|

|

市場調査レポート

商品コード

1571997

経皮的冠動脈インターベンション(PCI)機器の世界市場Percutaneous Coronary Intervention (PCI) Devices |

||||||

|

|||||||

適宜更新あり

|

|||||||

| 経皮的冠動脈インターベンション(PCI)機器の世界市場 |

|

出版日: 2024年10月18日

発行: Market Glass, Inc. (Formerly Global Industry Analysts, Inc.)

ページ情報: 英文 193 Pages

納期: 即日から翌営業日

|

全表示

- 概要

- 目次

経皮的冠動脈インターベンション(PCI)機器の世界市場は2030年までに米国で138億米ドルに達する見込み

2023年に93億米ドルと推定される経皮的冠動脈インターベンション(PCI)機器の世界市場は、分析期間2023-2030年にCAGR 5.8%で成長し、2030年には138億米ドルに達すると予測されます。本レポートで分析したセグメントの1つである冠動脈ステントは、CAGR 5.1%を記録し、分析期間終了時には54億米ドルに達すると予測されます。PTCAカテーテルセグメントの成長率は、分析期間でCAGR 7.3%と推定されます。

米国市場は25億米ドル、中国はCAGR5.5%で成長予測

米国の経皮的冠動脈インターベンション(PCI)機器市場は2023年に25億米ドルと推定されます。世界第2位の経済大国である中国は、2030年までに22億米ドルの市場規模に達すると予測され、分析期間2023-2030年のCAGRは5.5%です。その他の注目すべき地域別市場としては、日本とカナダがあり、分析期間中のCAGRはそれぞれ4.9%と4.9%と予測されています。欧州では、ドイツがCAGR 4.5%で成長すると予測されています。

世界の経皮的冠動脈インターベンション(PCI)機器市場- 主要動向と促進要因まとめ

技術革新はPCIデバイスをどう変えるか?

経皮的冠動脈インターベンション(PCI)機器市場は、冠動脈疾患治療の安全性と有効性の向上を目指した技術革新によって著しい変貌を遂げています。狭窄した冠動脈を開くために用いられる低侵襲手技であるPCIは、ステント、カテーテル、バルーン血管形成術など様々なデバイスに依存しています。技術の進歩により薬剤溶出ステント(DES)が開発され、これは再狭窄(動脈の再狭窄)を防ぐために薬剤を放出するもので、ベアメタルステントと比較して長期予後を大幅に改善します。さらに、時間の経過とともに溶解する生体吸収性ステントも有望な選択肢として台頭してきており、長期的な合併症を減らす可能性があります。光干渉断層計(OCT)や血管内超音波(IVUS)のような血管内イメージング技術などの他の技術革新は、動脈の正確な可視化を可能にし、より正確なステント留置を可能にし、手技のリスクを軽減します。ロボット支援型PCIの出現も勢いを増しており、複雑な手技中の精度の向上とオペレーターの疲労の軽減を提供しています。このような技術的進歩により、PCI機器はより効果的で患者に優しいものとなり、世界中のヘルスケアシステムで採用が進んでいます。

なぜPCI装置は冠動脈疾患の治療において不可欠になってきているのか?

人口の高齢化、座りがちなライフスタイル、糖尿病や高血圧の増加などの要因によって冠動脈疾患(CAD)の有病率が増加しているため、PCI装置の需要が大幅に増加しています。PCI手術は、従来の冠動脈バイパス移植(CABG)手術に代わる侵襲の少ない代替手段を提供し、回復時間を短縮し、合併症のリスクを低下させる。ステント技術やカテーテル設計の進歩と相まって、PCIの高い成功率は、安定狭心症と心臓発作のような急性冠症候群の両方に対する好ましい治療選択肢となっています。さらに、心臓カテーテル検査室の増加と熟練したインターベンショナル・カーディオロジストの増加が、PCI機器の採用をさらに後押ししています。ヘルスケアプロバイダーが心血管疾患患者の予後改善に注力する中、PCI機器はCADの管理と治療において、特にハイリスク患者や開心術の理想的な候補者ではない患者において、ますます重要な役割を果たすようになっています。

規制当局の承認と市場力学はPCI機器市場にどのような影響を与えているか?

