自動乳房超音波システム市場の機会、成長促進要因、産業動向分析、2025年~2034年の予測

Automated Breast Ultrasound Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034

- 発行日

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日

- 商品コード

- 1801949

- カスタマイズ可能 お客様のご希望に応じて、既存データの加工や未掲載情報(例:国別セグメント)の追加などの対応が可能です。詳細はお問い合わせください。

- 翻訳ツール提供対象 PDF対応AI翻訳ツールの無料貸し出しサービスのご利用が可能です

概要

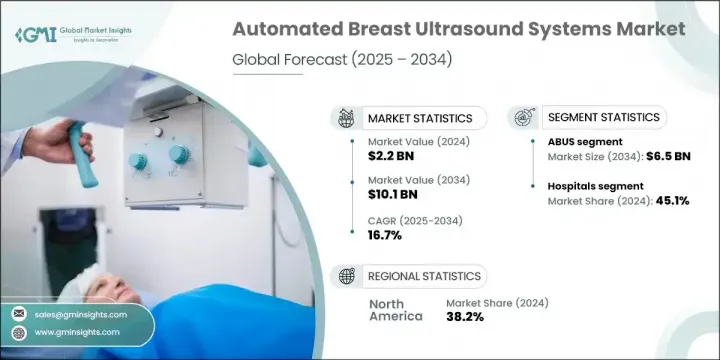

自動乳房超音波システムの世界市場は、2024年には22億米ドルと評価され、CAGR 16.7%で成長し、2034年には101億米ドルに達すると推定されています。

世界の乳がん罹患率の上昇、早期発見の重要性の高まり、公衆衛生に対する強い意識、政府による検診イニシアチブは、この市場を前進させる中核的な要因の一つです。医療画像と診断技術の急速な進歩により、自動乳房超音波システムは乳がん検診の必須ツールとして、特に乳腺組織の密度が高い女性の間で浸透しつつあります。

自動乳房超音波システム(ABUS)は、乳房全体の高度な3D可視化を提供し、オペレーターの技量に大きく依存することなく、一貫性のある標準化された画像診断を提供します。検出精度を高めることができるため、病院、画像診断センター、乳腺専門医療施設での導入が急速に進んでいます。組織層全体にわたって高解像度の画像を撮影することで、これらのシステムは早期診断をサポートし、患者の転帰を改善します。医療機関が早期がんの特定を優先し続ける中、ABUSを他の画像診断法と統合することの重要性はさらに高まっています。高濃度乳房検診とAIを活用した診断への注目は、世界の需要と普及の原動力になると予想されます。

| 市場範囲 | |

|---|---|

| 開始年 | 2024 |

| 予測年 | 2025-2034 |

| 開始金額 | 22億米ドル |

| 予測金額 | 101億米ドル |

| CAGR | 16.7% |

2024年、ABUSカテゴリーは14億米ドルで最大の市場価値を占め、2034年には65億米ドルに達し、CAGR 16.9%で成長します。同市場におけるABUSのリーダーシップは、AIを活用した診断に対する需要の増加、乳がんリスクに対する幅広い認識、徹底的なスクリーニングと詳細な分析を目的としたヘルスケア環境全体におけるこれらのシステムの使用の拡大に起因しています。ABUSは完全な3D乳房画像を提供し、放射線科医が従来のマンモグラフィでは気づかなかった異常箇所を特定できるようにします。鮮明度が高いため人為的ミスが少なく、標準化されているため、乳腺が密集している患者の乳がん発見において重要な資産となっています。

病院部門は2024年に45.1%のシェアを占めました。これらの施設は高度な診断技術を備え、熟練した専門家を利用できるため、ABUSの主要な導入施設となっています。がん検診、診断、治療の中心的な拠点である病院は患者数が多く、公的検診プログラムの恩恵を受けているため、自動超音波診断装置の使用はさらに促進されます。ABUSをより広範な診断ワークフローに組み込むことで、ヘルスケアプロバイダーはより完全で効率的な乳房ケアサービスを提供できるようになります。

米国の自動乳房超音波システム市場は2024年に7億5,830万米ドルに達しました。この成長は、全米で乳がん罹患率が増加していることと密接に関連しており、精密な早期診断ツールの需要が急増しています。米国のヘルスケア・エコシステムはまた、良好な規制環境、がん検診に関する普及教育、医療技術革新への強力な投資からも恩恵を受けています。これらの要因はABUSの採用と継続的な市場拡大のための強固な基盤となっています。

