小児インターベンショナル心臓病学の市場機会、成長促進要因、産業動向分析、2025年~2034年予測

Pediatric Interventional Cardiology Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1750432

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

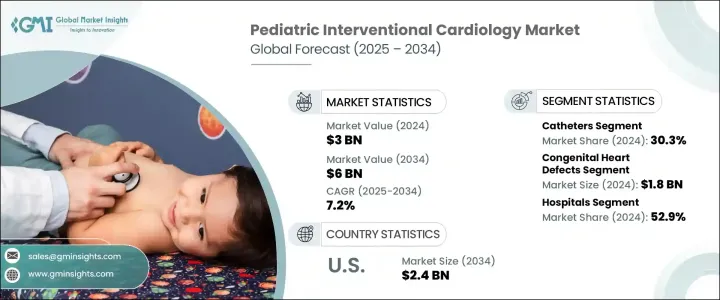

世界の小児インターベンショナル心臓病学市場は、2024年には30億米ドルと評価され、乳幼児の先天性心疾患診断の増加に牽引され、CAGR 7.2%で成長し、2034年には60億米ドルに達すると推定されています。

医療関係者は現在、従来の手術に代わる、より安全で効率的な低侵襲の経カテーテル手技を広く採用しています。こうした最新の技術は、小児患者の生存率の向上と回復の早さに貢献し、市場の拡大を続けています。この分野の技術革新が加速するにつれて、小型化されたツールや高度な画像システムが利用可能になり、医師は合併症の少ない正確で小児に特化した治療を実施できるようになりました。

技術開発は、弁狭窄や中隔奇形といった先天性欠損の治療アプローチを一変させました。侵襲的な開心術に頼るのではなく、ヘルスケアプロバイダーは現在、小児の解剖学的要件に合わせたカテーテルベースの介入を好んでいます。小児患者用に特別に設計された器具は、成人用の器具を適応した場合と比較して、より優れたコントロールが可能であり、手技成績も大幅に改善します。カテーテルは、バルーン血管形成術、弁形成術、欠損部閉鎖術などの手技を、最小限の外傷と迅速な回復時間で行えるように支援するものであり、こうした手技において不可欠なものであることに変わりはないです。優れた生体適合性を備えた、ステアラブルで柔軟性の高いカテーテルのような技術革新が、新生児や乳児のケアにおけるカテーテルの普及を後押ししています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 30億米ドル |

| 予測金額 | 60億米ドル |

| CAGR | 7.2% |

2024年の市場シェアはカテーテル部門が30.3%で首位。次世代小児専用カテーテルに対する需要の高まりが、この優位性を支えています。手術の複雑さを最小限に抑え、入院期間を短縮できることから、これらの器具は引き続き専門医の間で好まれています。これらの器具は、柔軟性が向上し、直径が小さく、生体適合性が強化された設計となっており、新生児や乳児の繊細な血管系をより安全に通過できるようになっています。バルーン弁形成術から欠陥閉鎖術に至るまで、その精度は介入をサポートし、同時に外傷や回復時間を軽減します。

先天性心疾患アプリケーション分野は、強化された新生児スクリーニングツールによる早期かつ正確な診断に支えられて、2024年に18億米ドルを生み出しました。非外科的方法によるタイムリーな介入は乳児の生存率向上に寄与し、カテーテルベースの治療が多くのCHD症例の標準的アプローチとなっています。胎児心エコー検査と出生後診断ツールの進歩により、臨床医はより早く異常を発見できるようになり、多くの場合、乳幼児期の早い段階で処置を計画し実施することが可能になります。

米国小児インターベンショナル心臓病学 2024年の市場規模は12億米ドルで、2034年には24億米ドルに達すると予想されています。米国は、インターベンショナル・カーディオロジー手技を大量に実施する小児専門病院や学術センターの高度なネットワークの恩恵を受けています。メディケイドや民間医療保険を含む包括的な保険適用により、最先端治療へのアクセスが改善され、小児を対象とした心血管治療が世界的に拡大しています。