規制当局の承認と進化するヘルスケア政策がPCI機器市場を大きく形成しています。米国食品医薬品局(FDA)や欧州医薬品庁(EMA)などの厳しい規制要件により、PCIデバイスは臨床使用が承認される前に高い安全性と有効性の基準を満たしていることが保証されています。新世代の薬剤溶出性ステントや生体吸収性血管足場が最近承認されたことで、これらのデバイスは予後が改善し合併症発生率が低下するため、市場の成長をさらに後押ししています。さらに、価値ベースのヘルスケアへの注目の高まりは、臨床転帰を改善するだけでなく長期的な医療費も削減するPCIデバイスの採用に病院や心臓病センターに影響を与えています。低侵襲手技が重視されるようになったことも、メーカーが革新的なPCI機器を開発・販売する機会を生み出しています。臨床試験の実施や最先端技術の開発を目的とした機器メーカーとヘルスケアプロバイダーのコラボレーションは、この競合市場における製品革新のペースを加速させています。

PCI機器市場の成長を促す要因とは?

経皮的冠動脈インターベンション(PCI)機器市場の成長は、技術の進歩、冠動脈疾患の有病率の上昇、ヘルスケアインフラ投資の増加など、いくつかの要因によって牽引されています。主な促進要因のひとつは、薬剤溶出ステント、生体吸収性ステント、改良型カテーテル技術の開発が進んでいることであり、これらはPCI手技の有効性を大幅に高めています。さらに、特に高齢化社会と肥満と糖尿病の割合が増加している地域における心血管系疾患の世界の負担が、低侵襲的冠動脈インターベンションに対する需要の高まりにつながっています。先進医療機器に対する規制上の支援は、心臓カテーテル検査室の増加とともに、先進国市場と新興国市場の両方でPCI手技の利用可能性を拡大しています。さらに、患者の転帰の改善と医療費の削減に重点を置く価値観に基づくヘルスケアモデルへのシフトが、病院や診療所に高度なPCI技術の採用を促しています。冠動脈疾患に対する低侵襲でより効果的な治療に対する需要が高まり続ける中、PCI機器市場は持続的な成長が見込まれています。

世界の穿孔ガン市場- 主要動向と促進要因のまとめ

技術進歩は穿孔ガン市場にどのような影響を与えているか?

技術の進歩は、石油・ガス井の穿孔をより効率的で正確なものにし、穿孔ガン市場に革命を起こす上で重要な役割を果たしています。坑井完成プロセスで使用される重要なツールである穿孔ガンは、坑井と貯水池の間にトンネルを作り、石油・ガスが坑井に流れ込むようにします。高度な形状の装薬、電子起爆システム、アドレス指定可能なスイッチなどの技術革新により、穿孔作業の効率と安全性が大幅に改善されました。先進的な形状の装薬により、より深くきれいな穿孔が可能になり、地層へのダメージを最小限に抑えながら坑井の生産性を向上させることができるようになった。さらに、従来の機械式に代わって電子式パーフォレーション・システムが採用され、信頼性の向上、正確なタイミング、起爆プロセスのリアルタイム制御が可能になった。これらのシステムは、誤爆のリスクを低減し、1回の作業で複数ゾーンの穿孔を可能にし、作業効率を最適化します。さらに、モジュール式や再利用可能な穿孔ガンを含むガン設計の革新は、運用コストを下げ、坑井の完成における環境の持続可能性を高めています。これらの進歩は、陸上および海上掘削作業におけるパーフォレーティングガンの採用を促進しています。

なぜ石油・ガス産業でパーフォレーティングガンが重要なのか?