自動乳房超音波システムの世界市場で活躍する主要企業には、シーメンス・ヘルティニアーズ、SonoCine, Inc.、キヤノン、GEヘルスケア、リアルイメージング、Seno Medical Instruments Inc.、ホロジック、スーパーソニック・イマジン、Shantou Institute of Ultrasonic Instruments、セラクリオン、メトリトラック、QView Medical、デルフィナス・メディカル・テクノロジーズ、Koninklijke Philips、CapeRay Medical、日立などがあります。自動乳房超音波システム市場で事業を展開する企業は、技術革新、世界展開、協業パートナーシップの組み合わせを通じて存在感を強めています。大手企業は、画質の向上、スキャン時間の短縮、AIベースの解釈ツールの統合のための研究開発に多額の投資を行っています。先進国市場と新興国市場の両方で高まる需要に対応するため、メーカーは販売網を拡大し、病院や診断チェーンとの戦略的提携を進めています。多くの企業は、特に高負担地域における製品展開を加速するため、より迅速な規制当局の承認取得に取り組んでいます。

目次

第1章 調査手法と範囲

第2章 エグゼクティブサマリー

第3章 業界考察

- エコシステム分析

- 業界への影響要因

- 促進要因

- 世界中で乳がんの罹患率が増加

- 自動乳房超音波システムにおける技術進歩の高まり

- 高濃度乳房組織患者におけるマンモグラフィーの能力の限界

- 乳がんに関する意識の高まりと政府の好ましい取り組み

- 世界中で乳がん検診プログラムが増加

- 米国における乳房超音波検査とデジタル乳房トモシンセシスの償還額増加

- 業界の潜在的リスク&課題

- 自動乳房超音波システムの高コスト

- 新興諸国におけるABUSの認知度が低い

- 新興国における熟練した人材や訓練を受けた人材の不足

- 市場機会

- 乳がんの予測スクリーニングにおけるAI統合ABUSの導入増加

- 促進要因

- 成長可能性分析

- 規制情勢

- 技術的進歩

- 現在の技術動向

- 新興技術

- サプライチェーン分析

- 価格分析、2024

- 将来の市場動向

- ギャップ分析

- ポーターの分析

- PESTEL分析

第4章 競合情勢

- イントロダクション

- 企業の市場シェア分析

- 北米

- 欧州

- アジア太平洋地域

- 企業マトリックス分析

- 主要市場企業の競合分析

- 競合ポジショニングマトリックス

- 主な発展

- 合併と買収

- パートナーシップとコラボレーション

- 新製品の発売

- 拡張計画

第5章 市場推計・予測:製品別、2021年~2034年

- 主要動向

- 自動乳房超音波システム(ABUS)

- 自動乳房ボリュームスキャナ(ABVS)

- その他の製品

第6章 市場推計・予測:最終用途別、2021年~2034年

- 主要動向

- 病院

- 画像診断センター

- 専門クリニック

第7章 市場推計・予測:地域別、2021年~2034年

- 主要動向

- 北米

- 米国

- カナダ

- 欧州

- ドイツ

- 英国

- フランス

- スペイン

- イタリア

- オランダ

- アジア太平洋地域

- 中国

- インド

- 日本

- オーストラリア

- 韓国

- ラテンアメリカ

- ブラジル

- メキシコ

- アルゼンチン

- 中東・アフリカ

- サウジアラビア

- 南アフリカ

- アラブ首長国連邦

第8章 企業プロファイル

- Canon

- CapeRay Medical

- Delphinus Medical Technologies

- GE Healthcare

- Hitachi

- Hologic

- Koninklijke Philips

- Metritrack

- QView Medical

- Real Imaging

- SonoCine, Inc.

- Supersonic Imagine

- Siemens Healthineers

- Seno Medical Instruments Inc.

- Shantou Institute of Ultrasonic Instruments

- Theraclion

目次

The Global Automated Breast Ultrasound Systems Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 16.7% to reach USD 10.1 billion by 2034. Rising breast cancer rates across the globe, growing emphasis on early detection, strong public health awareness, and government-backed screening initiatives are among the core factors driving this market forward. With rapid advances in medical imaging and diagnostic technology, automated breast ultrasound systems are gaining ground as essential tools in breast cancer screening, especially among women with dense breast tissue.

