|

市場調査レポート

商品コード

1716617

商用給湯器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測Commercial Water Heater Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

カスタマイズ可能

|

|||||||

| 商用給湯器市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測 |

|

出版日: 2025年03月06日

発行: Global Market Insights Inc.

ページ情報: 英文 120 Pages

納期: 2~3営業日

|

全表示

- 概要

- 目次

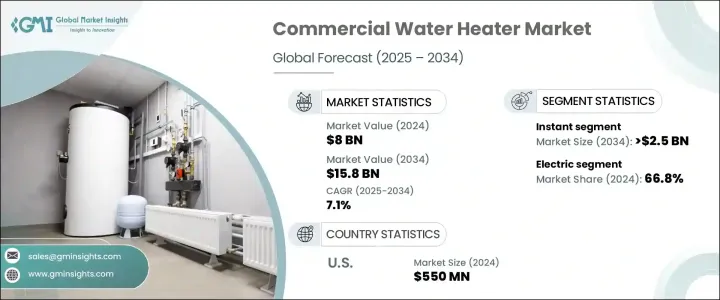

世界の商用給湯器市場は2024年に80億米ドルに達し、2025年から2034年にかけてCAGR 7.1%で成長すると推定されています。

この業界は、ホスピタリティ、ヘルスケア、教育、商業セクターの企業が、エネルギー効率が高く、持続可能で、技術的に高度な給湯ソリューションをますます求めるようになり、勢いを増しています。都市化やインフラ開発の進展と相まって、二酸化炭素排出量の削減が重視されるようになり、現代の要件を満たす効率的な給湯システムへのニーズがさらに高まっています。高度な給湯器に関連するエネルギー消費、コスト削減、環境上の利点に対する消費者の意識の高まりが、市場動向を大きく形成しています。

さらに、世界各国の政府は、高効率で再生可能エネルギーが統合された給湯システムの採用を支援する有利な規制枠組みやインセンティブを導入しています。スマート技術統合への注目が高まる中、IoT、遠隔監視、自動化機能を備えた商用給湯器も大きな支持を得ており、エンドユーザーのエネルギー使用と業務効率の最適化を支援しています。このようなインテリジェントで環境に優しいシステムに対する需要の高まりは、商業施設の進化するニーズに合わせたソリューションを革新し提供するメーカーに新たな道を開いています。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 80億米ドル |

| 予測金額 | 158億米ドル |

| CAGR | 7.1% |

市場はヒータータイプ、エネルギー源、デザインによって細分化され、幅広い商業用途に対応しています。その中でも、瞬間湯沸かし器分野は目覚ましい成長を遂げ、2034年までに25億米ドルを生み出すと予測されています。コンパクトな設計と急速加熱能力で知られる瞬間湯沸かし器は、使用箇所の近くに設置できるよう設計されており、大規模な配管の必要性を減らし、熱損失を最小限に抑えます。省スペースであるため、ホテル、オフィス、レストランなど、限られたスペースしかない商業施設にとって理想的なソリューションとなっています。商業施設がエネルギー効率を優先し、運営コストの削減を求める中、瞬間湯沸かし器の需要は増加の一途をたどっており、市場で最も急成長しているカテゴリーの一つとなっています。

商用給湯器業界はエネルギー源によっても分類され、主に電気ヒーターとガスヒーターに分けられます。電気温水器は、その信頼性、耐久性、太陽光発電のような新たな再生可能エネルギー源との互換性により、2024年には66.8%のシェアで市場を独占しました。これらのユニットは、長期的な性能を確保しつつ、業務用の過酷な使用にも対応できるよう堅牢な部品で設計されています。持続可能性の目標が組織にクリーンな代替エネルギーを求めるよう促す中、電気およびハイブリッド・ソリューションへの移行が加速しています。メーカー各社は、エネルギー規制の強化に準拠した高効率モデルの革新に注力しており、商業団体が厳しい環境・エネルギー規範を満たすのに役立っています。

北米の商用給湯器市場は、厳格なエネルギー効率の義務と環境に優しい給湯システムのインストールを奨励する魅力的な政府のインセンティブに支えられ、2024年に5億5,000万米ドルと13%のシェアを占めました。LEED(エネルギーと環境設計におけるリーダーシップ)認証を目指す商業施設が増える中、エネルギー効率の高い給湯器は、グリーンビルディング基準を達成し、長期的なエネルギーコストを削減するための重要な要素となっています。