パーフォレーションガンは、貯留層からの炭化水素の効率的な抽出を可能にすることで、石油・ガス産業において重要な役割を果たしています。坑井が掘削された後、穿孔ガンはケーシングとセメントを貫通し、坑井と石油・ガス貯留層をつなぐ溝を作るために使用されます。このプロセスは、炭化水素の流れを促進し、坑井の生産性を最大化するために不可欠です。パーフォレーティング・ガンは汎用性が高いため、シェール層での水圧破砕(フラッキング)を含め、従来型と非従来型の両方の掘削作業に不可欠です。掘削条件がより厳しい海洋作業では、高圧高温(HPHT)環境用に設計されたパーフォレーティングガンが、信頼性の高い性能と安全性を保証します。石油・ガスに対する世界の需要が、特に新興経済国において増加し続けているため、先進的なパーフォレーティングガンのような、効率的で費用対効果の高い坑井掘削技術に対するニーズも高まっています。パーフォレーティングガンは、生産量を最適化するために不可欠であるだけでなく、ダウンタイムを削減し、坑井作業の全体的な経済性を向上させる上で重要な役割を果たします。

業界動向と環境への配慮はどのようにパーフォレーティングガン市場を形成しているか?

業界動向、特にコスト効率と環境の持続可能性への関心の高まりが、パーフォレーティングガン市場の将来を形成しています。石油・ガス会社は、環境への影響を低減しながら坑井の生産性を高めるパーフォレーティング技術をますます求めるようになっています。その結果、何度も配備できる再利用可能なモジュール式穿孔ガンに対する需要が高まっており、廃棄物の削減と運用コストの低減を実現しています。さらに、高性能の成形爆薬の進歩により、穿孔時に使用される爆薬の量が最小限に抑えられており、坑井の完成に伴う環境フットプリントの低減に役立っています。石油・ガス操業のデジタル化と自動化へのシフトも市場に影響を及ぼしており、電子雷管システムは、その精度、信頼性、他の坑内技術との統合能力により、普及が進んでいます。さらに、水平掘削やフラッキングなどの非従来型掘削技術の採用が増加しているため、複雑な坑井形状と高圧に対応できる高度な穿孔システムに対する需要が高まっています。環境規制が厳しくなるにつれ、持続可能で効率的な穿孔ソリューションに対する業界の注目は高まり続けると思われます。

穿孔ガン市場の成長を促進する要因は何か?

穿孔ガン市場の成長は、技術の進歩、石油・ガスに対する世界の需要の増加、非従来型掘削作業の拡大など、いくつかの要因によってもたらされます。主な促進要因の1つは、坑井の生産性と作業効率を向上させる高度な穿孔技術の開発です。また、電子爆発システムや再利用可能な穿孔ガンの採用が増加していることも、これらの技術が坑井完成時のコストを削減し安全性を向上させることから、市場成長に寄与しています。さらに、シェール層での水圧破砕などの非従来型掘削方法への世界のシフトが、複雑な坑井環境に対応できる高性能のパーフォレーティングガンに対する需要を煽っています。環境の持続可能性への関心の高まりと、より厳しい規制に準拠する必要性から、石油・ガス会社は、資源を最大限に抽出しながら環境への影響を最小限に抑えるパーフォレーティングシステムへの投資を促しています。エネルギー産業が進化を続ける中、パーフォレーティングガン市場は、こうした技術、環境、運用の動向に後押しされて拡大すると予想されます。

調査対象企業の例(注目の44社)

- Abbott Laboratories

- AMG International

- Asahi Intecc Co., Ltd.

- B. Braun Melsungen AG

- Biosensors International Group Ltd.

- Biotronik SE & Co. KG

- Boston Scientific Corporation

- BrosMed Medical Co., Ltd.

- Claret Medical

- Comed B.V.

- Contego Medical, LLC

- Cordis Corporation

- Elixir Medical Corporation

- EPflex Feinwerktechnik GmbH

- GaltNeedleTech

- Lepu Mdicial Technology(Beijing)Co., Ltd

- Medtronic PLC

- Meril Life Sciences Pvt., Ltd.

- Merit Medical Systems, Inc.

- OptiMed Medizinische Instrumente GmbH

- OrbusNeich

- Penumbra, Inc.

- RONTIS

- SP Medical A/S

- Stentys SA

- Teleflex Inc.

