a large share of the industrial gas market in the U.S. They have a large customer base globally. Moreover, these large manufacturers cater to the industrial gas requirements of almost every end-use industry owing to their broad product portfolios.

U.S. Industrial Gases Market Report Highlights:

- Oxygen emerged as the fastest-growing product segment with a CAGR of 7.0% from 2024 to 2030, the versatility of oxygen makes it a vital component in the healthcare and chemicals industries. In hospitals and health clinics, medical oxygen is essential for a variety of surgeries and therapies

- Oxygen is also used for welding, metal cutting, cleaning, and melting applications. Furthermore, oxygen is used to maintain the fresh and natural color of red meat in the food industry

- Healthcare is the fastest growing product segment with a CAGR of 7.3% from 2024 to 2030 owing to the rising health conditions among people

- Increasing demand for industrial gases from various end-use industries in U.S. has encouraged the market players to increase their regional footprint and broaden their product range. Some key companies actively operating in this market are The Linde Group, Messer Group, Air Products & Chemicals Inc., Air Liquide, etc

- Numerous product developments and innovations are being made by the industry players in order to serve a larger geographical portion, further increasing their market share in the industry. For instance, in January 2023, Air Liquide signed multiple long-term contracts to provide hydrogen, nitrogen, and oxygen to customers in the expanding markets of metals, glass, secondary electronics, and water purification for its industrial merchant business line

- Moreover, players also adopt the expansion strategy to increase the reach of their products in the market. Key market players adopting this inorganic growth strategy include INOX-Air Products, Air Liquide, and Linde plc. For instance, Linde Company plans to build a new helium processing plant in Freeport by 2024, which will purify and liquefy recovered helium for use in end-use industries in the U.S. The plant will produce nearly 200 MCF (million cubic feet) of helium

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market Segmentation & Scope

- 1.2 Market Definition

- 1.3 Information Procurement

- 1.3.1 Purchased Database

- 1.3.2 GVR's Internal Database

- 1.4 Information analysis

- 1.5 Market formulation & data visualization

- 1.6 Data validation & publishing

- 1.6.1 Research scope and assumptions

- 1.6.2 List of Data Sources

Chapter 2 Executive Summary

- 2.1 Market Snapshot

- 2.2 Segment Snapshot

- 2.3 Competitive Landscape Snapshot

Chapter 3 U.S. Industrial Gases: Market Variables, Trends & Scope

- 3.1 Market Lineage Outlook

- 3.1.1 Global Industrial Gases Market Outlook

- 3.2 Industry Value Chain Analysis

- 3.2.1 Raw Material Trends

- 3.2.3 Manufacturing/Technology Trends

- 3.3.3 Sales Channel Analysis

- 3.3 List of Potential End-Users

- 3.4 Factors influencing prices

- 3.5 Regulatory Framework

- 3.6 Market Dynamics

- 3.6.1 Market Driver Analysis

- 3.6.2 Market Restraint Analysis

- 3.6.3 Market Challenge Analysis

- 3.6.4 Market Opportunities Analysis

- 3.7 Industry Analysis Tools

- 3.7.1 PORTERs Analysis

- 3.7.2 Macroeconomic Analysis- PESTLE Analysis

Chapter 4 U.S. Industrial Gases: Supplier Portfolio Analysis

- 4.1 List of Key Raw Material Suppliers

- 4.2 Portfolio Analysis/Kraljic Matrix

- 4.3 Engagement Model

- 4.4 Negotiation Strategies

- 4.5 Sourcing Best Practices

Chapter 5 Las Vegas Industrial Gases Market Outlook

- 5.1 Product Estimates & Trend Analysis

- 5.1.1 Product Movement Analysis & Market Share, 2023 & 2030

- 5.1.1.1 Nitrogen

- 5.1.1.2 Hydrogen

- 5.1.1.3 Carbon Dioxide

- 5.1.1.4 Oxygen

- 5.1.1.5 Argon

- 5.1.1.6 Acetylene

- 5.1.1 Product Movement Analysis & Market Share, 2023 & 2030

- 5.2 Application Estimates & Trend Analysis

- 5.2.1 Application Movement Analysis & Market Share, 2023 & 2030

- 5.2.1.1 Healthcare

- 5.2.1.2 Manufacturing

- 5.2.1.3 Metallurgy & Glass

- 5.2.1.4 Food & Beverages

- 5.2.1.5 Retail

- 5.2.1.6 Chemicals & Energy

- 5.2.1.7 Others Applications

- 5.2.1 Application Movement Analysis & Market Share, 2023 & 2030

Chapter 6 U.S. Industrial Gases Market: Product Estimates & Trend Analysis

- 6.1 Product Movement Analysis & Market Share, 2023 & 2030

- 6.1.1 Nitrogen

- 6.1.2 Hydrogen

- 6.1.3 Carbon Dioxide

- 6.1.4 Oxygen

- 6.1.5 Argon

- 6.1.6 Acetylene

Chapter 7 U.S. Industrial Gases Market: Application Estimates & Trend Analysis

- 7.1 Application Movement Analysis & Market Share, 2023 & 2030

- 7.1.1 Healthcare

- 7.1.2 Manufacturing

- 7.1.3 Metallurgy & Glass

- 7.1.4 Food & Beverages

- 7.1.5 Retail

- 7.1.6 Chemicals & Energy

- 7.1.7 Others Applications

Chapter 8 Competitive Landscape

- 8.1 Recent Developments & Impact Analysis, By Key Market Participants

- 8.2 Company Categorization'

- 8.3 Vendor Landscape

- 8.3.1 List Of Key Distributors & Channel Partners

- 8.3.2 List Of End-Users

- 8.4 Company Market Positioning Analysis, 2023

- 8.5 Company Heat Map Analysis

- 8.6 Strategy Mapping

- 8.7 Company Listing (Business Overview, Financial Performance, Product Benchmarking)

- 8.7.1 Messer North America, Inc.

- 8.7.2 Air Products and Chemicals, Inc.

- 8.7.3 Linde plc

- 8.7.4 Air Liquide

- 8.7.5 Matheson Tri-Gas, Inc

- 8.7.6 BASF SE

- 8.7.7 MESA Specialty Gases & Equipment

- 8.7.8 Universal Industrial Gases, Inc.