目次

第1章 調査手法と調査範囲

第2章 エグゼクティブサマリー

第3章 業界洞察

- 業界エコシステム

- 規制状況

- 業界への影響要因

- 促進要因

- 業界の潜在的リスク&課題

- 成長ポテンシャル分析

- 価格動向分析

- ポーター分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 戦略ダッシュボード

- イノベーションとテクノロジーの展望

第5章 市場規模・予測:製品別、2021年~2034年

- 主要動向

- 瞬間

- 貯湯

第6章 市場規模・予測:エネルギー源別、2021年~2034年

- 主要動向

- 電気

- ガス

第7章 市場規模・予測:容量別、2021年~2034年

- 主要動向

- 30リットル未満

- 30-100リットル

- 100-250リットル

- 250-400リットル

- 400リットル以上

第8章 市場規模・予測:用途別、2021年~2034年

- 主要動向

- 大学

- オフィス

- 政府/軍

- その他

第9章 市場規模・予測:チャネル別、2021年~2034年

- 主要動向

- オンライン

- ディーラー

- 小売

第10章 市場規模・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- 英国

- フランス

- ドイツ

- イタリア

- スペイン

- オランダ

- ポルトガル

- ルーマニア

- スイス

- アジア太平洋

- 中国

- 日本

- インド

- オーストラリア

- 韓国

- 中東・アフリカ

- サウジアラビア

- アラブ首長国連邦

- 南アフリカ

- エジプト

- ラテンアメリカ

- ブラジル

- アルゼンチン

第11章 企業プロファイル

- American Standard Water Heaters

- A.O Smith

- AQUAMAX Australia

- Bosch Thermotechnology

- Bradford White Corporation

- BDR Thermea Group

- GE Appliances

- Heatre Sadia

- HTP

- ORBITAL HORIZON

- Powrmatic

- Racold

- Rinnai Corporation

- Rheem Manufacturing Company

- STIEBEL ELTRON GmbH &Co. KG

- State Industries

- Saudi Ceramic Company

- Toshiba Corporation

- Westinghouse Electric Corporation

The Global Commercial Water Heater Market reached USD 8 billion in 2024 and is estimated to grow at a CAGR of 7.1% between 2025 and 2034. The industry is gaining momentum as businesses across hospitality, healthcare, education, and commercial sectors increasingly demand energy-efficient, sustainable, and technologically advanced water heating solutions. The rising emphasis on reducing carbon footprints, coupled with growing urbanization and infrastructural developments, is further fueling the need for efficient water heating systems that meet modern-day requirements. Heightened consumer awareness of energy consumption, cost savings, and environmental benefits associated with advanced water heaters is significantly shaping market trends.

Moreover, governments worldwide are introducing favorable regulatory frameworks and incentives that support the adoption of high-efficiency and renewable energy-integrated water heating systems. As the focus on smart technology integration grows, commercial water heaters equipped with IoT, remote monitoring, and automation features are also gaining considerable traction, helping end-users optimize energy use and operational efficiency. This increasing demand for intelligent and eco-friendly systems is opening new avenues for manufacturers to innovate and deliver solutions tailored to the evolving needs of commercial establishments.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8 Billion |

| Forecast Value | $15.8 Billion |

| CAGR | 7.1% |

The market is segmented based on heater type, energy source, and design, catering to a broad range of commercial applications. Among these, the instant water heater segment is poised for remarkable growth and is projected to generate USD 2.5 billion by 2034. Instant water heaters, known for their compact design and rapid heating capability, are engineered to be installed close to points of use, reducing the need for extensive piping and minimizing heat loss. Their space-saving nature makes them an ideal solution for commercial buildings with limited space, such as hotels, offices, and restaurants. As commercial facilities prioritize energy efficiency and seek to lower operational costs, the demand for instant water heaters continues to rise, making them one of the fastest-growing categories in the market.

The commercial water heater industry is also classified by energy source, primarily into electric and gas heaters. Electric water heaters dominated the market with a 66.8% share in 2024, driven by their reliability, durability, and compatibility with emerging renewable energy sources like solar power. These units are designed with robust components to handle heavy-duty commercial usage while ensuring long-term performance. As sustainability goals push organizations to seek cleaner energy alternatives, the transition towards electric and hybrid solutions is accelerating. Manufacturers are focusing on innovating high-efficiency models that comply with tightening energy regulations, helping commercial entities meet stringent environmental and energy codes.

North America commercial water heater market accounted for USD 550 million and a 13% share in 2024, supported by strict energy efficiency mandates and attractive government incentives that encourage the installation of eco-friendly water heating systems. With more commercial properties aiming for LEED (Leadership in Energy and Environmental Design) certification, energy-efficient water heaters have become a critical component for achieving green building standards and reducing long-term energy costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Base estimates & calculations

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 – 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Price trend analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Innovation & technology landscape

Chapter 5 Market Size and Forecast, By Product, 2021 – 2034 (USD Million & ‘000 Units)

- 5.1 Key trends

- 5.2 Instant

- 5.3 Storage

Chapter 6 Market Size and Forecast, By Energy Source, 2021 – 2034 (USD Million & ‘000 Units)

- 6.1 Key trends

- 6.2 Electric

- 6.3 Gas

Chapter 7 Market Size and Forecast, By Capacity, 2021 – 2034 (USD Million & ‘000 Units)

- 7.1 Key trends

- 7.2 <30 liters

- 7.3 30-100 liters

- 7.4 100-250 liters

- 7.5 250-400 liters

- 7.6 >400 liters

Chapter 8 Market Size and Forecast, By Application, 2021 – 2034 (USD Million & ‘000 Units)

- 8.1 Key trends

- 8.2 College/University

- 8.3 Offices

- 8.4 Government/Military

- 8.5 Others

Chapter 9 Market Size and Forecast, By Channel, 2021 – 2034 (USD Million & ‘000 Units)

- 9.1 Key trends

- 9.2 Online

- 9.3 Dealer

- 9.4 Retail

Chapter 10 Market Size and Forecast, By Region, 2021 – 2034 (USD Million & ‘000 Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 France

- 10.3.3 Germany

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.3.7 Portugal

- 10.3.8 Romania

- 10.3.9 Switzerland

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 South Africa

- 10.5.4 Egypt

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

Chapter 11 Company Profiles

- 11.1 American Standard Water Heaters

- 11.2 A.O Smith

- 11.3 AQUAMAX Australia

- 11.4 Bosch Thermotechnology

- 11.5 Bradford White Corporation

- 11.6 BDR Thermea Group

- 11.7 GE Appliances

- 11.8 Heatre Sadia

- 11.9 HTP

- 11.10 ORBITAL HORIZON

- 11.11 Powrmatic

- 11.12 Racold

- 11.13 Rinnai Corporation

- 11.14 Rheem Manufacturing Company

- 11.15 STIEBEL ELTRON GmbH & Co. KG

- 11.16 State Industries

- 11.17 Saudi Ceramic Company

- 11.18 Toshiba Corporation

- 11.19 Westinghouse Electric Corporation