- Terumo Medical Corporation

目次

第1章 調査手法

第2章 エグゼクティブサマリー

- 市場概要

- 主要企業

- 市場動向と促進要因

- 世界市場の見通し

第3章 市場分析

- 米国

- カナダ

- 日本

- 中国

- 欧州

- フランス

- ドイツ

- イタリア

- 英国

- その他欧州

- アジア太平洋

- その他の地域

第4章 競合

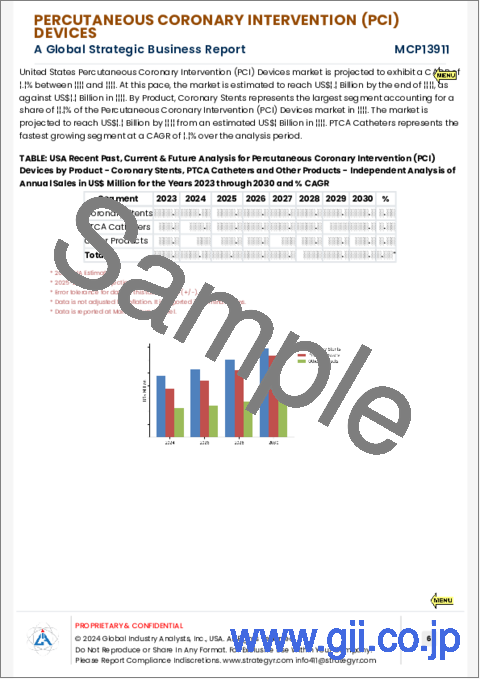

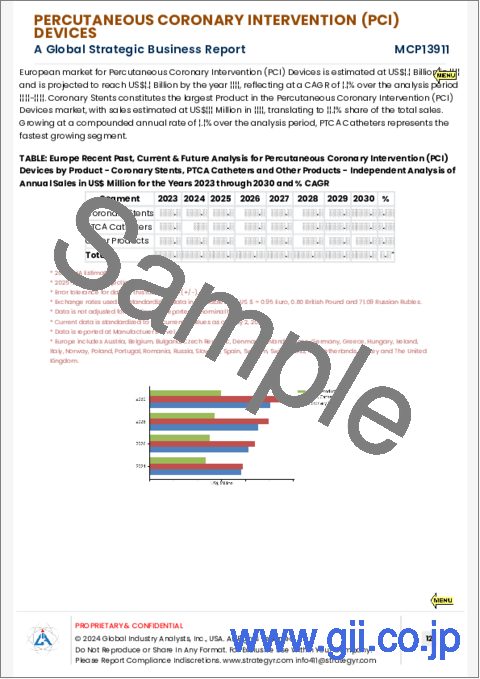

Global Percutaneous Coronary Intervention (PCI) Devices Market to Reach US$13.8 Billion by 2030

The global market for Percutaneous Coronary Intervention (PCI) Devices estimated at US$9.3 Billion in the year 2023, is expected to reach US$13.8 Billion by 2030, growing at a CAGR of 5.8% over the analysis period 2023-2030. Coronary Stents, one of the segments analyzed in the report, is expected to record a 5.1% CAGR and reach US$5.4 Billion by the end of the analysis period. Growth in the PTCA Catheters segment is estimated at 7.3% CAGR over the analysis period.

The U.S. Market is Estimated at US$2.5 Billion While China is Forecast to Grow at 5.5% CAGR

The Percutaneous Coronary Intervention (PCI) Devices market in the U.S. is estimated at US$2.5 Billion in the year 2023. China, the world's second largest economy, is forecast to reach a projected market size of US$2.2 Billion by the year 2030 trailing a CAGR of 5.5% over the analysis period 2023-2030. Among the other noteworthy geographic markets are Japan and Canada, each forecast to grow at a CAGR of 4.9% and 4.9% respectively over the analysis period. Within Europe, Germany is forecast to grow at approximately 4.5% CAGR.

Global Percutaneous Coronary Intervention (PCI) Devices Market – Key Trends & Drivers Summarized

How Are Technological Innovations Transforming PCI Devices?