競合優位性を獲得するため、Abbott Laboratories、Osypka、Cordis、SMT、テルモ、メドトロニック、Lifetech Scientificなどの企業は、小児に特化したインターベンショナルツールを発売するため、研究開発に多額の投資を行っています。主な戦略には、新しいタイプのデバイスの規制当局による承認、国際的な販売提携、小児循環器専門医向けの教育・トレーニングプログラムなどがあります。特注設計のカテーテルシステムと閉鎖器具は主要な重点分野であり、製品ポートフォリオと世界市場へのリーチを強化しています。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 新生児の先天性心疾患の有病率の上昇

- 小児用介入機器の技術的進歩

- 親とヘルスケア従事者の間で高まる意識

- ヘルスケア費の増加と政府の支援策

- 業界の潜在的リスク&課題

- 小児インターベンショナル心臓病学の手順とデバイスの高コスト

- 熟練した専門家の不足

- 促進要因

- 成長可能性分析

- トランプ政権による関税への影響

- 貿易への影響

- 貿易量の混乱

- 報復措置

- 業界への影響

- 供給側の影響(原材料)

- 主要原材料の価格変動

- サプライチェーンの再構築

- 生産コストへの影響

- 需要側の影響(販売価格)

- 最終市場への価格伝達

- 市場シェアの動向

- 消費者の反応パターン

- 供給側の影響(原材料)

- 影響を受ける主要企業

- 戦略的な業界対応

- サプライチェーンの再構成

- 価格設定と製品戦略

- 政策関与

- 展望と今後の検討事項

- 貿易への影響

- テクノロジーの情勢

- 将来の市場動向

- 規制情勢

- 特許分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 競争市場シェア分析

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 戦略的展望マトリックス

第5章 市場推計・予測:製品タイプ別、2021-2034

- 主要動向

- カテーテル

- ステント

- 風船

- バルブ

- 閉鎖装置

- ガイドワイヤー

- その他の製品タイプ

第6章 市場推計・予測:用途別、2021-2034

- 主要動向

- 先天性心疾患

- 不整脈

- 肺動脈狭窄

- 弁膜症

- その他の用途

第7章 市場推計・予測:最終用途別、2021-2034

- 主要動向

- 病院

- 外来手術センター

- 専門クリニック

- 小児心臓病センター

第8章 市場推計・予測:地域別、2021-2034

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- イタリア

- スペイン

- オランダ

- アジア太平洋地域

- 日本

- 中国

- インド

- オーストラリア

- 韓国

- ラテンアメリカ

- メキシコ

- ブラジル

- アルゼンチン

- 中東・アフリカ

- 南アフリカ

- サウジアラビア

- アラブ首長国連邦

第9章 企業プロファイル

- Abbott Laboratories

- B. Braun

- Balton

- Biotronik

- Boston Scientific

- Cordis

- Edwards Lifesciences

- Lepu Medical

- Lifetech Scientific

- Medtronic

- Meril Life Sciences

- Osypka

- Renata Medical

- Terumo

- W. L. Gore &Associates

目次

The Global Pediatric Interventional Cardiology Market was valued at USD 3 billion in 2024 and is estimated to grow at a CAGR of 7.2% to reach USD 6 billion by 2034, driven by the rising diagnoses of congenital heart defects among infants. Medical professionals are now widely adopting minimally invasive transcatheter procedures that offer safer and more efficient alternatives to traditional surgery. These modern techniques contribute to better survival rates and faster recovery for pediatric patients, which continues to expand the market. As innovation in this space accelerates, the availability of miniaturized tools and advanced imaging systems enables physicians to conduct precise and child-specific treatments with fewer complications.