Automated breast ultrasound systems, or ABUS, offer advanced 3D visualization of the entire breast, providing consistent and standardized imaging without relying heavily on the skill of the operator. Their implementation is rapidly increasing in hospitals, imaging centers, and specialized breast care facilities due to their ability to enhance detection accuracy. By capturing high-resolution images across tissue layers, these systems support early diagnosis and improve patient outcomes. As health organizations continue prioritizing early-stage cancer identification, the integration of ABUS alongside other imaging methods becomes even more important. The focus on dense breast screening and AI-enhanced diagnostics is expected to drive demand and adoption worldwide.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $10.1 Billion |

| CAGR | 16.7% |

In 2024, the ABUS category held the largest market value at USD 1.4 billion and will reach USD 6.5 billion by 2034, growing at a CAGR of 16.9%. Its leadership in the market stems from increasing demand for AI-powered diagnostics, wider awareness of breast cancer risks, and the growing use of these systems across healthcare environments for thorough screening and detailed analysis. ABUS delivers full 3D breast imaging, enabling radiologists to identify abnormalities that may go unnoticed with conventional mammography. Its high clarity reduced human error, and standardization has made it a key asset in breast cancer detection for patients with dense breast composition.

The hospitals segment held a 45.1% share in 2024. These facilities are equipped with advanced diagnostic technology and have access to skilled professionals, making them leading adopters of ABUS. As central hubs for cancer screening, diagnosis, and treatment, hospitals handle high patient volumes and benefit from public health screening programs, further promoting the use of automated ultrasound systems. The integration of ABUS into broader diagnostic workflows allows healthcare providers to offer more complete and efficient breast care services.

United States Automated Breast Ultrasound Systems Market reached USD 758.3 million in 2024. This growth is closely tied to the increasing incidence of breast cancer across the country, which has led to a surge in demand for precise, early-stage diagnostic tools. The U.S. healthcare ecosystem also benefits from a favorable regulatory environment, widespread public education on cancer screening, and strong investments in medical technology innovation. These factors create a solid foundation for ABUS adoption and continued market expansion.

Key companies active in the Global Automated Breast Ultrasound Systems Market include Siemens Healthineers, SonoCine, Inc., Canon, GE Healthcare, Real Imaging, Seno Medical Instruments Inc., Hologic, Supersonic Imagine, Shantou Institute of Ultrasonic Instruments, Theraclion, Metritrack, QView Medical, Delphinus Medical Technologies, Koninklijke Philips, CapeRay Medical, and Hitachi. Companies operating in the automated breast ultrasound systems market are strengthening their presence through a combination of innovation, global expansion, and collaborative partnerships. Leading players are heavily investing in R&D to enhance image quality, reduce scan time, and integrate AI-based interpretation tools. To meet increasing demand in both developed and emerging markets, manufacturers are expanding their distribution networks and entering strategic alliances with hospitals and diagnostic chains. Many firms are working on gaining faster regulatory approvals to accelerate product rollouts, especially in high-burden regions.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of breast cancer worldwide

- 3.2.1.2 Rising technological advancements in automated breast ultrasound systems

- 3.2.1.3 Limited capability of mammography in dense breast tissue patients

- 3.2.1.4 Rising awareness and favorable government initiatives regarding breast cancer

- 3.2.1.5 Increasing national breast screening programs across the globe

- 3.2.1.6 Increased reimbursement for breast ultrasound and digital breast tomosynthesis in the U.S.

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of the automated breast ultrasound system

- 3.2.2.2 Limited awareness of ABUS in developing countries

- 3.2.2.3 Lack of skilled or trained personnel in emerging nations

- 3.2.3 Market opportunities

- 3.2.3.1 Rising adoption of AI-integrated ABUS for predictive breast cancer screening

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Pricing analysis, 2024

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Automated breast ultrasound system (ABUS)

- 5.3 Automated breast volume scanner (ABVS)

- 5.4 Other products

Chapter 6 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Hospitals

- 6.3 Diagnostic imaging centers

- 6.4 Specialty clinics

Chapter 7 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.3.6 Netherlands

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.5.3 Argentina

- 7.6 Middle East and Africa

- 7.6.1 Saudi Arabia

- 7.6.2 South Africa

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 Canon

- 8.2 CapeRay Medical

- 8.3 Delphinus Medical Technologies

- 8.4 GE Healthcare

- 8.5 Hitachi

- 8.6 Hologic

- 8.7 Koninklijke Philips

- 8.8 Metritrack

- 8.9 QView Medical

- 8.10 Real Imaging

- 8.11 SonoCine, Inc.

- 8.12 Supersonic Imagine

- 8.13 Siemens Healthineers

- 8.14 Seno Medical Instruments Inc.

- 8.15 Shantou Institute of Ultrasonic Instruments

- 8.16 Theraclion

- 発行日

- 発行

- Global Market Insights Inc.

- ページ情報

- 英文 120 Pages

- 納期

- 2~3営業日