The percutaneous coronary intervention (PCI) devices market has undergone remarkable transformation, driven by technological innovations aimed at improving the safety and efficacy of coronary artery disease treatments. PCI, a minimally invasive procedure used to open narrowed coronary arteries, relies on a variety of devices such as stents, catheters, and balloon angioplasty. Technological advancements have led to the development of drug-eluting stents (DES), which release medication to prevent restenosis (re-narrowing of the arteries), significantly improving long-term outcomes compared to bare-metal stents. Additionally, bioresorbable stents, which dissolve over time, are emerging as a promising alternative, offering the potential to reduce long-term complications. Other innovations, such as intravascular imaging technologies like optical coherence tomography (OCT) and intravascular ultrasound (IVUS), allow for precise visualization of the arteries, enabling more accurate stent placement and reducing procedural risks. The advent of robotics-assisted PCI is also gaining momentum, offering enhanced precision and reduced operator fatigue during complex procedures. These technological advancements are making PCI devices more effective and patient-friendly, thereby driving adoption across healthcare systems globally.

Why Are PCI Devices Becoming Crucial in the Treatment of Coronary Artery Disease?

The growing prevalence of coronary artery disease (CAD), driven by factors such as aging populations, sedentary lifestyles, and rising incidences of diabetes and hypertension, has significantly increased the demand for PCI devices. PCI procedures offer a less invasive alternative to traditional coronary artery bypass graft (CABG) surgery, reducing recovery times and lowering the risk of complications. The high success rates of PCI, coupled with advancements in stent technology and catheter design, have made it a preferred treatment option for both stable angina and acute coronary syndromes like heart attacks. Furthermore, the increasing number of cardiac catheterization labs and the rise in skilled interventional cardiologists worldwide are further boosting the adoption of PCI devices. As healthcare providers focus on improving outcomes for patients with cardiovascular diseases, PCI devices are playing an increasingly critical role in managing and treating CAD, particularly in patients who are high-risk or not ideal candidates for open-heart surgery.

How Are Regulatory Approvals and Market Dynamics Influencing the PCI Devices Market?

Regulatory approvals and evolving healthcare policies are significantly shaping the PCI devices market. Stringent regulatory requirements from agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) ensure that PCI devices meet high standards for safety and efficacy before they are approved for clinical use. Recent approvals of newer-generation drug-eluting stents and bioresorbable vascular scaffolds are further driving market growth, as these devices offer improved outcomes and reduced complication rates. In addition, the rising focus on value-based healthcare is influencing hospitals and cardiology centers to adopt PCI devices that not only improve clinical outcomes but also reduce long-term healthcare costs. The growing emphasis on minimally invasive procedures is also creating opportunities for manufacturers to develop and market innovative PCI devices. Collaborations between device manufacturers and healthcare providers, aimed at conducting clinical trials and developing cutting-edge technologies, are accelerating the pace of product innovation in this competitive market.

What Factors Are Driving Growth in the PCI Devices Market?

The growth in the percutaneous coronary intervention (PCI) devices market is driven by several factors, including technological advancements, the rising prevalence of coronary artery disease, and increasing healthcare infrastructure investments. One of the primary drivers is the ongoing development of drug-eluting stents, bioresorbable stents, and improved catheter technologies, which are significantly enhancing the effectiveness of PCI procedures. Additionally, the global burden of cardiovascular diseases, particularly in aging populations and regions with increasing rates of obesity and diabetes, is leading to higher demand for minimally invasive coronary interventions. Regulatory support for advanced medical devices, along with the growing number of cardiac catheterization labs, is expanding the accessibility of PCI procedures in both developed and emerging markets. Moreover, the shift toward value-based healthcare models, which focus on improving patient outcomes and reducing healthcare costs, is prompting hospitals and clinics to adopt advanced PCI technologies. As the demand for less invasive, more effective treatments for coronary artery disease continues to rise, the PCI devices market is expected to experience sustained growth.

Global Perforating Guns Market – Key Trends & Drivers Summarized

How Are Technological Advancements Impacting the Perforating Guns Market?