Technological development has transformed the approach to treating congenital defects like valve stenosis and septal malformations. Rather than relying on invasive open-heart procedures, healthcare providers now favor catheter-based interventions tailored to pediatric anatomical requirements. Devices designed specifically for young patients offer better control and significantly improve procedural outcomes compared to adapted adult tools. Catheters remain essential in these interventions, helping clinicians perform tasks such as balloon angioplasty, valvuloplasty, defect closure with minimal trauma and quicker recovery times. Innovations like steerable, highly flexible catheters with superior biocompatibility drive their widespread adoption in neonatal and infant care.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3 Billion |

| Forecast Value | $6 Billion |

| CAGR | 7.2% |

The catheters segment led the market with a 30.3% share in 2024. Increasing demand for next-generation pediatric-specific catheters supports this dominance. The ability to minimize surgical complexity and shorten hospital stays continues to make these tools a preferred choice among specialists. These devices are designed with improved flexibility, smaller diameters, and enhanced biocompatibility, allowing safer navigation through delicate vascular systems in neonates and infants. Their precision supports interventions, from balloon valvuloplasty to defect closures, all while reducing trauma and recovery time.

The congenital heart defects application segment generated USD 1.8 billion in 2024, supported by earlier and more accurate diagnosis through enhanced neonatal screening tools. Timely intervention through non-surgical methods contributes to improved infant survival, making catheter-based treatments the standard approach for many CHD cases. Advancements in fetal echocardiography and postnatal diagnostic tools allow clinicians to detect abnormalities sooner, often enabling procedures to be planned and performed in early infancy.

U.S. Pediatric Interventional Cardiology Market stood at USD 1.2 billion in 2024 and is expected to reach USD 2.4 billion by 2034. The U.S. benefits from an advanced network of pediatric specialty hospitals and academic centers that conduct high volumes of interventional cardiology procedures. Comprehensive insurance coverage, including Medicaid and private health plans, improves access to cutting-edge treatments and expands the reach of pediatric-focused cardiovascular services globally.

To gain a competitive edge, companies like Abbott Laboratories, Osypka, Cordis, SMT, Terumo, Medtronic, and Lifetech Scientific are investing heavily in R&D to launch pediatric-specific interventional tools. Key strategies include regulatory approvals for new device types, international distribution partnerships, and education & training programs for pediatric cardiologists. Custom-designed catheter systems and closure devices are a major focus area, enhancing product portfolios and market reach globally.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising prevalence of congenital heart defects in newborns

- 3.2.1.2 Technological advancements in pediatric-sized interventional devices

- 3.2.1.3 Growing awareness among parents and healthcare providers

- 3.2.1.4 Increasing healthcare spending and supportive government initiatives

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of pediatric interventional cardiology procedures and devices

- 3.2.2.2 Limited availability of skilled professionals

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures

- 3.4.2 Impact on the Industry

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.2.1.1 Price volatility in key materials

- 3.4.2.1.2 Supply chain restructuring

- 3.4.2.1.3 Production cost implications

- 3.4.2.2 Demand-side impact (selling price)

- 3.4.2.2.1 Price transmission to end markets

- 3.4.2.2.2 Market share dynamics

- 3.4.2.2.3 Consumer response patterns

- 3.4.2.1 Supply-side impact (raw materials)

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.4.3 Policy engagement

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Regulatory landscape

- 3.8 Patent analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Competitive market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategic outlook matrix

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Catheters

- 5.3 Stents

- 5.4 Balloons

- 5.5 Valves

- 5.6 Closure devices

- 5.7 Guidewires

- 5.8 Other product types

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Congenital heart defects

- 6.3 Arrhythmias

- 6.4 Pulmonary artery stenosis

- 6.5 Valvular heart disease

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgical centers

- 7.4 Specialty clinics

- 7.5 Pediatric cardiology centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 Japan

- 8.4.2 China

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Mexico

- 8.5.2 Brazil

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 B. Braun

- 9.3 Balton

- 9.4 Biotronik

- 9.5 Boston Scientific

- 9.6 Cordis

- 9.7 Edwards Lifesciences

- 9.8 Lepu Medical

- 9.9 Lifetech Scientific

- 9.10 Medtronic

- 9.11 Meril Life Sciences

- 9.12 Osypka

- 9.13 Renata Medical

- 9.14 Terumo

- 9.15 W. L. Gore & Associates

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日