Technological advancements are playing a crucial role in revolutionizing the perforating guns market, making oil and gas well perforation more efficient and precise. Perforating guns, essential tools used in well-completion processes, create tunnels between the wellbore and the reservoir, allowing oil or gas to flow into the well. Innovations such as advanced-shaped charges, electronic detonation systems, and addressable switches have significantly improved the efficiency and safety of perforation operations. Advanced-shaped charges are now capable of producing deeper and cleaner perforations, enhancing well productivity while minimizing formation damage. Additionally, electronic perforating systems have replaced traditional mechanical ones, offering improved reliability, precise timing, and real-time control over the detonation process. These systems reduce the risk of misfires and allow for multi-zone perforation in a single run, optimizing operational efficiency. Moreover, innovations in gun design, including modular and reusable perforating guns, are lowering operational costs and increasing the environmental sustainability of well completions. These advancements are driving greater adoption of perforating guns in both onshore and offshore drilling operations.

Why Are Perforating Guns Critical in the Oil and Gas Industry?

Perforating guns play a critical role in the oil and gas industry by enabling the efficient extraction of hydrocarbons from reservoirs. After a well has been drilled, perforating guns are used to penetrate the casing and cement to create channels that connect the wellbore to the oil or gas reservoir. This process is vital for enhancing the flow of hydrocarbons and maximizing well productivity. The versatility of perforating guns makes them indispensable for both conventional and unconventional drilling operations, including hydraulic fracturing (fracking) in shale formations. In offshore operations, where drilling conditions are more challenging, perforating guns designed for high-pressure, high-temperature (HPHT) environments ensure reliable performance and safety. As global demand for oil and gas continues to rise, particularly in emerging economies, the need for efficient and cost-effective well-completion technologies, such as advanced perforating guns, is also increasing. Perforating guns are not only essential for optimizing production but also play a key role in reducing downtime and improving the overall economics of well operations.

How Are Industry Trends and Environmental Considerations Shaping the Perforating Guns Market?

Industry trends, particularly the growing focus on cost-efficiency and environmental sustainability, are shaping the future of the perforating guns market. Oil and gas companies are increasingly seeking perforating technologies that enhance well productivity while reducing environmental impact. As a result, there is growing demand for reusable and modular perforating guns that can be deployed multiple times, reducing waste and lowering operational costs. Additionally, advancements in high-performance shaped charges are minimizing the amount of explosives used during perforation, which helps reduce the environmental footprint of well completions. The shift toward digitalization and automation in oil and gas operations is also influencing the market, with electronic detonation systems becoming more popular due to their precision, reliability, and ability to integrate with other downhole technologies. Furthermore, the rising adoption of unconventional drilling techniques, such as horizontal drilling and fracking, is driving demand for advanced perforating systems that can handle complex well geometries and high pressures. As environmental regulations become stricter, the industry’s focus on sustainable and efficient perforating solutions will continue to grow.

What Factors Are Driving Growth in the Perforating Guns Market?

The growth in the perforating guns market is driven by several factors, including technological advancements, increasing global demand for oil and gas, and the expansion of unconventional drilling operations. One of the main drivers is the development of advanced perforating technologies that improve well productivity and operational efficiency. The rising adoption of electronic detonation systems and reusable perforating guns is also contributing to market growth, as these technologies reduce costs and improve safety during well completions. Additionally, the global shift toward unconventional drilling methods, such as hydraulic fracturing in shale formations, is fueling demand for high-performance perforating guns capable of handling complex well environments. The growing focus on environmental sustainability and the need to comply with stricter regulations are prompting oil and gas companies to invest in perforating systems that minimize environmental impact while maximizing resource extraction. As the energy industry continues to evolve, the perforating guns market is expected to expand, driven by these technological, environmental, and operational trends.

Select Competitors (Total 44 Featured) -

- Abbott Laboratories

- AMG International

- Asahi Intecc Co., Ltd.

- B. Braun Melsungen AG

- Biosensors International Group Ltd.

- Biotronik SE & Co. KG

- Boston Scientific Corporation

- BrosMed Medical Co., Ltd.

- Claret Medical

- Comed B.V.

- Contego Medical, LLC

- Cordis Corporation

- Elixir Medical Corporation

- EPflex Feinwerktechnik GmbH

- GaltNeedleTech

- Lepu Mdicial Technology (Beijing) Co., Ltd

- Medtronic PLC

- Meril Life Sciences Pvt., Ltd.

- Merit Medical Systems, Inc.

- OptiMed Medizinische Instrumente GmbH

- OrbusNeich

- Penumbra, Inc.

- RONTIS

- SP Medical A/S

- Stentys SA

- Teleflex Inc.

- Terumo Medical Corporation

TABLE OF CONTENTS

I. METHODOLOGY

II. EXECUTIVE SUMMARY

- 1. MARKET OVERVIEW

- Influencer Market Insights

- World Market Trajectories

- Global Economic Update

- Percutaneous Coronary Intervention (PCI) Devices - Global Key Competitors Percentage Market Share in 2024 (E)

- Competitive Market Presence - Strong/Active/Niche/Trivial for Players Worldwide in 2024 (E)

- 2. FOCUS ON SELECT PLAYERS

- 3. MARKET TRENDS & DRIVERS

- Rising Prevalence of Cardiovascular Diseases (CVD) Drives Growth in Percutaneous Coronary Intervention (PCI) Devices Market

- Technological Advancements in Drug-Eluting Stents (DES) Improve Long-Term Outcomes and Spur Market Growth

- Increasing Adoption of Minimally Invasive Procedures Propels Demand for PCI Devices in Cardiac Interventions

- Rising Use of Bioresorbable Stents Expands Market for Innovative, Temporary PCI Devices

- Technological Innovations in Intravascular Imaging Systems (OCT and IVUS) Enhance Precision in PCI Procedures

- Growing Focus on Robotic-Assisted PCI Systems Strengthens the Business Case for High-Precision Cardiac Interventions

- Increased Demand for Next-Generation Balloon Catheters Expands Market for Advanced PCI Tools

- Rising Adoption of PCI Devices in Treating Acute Coronary Syndromes (ACS) Expands Clinical Applications

- Technological Advancements in Antithrombotic Devices and Drug-Coated Balloons Improve PCI Outcomes

- Growing Focus on Outpatient and Ambulatory PCI Procedures Expands Market for Less Invasive Cardiac Devices

- Rising Geriatric Population and High Prevalence of Coronary Artery Disease (CAD) Drive PCI Market Growth

- Growing Emphasis on Personalized and Precision Medicine Fuels Development of Customized PCI Devices

- 4. GLOBAL MARKET PERSPECTIVE

- TABLE 1: World Percutaneous Coronary Intervention (PCI) Devices Market Analysis of Annual Sales in US$ Million for Years 2014 through 2030

- TABLE 2: World Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 3: World Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 4: World 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets for Years 2014, 2024 & 2030

- TABLE 5: World Recent Past, Current & Future Analysis for Coronary Stents by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 6: World Historic Review for Coronary Stents by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 7: World 16-Year Perspective for Coronary Stents by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 8: World Recent Past, Current & Future Analysis for PTCA Catheters by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 9: World Historic Review for PTCA Catheters by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 10: World 16-Year Perspective for PTCA Catheters by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 11: World Recent Past, Current & Future Analysis for Other Products by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 12: World Historic Review for Other Products by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 13: World 16-Year Perspective for Other Products by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 14: World Recent Past, Current & Future Analysis for Hospitals by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 15: World Historic Review for Hospitals by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 16: World 16-Year Perspective for Hospitals by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 17: World Recent Past, Current & Future Analysis for Ambulatory Surgery Centers by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 18: World Historic Review for Ambulatory Surgery Centers by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 19: World 16-Year Perspective for Ambulatory Surgery Centers by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

- TABLE 20: World Recent Past, Current & Future Analysis for Catheterization Labs by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 21: World Historic Review for Catheterization Labs by Geographic Region - USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 22: World 16-Year Perspective for Catheterization Labs by Geographic Region - Percentage Breakdown of Value Sales for USA, Canada, Japan, China, Europe, Asia-Pacific and Rest of World for Years 2014, 2024 & 2030

III. MARKET ANALYSIS

- UNITED STATES

- Percutaneous Coronary Intervention (PCI) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in the United States for 2024 (E)

- TABLE 23: USA Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 24: USA Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 25: USA 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 26: USA Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 27: USA Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 28: USA 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- CANADA

- TABLE 29: Canada Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 30: Canada Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 31: Canada 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 32: Canada Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 33: Canada Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 34: Canada 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- JAPAN

- Percutaneous Coronary Intervention (PCI) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in Japan for 2024 (E)

- TABLE 35: Japan Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 36: Japan Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 37: Japan 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 38: Japan Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 39: Japan Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 40: Japan 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- CHINA

- Percutaneous Coronary Intervention (PCI) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in China for 2024 (E)

- TABLE 41: China Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 42: China Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 43: China 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 44: China Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 45: China Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 46: China 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- EUROPE

- Percutaneous Coronary Intervention (PCI) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in Europe for 2024 (E)

- TABLE 47: Europe Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Geographic Region - France, Germany, Italy, UK and Rest of Europe Markets - Independent Analysis of Annual Sales in US$ Million for Years 2023 through 2030 and % CAGR

- TABLE 48: Europe Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Geographic Region - France, Germany, Italy, UK and Rest of Europe Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 49: Europe 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Geographic Region - Percentage Breakdown of Value Sales for France, Germany, Italy, UK and Rest of Europe Markets for Years 2014, 2024 & 2030

- TABLE 50: Europe Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 51: Europe Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 52: Europe 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 53: Europe Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 54: Europe Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 55: Europe 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- FRANCE

- Percutaneous Coronary Intervention (PCI) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in France for 2024 (E)

- TABLE 56: France Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 57: France Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 58: France 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 59: France Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 60: France Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 61: France 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- GERMANY

- Percutaneous Coronary Intervention (PCI) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in Germany for 2024 (E)

- TABLE 62: Germany Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 63: Germany Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 64: Germany 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 65: Germany Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 66: Germany Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 67: Germany 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- ITALY

- TABLE 68: Italy Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 69: Italy Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 70: Italy 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 71: Italy Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 72: Italy Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 73: Italy 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- UNITED KINGDOM

- Percutaneous Coronary Intervention (PCI) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in the United Kingdom for 2024 (E)

- TABLE 74: UK Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 75: UK Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 76: UK 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 77: UK Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 78: UK Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 79: UK 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- REST OF EUROPE

- TABLE 80: Rest of Europe Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 81: Rest of Europe Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 82: Rest of Europe 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 83: Rest of Europe Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 84: Rest of Europe Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 85: Rest of Europe 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- ASIA-PACIFIC

- Percutaneous Coronary Intervention (PCI) Devices Market Presence - Strong/Active/Niche/Trivial - Key Competitors in Asia-Pacific for 2024 (E)

- TABLE 86: Asia-Pacific Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 87: Asia-Pacific Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 88: Asia-Pacific 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 89: Asia-Pacific Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 90: Asia-Pacific Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 91: Asia-Pacific 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030

- REST OF WORLD

- TABLE 92: Rest of World Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 93: Rest of World Historic Review for Percutaneous Coronary Intervention (PCI) Devices by Product - Coronary Stents, PTCA Catheters and Other Products Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 94: Rest of World 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by Product - Percentage Breakdown of Value Sales for Coronary Stents, PTCA Catheters and Other Products for the Years 2014, 2024 & 2030

- TABLE 95: Rest of World Recent Past, Current & Future Analysis for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs - Independent Analysis of Annual Sales in US$ Million for the Years 2023 through 2030 and % CAGR

- TABLE 96: Rest of World Historic Review for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Hospitals, Ambulatory Surgery Centers and Catheterization Labs Markets - Independent Analysis of Annual Sales in US$ Million for Years 2014 through 2022 and % CAGR

- TABLE 97: Rest of World 16-Year Perspective for Percutaneous Coronary Intervention (PCI) Devices by End-Use - Percentage Breakdown of Value Sales for Hospitals, Ambulatory Surgery Centers and Catheterization Labs for the Years 2014, 2024 & 2030